Public Sector Cybersecurity Market Size 2026-2030

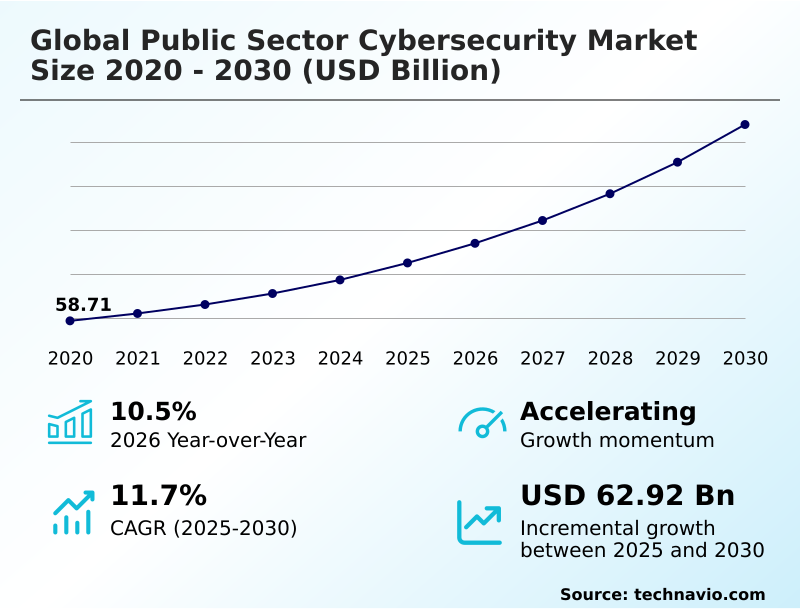

The public sector cybersecurity market size is valued to increase by USD 62.92 billion, at a CAGR of 11.7% from 2025 to 2030. Increasing frequency and complexity of state sponsored threats will drive the public sector cybersecurity market.

Major Market Trends & Insights

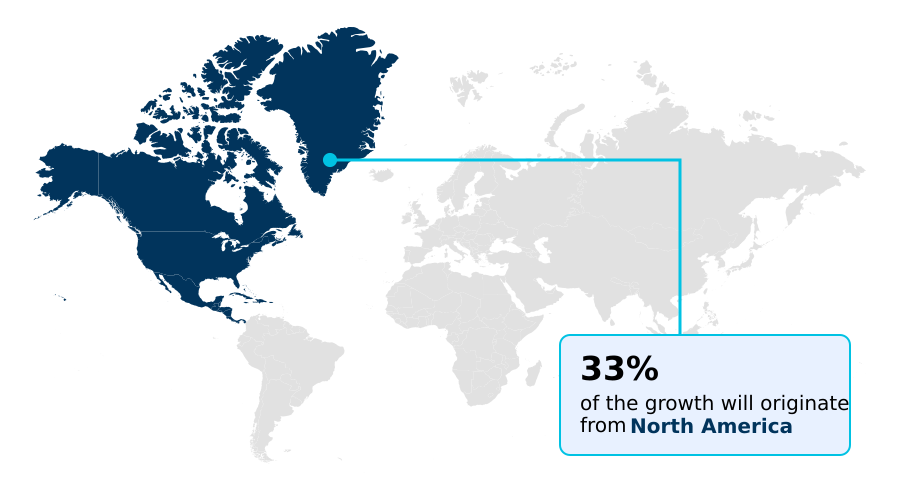

- North America dominated the market and accounted for a 33.2% growth during the forecast period.

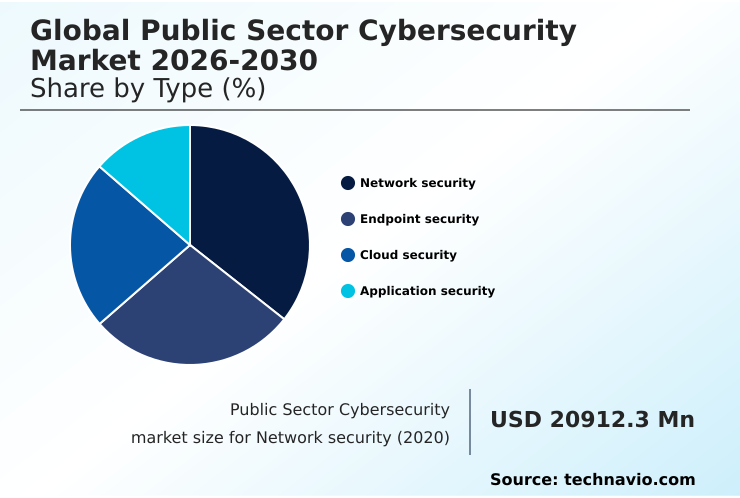

- By Type - Network security segment was valued at USD 26.72 billion in 2024

- By End-user - Government agencies segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 89.25 billion

