Racing Clutches Market Size 2024-2028

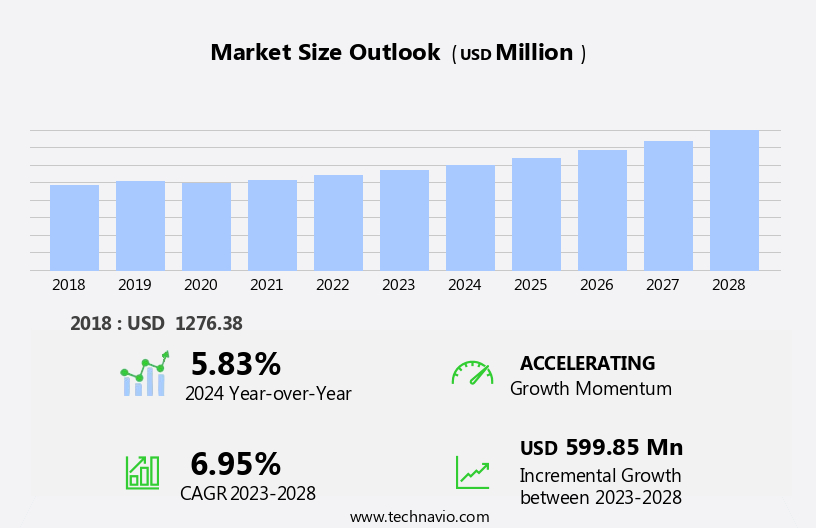

The racing clutches market size is forecast to increase by USD 599.85 million at a CAGR of 6.95% between 2023 and 2028.

- The market presents significant growth opportunities for suppliers, driven by the increasing popularity of high-performance vehicles and the expanding automotive aftermarket. Friction-less engine coupling with drive systems is a key trend, as racing clutches offer improved power transfer and efficiency, enhancing the overall driving experience. However, the market remains unregulated, creating both opportunities and challenges. With multiple suppliers developing racing clutches as a product portfolio, competition is fierce. Companies must differentiate themselves through innovation, quality, and customer service to gain market share.

- Additionally, the aftermarket's fragmented nature necessitates effective distribution networks and strategic partnerships to reach consumers. By staying abreast of these trends and navigating the competitive landscape, companies can capitalize on the market's potential and thrive in this dynamic industry.

What will be the Size of the Racing Clutches Market during the forecast period?

- The market in the United States is experiencing significant growth, driven by the increasing popularity of motorsports and the demand for high-performance racing drivetrains. These clutches, which include basic friction components such as pressure plates, driving members, and operating members, are essential for transferring power from the engine to the racing transmission or gearbox in high-performance vehicles. Manufacturers are focusing on using lightweight materials, such as metallic, cerametallic, and carbon, to create specialized clutches that can withstand extreme conditions and provide superior performance. The market is also witnessing the emergence of energy-efficient clutch designs, aligning with the broader trend toward automotive technology and engine technology innovation.

- Aftermarket buyers are a significant market segment, as racing cars frequently undergo frequent upgrades and require regular clutch replacements. The market encompasses various types of racing clutches, including wet and dry clutches, multiplate clutches, and clutches for dual-clutch systems. The growing adoption of electric powertrains in racing applications is also expected to create new opportunities in this market. Overall, the market is poised for continued growth, driven by technological advancements and the enduring appeal of motorsports.

How is this Racing Clutches Industry segmented?

The racing clutches industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Eco performance

- High performance

- Application

- OEMs

- Aftermarkets

- Geography

- Europe

- Germany

- Italy

- UK

- North America

- US

- APAC

- China

- South America

- Middle East and Africa

- Europe

By Type Insights

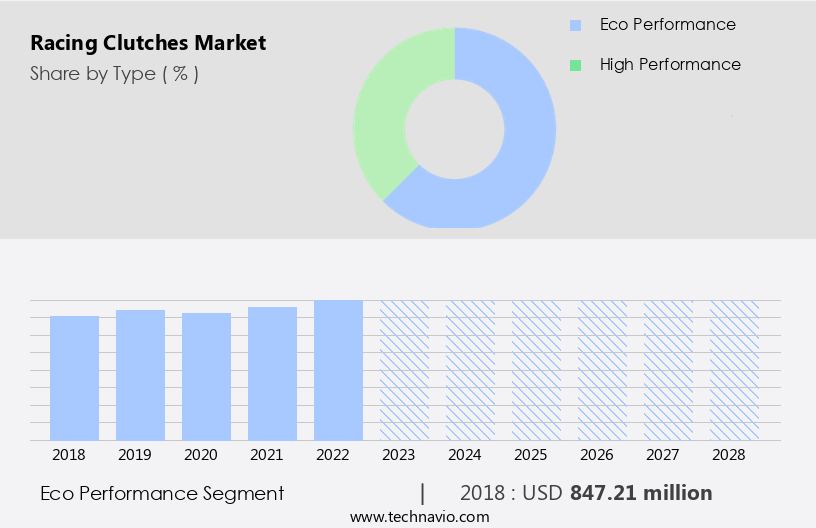

The eco performance segment is estimated to witness significant growth during the forecast period.

