Renewable Distributed Energy Generation (RDEG) Technologies Market Size 2026-2030

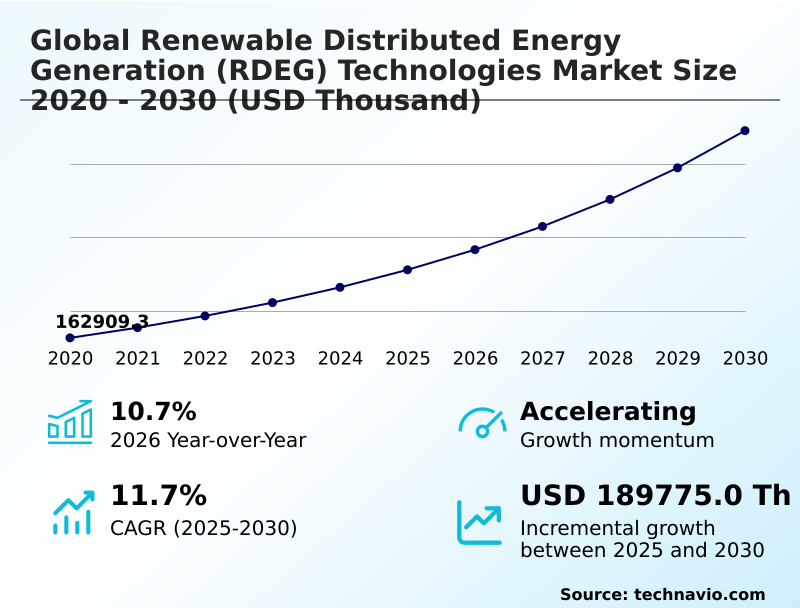

The Renewable Distributed Energy Generation (RDEG) Technologies Market size was valued at USD 255.71 million in 2025, growing at a CAGR of 11.7% during the forecast period 2026-2030.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 54.2% growth during the forecast period.

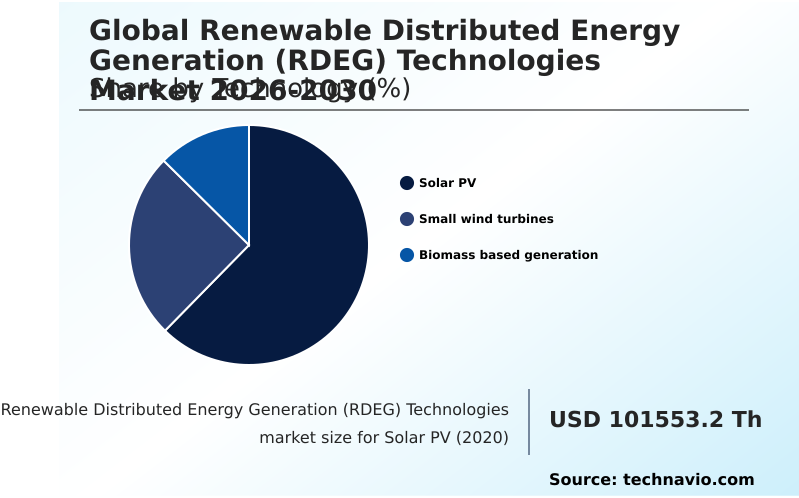

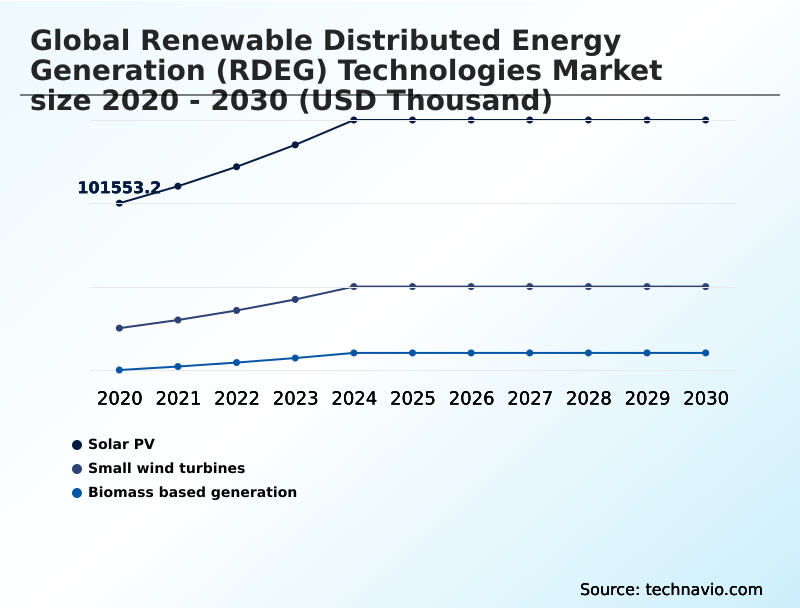

- By Technology - Solar PV segment was valued at USD 141.97 million in 2024

- By Connectivity - On-grid systems segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024:

