Port Infrastructure Market Size and Growth Forecast 2026-2030

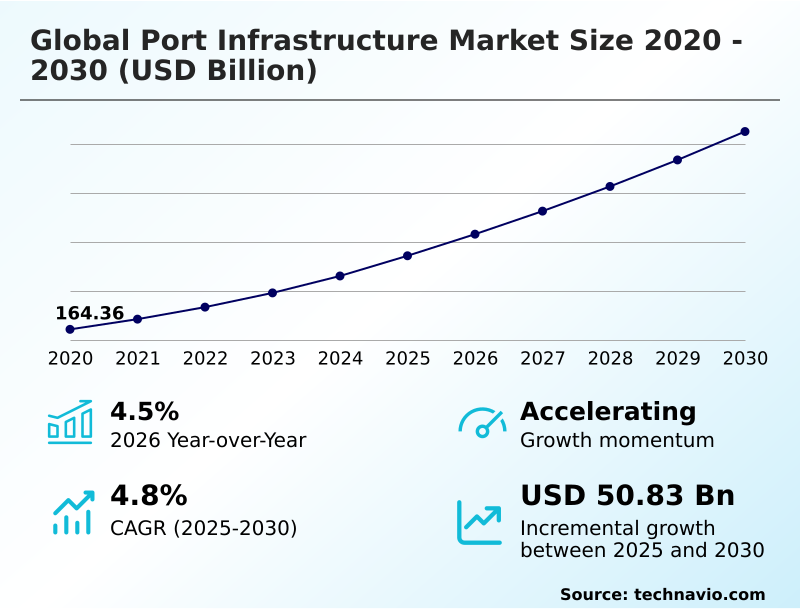

The Port Infrastructure Market size was valued at USD 194.46 billion in 2025 growing at a CAGR of 4.8% during the forecast period 2026-2030.

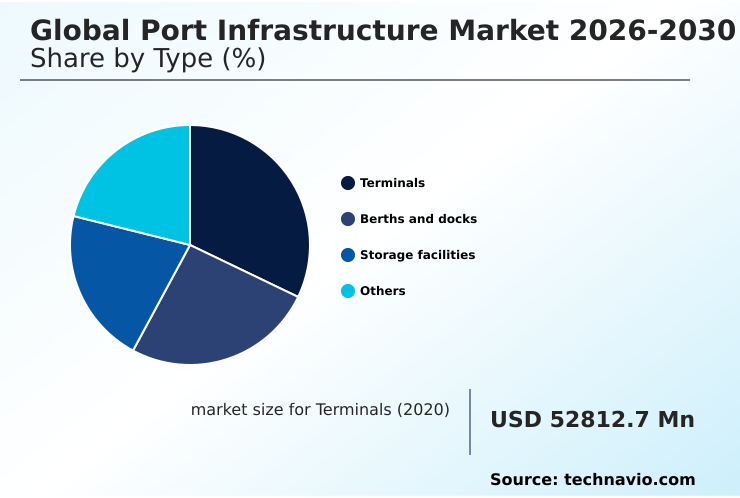

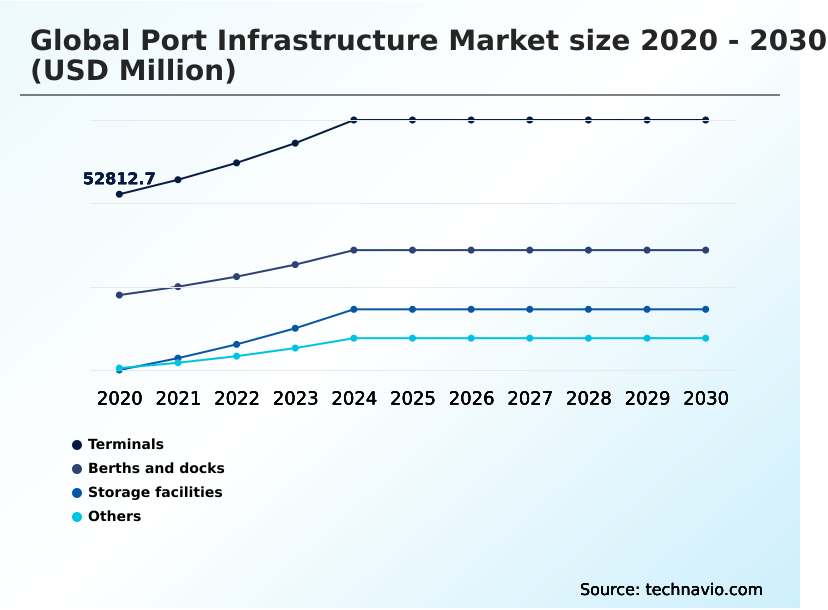

APAC accounts for 32.9% of incremental growth during the forecast period. The Terminals segment by Type was valued at USD 60.54 billion in 2024, while the Seaports segment holds the largest revenue share by End-user.