The market encompasses high-performance clutches designed for extreme conditions in motorsport applications. These clutches cater to the rapid shifts and precise control required in racing environments. Multidisc clutch designs, including carbon fiber, wet and dry, cerametallic, and metallic, are popular choices due to their increased torque capacity and durability. Lightweight materials, such as carbon fiber, are increasingly used to reduce weight in racing transmissions and drivetrains. Eco-performance clutches, a segment of this market, are gaining traction due to the growing emphasis on sustainability in the automotive industry. These clutches integrate environmentally friendly materials and manufacturing processes while maintaining optimal performance.

Strict emissions regulations and environmental standards worldwide are driving the demand for eco-friendly components. As a result, racing teams and automotive enthusiasts can meet these regulations without compromising on performance. Dual-clutch systems and paddle-shift transmissions are popular applications for these specialized clutches. Clutch systems play a crucial role in engine technology, with the driving member and driven member working together to transmit power efficiently. Clutch pressure plates and clutch discs are essential components, ensuring reliable and quick shifts. Energy-efficient clutch designs are also gaining popularity due to their potential to save fuel and reduce emissions. In summary, the market is characterized by the need for high-performance, durable, and lightweight components that meet the demands of racing environments.

The eco-performance segment is gaining traction due to the growing emphasis on sustainability and environmental regulations. Manufacturers are responding by developing innovative solutions that meet these requirements while maintaining superior performance.

Get a glance at the market report of share of various segments Request Free Sample

The Eco performance segment was valued at USD 847.21 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

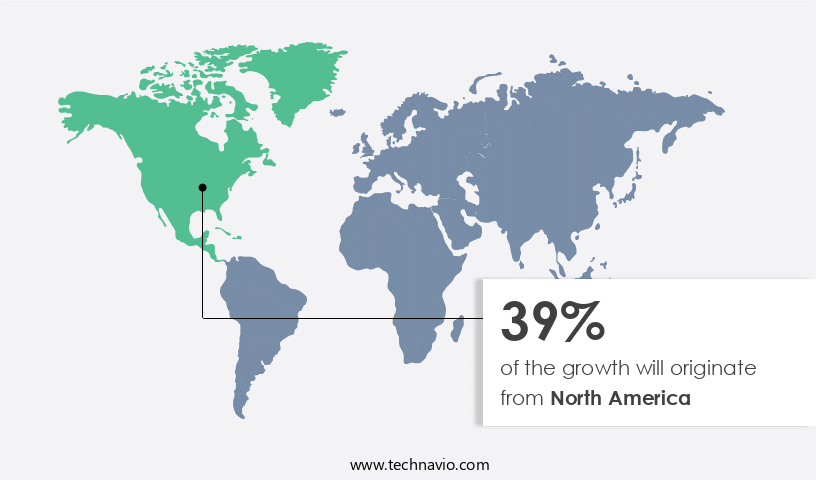

North America is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The high-performance the market experiences significant demand due to the extreme conditions and rapid shifts required in motorsport applications. Carbon fiber, electric powertrains, and advanced clutch systems are key trends in this market. Multidisc clutch designs, such as carbon fiber, wet and dry, cerametallic, and metallic, cater to the need for increased torque capacity, superior performance, and precise control. Dualclutch systems and paddle-shift transmissions are popular choices for racing cars due to their quick shifts and optimal performance. OEMs and aftermarket buyers prioritize durability, reliability, and lightweight materials in their racing transmissions and drivetrains. The automotive technology industry continues to innovate with energy-efficient clutch designs and specialized clutches for motorsport environments.

The market for aftermarket clutches is growing as racing cars demand frequent clutch replacements. Overall, the market is driven by the need for extreme torque, rapid engagement requirements, and the pursuit of superior performance in the world of motorsports.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Racing Clutches Industry?

- Multiple suppliers developing performance/racing clutches as a product portfolio is the key driver of the market.

- Multiple leading suppliers in the global clutch market have established subsidiaries dedicated to creating high-performance products for motorsport and high-end automotive applications. The racing clutch market has experienced growth due to advancements in research and development (R&D) and innovation. Suppliers are focusing on developing efficient anti-heating and anti-skid designs to expand their customer base and tap into lucrative motorsport opportunities. Additionally, the availability of compatible clutch kits for various existing automotive models offers a viable option for part replacement.

- Transmission and suspension system manufacturers have invested significantly in R&D to collaborate with Original Equipment Manufacturers (OEMs) and create high-performance technologies.

What are the market trends shaping the Racing Clutches Industry?