- Market Future Opportunities 2025-2030: USD 189.78 million

- CAGR from 2025 to 2030 : 11.7%

Market Summary

- The renewable distributed energy generation (rdeg) technologies market is undergoing accelerated expansion, fundamentally reshaping energy systems with a projected 11.7% growth. This maturation is driven by a strategic pivot towards energy security, where a business might deploy a solar-plus-storage microgrid to ensure 99.9% uptime for critical manufacturing operations, insulating them from grid failures.

- The market's impetus is broadening from purely economic considerations to include strategic imperatives; for instance, the integration of energy management systems (ems) can optimize energy flows, reducing operational costs by over 15%. A primary driver is the global mandate for decarbonization, fostering supportive regulatory environments.

- However, a significant challenge remains the technical difficulty of integrating a vast number of decentralized power sources into legacy grid infrastructure, which can limit hosting capacity and require substantial investment in grid modernization.

What will be the Size of the Renewable Distributed Energy Generation (RDEG) Technologies Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Renewable Distributed Energy Generation (RDEG) Technologies Market Segmented?

The renewable distributed energy generation (rdeg) technologies industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Technology

- Solar PV

- Small wind turbines

- Biomass based generation

- Connectivity

- On-grid systems

- Off-grid systems

- Hybrid

- Application

- Commercial

- Industrial

- Residential

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- APAC

How is the Renewable Distributed Energy Generation (RDEG) Technologies Market Segmented by Technology?

The solar pv segment is estimated to witness significant growth during the forecast period.

The solar PV segment, which represents over 60% of new capacity, is pivotal to the renewable distributed energy generation (rdeg) technologies market, driven by falling production costs and advancing technological efficiencies.

This segment, covering everything from residential rooftops to large-scale commercial installations, is seeing a significant shift with the integration of energy storage systems, which improves asset value by over 15% through enhanced self-consumption.

Innovations in smart inverters and energy management systems are crucial for managing dispatchable power.

The market expansion relies on supportive regulatory frameworks like net metering and renewable portfolio standards that encourage adoption by both consumers and corporations, enhancing grid stability and energy security.

The Solar PV segment was valued at USD 141.97 million in 2024 and showed a gradual increase during the forecast period.

How demand for the Renewable Distributed Energy Generation (RDEG) Technologies market is rising in the leading region?

APAC is estimated to contribute 54.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Renewable Distributed Energy Generation (RDEG) Technologies Market demand is rising in APAC Request Free Sample

The global landscape for renewable distributed energy generation (rdeg) technologies is led by APAC, which accounts for 54.2% of the market's incremental growth, significantly outpacing Europe's 23.9%.

This dominance is fueled by countries like China, which is expanding its distributed solar capacity, and India, with initiatives aiming to install rooftop systems on millions of households.

In contrast, North America's market, representing 12.6% of growth, is driven by state-level renewable portfolio standards and a strong focus on grid resilience and energy security.

Regional differences in adoption are heavily influenced by regulatory support, such as feed-in tariffs in Europe versus tax incentives in the US, and the maturity of grid modernization efforts to manage demand-side flexibility.

What are the key Drivers, Trends, and Challenges in the Renewable Distributed Energy Generation (RDEG) Technologies Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Exploring renewable distributed energy generation technologies applications reveals a shift from simple grid-tied systems to complex, resilient microgrid solutions for commercial industrial facilities. The benefits of integrating solar PV with battery storage are increasingly evident, with analyses showing a more than 15% improvement in energy self-sufficiency and a significant reduction in exposure to grid volatility.

- This synergy is crucial for businesses seeking to optimize their energy strategy. Furthermore, the impact of V2G on renewable energy systems is a transformative trend, turning electric vehicle fleets into distributed energy assets that enhance grid stability and provide ancillary services, with some projections indicating a potential 10% reduction in peak load stress on local distribution networks.

- For regions lacking robust infrastructure, off-grid solar systems for rural electrification are proving to be the most cost-effective path to energy access, leapfrogging traditional grid extension.

- However, the industry still grapples with the challenges of integrating rdeg into legacy grids, a complex issue that requires substantial investment in grid modernization to overcome technical hurdles like limited hosting capacity and reverse power flow, ensuring the continued growth and reliability of decentralized power.

