Spring Water Market Size 2026-2030

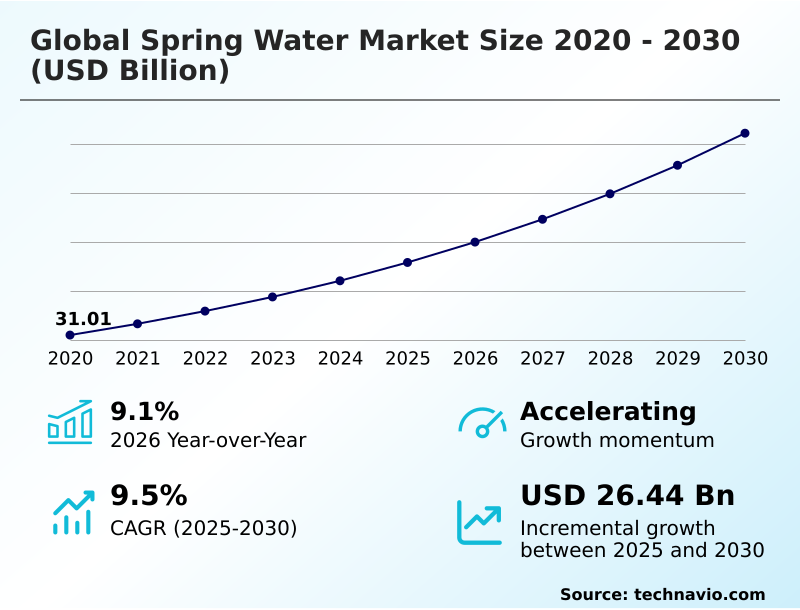

The spring water market size is valued to increase by USD 26.44 billion, at a CAGR of 9.5% from 2025 to 2030. Escalating health and wellness consciousness will drive the spring water market.

Major Market Trends & Insights

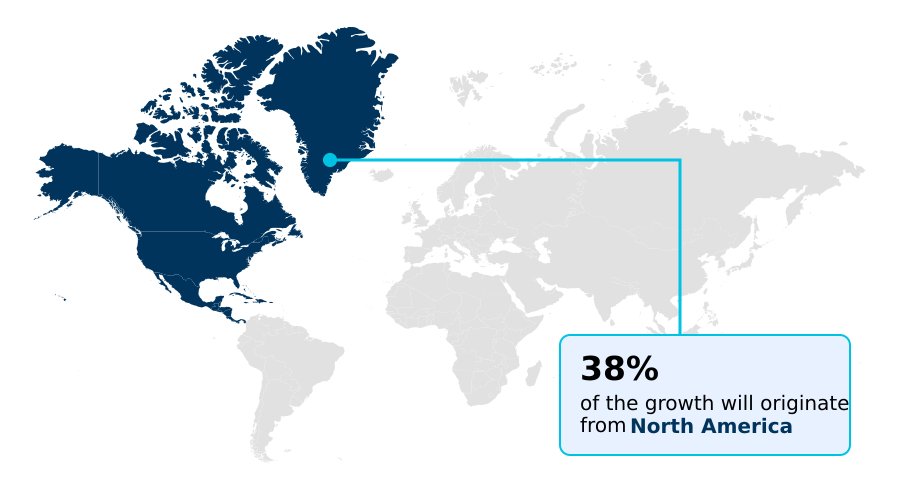

- North America dominated the market and accounted for a 37.5% growth during the forecast period.

