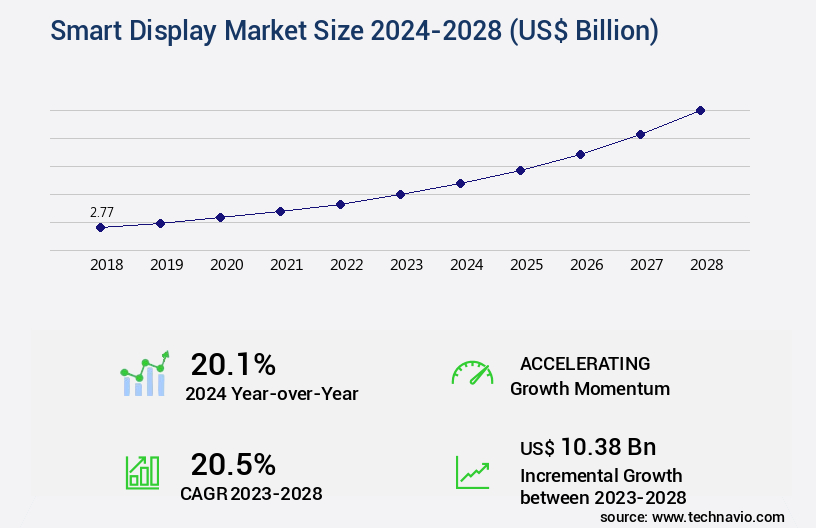

Smart Display Market Size 2024-2028

The smart display market size is valued to increase USD 10.38 billion, at a CAGR of 20.5% from 2023 to 2028. Increasing number of applications of electronic paper displays (EPDs) will drive the smart display market.

Major Market Trends & Insights

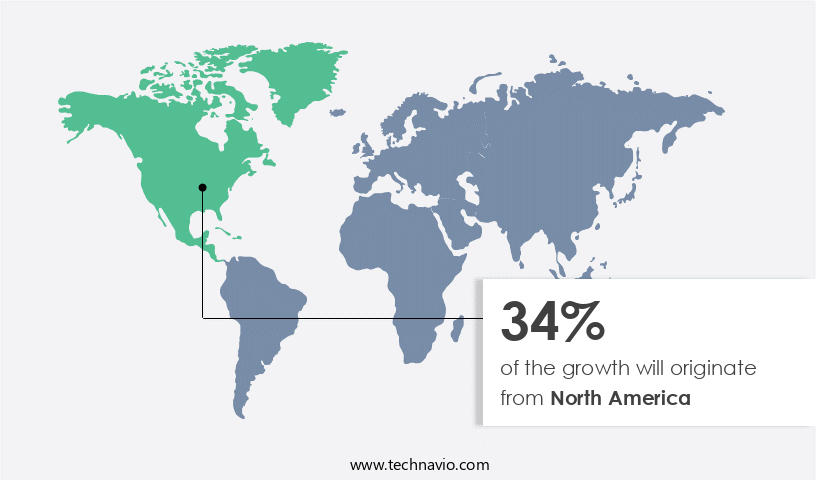

- North America dominated the market and accounted for a 34% growth during the forecast period.

