Portable Oxygen Concentrators Market Size 2024-2028

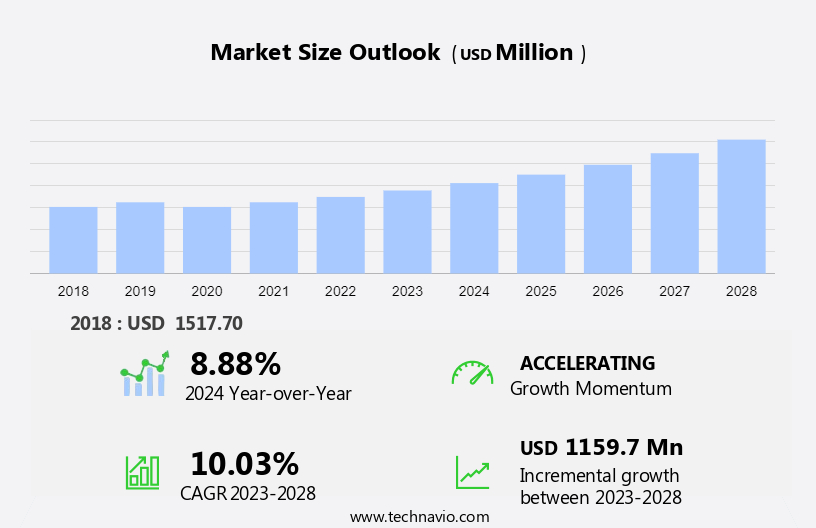

The portable oxygen concentrators market size is estimated to grow by USD 1.15 billion at a CAGR of 10.03% between 2023 and 2028. The respiratory industry is experiencing significant growth due to several key factors. The increasing prevalence of respiratory diseases, such as asthma, chronic obstructive pulmonary disease (COPD), and lung cancer, is driving demand for innovative diagnostic and therapeutic solutions. Additionally, the rise in the geriatric population, who are more susceptible to respiratory conditions, is expanding the market size. Furthermore, increasing awareness programs on respiratory health conditions, led by governments and healthcare organizations, are encouraging early detection and treatment, thereby fueling market growth. Companies in this industry focus on developing advanced technologies, such as telemedicine, wearable devices, and digital health platforms, to improve patient outcomes and enhance the overall healthcare experience.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Request Free Sample

Market Dynamic and Customer Landscape

The market is witnessing significant growth due to the increasing prevalence of respiratory diseases such as COPD, asthma, pulmonary fibrosis, tuberculosis (TB), and lung cancer. The aging population, with its higher susceptibility to respiratory diseases, is a major consumer group for POCs. Home healthcare solutions are gaining popularity as they offer convenience and cost savings compared to hospitalizations. Healthcare expenditures, insurance coverage, and reimbursement policies are key factors influencing the market growth. POCs are medical devices that concentrate oxygen from the ambient air and deliver it to the user. They are compact and lightweight, making them ideal for remote patient monitoring, telemedicine, and mobile health apps. POCs use pulse flow technology to deliver oxygen continuously, ensuring optimal oxygen saturation levels. Oxygen and nitrogen are the primary gases used in POCs. The market is expected to grow further due to the increasing healthcare services focus on improving patient outcomes and reducing hospital readmissions. Social segregation policies and respiratory complications are other factors driving the market demand. Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Key Market Driver

The increasing prevalence of respiratory diseases is notably driving market growth. Respiratory diseases, including lung cancer, are a significant health concern worldwide, leading to dyspnea or shortness of breath. This symptom, which can be progressive and debilitating, is often associated with chronic conditions such as chronic obstructive pulmonary disease (COPD), asthma, and pneumonia. COPD, in particular, is on the rise due to factors such as allergies, pollution, and smoking. While some individuals may only experience shortness of breath during strenuous activities, others may be immobilized by it, even during normal daily tasks.

Furthermore, portable oxygen concentrators have emerged as essential home care products for individuals requiring oxygen treatment. These mobile concentrators enable users to receive oxygen on-demand, improving their ability to perform daily activities and enhancing their quality of life. The increasing prevalence of chronic respiratory diseases, including COPD, pneumonia, and lung cancer, has led to a growing demand for portable oxygen concentrators. Thus, such factors are driving the market's growth during the forecast period.

