Satellite Internet Market Size 2026-2030

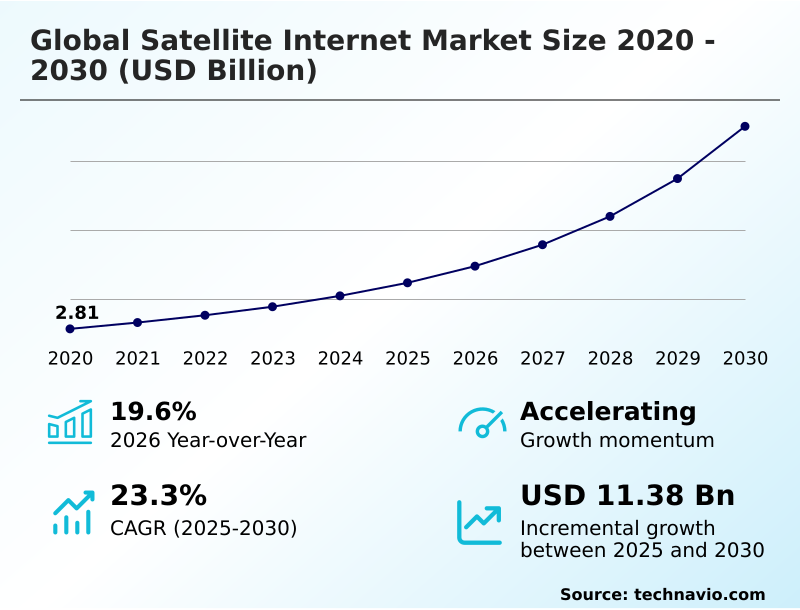

The satellite internet market size is valued to increase by USD 11.38 billion, at a CAGR of 23.3% from 2025 to 2030. Escalating global demand for connectivity in unserved and underserved geographic areas will drive the satellite internet market.

Major Market Trends & Insights

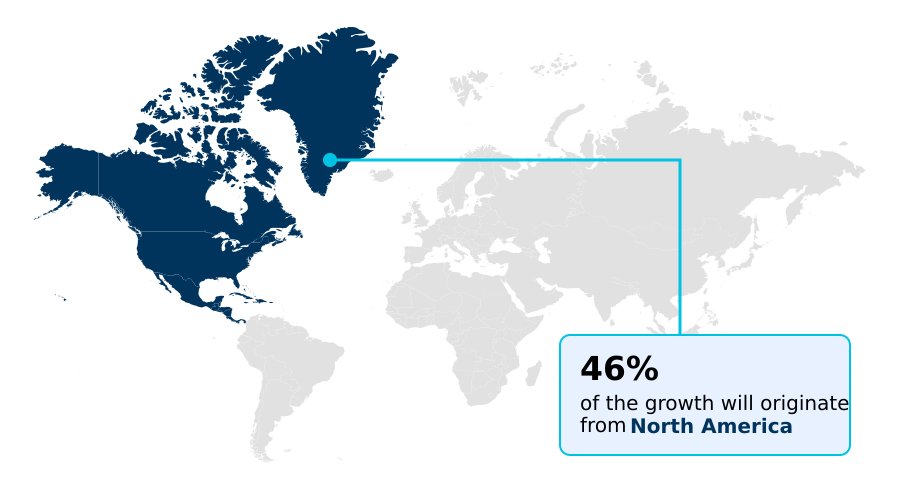

- North America dominated the market and accounted for a 45.5% growth during the forecast period.