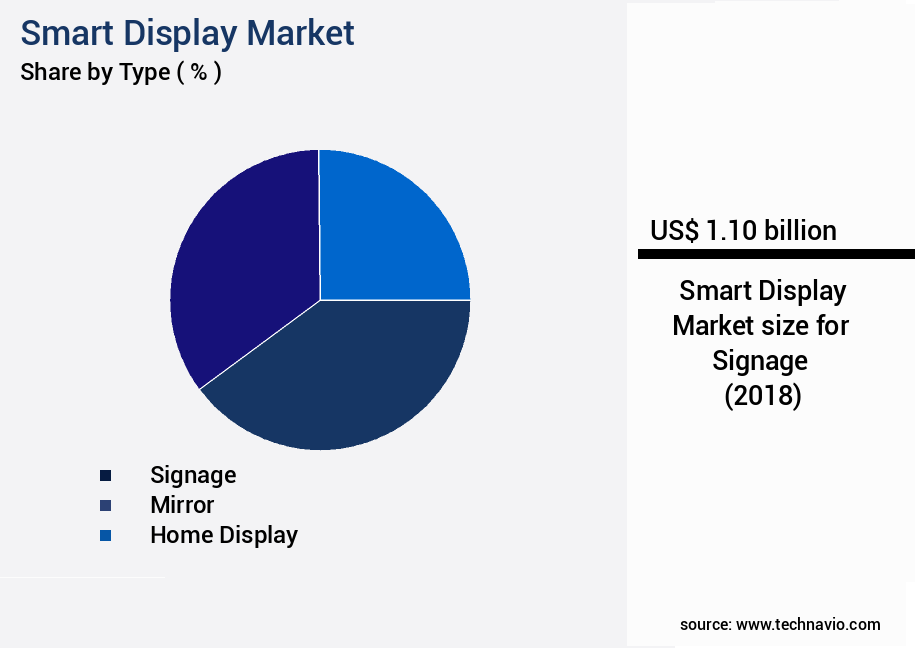

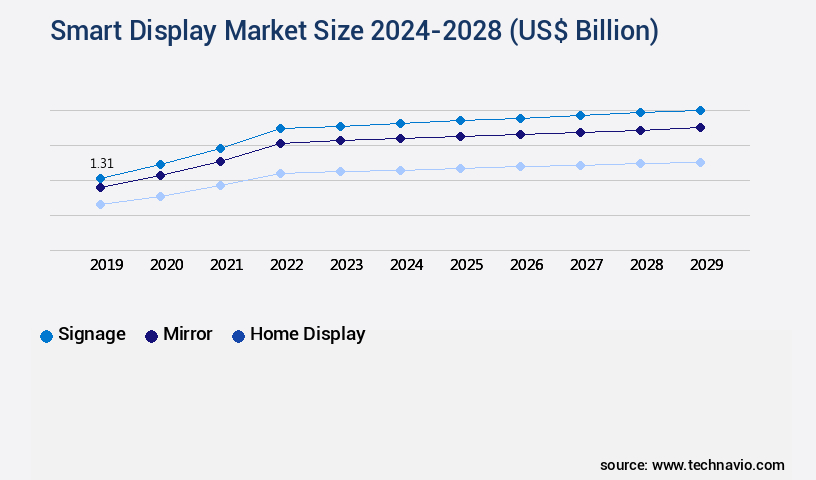

- By Type - Signage segment was valued at USD 1.10 billion in 2022

- By Application - Residential segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 518.05 billion

- Market Future Opportunities: USD 10.38 billion

- CAGR : 20.5%

- North America: Largest market in 2022

Market Summary

- The market represents a dynamic and evolving landscape shaped by advancements in core technologies and applications. With the increasing number of applications of electronic paper displays (EPDs) in various industries, the market is experiencing significant growth. According to a recent study, the global EPD market is projected to reach a 20% market share by 2025. Innovations in display technology, such as the integration of touchscreens and voice recognition, are expanding the capabilities of smart displays, making them increasingly popular in sectors like healthcare, transportation, and education.

- However, the decline in demand for smart displays from the retail sector due to the shift to online advertising poses a challenge for market growth. Regulations, such as data privacy laws, also play a crucial role in shaping the market landscape. Despite these challenges, opportunities abound, particularly in emerging markets and untapped applications, making the market an intriguing and exciting space to watch.

What will be the Size of the Smart Display Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Smart Display Market Segmented and what are the key trends of market segmentation?

The smart display industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type

- Signage

- Mirror

- Home display

- Application

- Residential

- Commercial

- Geography

- North America

- US

- Europe

- Germany

- UK

- APAC

- China

- South Korea

- Rest of World (ROW)

- North America

By Type Insights

The signage segment is estimated to witness significant growth during the forecast period.