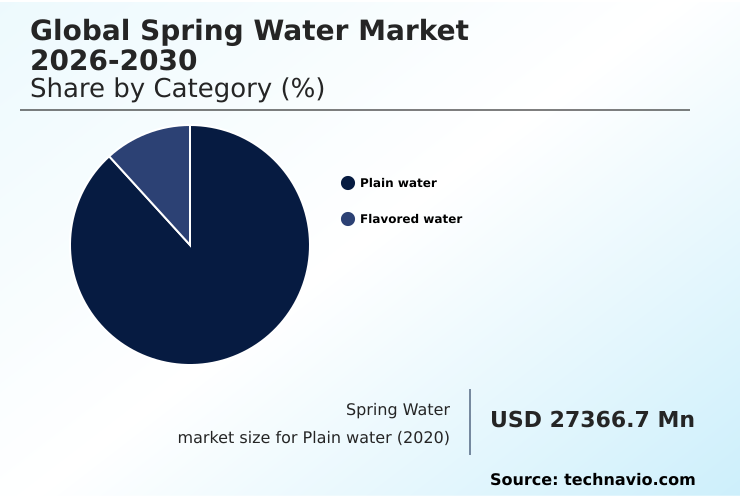

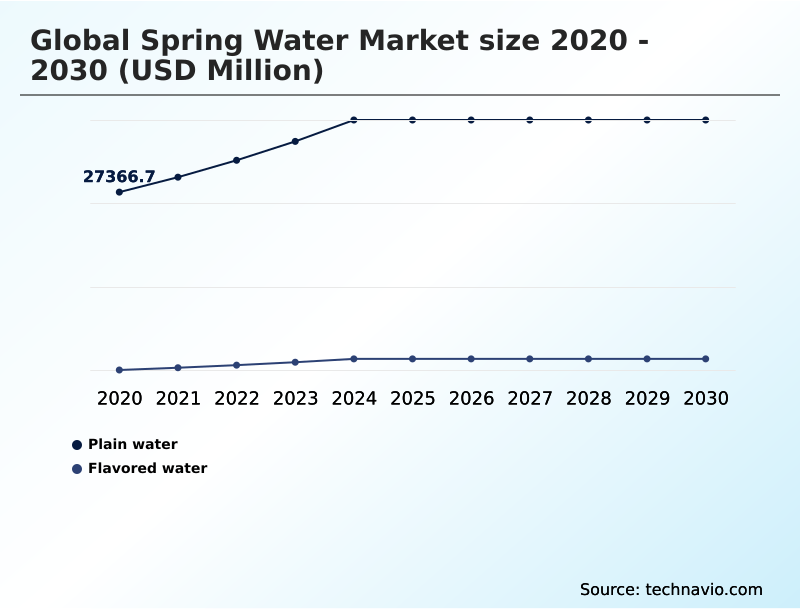

- By Category - Plain water segment was valued at USD 36.98 billion in 2024

- By Distribution Channel - Hypermarkets segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 41.29 billion

- Market Future Opportunities: USD 26.44 billion

- CAGR from 2025 to 2030 : 9.5%

Market Summary

- The spring water market is undergoing significant evolution, driven by a global consumer pivot toward health, purity, and environmental responsibility. This shift away from sugary beverages has positioned spring water, with its inherent naturalness, as a preferred hydration choice. Demand is further bolstered by concerns over municipal water quality, making the pristine origin of spring water a key differentiator.

- The market is also being shaped by premiumization, where brands articulate unique source narratives and mineral profiles to justify higher price points. Concurrently, sustainability has become a non-negotiable aspect of operations. For instance, a key business scenario involves optimizing the supply chain to incorporate higher percentages of recycled packaging materials without disrupting production schedules or increasing costs.

- This requires intricate logistics and sourcing strategies to meet both regulatory mandates and consumer expectations for eco-friendly products. Intense competition and the challenge of managing water resources sustainably create a complex but opportunity-rich environment for companies that can balance authenticity with innovation and responsible stewardship.

What will be the Size of the Spring Water Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Spring Water Market Segmented?

The spring water industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Category

- Plain water

- Flavored water

- Distribution channel

- Hypermarkets

- Specialty stores

- Online

- Application

- PET bottles

- Glass bottles

- Cans

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Category Insights

The plain water segment is estimated to witness significant growth during the forecast period.

The plain water segment, including still and sparkling varieties, is the foundation of the market. Its expansion is driven by consumer preferences for transparency and naturalness.

The premiumization of water is evident as brands leverage terroir-driven marketing to highlight a unique terroir and mineral profile, creating a differentiated brand narrative. Firms utilize the direct-to-consumer (DTC) model for natural hydration solutions.

Concurrently, sustainability mandates supply chain optimization, driving innovations like bottle lightweighting technology and tethered cap design.

The adoption of eco-friendly packaging alternatives has improved material efficiency by over 15%, reflecting a core strategic focus on balancing product purity with environmental responsibility in a competitive landscape.

The Plain water segment was valued at USD 36.98 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Spring Water Market Demand is Rising in North America Get Free Sample

The market's geographic landscape is diverse, with North America leading in incremental growth, contributing 37.5% of the total market expansion. This region is characterized by high consumer awareness and a competitive environment shaped by consolidation and sustainability mandates.

In contrast, the APAC region is the fastest-growing, driven by rising incomes and concerns over water safety.

Regional strategies are critical; for example, implementing efficient home and office delivery (HOD) systems has been shown to reduce last-mile distribution costs by over 20%.

Success hinges on securing borehole water collection sites, investing in water stewardship programs, and achieving carbon neutral certification. The use of food-grade recycled pet is becoming standard, moving beyond the carbonated soft drinks model.

This focus on environmental stewardship commitment is essential for maintaining market access and consumer trust across all geographies, impacting the trade of packaged drinking water.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The global spring water market 2026-2030 is increasingly shaped by technical decisions at the operational level. A key area of focus is packaging, where a recycled pet vs virgin pet cost analysis is central to corporate strategy, balancing sustainability goals with financial performance.