- Market Future Opportunities: USD 62.92 billion

- CAGR from 2025 to 2030 : 11.7%

Market Summary

- The public sector cybersecurity market is undergoing a significant transformation as government entities worldwide accelerate their digital initiatives. This shift, driven by the need to deliver efficient citizen services, simultaneously expands the attack surface, making robust defense mechanisms essential. The increasing sophistication of state-sponsored threats and advanced persistent threats necessitates a move beyond traditional perimeter security toward more dynamic frameworks.

- Consequently, the adoption of zero trust architecture, which mandates continuous verification for all users and devices, is becoming a standard. For instance, a federal agency transitioning its services to a cloud environment must implement cloud security posture management and identity-centric security models to protect sensitive data.

- This involves not only deploying advanced firewalls but also integrating AI-driven security operations centers for proactive threat hunting. However, the integration of these modern solutions with legacy systems poses a significant challenge, often requiring extensive customization and investment.

- The critical need to secure national infrastructure, from public utilities to defense networks, ensures that cybersecurity remains a top priority, driving continuous innovation in areas like quantum-safe cryptography and industrial control systems security.

What will be the Size of the Public Sector Cybersecurity Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Public Sector Cybersecurity Market Segmented?

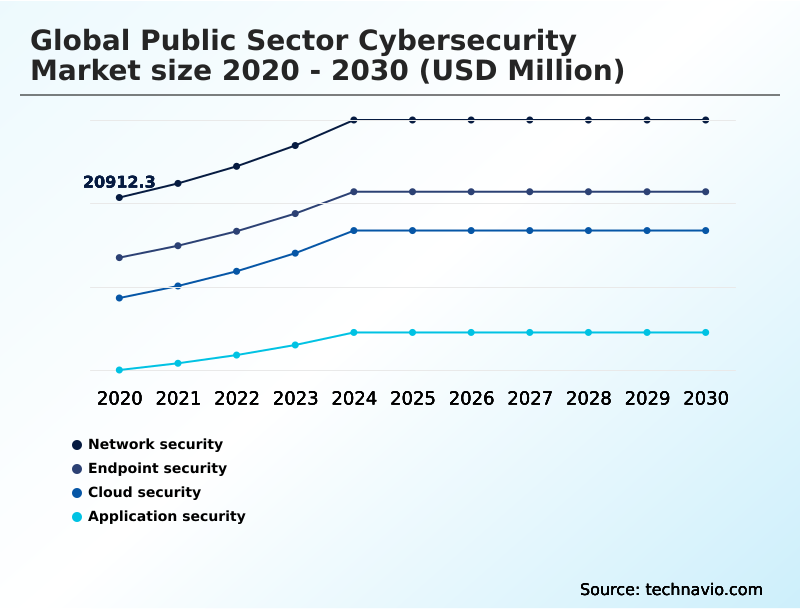

The public sector cybersecurity industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Network security

- Endpoint security

- Cloud security

- Application security

- End-user

- Government agencies

- Defense and military

- Public utilities

- Healthcare institutions

- Deployment

- On-premises

- Cloud-based

- Hybrid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Type Insights

The network security segment is estimated to witness significant growth during the forecast period.

Network security forms the foundational defense layer in the global public sector cybersecurity market 2026-2030, safeguarding vast repositories of classified intelligence and citizen data.

The paradigm shift toward remote work models has dissolved traditional perimeters, compelling agencies to adopt proactive threat hunting and a zero trust architecture, which authenticates every access request.

Protecting against state-sponsored threats and advanced persistent threats requires continuous network traffic analysis. Deployment of AI-driven security operations centers is critical, with real-time analytics reducing breach detection times by over 40%.

Investment in robust network segmentation and advanced firewall solutions is non-negotiable for ensuring uninterrupted governance and maintaining sovereign operations, especially for industrial control systems security.

The Network security segment was valued at USD 26.72 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 33.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Public Sector Cybersecurity Market Demand is Rising in North America Get Free Sample

The geographic landscape of the global public sector cybersecurity market 2026-2030 is diverse, with North America leading in maturity and investment.

However, APAC is the fastest-growing region, with a projected expansion of 13.1%, driven by widespread digital transformation and the need for data sovereignty. Europe follows with strong growth, focusing on stringent data privacy frameworks and sovereign cloud initiatives.