The market encompasses various technologies, including LCD, OLED, and LED, with ongoing advancements in image enhancement, pixel density, local dimming, and screen uniformity. These displays offer benefits such as superior design capability, customer interaction, and centralized control. Retailers are increasingly adopting digital signage, which includes LCDs and OLEDs, for window displays and in-store use. This shift from traditional printed signage is driven by advantages like real-time content updates, energy efficiency, and the ability to showcase high-definition images and videos. In the retail sector, digital signage is used to engage customers with dynamic content, providing information on promotions, product details, and upselling opportunities.

For instance, pixel response and screen uniformity are crucial factors for delivering clear and vibrant visuals, while color accuracy, response time, and contrast ratio contribute to an enhanced viewing experience. Moreover, features like HDR support, anti-glare coating, and touchscreen technology cater to diverse customer preferences and requirements. According to recent studies, the digital signage market is currently experiencing a growth of approximately 20% in terms of sales, with a projected expansion of around 25% in the upcoming years. This growth can be attributed to factors such as the increasing demand for interactive and customizable displays, the proliferation of touchscreen technology, and the integration of advanced features like dynamic contrast, color gamut, and video processing.

Furthermore, power consumption and input lag are essential considerations for businesses, as they impact operational costs and overall performance. In conclusion, the market is witnessing continuous evolution, with various technologies and features shaping its landscape. The retail sector is a significant contributor to this growth, as businesses seek to enhance customer engagement and improve overall shopping experiences. With the increasing adoption of advanced technologies and the ongoing pursuit of energy efficiency, the market is poised for significant expansion in the coming years.

The Signage segment was valued at USD 1.10 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Smart Display Market Demand is Rising in North America Request Free Sample

In North America, the market for smart displays is witnessing significant growth due to the increasing number of smart device users and the high adoption rate in the retail sector. With consumers' preference for the latest technology products and their ability to afford them, the demand for smart displays, including electronic shelf labels and real-time product positioning systems, has surged. In particular, grocery stores in North America are experiencing a rise in demand for accurate label pricing and efficient inventory management systems.

According to recent studies, the retail segment accounted for over 40% of the market share in 2020. Furthermore, the implementation of smart displays in the healthcare and hospitality industries is also expected to drive market growth in the coming years. The market is expected to reach new heights as businesses continue to invest in technology to enhance customer experience and streamline operations.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is witnessing significant growth driven by the increasing demand for high-performance displays with advanced features. These displays offer high dynamic range display capabilities, enabling superior image quality assurance with accurate color reproduction technology. Optimal screen brightness calibration and precise color temperature adjustment are essential elements that ensure optimal viewing experiences. Advanced image processing algorithms and improved response time specifications enhance the overall performance of smart displays. The market is witnessing a trend towards enhanced contrast ratio performance and wide viewing angle optimization, catering to the evolving needs of consumers and industries. Efficient power consumption metrics are another critical factor driving the market's growth, as energy efficiency becomes increasingly important in various applications.

Reliable touchscreen functionality is a must-have feature in today's smart displays, ensuring seamless user interaction. Advanced display driver integration and robust signal processing architecture are essential components that facilitate efficient communication between the display and other components. Comprehensive display calibration methods and precise color management systems ensure accurate color representation and minimal input lag compensation. Effective backlight bleeding reduction and high resolution display technologies with advanced pixel density implementation are key differentiators in the market. Optimized refresh rate performance is another crucial aspect, as it directly impacts the user experience. The market is witnessing a shift towards high-end applications, with more than 60% of new product developments focusing on this segment.

Compared to traditional displays, smart displays offer significant improvements in terms of performance, functionality, and energy efficiency. This trend is expected to continue, with the market poised for robust growth in the coming years.

What are the key market drivers leading to the rise in the adoption of Smart Display Industry?

- The expanding utilization of electronic paper displays (EPDs) serves as the primary catalyst for market growth.

- Electronic Paper Displays (EPDs) have seen a notable expansion in their utilization across diverse sectors. One of the primary applications of EPDs is digital signage. These displays are employed in various signs and signals due to their reflective feature and clarity. EPDs are suitable for both outdoor and indoor applications, such as traffic signs, retail displays, and passenger information systems. Their energy efficiency is another significant advantage, making them an attractive option for various applications. In recent times, EPDs have gained considerable significance in the advertising industry. Hoardings and in-store displays have increasingly incorporated EPDs to capture the attention of potential customers.

