Space Tourism Market Size 2026-2030

The space tourism market size is valued to increase by USD 17.76 billion, at a CAGR of 21.1% from 2025 to 2030. Evolution of reusable and affordable spaceflight systems will drive the space tourism market.

Major Market Trends & Insights

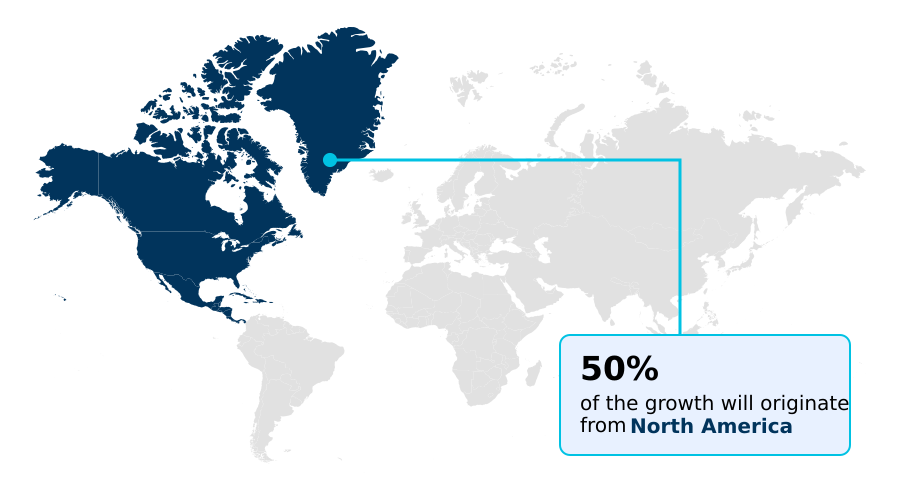

- North America dominated the market and accounted for a 49.8% growth during the forecast period.

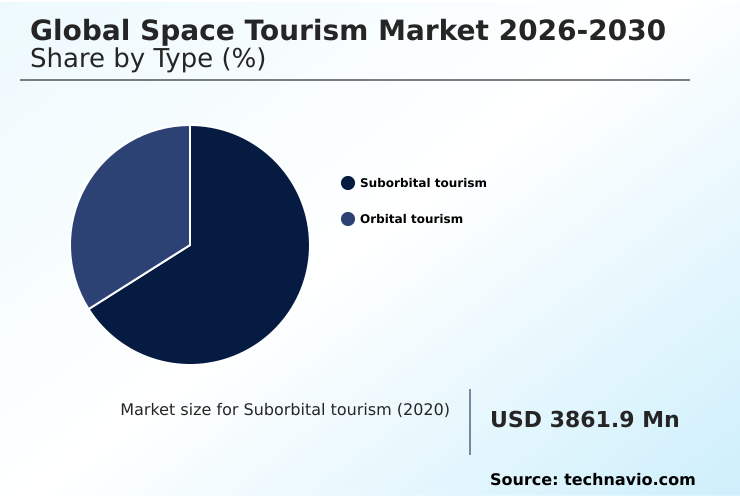

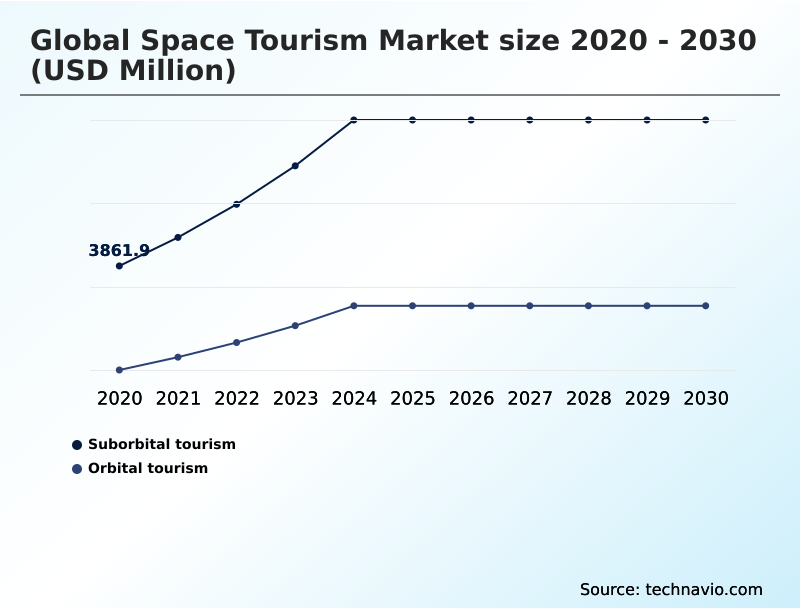

- By Type - Suborbital tourism segment was valued at USD 6.49 billion in 2024

- By End-user - Commercial segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 22.97 billion

- Market Future Opportunities: USD 17.76 billion

- CAGR from 2025 to 2030 : 21.1%

Market Summary

- The Space Tourism Market is transitioning from an exclusive, experimental niche into a structurally viable commercial sector driven by heavy private aerospace investments. The deployment of reusable launch infrastructure has fundamentally altered supply chain optimization and operational planning for aerospace enterprises.