What are the key market drivers leading to the rise in the adoption of Renewable Distributed Energy Generation (RDEG) Technologies Industry?

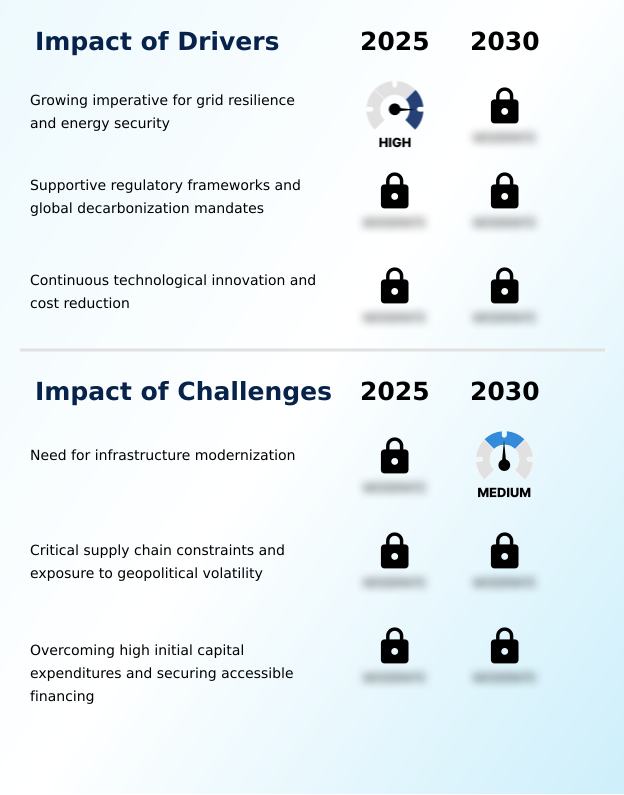

- The growing imperative for enhanced grid resilience and energy security is a key driver for the market.

- The escalating need for grid resilience is a primary driver for the renewable distributed energy generation (rdeg) technologies market, with microgrids demonstrating the ability to reduce outage durations by over 90% for critical facilities.

- This imperative for energy security, amplified by extreme weather events and geopolitical volatility, is accelerating the adoption of decentralized systems like solar PV and energy storage systems.

- Supportive regulatory frameworks, including renewable portfolio standards and streamlined net metering policies, have been shown to boost deployment rates by 40% in some regions.

- Simultaneously, continuous technological innovation and cost reductions, particularly a dramatic decline in the levelized cost of energy for solar, make on-grid systems and hybrid systems economically compelling alternatives to traditional power sources.

What are the market trends shaping the Renewable Distributed Energy Generation (RDEG) Technologies Industry?

- The convergence of renewable distributed energy generation with advanced energy storage and digitalization is fundamentally reshaping the market. This synergy transforms standalone assets into comprehensive, intelligent energy solutions.

- A predominant trend in renewable distributed energy generation (rdeg) technologies is the deep integration with advanced energy storage and digitalization, which can increase system efficiency by up to 20%. This convergence is creating intelligent, dispatchable power solutions that provide critical ancillary services to the grid.

- The proliferation of prosumer-centric models and community-based business models, including peer-to-peer energy trading platforms, is democratizing energy access, expanding the market addressable by over 30%. Furthermore, increasing sector coupling with transportation and heating through the electrification of end-use applications creates powerful symbiotic relationships, enhancing the systemic value of distributed assets and driving demand-side flexibility.

What challenges does the Renewable Distributed Energy Generation (RDEG) Technologies Industry face during its growth?

- The need for comprehensive infrastructure modernization to accommodate bidirectional energy flows presents a key challenge to industry growth.

- A paramount challenge constraining the renewable distributed energy generation (rdeg) technologies market is the technical difficulty of grid integration, where high penetration can lead to reverse power flow issues and require grid upgrades costing 15-20% of the total project value. The legacy grid's limited hosting capacity acts as a significant bottleneck.

- A second formidable challenge involves critical supply chain constraints and exposure to geopolitical volatility, with over 80% of key components like smart inverters and battery cells concentrated in a few geographic regions. This raw material sourcing risk, coupled with high initial capital expenditure and difficulties in securing accessible financing for smaller projects, impedes faster market expansion despite favorable long-term economics.