The market is projected to grow by USD 80.94 billion from 2020 to 2030, with USD 50.83 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Port Infrastructure Market Overview

The port infrastructure market is defined by continuous modernization to support maritime trade facilitation. Growth, which saw a 4.5% year-over-year increase, is propelled by the need for greater efficiency in container terminal optimization and bulk handling capabilities. A key dynamic is the integration of digital logistics platforms and smart port technologies to improve cargo fluidity. For instance, a container terminal deploying automated guided vehicles and a new terminal operating system can reduce vessel turnaround times by up to 20%, directly impacting supply chain costs. With APAC contributing 32.9% of the market's incremental growth, development is concentrated in regions supporting high-volume manufacturing and trade. This investment cycle focuses on expanding deepwater capabilities and enhancing intermodal transport corridors to manage the relentless flow of global commerce, making resilient port infrastructure a critical economic asset.

Drivers, Trends, and Challenges in the Port Infrastructure Market

Strategic decisions in the port infrastructure market are increasingly shaped by long-term resilience and sustainability mandates. The development of infrastructure for ultra large container vessels is no longer just about capacity but also about integrating climate adaptation for coastal infrastructure, a crucial consideration for facilities facing rising sea levels.

For example, a terminal operator evaluating a major expansion must balance the need for deeper channels and stronger quays with the implementation of green technologies.

A key differentiator is the adoption of shore power infrastructure for emissions reduction, which is vital for compliance with MARPOL Annex VI regulations and can cut a docked vessel's emissions by over 90% compared to running auxiliary engines. Concurrently, investments in inland port development for supply chain resilience are critical for mitigating coastal congestion.

However, this increased connectivity introduces new risks, making robust cybersecurity for automated port systems a non-negotiable component of any modernization project to protect against operational paralysis.

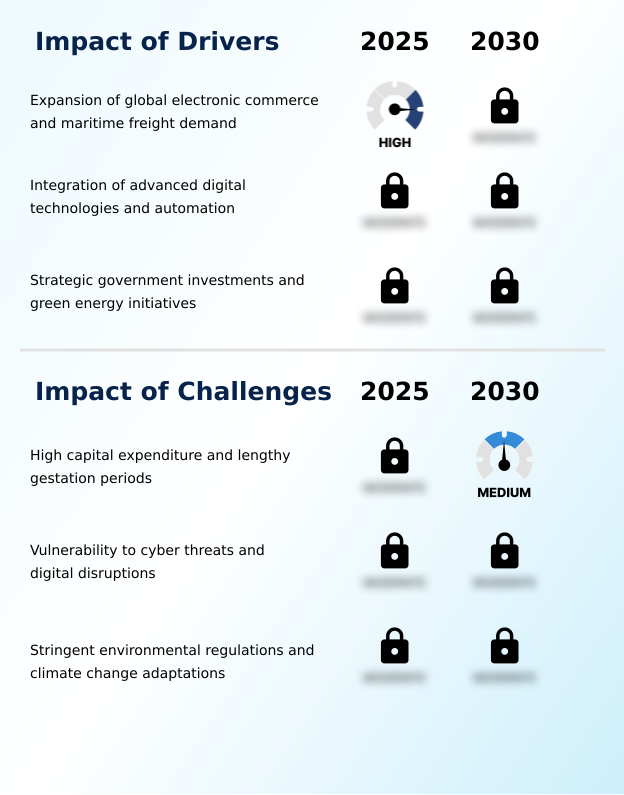

Primary Growth Driver: The expansion of global electronic commerce and the corresponding rise in maritime freight demand serve as a primary catalyst for port infrastructure development.