- Friction-less engine coupling with drive system is the upcoming market trend.

- The clutch system, a long-standing method for engine and transmission connection, has been the focus of extensive research in the realm of engine technology. The primary objectives of this research have been the reduction of friction and enhancement of energy transfer efficiency. With the anticipated phase-out of manual gearboxes from the automotive industry, there is a growing demand for advanced clutch technologies. One such innovation eliminates clutch friction and pressure plates, offering increased efficiency and extended lifetime.

- A novel design has emerged, replacing the conventional clutch kit with an individual dog gear and utilizing interlocking teeth instead of friction for engine-gearbox coupling. This technological advancement signifies a significant stride towards more efficient and durable transmission systems.

What challenges does the Racing Clutches Industry face during its growth?

- Unregulated automotive aftermarket is a key challenge affecting the industry growth.

- The aftermarket represents a significant opportunity for technological enhancements in the automotive industry. However, The market is plagued with counterfeit and underperforming products, which proliferate due to their low prices. Chinese producers play a pivotal role in disrupting the aftermarket with affordable offerings and technology degradation. Despite the unregulated market landscape, the racing clutch holds immense importance as a critical component of the transmission system.

- Its design intricacies and high safety concerns necessitate stringent performance standards. Engineered with enhanced torsional rigidity, the racing clutch is an indispensable element for high-performance applications. The market dynamics underscore the importance of product quality and safety, making it essential for consumers to exercise caution when selecting racing clutches.

Exclusive Customer Landscape

The racing clutches market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the racing clutches market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, racing clutches market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ace Manufacturing and Parts Co. - The company specializes in high-performance racing clutches, catering to the demands of professional racers. Our product range encompasses circle track clutches and drag racing clutches, engineered for optimal power transfer and durability. These clutches undergo rigorous testing to ensure superior performance and reliability, making them a top choice for serious racers worldwide.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ace Manufacturing and Parts Co.

- Advanced Clutch Technology Inc.

- AIM Corp.

- AP Racing Ltd

- Australian Clutch Services Pty. Ltd.

- Brembo Spa

- Clutch Masters Industries Inc.

- Competition Clutch Inc.

- EXEDY Corp.

- Helix Autosport Ltd.

- Holley Inc.

- Klaus Reinicke GmbH

- OS Giken USA

- Quarter Master

- Schaeffler AG

- SPEC Clutch Inc

- Tilton Engineering Inc.

- TTV Industrial Ltd.

- ZF Friedrichshafen AG

- FCC Co. ltd

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The high-performance racing clutch market experiences rapid shifts in response to the evolving demands of motorsport applications. Extreme conditions, such as high torque and rapid engagement requirements, place significant stress on these components, necessitating advanced materials and designs. Carbon fiber and lightweight metals are increasingly utilized in the production of high-performance racing clutches due to their superior strength-to-weight ratio. These materials enable the creation of clutches that offer increased torque capacity and durability, essential for racing transmissions in extreme conditions. Electric powertrains, while gaining popularity in the automotive industry, present unique challenges for racing clutches.

The demand for precise control and quick shifts in electric vehicles necessitates specialized clutch designs that cater to the specific requirements of these powertrains. Aftermarket buyers play a crucial role in the market, as they seek to enhance the performance of their racing cars. They require clutches that offer superior performance, reliability, and durability, often turning to multidisc clutch designs and carbon fiber clutch pressure plates for their racing gearboxes. Wet and dry cerametallic and metallic clutches are popular choices for racing applications due to their ability to handle extreme torque and provide quick shifts.

These clutches are designed to operate under high temperatures and pressures, making them ideal for racing environments. The automotive technology landscape is continually evolving, with a focus on energy-efficient clutch designs and dual-clutch systems. These systems offer improved performance and efficiency, making them a popular choice for motorsport applications. The market is characterized by intense competition and innovation. OEMs and aftermarket suppliers strive to develop clutches that offer optimal performance, reliability, and durability. Lightweight materials, such as carbon fiber, continue to gain favor due to their ability to reduce weight and improve power-to-weight ratio. Racing cars place extreme demands on clutch systems, requiring components that can handle high torque, rapid shifts, and precise control.

Clutch systems must be designed to operate efficiently under extreme conditions, making them a critical component of racing drivetrains. Engine technology advances continue to impact the market, with multiplate and racing drivetrains requiring specialized clutches to handle increased torque capacity. The focus on reliability and durability ensures that racing clutches remain a key area of investment for the motorsports industry.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

160 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.95% |

|

Market growth 2024-2028 |

USD 599.85 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

5.83 |

|

Key countries |

US, China, Germany, UK, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Racing Clutches Market Research and Growth Report?

- CAGR of the Racing Clutches industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the racing clutches market growth of industry companies

We can help! Our analysts can customize this racing clutches market research report to meet your requirements.

RIA -

RIA -