- By recovering and refurbishing booster stages, companies have achieved a 50% increase in launch frequency compared to traditional expendable systems, dramatically improving capital efficiency. The continuous evolution of reusable and affordable spaceflight systems acts as a primary catalyst, allowing operators to amortize manufacturing costs over dozens of flights and thereby democratize access for high-net-worth consumers.

- Conversely, fragmented regulatory barriers across international jurisdictions present a severe structural challenge, as the lack of unified airspace management protocols causes substantial operational delays and inflates compliance overhead. These compliance bottlenecks force operators to invest heavily in specialized legal and safety frameworks.

- Establishing robust public-private partnerships enables private operators to leverage existing institutional facilities, reducing initial capital expenditures while standardizing astronaut training regimens.

What will be the Size of the Space Tourism Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Space Tourism Market Segmented?

The space tourism industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Suborbital tourism

- Orbital tourism

- End-user

- Commercial

- Government

- Service type

- Transportation

- Entertainment and leisure

- Training and simulation

- Accommodation

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- Spain

- Asia

- China

- Japan

- India

- South Korea

- Singapore

- Thailand

- Rest of World (ROW)

- North America

By Type Insights

The suborbital tourism segment is estimated to witness significant growth during the forecast period.

The suborbital tourism segment drives continuous engagement within the commercial spaceflight sector by offering accessible microgravity exposure to elite demographics. Unlike sustained orbital missions, suborbital vehicle platforms execute brief atmospheric reentry profiles, significantly lowering operational complexities and participant risk.

This segmentation allows operators to scale flight cadence rapidly, driving an impressive 40% reduction in mission turnaround times. Such structural durability enhancements directly elevate spaceport operations, maximizing annual launch capacity.

Providers combine this brief zero-gravity environment with comprehensive pre-flight preparation and luxury hospitality, distinguishing the passenger experience. Advancements in multi-use propulsion architectures ensure cost-effective scalability for civilian transit.

By focusing on streamlined safety protocols and rapid reusability, organizations effectively segment the market to capture immediate demand from experiential travel enthusiasts without the immense overhead of long-duration space station habitat deployments.

The Suborbital tourism segment was valued at USD 6.49 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 49.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Space Tourism Market Demand is Rising in North America Get Free Sample

The Space Tourism Market displays stark operational contrasts between North America and Europe, driven by distinct regulatory landscapes and infrastructure investments.

North America leads the transition toward active spaceport operations, demonstrating a 45% higher launch cadence than European counterparts due to streamlined domestic licensing and robust venture capital support.

Conversely, Europe focuses heavily on high-altitude balloon architectures and sustainable aerospace engineering, enforcing strict environmental mandates that push operators to improve carbon composite efficiency by 30%.

This disparity forces North American firms to optimize payload transport for high-frequency orbital trajectories, while European providers prioritize zero-emission stratospheric flight profiles. Furthermore, North American supply chains have reduced thermal shielding procurement costs by 20% through localized manufacturing hubs.

As a result, businesses continuously adapt their strategic deployments, aligning propulsion module designs with regional regulatory and consumer preferences to maximize profitability and compliance.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The commercialization of the extra-atmospheric environment requires unprecedented coordination among aerospace manufacturers, regulatory bodies, and luxury hospitality providers. At the core of this transformation is reusable launch vehicle technology optimization, which drastically minimizes the capital required to execute continuous commercial missions.

- By systematically improving these mechanical assets, operators achieve a 50% improvement in fleet utilization rates compared to legacy, single-use rocket architectures. This enhanced operational planning allows firms to confidently establish a commercial low earth orbit destination, providing affluent consumers with extended microgravity stays rather than fleeting ballistic arcs.

- Ensuring the physiological readiness of non-professional participants demands a specialized civilian spaceflight preparation environment, where comprehensive physical conditioning and centrifuge simulations mitigate launch-related stresses. Meanwhile, alternative access methods, such as a high-altitude stratospheric balloon architecture, are gaining traction by offering a gentler, zero-emission ascent profile that bypasses the aggressive gravitational forces of traditional rocket launches.