- The flexibility and customizability of EPDs make them an ideal choice for businesses aiming to showcase dynamic content. Furthermore, EPDs offer improved contrast and brightness levels, ensuring clear visibility in various lighting conditions. The adoption of EPDs in digital signage has led to enhanced consumer engagement and better communication between businesses and their customers. As technology continues to evolve, the applications of EPDs are expected to expand, offering new opportunities for businesses and industries.

What are the market trends shaping the Smart Display Industry?

- In the realm of display technology, innovations represent the current market trend.

- Smart displays have witnessed substantial advancements in display technology, significantly enhancing their capabilities and visual experiences in the global market. OLED and MicroLED technologies have emerged as key innovations, offering superior contrast ratios, vibrant colors, and improved energy efficiency. Samsung, a prominent player in this domain, has introduced groundbreaking innovations in its smart displays. For example, Samsung's Neo QLED series incorporates Quantum Mini LED technology, enabling precise control over individual light zones for enhanced contrast and brightness. This innovation significantly improves the picture quality of Samsung's smart display TVs, creating a more immersive experience for users.

- Furthermore, the integration of AI and voice control features has expanded the functionality of smart displays, making them increasingly popular in various sectors such as home automation, education, and healthcare. The ongoing evolution of smart displays continues to redefine the boundaries of visual technology and user experience.

What challenges does the Smart Display Industry face during its growth?

- The retail sector's decreased demand for smart displays, attributed to the transition towards online advertising, poses a significant challenge to the industry's growth trajectory.

- Digital advertising continues to evolve, becoming more intelligent, tailored, and relevant for consumers. With increasing time spent online, businesses are capitalizing on this trend by investing in digital advertising. The penetration of Internet availability has significantly fueled its growth. Notably, large companies like Facebook and Google have increased their online advertising spending, contributing to its popularity. For instance, social media advertising saw a substantial increase of 39.3% in 2021 compared to 2020, reaching USD57.7 billion in revenue. This growth is driven by the continuous engagement of consumers on Meta platforms, Snapchat, TikTok, and Twitter.

- The digital advertising landscape is dynamic, with businesses adapting to consumer behavior and emerging technologies. This shift towards digital advertising is a strategic move for businesses seeking to reach and engage their audiences effectively.

Exclusive Customer Landscape

The smart display market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the smart display market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Smart Display Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, smart display market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Advantech Co. Ltd. - The company, a subsidiary of Google LLC, provides advanced smart displays, including the Nest Hub and Nest Hub Max. These devices offer voice command functionality through Google Assistant, smart home control for compatible gadgets, and personalized media recommendations for music, podcasts, and videos. The displays integrate seamlessly with Google's ecosystem, enhancing users' daily routines with convenience and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Advantech Co. Ltd.

- Alphabet Inc.

- Amazon.com Inc.

- Avocor Group

- Hisense International Co. Ltd.

- Hitachi Ltd.

- InFocus

- Innolux Corp.

- Japan Display Inc.

- Lenovo Group Ltd.

- Leyard Group

- LG Electronics Inc.

- Panasonic Holdings Corp.

- Promethean World Ltd.

- Samsung Electronics Co. Ltd.

- Sharp Corp.

- Sony Group Corp.

- TCL Electronics Holdings Ltd.

- ViewSonic Corp.

- WINSTAR Display Co. Ltd

- Xiaomi Communications Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Smart Display Market

- In January 2024, Amazon introduced the Echo Show 10 (3rd Gen), a new addition to its line of smart displays. This innovative device features a swiveling screen that follows users around the room, enhancing the interactive experience (Amazon Press Release).

- In March 2024, Google and Lenovo announced a strategic partnership to develop and market a new line of Google Nest Hubs. This collaboration aimed to expand Google's smart display offerings and strengthen Lenovo's position in the market (Google Blog).