Market expansion is propelled by the integration of digital technologies and a global push for sustainability, reflected in the market's 4.5% year-over-year growth.

The adoption of smart port technologies, including advanced terminal operating systems and predictive maintenance protocols, is creating more efficient and resilient automated terminal solutions. This digital transformation enables higher cargo throughput velocity and optimized vessel traffic management.

Simultaneously, strategic green port initiatives are a powerful driver, with governments mandating eco-friendly operational models.

This compels investment in infrastructure like cold ironing systems and facilities to support offshore wind energy projects, aligning economic development with environmental sustainability goals and ensuring long-term opportunities for market participants.

Emerging Market Trend: A primary trend is the adaptation of port infrastructure to support supply chain diversification and nearshoring, fundamentally altering capital expenditure priorities.

Key trends are reshaping capital investment priorities, driven by shifts in global trade patterns and vessel technology. The move toward supply chain diversification is fueling nearshoring infrastructure adaptation, particularly in North America and Southeast Asia, requiring more flexible terminals.

Concurrently, the deployment of ultra large container vessels necessitates massive physical upgrades, including the expansion of deepwater capabilities and reinforcement of quay walls, a trend driving over 4% growth in related construction activities. Another critical trajectory is the enhancement of hinterland connectivity through on-dock rail facilities and expanded intermodal logistics networks.

This focus on cargo fluidity beyond the terminal gate is essential for alleviating bottlenecks and improving the efficiency of the entire maritime logistics network.

Key Industry Challenge: The port infrastructure industry is constrained by the high capital expenditure and lengthy gestation periods required for new development and modernization projects.

Significant constraints hinder development, primarily the massive capital expenditure and long project timelines associated with deep water dredging and land reclamation. These financial hurdles are compounded by stringent environmental regulations, such as those mandated by the International Maritime Organization, which can delay or halt projects to protect marine ecosystems.

Furthermore, the increasing digitalization of ports creates a substantial challenge related to cybersecurity for automated port systems, where a single breach can cause catastrophic disruptions. Terminal operators must also invest heavily in climate adaptation for coastal infrastructure, reinforcing breakwaters and elevating quay walls to protect against rising sea levels and extreme weather, straining financial resources and complicating long-term planning.

Explore Full Market Dynamics Analysis Request Free Sample

Port Infrastructure Market Segmentation

The port infrastructure industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Type Segment Analysis

The terminals segment is estimated to witness significant growth during the forecast period.

Terminals represent the primary segment, driven by the need to enhance cargo throughput and accommodate larger vessels. Modernization efforts focus on integrating sophisticated terminal operating systems and deploying advanced gantry equipment and automated stacking cranes to optimize space and speed.

This includes extensive quay wall reinforcement to support heavier loads and the development of specialized facilities like liquid bulk terminals and dry ports.

Operational efficiency within these zones is paramount, with investments in robotic container handlers and other automated terminal solutions becoming standard.

As the largest segment, terminals captured over 32% of the market in the base year, reflecting sustained capital expenditure in both greenfield projects and the retrofitting of existing assets to meet evolving maritime logistics demands.

The Terminals segment was valued at USD 60.54 billion in 2024 and showed a gradual increase during the forecast period.

Port Infrastructure Market by Region: APAC Leads with 32.9% Growth Share

APAC is estimated to contribute 32.9% to the growth of the global market during the forecast period.

The geographic landscape is dominated by APAC, which accounts for 32.9% of incremental growth, driven by its central role in global manufacturing and the presence of numerous high-volume transshipment hub operations.

Countries like China and Japan are investing heavily in automated terminal solutions and expanding their maritime logistics networks. In contrast, North America is focused on enhancing hinterland connectivity through intermodal transport corridors and on-dock rail facilities to alleviate congestion.

Europe leads in sustainable maritime operations, with significant investment in green port initiatives.

The development of deepwater capabilities remains a global priority, ensuring ports can service the largest vessels and maintain competitiveness in international trade routes, thereby reinforcing the strategic importance of regional infrastructure investment.