Significant Market Trends

The prevailing presence of assisted-living facilities and home-care settings is the key trend in the market.

Portable oxygen concentrators have gained significant importance in the healthcare industry due to their effectiveness in delivering oxygen treatment to individuals with lung cancer, chronic respiratory diseases, and other breathing issues. These mobile concentrators are compact and lightweight, making them suitable for home care use and ideal for individuals requiring oxygen therapy while on the move.

Furthermore, the increasing prevalence of chronic respiratory diseases, such as lung cancer, pneumonia, and infections caused by smoking, is driving the demand for portable oxygen concentrators. According to the World Health Organization, pneumonia is the leading cause of death among children under five years of age, and many of these deaths occur due to oxygen shortages. Healthcare professionals recommend the use of portable oxygen concentrators to improve survival rates and manage breathing issues. In addition, the public healthcare system's increasing focus on home care products and accessories, such as portable oxygen concentrators, is expected to boost market growth. Senior assisted living facilities, such as Aegis Living, Integral Senior Living, American House, Americare Senior Living, Epoch Elder Care, and Ashiana Housing, are significant consumers of portable oxygen concentrators. Distributors, including Ports International and The Bahamas, cater to the demand for these devices in assisted living facilities. Thus, such trends will shape the market's growth during the forecast period.

Major Market Challenge

The high cost of portable oxygen concentrators is the major challenge that affects the growth of the market.

Portable oxygen concentrators have become essential medical devices for individuals suffering from lung cancer, chronic respiratory diseases, and other breathing issues. These devices provide oxygen treatment by concentrating normal air into medical-grade oxygen, making them indispensable for patients during oxygen shortages or infections, such as pneumonia or complications arising from smoking. However, the high cost of these devices, which ranges from USD2,000 to USD8,000 for continuous flow and pulse dose models, respectively, can hinder their widespread adoption. Advanced features like long-lasting battery life, compact size, and the ability to purify oxygen on the go increase the cost of portable oxygen concentrators.

Moreover, this high cost may discourage patients from purchasing these devices outright and instead opt for rented or borrowed units from the public healthcare system or healthcare professionals. This trend can negatively impact the sales of newly launched portable oxygen concentrators and reduce the market growth. Additionally, the affordability issue can lead to lower adoption rates of advanced pulse flow portable oxygen concentrators, which offer improved oxygen delivery efficiency and better patient comfort. Despite these challenges, the market for portable oxygen concentrators continues to grow due to the increasing prevalence of chronic respiratory diseases and the need for effective oxygen treatment solutions for children and adults alike. Hence, the above factors will impede the growth of the market during the forecast period

Key Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Chart Industries Inc. - The company offers portable oxygen concentrators to supply supplemental oxygen to users suffering from discomfort due to ailments, which affect the efficiency of the lungs, under the brand name FreeStyle.

The market research and growth report also includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Chart Industries Inc.

- Colfax Corporation

- Inogen Inc.

- Invacare Corp.

- Koninklijke Philips N.V.

- Medical Depot Inc.

- Mediniq Healthcare Pvt. Ltd.

- Niterra Co. Ltd.

- Nidek Medical India Pvt. Ltd.

- O2 Concepts LLC

- Precision Medical Inc.

- ResMed Inc.

- Teijin Ltd.