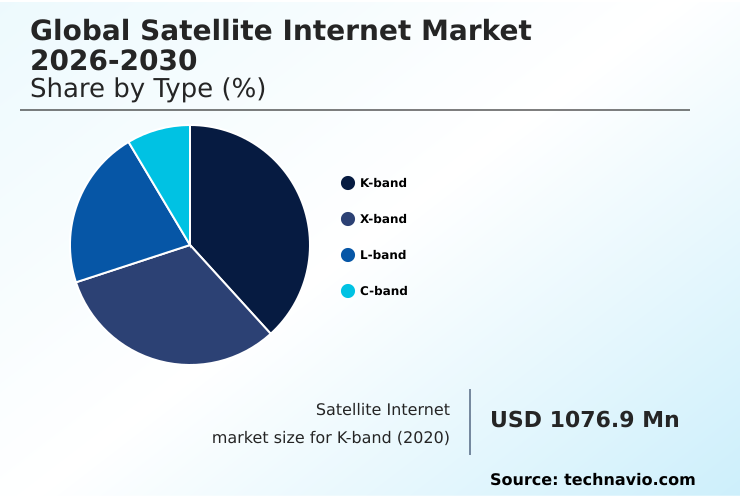

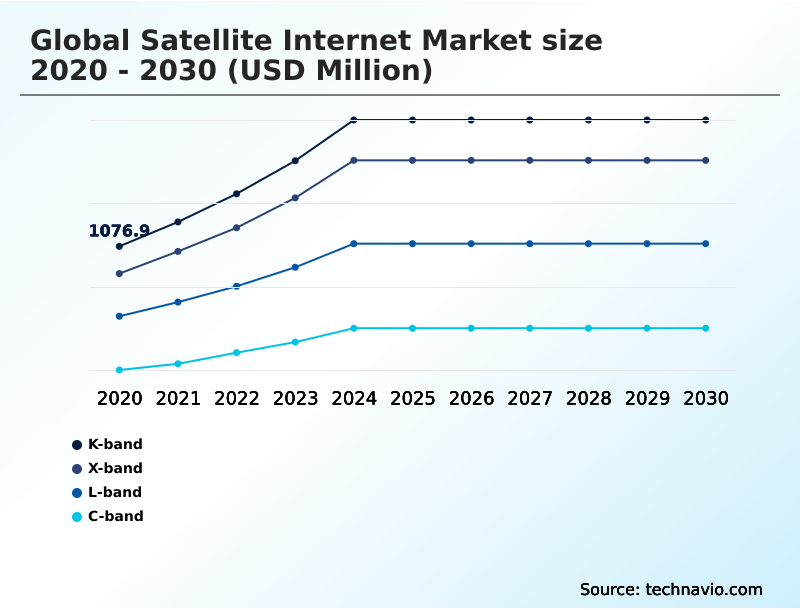

- By Type - K-band segment was valued at USD 1.93 billion in 2024

- By End-user - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 14.72 billion

- Market Future Opportunities: USD 11.38 billion

- CAGR from 2025 to 2030 : 23.3%

Market Summary

- The satellite internet market is undergoing a significant transformation, driven by the imperative to deliver high-speed broadband to regions beyond the reach of terrestrial infrastructure. Technological advancements, particularly in low earth orbit constellations and high-throughput satellites, are fundamentally lowering signal latency and increasing network capacity, making satellite a viable alternative for residential and enterprise use.

- This evolution supports a wide array of applications, from enabling remote work and online education in rural communities to providing critical connectivity for maritime and aviation mobility. For instance, a global logistics company can leverage satellite IoT connectivity to track assets in real-time across oceans and remote land routes, optimizing supply chains and enhancing security where cellular coverage is nonexistent.

- However, the industry grapples with immense capital expenditure for network deployment, complex global frequency allocation, and the challenge of making user terminals affordable for mass adoption. These dynamics create a competitive landscape where technological innovation, strategic partnerships, and scalable business models are essential for success.

What will be the Size of the Satellite Internet Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Satellite Internet Market Segmented?

The satellite internet industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- K-band

- X-band

- L-band

- C-band

- End-user

- Commercial

- Non-commercial

- Connectivity

- Two-way service

- One-way service

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- South Africa

- UAE

- Rest of World (ROW)

- North America

By Type Insights

The k-band segment is estimated to witness significant growth during the forecast period.

The K-band segment, utilizing both Ku-band and Ka-band spectrum, is pivotal for high-speed data transmission. Its use of higher frequencies facilitates high-throughput satellite (HTS) systems, which employ spot beam technology and advanced digital signal processing to serve data-intensive applications.

This capability is crucial for delivering broadband to residential subscribers and enterprise satellite networks. The development of electronically steered antennas allows for more compact and efficient user terminals, a key factor in expanding into consumer markets.

While susceptible to rain fade, advanced rain fade mitigation techniques ensure high service availability, with modern systems achieving over 99.5% uptime.

The band's high spectral efficiency is essential for network capacity management, supporting both geostationary satellites and emerging non-geostationary satellite orbit constellations.

The K-band segment was valued at USD 1.93 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 45.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Satellite Internet Market Demand is Rising in North America Get Free Sample

The geographic landscape of the satellite internet market is defined by a strategic focus on bridging the digital divide, with North America leading in market share, commanding over 45% of the global opportunity.