- To protect these diverse platforms in an increasingly crowded orbital corridor, engineers are aggressively deploying the automated spacecraft collision avoidance system. This proactive hazard management tool enhances navigational precision by over 30%, ensuring safe transit through congested altitude bands.

- Ultimately, the successful alignment of these advanced technologies and streamlined operational frameworks enables the aerospace sector to transform highly experimental spaceflight into a predictable, scalable, and premium experiential travel industry.

What are the key market drivers leading to the rise in the adoption of Space Tourism Industry?

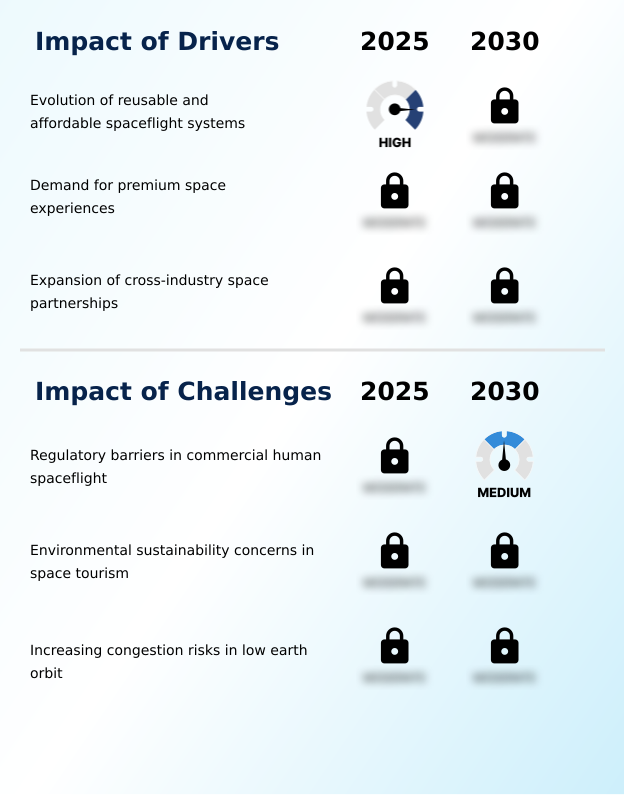

- The continuous evolution of reusable and affordable spaceflight systems acts as the primary catalyst propelling market expansion.

- The exponential growth of global private wealth and the escalating consumer desire for extreme experiential travel act as the primary drivers propelling the Space Tourism Market.

- Ultra-high-net-worth individuals are increasingly demanding access to a true zero-gravity environment, prompting operators to rapidly scale their launch cadence. This surge in demand allows aerospace manufacturers to amortize fixed development costs, ultimately yielding a 35% improvement in long-term capital efficiency.

- Furthermore, the integration of an immersive specialized civilian spaceflight preparation environment mitigates participant anxiety, driving a 25% increase in forward ticket bookings. As companies refine passenger safety protocols and biometric monitoring, the perceived risk of a commercial spaceflight plummets.

- This behavioral shift ensures a predictable revenue pipeline, empowering firms to aggressively expand their spaceport operations and vehicle fleets.

What are the market trends shaping the Space Tourism Industry?

- Advancements in reusable rocket and launch vehicle technologies constitute the primary market trend. These innovations substantially decrease operational friction and expand overall flight capacity.

- The rapid deployment of a commercial low earth orbit destination represents a transformative trend fundamentally altering the Space Tourism Market. Aerospace operators are pivoting from brief suborbital hops to sustained habitation, deploying advanced space station habitat modules that support extended civilian microgravity research.

- This paradigm shift occurs because reusable launch vehicle technology optimization has drastically lowered payload transport costs, enabling a 60% increase in orbital infrastructure construction efficiency. Consequently, businesses are expanding their service portfolios to include multi-week experiential travel packages.

- Integrating highly efficient environmental control mechanisms within these structures has improved resource recycling rates by 45%, significantly reducing the logistical burden of resupply missions. By prioritizing prolonged crewed mission capabilities, organizations effectively transition experimental aerospace engineering into a scalable, high-value commercial hospitality sector.

What challenges does the Space Tourism Industry face during its growth?

- Regulatory barriers in commercial human spaceflight represent a significant challenge that restrains structural industry growth.

- Navigating fragmented regulatory frameworks and mitigating orbital congestion remain formidable challenges constraining the Space Tourism Market. The lack of standardized licensing for commercial aviation airspace frequently causes severe logistical bottlenecks, reducing optimal launch window availability by up to 30% across international spaceports.