Customer Landscape Analysis for the Port Infrastructure Market

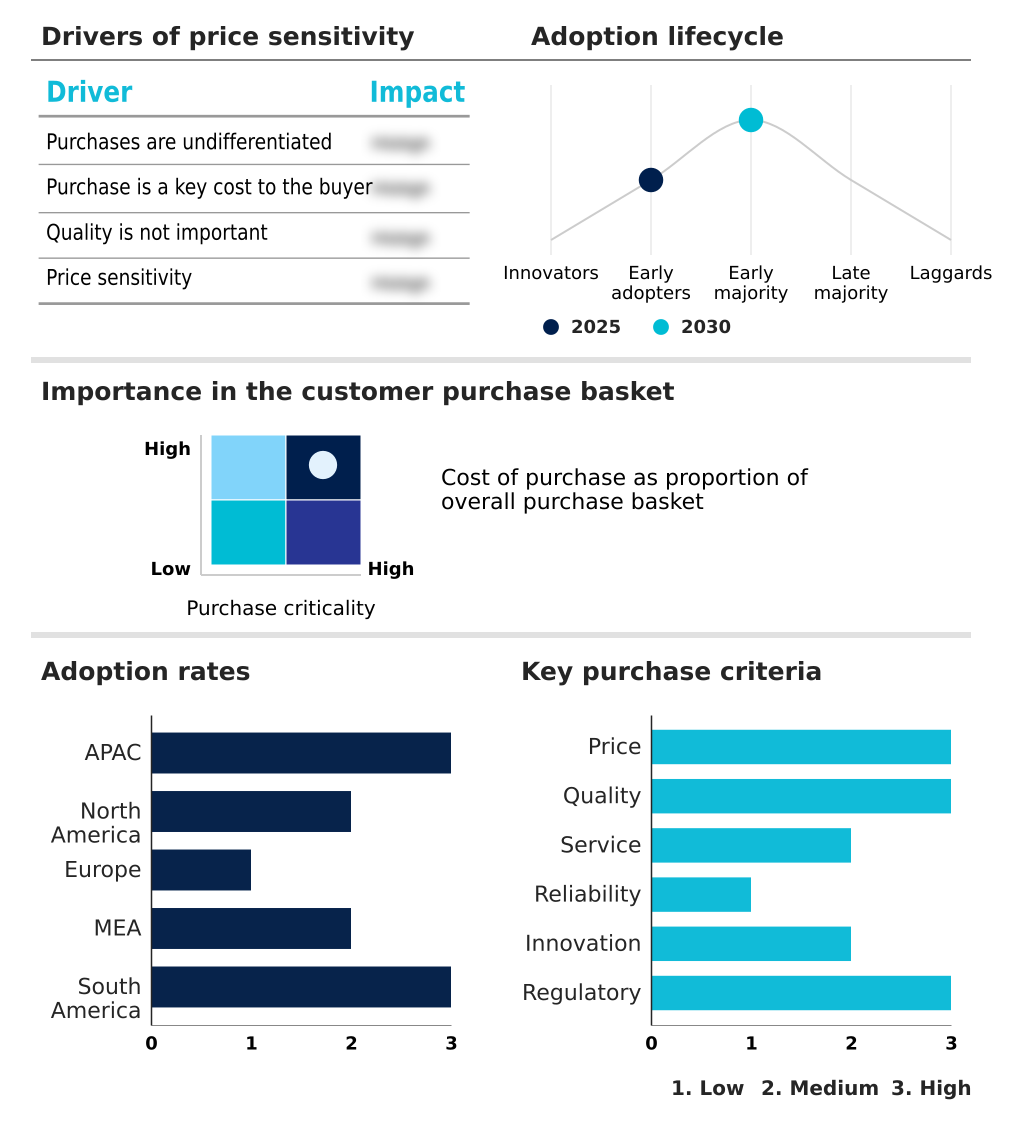

The port infrastructure market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the port infrastructure market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Port Infrastructure Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the port infrastructure market industry.

ABB Ltd. - Core offerings include port electrification, automation solutions, terminal operating systems, heavy machinery, and specialized marine engineering for global trade facilitation.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABB Ltd.

- APM Terminals

- Bechtel Corp.

- Boskalis

- CK Hutchison Holdings Ltd.

- DP World

- Essar

- Jan De Nul

- Kaleris

- Kalmar Corp.

- Konecranes plc

- Larsen and Toubro Ltd.

- Liebherr International AG

- Sany Heavy Industry Co. Ltd.

- Siemens AG

- Van Oord

- Vinci Construction

- Wartsila Corp.