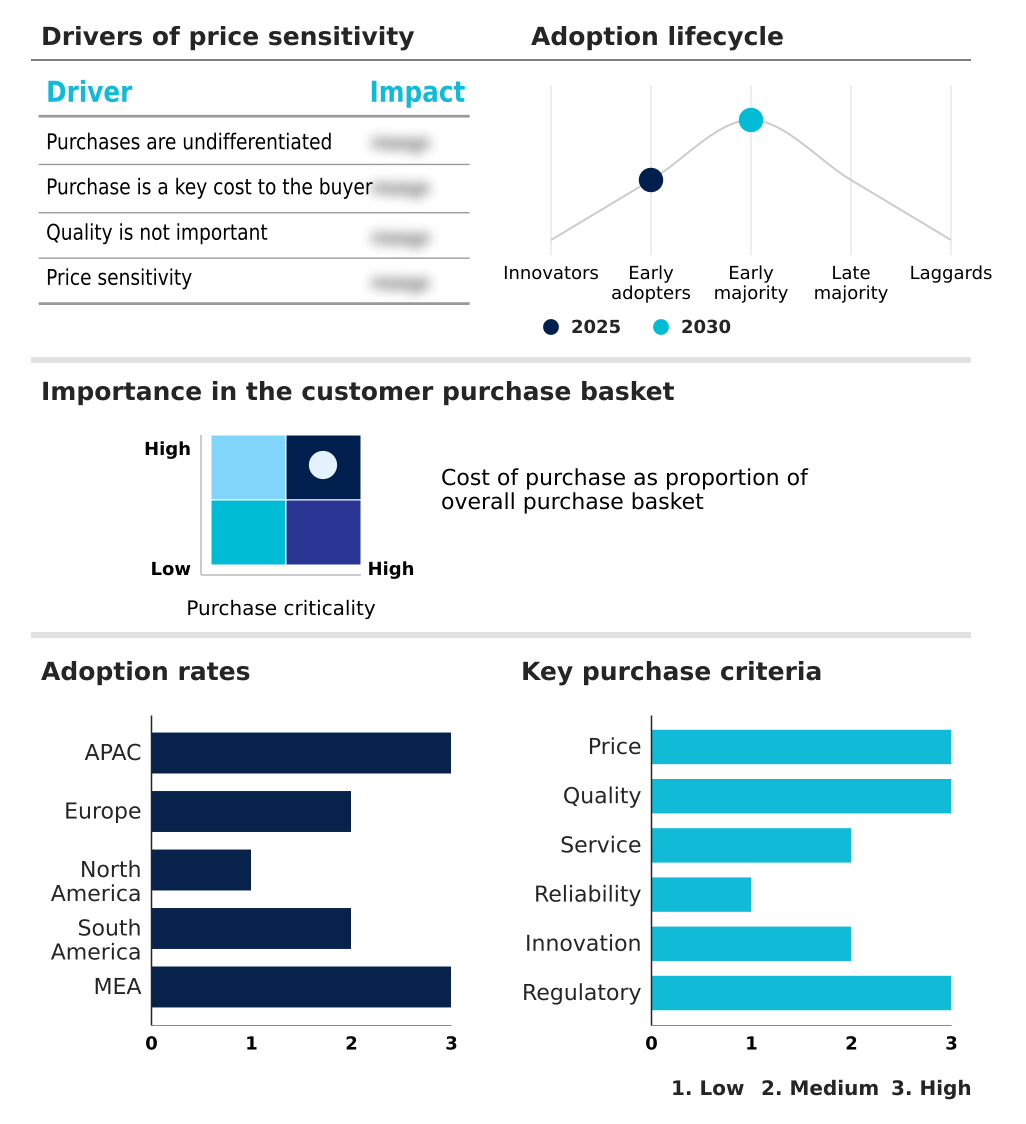

Exclusive Technavio Analysis on Customer Landscape

The renewable distributed energy generation (rdeg) technologies market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the renewable distributed energy generation (rdeg) technologies market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Renewable Distributed Energy Generation (RDEG) Technologies Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, renewable distributed energy generation (rdeg) technologies market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bloom Energy Corp. - Key offerings focus on integrated solutions, including solid oxide fuel cells, microgrids, and carbon capture technology, designed to enhance on-site power generation and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bloom Energy Corp.

- BYD Co. Ltd.

- Canadian Solar Inc.

- Caterpillar Inc.

- Enphase Energy Inc.

- Envision Group

- First Solar Inc.

- FuelCell Energy Inc.

- General Electric Co.

- Huawei Technologies Co. Ltd.

- JinkoSolar Holding Co. Ltd.

- Kingspan Group Plc

- LONGi Green Energy Co. Ltd.

- Northern Power Systems

- Schneider Electric SE

- Siemens AG

- SolarEdge Technologies Inc.

- Tesla Inc.

- Trina Solar Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Renewable Electricity industry, supportive government policies and ambitious renewable power targets have created a surge in demand for market-based approaches like feed-in tariffs and renewable portfolio standards, directly expanding the market for grid-tied renewable distributed energy generation (rdeg) technologies.