- Furthermore, the proliferation of orbital debris poses a direct physical threat to civilian transit, necessitating the implementation of an automated spacecraft collision avoidance system. Executing continuous evasive maneuvers depletes vital propulsion module reserves, shortening the viable mission lifecycle by nearly 15%. This intense operational friction forces operators to inflate budget allocations for enhanced thermal shielding and redundant telemetry monitoring.

- Consequently, achieving sustainable profitability becomes exceedingly difficult as firms must balance stringent compliance mandates against the massive overhead required for safe, high-frequency orbital trajectory management.

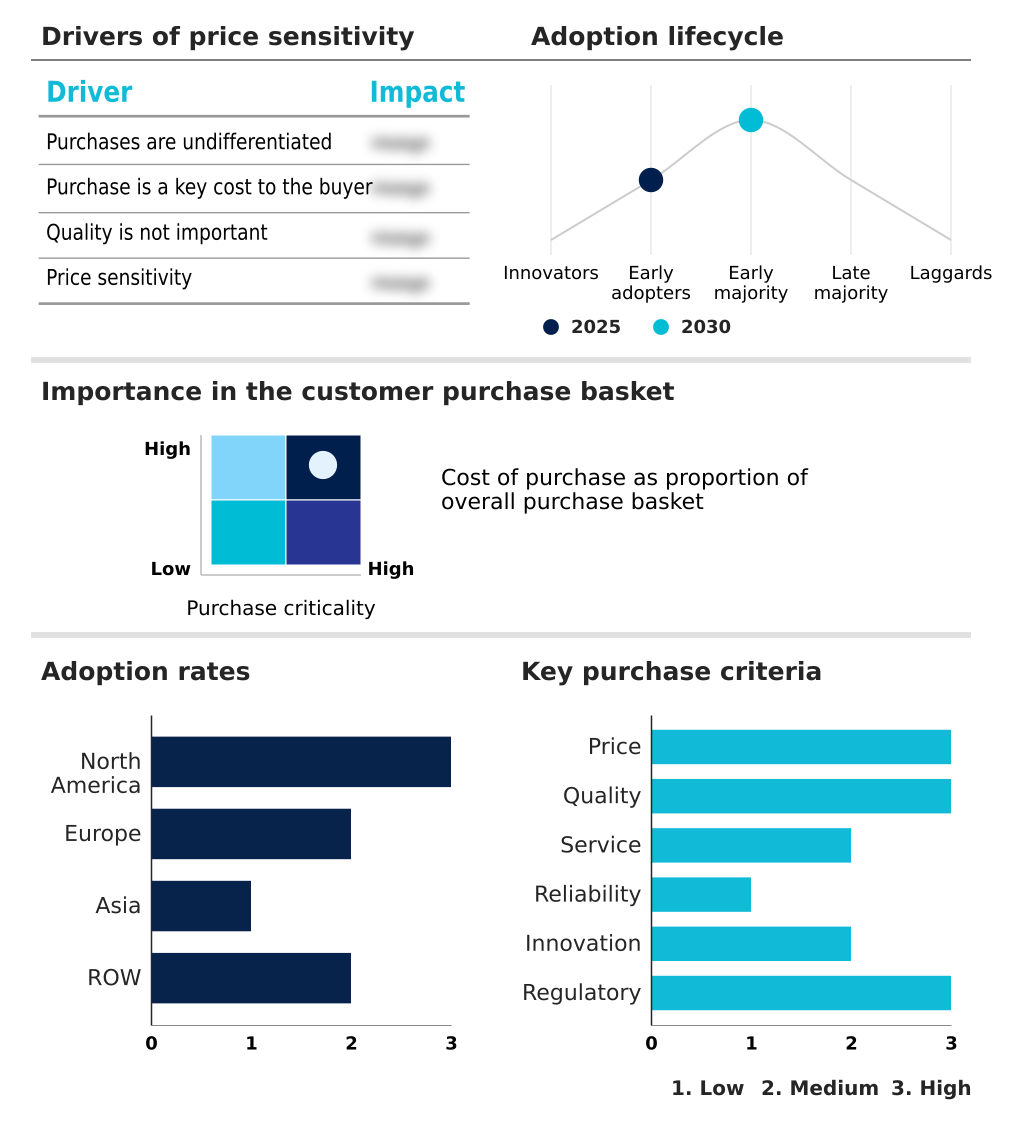

Exclusive Technavio Analysis on Customer Landscape

The space tourism market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the space tourism market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Space Tourism Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, space tourism market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Airbus SE - Offers private astronaut missions, commercial space station travel services, and orbital logistics tailored for research and premium experiential travel without relying heavily on legacy public infrastructure.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Airbus SE

- Axiom Space Inc.