- Zhenhua Heavy Industries Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Port Infrastructure Market

- In May 2025, DP World announced plans to invest approximately $2.5 billion over the year to strengthen and expand its global logistics network.

- In May 2025, Kale Logistics Solutions partnered with Omans Ministry of Transport, Communications and TTechnology to design and implement a National Port Community System for digital logistics transformation.

- In April 2025, SOHAR Port and Freezone in Oman announced plans to expand its free zone area with an investment of $23 million to accommodate growing demand from tenants.

- In April 2025, Mexico officially advanced a major expansion of the Port of Manzanillo as part of a long-term strategy to strengthen global trade links.

Research Analyst Overview: Port Infrastructure Market

The port infrastructure market's evolution is driven by the need for operational resilience and efficiency, compelling significant capital investment in both physical and digital assets. Boardroom decisions now center on the total cost of ownership for advanced container handling equipment, including automated guided vehicles and ship-to-shore cranes, weighing upfront CAPEX against long-term labor savings and throughput gains.

The deployment of sophisticated terminal operating systems and yard management systems is critical for optimizing assets. A major focus is upgrading physical structures through quay wall reinforcement and the construction of new breakwater structures and mooring buoys.

Simultaneously, sustainability pressures mandate the adoption of cold ironing systems and other zero-emission terminal equipment to comply with standards like the IMO's SOLAS convention. This requires a holistic approach, integrating everything from deep water dredging and land reclamation to the build-out of intermodal rail yards, ensuring seamless, compliant, and competitive maritime logistics.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Port Infrastructure Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 299 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.8% |

| Market growth 2026-2030 | USD 50834.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.5% |

| Key countries | China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, The Netherlands, Germany, UK, France, Italy, Spain, UAE, Saudi Arabia, South Africa, Turkey, Israel, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Port Infrastructure Market: Key Questions Answered in This Report

-

What is the expected growth of the Port Infrastructure Market between 2026 and 2030?

-

The Port Infrastructure Market is expected to grow by USD 50.83 billion during 2026-2030, registering a CAGR of 4.8%. Year-over-year growth in 2026 is estimated at 4.5%%. This acceleration is shaped by expansion of global electronic commerce and maritime freight demand , which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Terminals, Berths and docks, Storage facilities, and Others), End-user (Seaports, and Inland ports), Application (Cargo port, and Passenger port) and Geography (APAC, North America, Europe, Middle East and Africa, South America). Among these, the Terminals segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, North America, Europe, Middle East and Africa and South America. APAC is estimated to contribute 32.9% to market growth during the forecast period. Country-level analysis includes China, Japan, India, South Korea, Australia, Indonesia, US, Canada, Mexico, The Netherlands, Germany, UK, France, Italy, Spain, UAE, Saudi Arabia, South Africa, Turkey, Israel, Brazil, Argentina and Colombia, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is expansion of global electronic commerce and maritime freight demand , which is accelerating investment and industry demand. The main challenge is high capital expenditure and lengthy gestation periods , creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Port Infrastructure Market?

-

Key vendors include ABB Ltd., APM Terminals, Bechtel Corp., Boskalis, CK Hutchison Holdings Ltd., DP World, Essar, Jan De Nul, Kaleris, Kalmar Corp., Konecranes plc, Larsen and Toubro Ltd., Liebherr International AG, Sany Heavy Industry Co. Ltd., Siemens AG, Van Oord, Vinci Construction, Wartsila Corp. and Zhenhua Heavy Industries Co.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Port Infrastructure Market Research Insights

Market dynamics are shaped by the dual pressures of operational efficiency and regulatory compliance. The push for higher cargo throughput velocity necessitates advanced vessel traffic management systems and predictive maintenance protocols for critical assets, directly influencing procurement decisions.

For example, European ports, which are projected to grow faster than those in South America, are rapidly adopting smart port technologies to comply with the EU's Green Deal objectives.

An operational scenario involves implementing a port community system compliant with ISO 28000 security standards, which integrates data from shipping lines and terminal operators to streamline customs clearance and reduce truck idling times. This not only enhances hinterland connectivity but also provides verifiable data for environmental reporting, aligning capital investment with both performance and sustainability mandates.

We can help! Our analysts can customize this port infrastructure market research report to meet your requirements.

RIA -

RIA -