This dominance is fueled by government-backed initiatives providing satellite internet for rural areas and strong demand from enterprise satellite networks.

The APAC region is the fastest-growing market, projected to expand at a rate of 24.0%, driven by the need for remote connectivity solutions across its vast archipelagos and remote territories.

In Europe, the focus is on achieving ubiquitous coverage and providing satellite for 5G backhaul. In contrast, markets in South America and the Middle East and Africa are leveraging satellite IoT connectivity to modernize key industries like agriculture and energy.

Global satellite coverage is expanding, with providers offering commercial satellite internet services tailored to regional demands for disaster recovery communications and government satellite communications.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decisions in the satellite internet market are increasingly shaped by nuanced performance and cost considerations. For businesses evaluating business continuity, understanding the cost of satellite internet for business continuity versus the potential losses from terrestrial outages is critical.

- A key question is how does satellite internet reduce latency, as this directly impacts the viability of applications like real-time financial transactions and cloud computing, where LEO systems show a performance improvement of over 900% compared to traditional GEO.

- The satellite internet vs fiber optic speed comparison remains a central debate, with fiber leading in raw speed but satellite offering unparalleled geographic reach. Further complexities arise from the technical and regulatory challenges of LEO satellite deployment, which include addressing orbital debris mitigation strategies for LEO and navigating the regulatory hurdles for global satellite operators.

- Technology choices are also pivotal; the efficiency of phased array antenna technology for satellite terminals determines hardware cost and user experience, while the impact of rain fade on ka-band satellite signal dictates reliability in certain climates. Enterprises are leveraging software-defined wide area network with satellite links for resilient, hybrid connectivity.

- The expansion into new use cases, such as direct-to-device satellite messaging services and using satellite for cellular backhaul in remote areas, highlights the market's broadening scope and the growing importance of spectral efficiency techniques in satellite communication.

What are the key market drivers leading to the rise in the adoption of Satellite Internet Industry?

- The escalating global demand for high-speed connectivity in unserved and underserved geographic areas serves as a foundational driver for the satellite internet market's expansion.

- Escalating demand for reliable connectivity in unserved regions remains the primary driver for the satellite internet market. Government-led initiatives are accelerating the adoption of residential satellite broadband, aiming to connect millions of households and bridge the digital divide.

- In the enterprise sector, industries such as agriculture and energy are leveraging satellite internet for remote work and operations, achieving productivity gains of over 25% in off-grid locations.

- The expansion of enterprise satellite networks is also crucial for business continuity, with satellite network redundancy offering a vital backup during terrestrial outages.

- This diversification into high-value mobility and enterprise applications, including military satellite communications and disaster recovery communications, is creating new revenue streams and solidifying the market's essential role in the global infrastructure.

What are the market trends shaping the Satellite Internet Industry?

- The proliferation and operational maturation of low earth orbit constellations represents a defining market trend. This architectural shift is fundamentally reshaping service performance and accessibility for a global user base.

- The satellite internet market is increasingly defined by the maturation of non-geostationary satellite orbit systems, which provide high-speed low-latency satellite internet. This trend is unlocking new commercial satellite internet applications in aviation and maritime sectors, with in-flight connectivity solutions showing a 50% increase in adoption rates by major airlines.

- Another key development is the deepening integration with terrestrial systems, particularly satellite for 5G backhaul, which can accelerate rural network deployment by up to 70% compared to fiber-only approaches. The emergence of direct-to-device connectivity is creating a new paradigm for public safety communications and satellite IoT connectivity.

- These shifts are transforming satellite from a niche service to an integral part of the global telecommunications fabric, driven by demand for ubiquitous global satellite coverage.

What challenges does the Satellite Internet Industry face during its growth?

- The confluence of spectrum scarcity and complex regulatory hurdles presents a significant challenge to the satellite internet industry's growth trajectory and operational scalability.

- The satellite internet market grapples with significant operational and financial challenges. The high cost of user terminals remains a primary barrier to mass adoption, particularly for residential satellite broadband in developing regions. To mitigate this, some providers subsidize hardware by up to 60%, impacting short-term profitability.

- Furthermore, the immense capital required for building and maintaining ground segment infrastructure and gateway earth stations creates a high barrier to entry. On the regulatory front, complex and fragmented rules for frequency allocation and orbital debris mitigation add significant operational overhead and can delay service rollouts by 18-24 months in some jurisdictions.