- Zhengzhou Olive Electronic Technology Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Segmentation

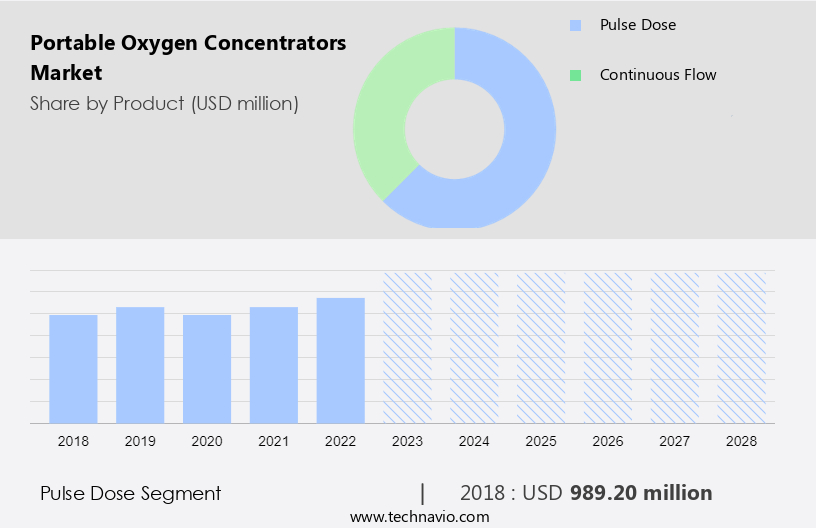

By Product

The market share growth by the pulse dose segment will be significant during the forecast period. Portable oxygen concentrators have emerged as essential medical devices for managing respiratory diseases in various healthcare settings. With an aging population and increasing prevalence of chronic respiratory conditions such as COPD, asthma, pneumonia, pulmonary fibrosis, and tuberculosis (TB), the demand for home healthcare solutions is on the rise.

Get a glance at the market share of various regions Download the PDF Sample

The pulse dose segment showed a gradual increase in the market share of USD 989.20 million in 2018. These devices offer medical oxygen to patients in continuous or pulse flow, making them ideal for homecare settings and even institutionalized care, including hospitals. Healthcare expenditures and insurance coverage have become significant factors driving the market growth for portable oxygen concentrators. Telemedicine, remote patient monitoring, and mobile health apps have further expanded their reach, allowing for seamless integration into healthcare services. However, challenges such as social segregation policies, skin irritation, and the presence of nitrogen in the output gas remain concerns. The portable concentrator O2 device market caters to both homecare and hospital settings, with continuous flow and portable options available. Reimbursement policies and healthcare systems play a crucial role in determining the accessibility and affordability of these devices for patients.

By Region

For more insights on the market share of various regions Download PDF Sample now!

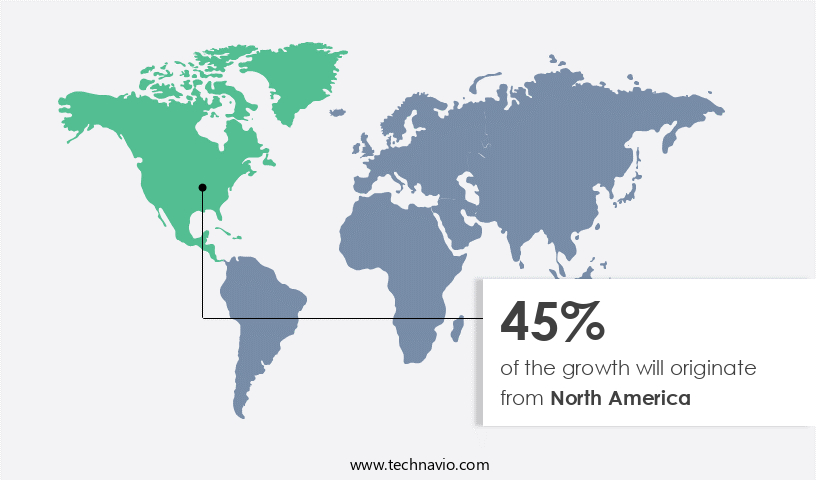

North America is estimated to contribute 45% to the growth of the global market during the forecast period. Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