- A persistent decline in the levelized cost of energy for renewable technologies, driven by economies of scale in manufacturing and technological efficiencies, has made renewable distributed energy generation (rdeg) technologies economically competitive with conventional power, accelerating adoption for on-site self-consumption.

- The global push to decarbonize and address environmental concerns is driving a fundamental shift in the energy mix away from fossil fuels, creating sustained demand for renewable distributed energy generation (rdeg) technologies as a primary tool for achieving national climate goals and ensuring grid stability.

- Widespread grid modernization initiatives, including the deployment of smart grid solutions and advanced distribution management systems, are being undertaken to manage the technical challenges of grid integration and reverse power flow from high penetrations of renewable distributed energy generation (rdeg) technologies.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Renewable Distributed Energy Generation (RDEG) Technologies Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.7% |

| Market growth 2026-2030 | USD 189775.0 thousand |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.7% |

| Key countries | China, India, Japan, Australia, South Korea, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, US, Canada, Mexico, Brazil, Chile, Argentina, South Africa, Saudi Arabia, UAE, Egypt and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ecosystem for renewable distributed energy generation (rdeg) technologies is a complex value chain starting with suppliers of raw materials like polysilicon and lithium, where sourcing is concentrated in a few regions, creating potential bottlenecks.

- Manufacturers, including vertically integrated firms and specialized component makers, produce hardware such as solar pv panels, smart inverters, and energy storage systems, with the solar PV segment alone projected to constitute over 60% of the market. These products reach residential and commercial end-users through a fragmented network of installers and project developers.

- Regulatory bodies set interconnection standards and incentives like feed-in tariffs, while technology firms provide essential energy management systems and virtual power plants that enable grid integration and demand-side flexibility, crucial for managing a system with increasing decentralization.

What are the Key Data Covered in this Renewable Distributed Energy Generation (RDEG) Technologies Market Research and Growth Report?

-

What is the expected growth of the Renewable Distributed Energy Generation (RDEG) Technologies Market between 2026 and 2030?

-

The Renewable Distributed Energy Generation (RDEG) Technologies Market is expected to grow by USD 189.78 million during 2026-2030, registering a CAGR of 11.7%. Year-over-year growth in 2026 is estimated at 10.7%%. This acceleration is shaped by growing imperative for grid resilience and energy security, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Solar PV, Small wind turbines, and Biomass based generation), Connectivity (On-grid systems, Off-grid systems, and Hybrid), Application (Commercial, Industrial, and Residential) and Geography (APAC, Europe, North America, South America, Middle East and Africa). Among these, the Solar PV segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC, Europe, North America, South America and Middle East and Africa. APAC is estimated to contribute 54.2% to market growth during the forecast period. Country-level analysis includes China, India, Japan, Australia, South Korea, Indonesia, Germany, UK, France, Italy, The Netherlands, Spain, US, Canada, Mexico, Brazil, Chile, Argentina, South Africa, Saudi Arabia, UAE, Egypt and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is growing imperative for grid resilience and energy security, which is accelerating investment and industry demand. The main challenge is need for infrastructure modernization, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Renewable Distributed Energy Generation (RDEG) Technologies Market?

-

Key vendors include Bloom Energy Corp., BYD Co. Ltd., Canadian Solar Inc., Caterpillar Inc., Enphase Energy Inc., Envision Group, First Solar Inc., FuelCell Energy Inc., General Electric Co., Huawei Technologies Co. Ltd., JinkoSolar Holding Co. Ltd., Kingspan Group Plc, LONGi Green Energy Co. Ltd., Northern Power Systems, Schneider Electric SE, Siemens AG, SolarEdge Technologies Inc., Tesla Inc. and Trina Solar Co. Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for renewable distributed energy generation (rdeg) technologies is intensely fragmented, with the top ten vendors accounting for less than 40% of the market share. This environment fosters rapid innovation as companies vie for dominance. Key players like Enphase Energy Inc. and SolarEdge Technologies Inc.

- are pushing the boundaries of system intelligence, launching advanced microinverters and power optimizers that improve energy yield by up to 5%. These developments are a direct response to enterprise demand for higher efficiency and reliability. Major industrial conglomerates such as Siemens AG and Schneider Electric SE are focusing on integrated microgrid and energy storage solutions.

- This strategic shift addresses the critical challenge of grid integration by providing comprehensive systems that enhance grid stability and support the broader energy transition.

We can help! Our analysts can customize this renewable distributed energy generation (rdeg) technologies market research report to meet your requirements.

RIA -

RIA -