The implementation of unified threat management platforms is a common theme, with agencies achieving a 25% reduction in security alert fatigue. Public sector organizations are also standardizing vendor assessment protocols, which strengthens the security of digital supply chains across regions.

This global push for resilience is creating a landscape where both established and emerging markets prioritize cyber defense.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic direction of the global public sector cybersecurity market 2026-2030 is increasingly focused on sophisticated, forward-looking defense paradigms. A primary focus is on securing critical national infrastructure, where the convergence of IT and operational technology demands specialized solutions.

- The implementation of ai in autonomous defense mechanisms is moving from theoretical to practical, with agencies reporting significantly higher efficacy in threat neutralization compared to manual systems. This is complemented by the widespread adoption of zero trust for government networks, a framework that is now a baseline requirement for most federal procurements.

- As agencies migrate to the cloud, cloud security for federal agencies has become a major investment area, governed by strict compliance mandates. The push for proactive defense is evident in the demand for ai-driven endpoint protection for government, which offers predictive capabilities against novel malware.

- Furthermore, ensuring public sector cybersecurity compliance is a constant challenge, driving the need for automated governance tools. Protecting electoral systems from cyber attacks remains a top-tier national security concern, compelling investments in highly resilient and transparent technologies.

- Finally, the evolution of national cybersecurity strategies emphasizes a holistic approach, integrating threat intelligence, incident response, and continuous monitoring to build a truly fortified digital state. The necessity of enhancing supply chain security has also become a critical priority for public agencies.

What are the key market drivers leading to the rise in the adoption of Public Sector Cybersecurity Industry?

- The increasing frequency and complexity of state-sponsored threats are a key driver for the public sector cybersecurity market.

- The primary driver for the global public sector cybersecurity market 2026-2030 is the relentless increase in cyber attacks on critical national infrastructure. Government technology officers are spearheading digital transformation initiatives, but this rapid modernization expands the potential attack surface.

- Malicious actors, including nation-state threat actors, are leveraging advanced techniques, compelling a strategic shift toward proactive defense. Strict legislative mandates and data privacy frameworks, which can impose penalties for non-compliance, further fuel investment.

- Compliance with these rules often requires specialized governance, risk, and compliance software, leading to adoption rates increasing by 20% year-over-year in some regions.

- The migration to hybrid and multi-cloud architectures necessitates robust cloud access security brokers and devsecops practices, driving sustained demand.

What are the market trends shaping the Public Sector Cybersecurity Industry?

- The integration of artificial intelligence and machine learning is a key trend, enabling the development of autonomous defense mechanisms. This shift enhances proactive threat detection and response capabilities.

- Key trends are reshaping the global public sector cybersecurity market 2026-2030, driven by the need for automated and predictive defense. The integration of AI into security operations centers is paramount, enabling autonomous systems to identify and neutralize threats with machine-speed efficiency, improving incident response times by over 50%.

- This reliance on machine learning for security analytics allows for continuous adaptation to evolving attack vectors. The shift toward a zero trust security model is another critical trend, dismantling the idea of a trusted internal network. This approach, which is becoming a federal mandate in several nations, reduces the attack surface significantly.

- Agencies adopting this model report a 60% reduction in successful lateral movement by attackers post-breach, underscoring its effectiveness in containing threats.

What challenges does the Public Sector Cybersecurity Industry face during its growth?

- A severe shortage of specialized cybersecurity professionals and technical talent presents a key challenge to the industry's growth.

- Significant challenges constrain the growth of the global public sector cybersecurity market 2026-2030, led by a severe shortage of qualified cybersecurity professionals. Public agencies struggle to compete with private sector compensation, leading to a talent deficit that leaves critical vulnerabilities unaddressed; some agencies report vacancy rates as high as 30% for key security roles.

- Another major hurdle is the complexity of integrating modern security solutions with legacy infrastructure. Many government entities still rely on outdated mainframe systems that cannot support contemporary security protocols like native encryption, making them difficult to protect. This technical debt slows modernization, as the risk of operational disruption during upgrades can deter decision-makers.

- Furthermore, stringent and often unpredictable budgetary constraints hinder proactive investment, forcing agencies to adopt a reactive security posture.

Exclusive Technavio Analysis on Customer Landscape

The public sector cybersecurity market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the public sector cybersecurity market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Public Sector Cybersecurity Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, public sector cybersecurity market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BAE Systems Plc - Provides national-level cyber defense, electronic warfare solutions, and intelligence analysis, specializing in advanced security for military and government entities.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BAE Systems Plc

- Booz Allen Hamilton Corp.