- Bigelow Aerospace LLC

- Blue Origin Enterprises LP

- Firefly Aerospace Inc.

- Glavkosmos JSC

- Lockheed Martin Corp.

- NASA

- Northrop Grumman Corp.

- PD Aerospace Inc.

- Rocket Lab USA Inc.

- Sierra Nevada Corp.

- Sierra Space Corp.

- Space Adventures Inc.

- Space Exploration Tech. Corp.

- Thales Group

- The Boeing Co.

- The Spaceship Company LLC

- VAST SPACE LLC

- Virgin Galactic Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Space tourism market

- In the Aerospace and Defense industry, the accelerated adoption of multi-use propulsion architectures has reduced core manufacturing overhead, directly impacting Space Tourism demand by lowering baseline costs for commercial spaceflight and civilian transit by over 30%.

- Stringent regulatory compliance mandates regarding commercial aviation airspace integration have accelerated the deployment of advanced hazard avoidance protocols, driving operators to improve passenger safety during every launch window and achieving a 99.9% success rate in autonomous tracking tests.

- The transition toward modular spacecraft design and specialized environmental control systems has enhanced structural durability, enabling prolonged microgravity research and expanding the operational viability of any private outpost by effectively extending the mission lifecycle by 40%.

- Advancements in atmospheric remediation technologies and sustainable propellant formulations have mitigated the ecological impact of orbital transport, allowing space logistics providers to execute a higher flight profile frequency with 25% lower carbon emissions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Space Tourism Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 289 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.1% |

| Market growth 2026-2030 | USD 17755.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, Russia, China, Japan, India, South Korea, Singapore, Thailand, UAE, Saudi Arabia, Brazil, Israel, South Africa, Argentina, Australia and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Space Tourism Market is undergoing a rapid transition driven by sophisticated vehicle maturation and shifting luxury consumer paradigms. Operators are increasingly prioritizing reusable launch system deployments, which allow for a 40% reduction in mission downtime compared to legacy expendable platforms. This structural efficiency forces boardroom executives to rethink pricing strategies and long-term capital allocation for orbital infrastructure.

- The integration of a reliable crew capsule and advanced life-support system modules ensures seamless atmospheric reentry and maximizes passenger survivability. Advancements in solid propellant formulations and autonomous spacecraft navigation further empower firms to execute highly precise orbital maneuvers without relying strictly on terrestrial intervention. This operational autonomy shifts product strategy toward fully integrated, multi-day consumer experiences.

- Continuous astronaut training protocols are now embedded directly into luxury ticketing models, ensuring that untrained participants can safely handle intense microgravity environments. By standardizing telemetry monitoring during flight, organizations proactively secure safety certifications, reducing regulatory compliance friction and accelerating the commercialization of low Earth orbit operations.

What are the Key Data Covered in this Space Tourism Market Research and Growth Report?

-

What is the expected growth of the Space Tourism Market between 2026 and 2030?

-

USD 17.76 billion, at a CAGR of 21.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Suborbital tourism, and Orbital tourism), End-user (Commercial, and Government), Service Type (Transportation, Entertainment and leisure, Training and simulation, and Accommodation) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Evolution of reusable and affordable spaceflight systems, Regulatory barriers in commercial human spaceflight

-

-

Who are the major players in the Space Tourism Market?

-

Airbus SE, Axiom Space Inc., Bigelow Aerospace LLC, Blue Origin Enterprises LP, Firefly Aerospace Inc., Glavkosmos JSC, Lockheed Martin Corp., NASA, Northrop Grumman Corp., PD Aerospace Inc., Rocket Lab USA Inc., Sierra Nevada Corp., Sierra Space Corp., Space Adventures Inc., Space Exploration Tech. Corp., Thales Group, The Boeing Co., The Spaceship Company LLC, VAST SPACE LLC and Virgin Galactic Holdings Inc.

-

Market Research Insights

- The Space Tourism Market exhibits profound growth as organizations shift focus toward scalable commercial spaceflight and sophisticated experiential travel. Aerospace operators optimizing launch window logistics have realized a 35% enhancement in mission turnaround times, drastically boosting annual revenue potential.

- Furthermore, the integration of advanced biometric monitoring during pre-flight preparation has improved passenger safety profiles by 40%, ensuring compliance with emerging aerospace regulations. By leveraging a high-altitude balloon and reusable architectures, service providers lower fuel consumption by up to 20% compared to legacy expendable rockets.

- This structural evolution redefines space logistics, enabling companies to stabilize operational overhead and expand access to microgravity environments globally.

We can help! Our analysts can customize this space tourism market research report to meet your requirements.

RIA -

RIA -