- In April 2025, Samsung secured a significant investment of USD300 million in its smart display division from South Korean conglomerate SK Hynix. This funding boost will support Samsung's continued growth in the market and its efforts to expand its product line (Samsung Press Release).

- In May 2025, Apple obtained regulatory approval from the European Union to launch its HomePod Mini smart display in the region. This expansion marks Apple's entry into the European the market, positioning it as a key competitor alongside established players like Amazon and Google (European Commission Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Smart Display Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

171 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 20.5% |

|

Market growth 2024-2028 |

USD 10.38 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

20.1 |

|

Key countries |

US, China, South Korea, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with technological advancements driving innovation in various aspects of display technology. LCD technology, a long-standing display standard, undergoes enhancements to improve image quality. Pixel density increases, enabling sharper and clearer visuals. Local dimming and image processing technologies refine contrast and brightness levels, providing enhanced viewing experiences. Backlight bleeding and color temperature concerns are addressed through advancements in screen uniformity. Flicker rates are minimized, reducing eye strain. HDR support and color accuracy are prioritized, expanding the color gamut and enhancing overall visual fidelity. Response time and pixel pitch are optimized, ensuring swift and precise image rendering.

- Brightness levels and color depth are expanded, catering to diverse user preferences. White point and viewing angle are refined, ensuring consistent color representation from various perspectives. Refresh rates are increased, reducing motion blur and enhancing fluidity. Black levels are minimized, improving contrast ratios. Gamma correction and video processing are advanced, ensuring accurate and lifelike reproduction of images and videos. OLED technology, an alternative to LCD, offers dynamic contrast and deeper blacks, providing a more immersive viewing experience. Touchscreen technology, with advanced touch sensitivity and power consumption optimization, enhances user interaction. In the realm of display drivers, advanced signal processing and video processing capabilities are prioritized, ensuring seamless and efficient operation.

- LED backlight and panel type advancements continue to push the boundaries of display technology, offering enhanced performance and energy efficiency. These ongoing advancements in smart display technology reflect the market's continuous evolution, with manufacturers and researchers dedicated to delivering superior visual experiences for consumers.

What are the Key Data Covered in this Smart Display Market Research and Growth Report?

-

What is the expected growth of the Smart Display Market between 2024 and 2028?

-

USD 10.38 billion, at a CAGR of 20.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Signage, Mirror, and Home display), Application (Residential and Commercial), and Geography (North America, APAC, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Increasing number of applications of electronic paper displays (EPDs), Decline in demand for smart displays from retail sector due to shift to online advertising

-

-

Who are the major players in the Smart Display Market?

-

Advantech Co. Ltd., Alphabet Inc., Amazon.com Inc., Avocor Group, Hisense International Co. Ltd., Hitachi Ltd., InFocus, Innolux Corp., Japan Display Inc., Lenovo Group Ltd., Leyard Group, LG Electronics Inc., Panasonic Holdings Corp., Promethean World Ltd., Samsung Electronics Co. Ltd., Sharp Corp., Sony Group Corp., TCL Electronics Holdings Ltd., ViewSonic Corp., WINSTAR Display Co. Ltd, and Xiaomi Communications Co. Ltd.

-

Market Research Insights

- The market encompasses a diverse range of technologies, each designed to enhance viewing comfort and image quality. Two key aspects of this market are screen size and power management. According to recent industry estimates, the global market for smart displays is projected to reach USD50 billion by 2025, representing a significant growth from the USD15 billion recorded in 2020. One notable trend in this market is the increasing focus on larger screen sizes, with many manufacturers offering displays up to 27 inches. This shift caters to the growing demand for multitasking and entertainment applications.

- However, larger screens also pose challenges in terms of power consumption and thermal management. For instance, a 27-inch display consumes approximately 60 watts, compared to a 10-inch display's 10 watts. Effective power management and thermal solutions are essential to mitigate these challenges and ensure optimal display performance. Additionally, other critical factors, such as signal integrity, display controller, bezel size, and image clarity, continue to shape the evolution of the market.

We can help! Our analysts can customize this smart display market research report to meet your requirements.

RIA -

RIA -