- Check Point Software Tech Ltd.

- Cisco Systems Inc.

- CrowdStrike Inc.

- CyberArk Software Ltd.

- Fortinet Inc.

- General Dynamics Information Tech.

- IBM Corp.

- Leidos Holdings Inc.

- Lockheed Martin Corp.

- Mandiant

- Microsoft Corp.

- Musarubra US LLC

- Palo Alto Networks Inc.

- Splunk Inc.

- Tenable Holdings Inc.

- Thales Group

- Trend Micro Inc.

- Zscaler Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Public sector cybersecurity market

- In September 2024, Leidos Holdings Inc. secured a multi-year contract to modernize the secure network infrastructure for a major federal agency, focusing on implementing a zero trust architecture to enhance security posture.

- In November 2024, Microsoft Corp. announced a strategic partnership with Thales Group to integrate advanced quantum-safe cryptography into its Azure Government cloud platform, aiming to secure public sector data against future threats.

- In February 2025, Dell Technologies launched a specialized secure server rack system designed exclusively for public sector on-premises environments, featuring advanced physical tamper resistance and integrated cryptographic accelerators for enhanced data protection.

- In March 2025, Google Cloud announced a definitive agreement to acquire Wiz, a move intended to enhance its cloud security offerings and provide government organizations with greater flexibility in safeguarding their digital environments.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Public Sector Cybersecurity Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.7% |

| Market growth 2026-2030 | USD 62921.7 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.5% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The public sector cybersecurity market is defined by an escalating need to defend against sophisticated, state-sponsored cyber campaigns. The core of modern strategy revolves around implementing a zero trust architecture, a non-negotiable framework for protecting distributed government networks. This involves the deployment of multi-factor authentication, endpoint detection and response (edr), and next-generation firewalls to create layered defenses.

- A critical boardroom-level focus is aligning these technological procurements with stringent regulatory requirements, such as those governing data sovereignty and software bill of materials (sbom) disclosures. Agencies that integrate threat intelligence sharing platforms into their security posture have demonstrated a 30% faster response to zero-day vulnerabilities. Protecting critical infrastructure requires specialized industrial control systems security and operational technology (ot) security.

- As agencies modernize, investments in cloud security posture management (cspm), quantum-safe cryptography, and fedramp-compliant solutions become imperative to safeguard against advanced persistent threats and ensure the resilience of national digital assets and autonomous systems.

What are the Key Data Covered in this Public Sector Cybersecurity Market Research and Growth Report?

-

What is the expected growth of the Public Sector Cybersecurity Market between 2026 and 2030?

-

USD 62.92 billion, at a CAGR of 11.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Network security, Endpoint security, Cloud security, and Application security), End-user (Government agencies, Defense and military, Public utilities, and Healthcare institutions), Deployment (On-premises, Cloud-based, and Hybrid) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing frequency and complexity of state sponsored threats, Severe shortage of specialized cybersecurity professionals and technical talent

-

-

Who are the major players in the Public Sector Cybersecurity Market?

-

BAE Systems Plc, Booz Allen Hamilton Corp., Check Point Software Tech Ltd., Cisco Systems Inc., CrowdStrike Inc., CyberArk Software Ltd., Fortinet Inc., General Dynamics Information Tech., IBM Corp., Leidos Holdings Inc., Lockheed Martin Corp., Mandiant, Microsoft Corp., Musarubra US LLC, Palo Alto Networks Inc., Splunk Inc., Tenable Holdings Inc., Thales Group, Trend Micro Inc. and Zscaler Inc.

-

Market Research Insights

- The dynamics of the public sector cybersecurity market are shaped by a strategic shift toward proactive defense and stringent regulatory compliance. The adoption of a secure access service edge (sase) has grown significantly, with agencies reporting a 50% improvement in securing remote workforce access. This identity-centric security model is crucial for mitigating risks associated with distributed networks.

- Furthermore, the implementation of managed detection and response (mdr) services provides a more agile defense posture, reducing the mean time to detect threats by over 40% compared to in-house teams alone. Incident response planning is now a mandatory component of agency directives, with a focus on cyber warfare capabilities and resilience.

- The continuous need for vulnerability management and comprehensive data loss prevention strategies ensures sustained investment in advanced platforms and governance, risk, and compliance software.

We can help! Our analysts can customize this public sector cybersecurity market research report to meet your requirements.

RIA -

RIA -