Portable oxygen concentrators have emerged as essential medical devices in addressing respiratory needs for patients suffering from chronic conditions such as COPD, asthma, pneumonia, pulmonary fibrosis, and tuberculosis (TB). With an aging population and increasing healthcare expenditures, home healthcare solutions have become more prevalent. Portable oxygen concentrators offer patients the freedom to manage their medical oxygen requirements in homecare settings and even in institutionalized care settings like hospitals. Insurance coverage for these devices is a significant consideration, with reimbursement policies varying among healthcare systems. These concentrator O2 devices come in both portable and stationary versions, catering to diverse patient needs. Continuous flow devices provide a constant stream of oxygen, while pulse flow devices deliver oxygen only when the patient inhales. Telemedicine, remote patient monitoring, and mobile health apps have revolutionized healthcare services, enabling seamless integration of portable oxygen concentrators into patient care. However, concerns regarding skin irritation and potential nitrogen build-up remain. Social segregation policies may impact the adoption of these devices in certain communities. The global portable oxygen concentrator market is expected to grow significantly, driven by the increasing prevalence of chronic respiratory conditions and hospitalizations due to respiratory complications.

Segment Overview

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD Billion " for the period 2024-2028, as well as historical data from 2018 - 2022 for the following segments.

- Product Outlook

- Pulse dose

- Continuous flow

- Region Outlook

- APAC

- China

- India

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- South America

- Brazil

- Argentina

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- APAC

You may also interested in the below market reports

-

Homecare Oxygen Concentrators Market: Homecare Oxygen Concentrators Market by Product, Technology, and Geography - Forecast and Analysis

-

Medical Gas Cylinder Market: Medical Gas Cylinder Market Analysis North America, Europe, Asia, Rest of World (ROW) - US, Germany, UK,China, Japan - Size and Forecast

-

Anesthesia Monitoring Devices Market: Anesthesia Monitoring Devices Market by Type, End-user, and Geography - Forecast and Analysis

Market Analyst Overview

Portable oxygen concentrators have gained significant attention in the healthcare market due to the rising prevalence of respiratory diseases such as COPD, asthma, pneumonia, pulmonary fibrosis, and tuberculosis (TB). The aging population, with its increased susceptibility to chronic respiratory conditions, is a major driver of the portable oxygen concentrator market. Home healthcare solutions have become increasingly popular, allowing patients to receive medical oxygen in homecare settings and institutionalized care settings, reducing hospitalizations and respiratory complications. Healthcare expenditures and insurance coverage have also played a crucial role in the growth of the market. These devices are classified into continuous flow and pulse flow, catering to various patient needs.

Furthermore, portable oxygen concentrators are gaining popularity over stationary concentrators due to their convenience and mobility. The healthcare market is witnessing the integration of telemedicine, remote patient monitoring, and mobile health apps, which further enhances the utility of portable oxygen concentrators. Reimbursement policies and social segregation policies are key factors influencing the market dynamics. Nitrogen and oxygen are the primary gases used in portable oxygen concentrators to deliver medical-grade oxygen to patients. Portable oxygen concentrators are essential medical devices for patients with chronic respiratory conditions, enabling them to lead active lives while managing their health effectively. The market for portable oxygen concentrators is expected to grow significantly in the coming years, driven by the increasing demand for home healthcare services and the rising prevalence of respiratory diseases.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

143 |

|

Base year |

2023 |

|

Historic period |

2018 - 2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.03% |

|

Market growth 2024-2028 |

USD 1.15 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

8.88 |

|

Regional analysis |

North America, Europe, Asia, and Rest of World (ROW) |

|

Performing market contribution |

North America at 45% |

|

Key countries |

US, Germany, China, UK, and Canada |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Chart Industries Inc., Colfax Corporation, Inogen Inc., Invacare Corp., Koninklijke Philips N.V., Medical Depot Inc., Mediniq Healthcare Pvt. Ltd., Niterra Co. Ltd., Nidek Medical India Pvt. Ltd., O2 Concepts LLC, Precision Medical Inc., ResMed Inc., Teijin Ltd., and Zhengzhou Olive Electronic Technology Co. Ltd. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, Market condition analysis for market forecast period |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting of the market between 2024 and 2028

- Precise estimation of the size of the market size and its contribution to the parent market

- Accurate predictions about upcoming market trends and analysis and changes in consumer behavior

- Growth of the market industry across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough market growth analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive market analysis and report on the factors that will challenge the market research and growth of market companies

RIA -

RIA -