- Intensifying competition is also compressing margins, forcing providers to innovate continuously in areas like link budget analysis to stay viable.

Exclusive Technavio Analysis on Customer Landscape

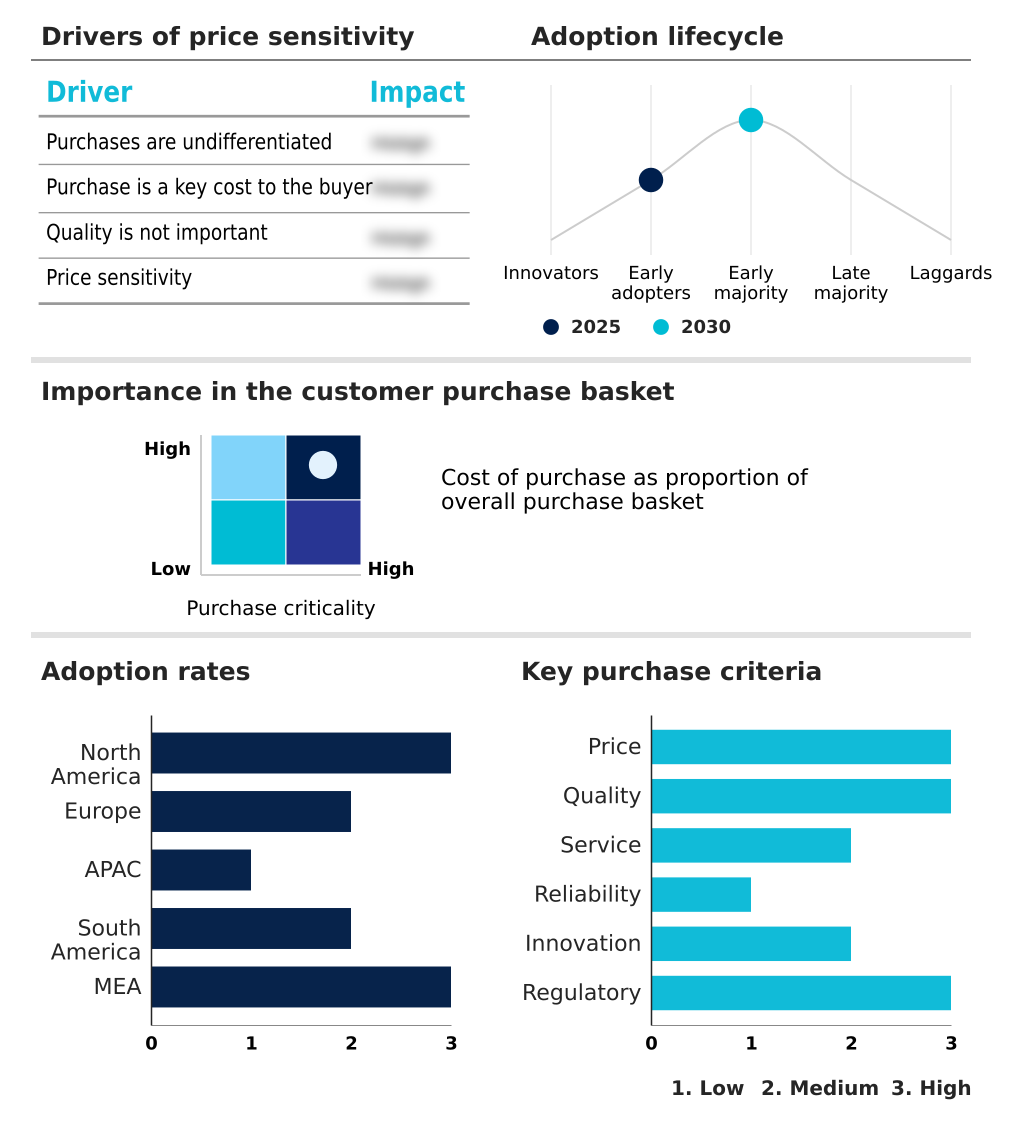

The satellite internet market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the satellite internet market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Satellite Internet Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, satellite internet market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Offers global broadband connectivity via its Starlink constellation, targeting residential, business, and mobility sectors with high-speed, low-latency satellite internet services.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Amazon.com Inc.

- AXESS Network

- EchoStar Corp.

- Eutelsat S.A.

- Gilat Satellite Networks Ltd.

- Globalstar Inc.

- Intelsat US LLC

- Iridium Communications Inc.

- Kepler Communications Inc.

- Marlink SAS

- SES SA

- Space Exploration Tech. Corp.

- Speedcast

- Telesat Corp.

- Thaicom Public Co. Ltd.

- Thales Group

- The Boeing Co.

- Viasat Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Satellite internet market

- In December, 2024, the European Commission signed a concession contract with the SpaceRISE consortium to develop, deploy, and operate the new IRIS² secure satellite system, aiming to provide communication services to governmental users and broadband connectivity across Europe.

- In March, 2025, Telesat Corp. received formal backing from the Canadian government for a new campus in Gatineau, Quebec, to serve as the operations center for its Telesat Lightspeed LEO satellite network, a project supported by over CAD 2.5 billion in government loans.

- In April, 2025, Amazon.com Inc.'s subsidiary, Kuiper Systems, successfully launched its first 27 prototype satellites for its Project Kuiper constellation, marking its official entry into the LEO broadband market and beginning its network deployment phase.

- In May, 2025, Space Exploration Tech. Corp. launched a record-setting batch of 29 lighter V2 Mini Optimized satellites for its Starlink network, enabling the company to double its user base to over 9 million subscribers globally within the same year.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Satellite Internet Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 23.3% |

| Market growth 2026-2030 | USD 11378.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 19.6% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Chile, Saudi Arabia, South Africa, UAE, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The satellite internet market's trajectory is being redrawn by rapid technological advancements, compelling a strategic pivot at the boardroom level. The widespread deployment of low earth orbit constellations and multi-orbit networks is fundamentally altering performance benchmarks, with next-generation high throughput satellite systems delivering unprecedented network capacity.

- This evolution is driven by innovations in ground segment infrastructure, including sophisticated gateway earth stations and advanced digital signal processing. A critical enabler has been the development of reusable launch vehicles, which have drastically lowered deployment costs. For end-users, technologies like electronically steered antennas and phased array antennas are making user terminals more compact and efficient.

- These shifts directly impact capital allocation and product strategy, forcing operators to balance innovation with profitability. For instance, the implementation of advanced beamforming technologies can increase spectral efficiency by 30%, a key metric for maximizing return on invested capital.

- This competitive environment demands continuous investment in technologies from Ka-band spectrum optimization to rain fade mitigation and orbital debris mitigation to maintain market leadership.

What are the Key Data Covered in this Satellite Internet Market Research and Growth Report?

-

What is the expected growth of the Satellite Internet Market between 2026 and 2030?

-

USD 11.38 billion, at a CAGR of 23.3%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (K-band, X-band, L-band, and C-band), End-user (Commercial, and Non-commercial), Connectivity (Two-way service, One-way service, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating global demand for connectivity in unserved and underserved geographic areas, Spectrum scarcity and complex regulatory hurdles

-

-

Who are the major players in the Satellite Internet Market?

-

Airbus SE, Amazon.com Inc., AXESS Network, EchoStar Corp., Eutelsat S.A., Gilat Satellite Networks Ltd., Globalstar Inc., Intelsat US LLC, Iridium Communications Inc., Kepler Communications Inc., Marlink SAS, SES SA, Space Exploration Tech. Corp., Speedcast, Telesat Corp., Thaicom Public Co. Ltd., Thales Group, The Boeing Co. and Viasat Inc.

-

Market Research Insights

- The satellite internet market's dynamism is driven by a convergence of technological innovation and expanding use cases, creating new value propositions for diverse end-users. The deployment of hybrid satellite-terrestrial networks is improving network resilience by over 40% for enterprise clients, ensuring robust business continuity solutions.

- Meanwhile, advancements in portable satellite internet are enabling reliable remote connectivity solutions for industries like agriculture and energy, boosting operational efficiency in off-grid environments. The shift toward low-latency satellite internet is critical, with performance tests showing a reduction in data transmission delays of up to 95% compared to legacy systems.

- This makes applications like real-time public safety communications and telemedicine feasible in previously disconnected areas. These shifts underscore a move from niche connectivity to an integrated component of global telecommunications.

We can help! Our analysts can customize this satellite internet market research report to meet your requirements.

RIA -

RIA -