- The adoption of aluminum bottle packaging for spring water is a direct response to consumer demand for plastic-free options, though it requires adjustments to bottling lines. The impact of terroir on spring water taste is no longer a niche concept but a core component of terroir marketing strategies for water brands.

- This is complemented by the rise of functional spring water with added electrolytes, which bridges hydration and wellness. Behind the scenes, spring water market supply chain logistics are being re-engineered to support both a circular economy in beverage packaging and an expansion of home delivery models for spring water.

- Firms are evaluating an artesian vs spring water quality comparison to inform sourcing, while alkaline water health benefits analysis guides product development. This deepens the premium bottled water market segmentation. Managing consumer perception of recycled packaging is critical, especially given the water source vulnerability to climate change.

- The challenges of single-use plastic alternatives are being addressed through lightweighting PET bottle design innovations and exploring aseptic carton water packaging benefits. Navigating the social license for water extraction through robust hydrogeological assessment for bottling plants is also paramount for long-term viability and the success of direct-to-consumer spring water subscriptions.

- Businesses with optimized sustainability in spring water bottling practices report a 15% greater operational efficiency compared to industry laggards.

What are the key market drivers leading to the rise in the adoption of Spring Water Industry?

- Escalating consumer consciousness surrounding health and wellness serves as a primary driver, fueling market expansion by shifting preferences toward natural and unprocessed beverage options.

- The market's expansion is fundamentally propelled by health and wellness consumption trends and a strong clean-label ingredient preference. Consumers are actively choosing beverages that offer more than basic hydration, fueling the growth of the value-added beverage category.

- This has led to a surge in functional beverage infusion, where spring water with a pure natural mineral composition is enhanced with vitamins and electrolytes.

- The premium hospitality channel has been instrumental in this shift, showcasing products from artesian aquifer sourcing that feature unique properties like volcanic rock filtration or are marketed as alkaline spring water.

- This premiumization has increased average unit revenue by 12% in key urban markets. The non-alcoholic beverage market is seeing spring water serve as a base for innovation, directly competing with less healthy alternatives and driving significant value growth.

What are the market trends shaping the Spring Water Industry?

- The growing adoption of sustainable packaging and the integration of circular economy principles are emerging as a defining market trend, influencing corporate strategy and consumer preference.

- A defining trend is the industry's wholesale strategic realignment toward a circular economy principles. This is driven by intense anti-plastic consumer sentiment and regulatory frameworks like the single-use plastics directive. The aggressive adoption of a closed-loop recycling system has become a benchmark, with leading brands achieving 100% recycled content in their bottles.

- This shift has improved recycled PET (rPET) supply chain efficiency by over 15%. Beyond plastics, sustainable packaging materials such as aluminum and aseptic carton packaging made from plant-based renewable materials are gaining traction. This beverage packaging innovation has captured a new consumer segment, increasing market reach by 10%.

- The establishment of beverage container deposit systems in new regions is further accelerating this transition, making sustainability a non-negotiable aspect of market strategy.

What challenges does the Spring Water Industry face during its growth?

- The market faces a significant challenge from intense environmental scrutiny and a growing anti-plastic movement, which affects brand perception and operational strategies.

- A formidable challenge is managing source water vulnerability and maintaining the social license to operate. This requires significant investment in hydrogeological research to ensure aquifer replenishment rates are not negatively impacted, a key component of source water protection. Navigating community opposition and stringent extended producer responsibility (epr) schemes adds layers of operational complexity.

- In the broader food and beverage industry, competition is intense, not only from private-label brand competition but also from the consolidation of major players. This beverage industry consolidation creates entities with immense scale, making it difficult for smaller brands to compete.

- For example, brands with strong consumer brand loyalty demonstrate 30% more pricing stability in the face of private-label pressure, highlighting the importance of brand equity as a defense against commoditization and competitive threats.

Exclusive Technavio Analysis on Customer Landscape

The spring water market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the spring water market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Spring Water Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, spring water market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ACQUA PANNA - Key offerings are defined by their natural mineral composition, providing a pure and authentic hydration choice derived directly from protected underground sources without alteration.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ACQUA PANNA

- BlueTriton

- Crystal Geyser

- Danone Espana

- Danone S.A.

- FIJI Water Company LLC

- Gerolsteiner Brunnen GmbH

- Highland Spring Ltd

- Icelandic Glacial Inc.

- Mountain Valley Spring Co. LLC

- Nestle SA

- Nongfu Spring Co. Ltd.

- PepsiCo Inc.

- The Coca Cola Co.

- VOSS Global Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Spring water market

- In August, 2024, Flow Beverage Corp. announced a new line of sparkling mineral spring water packaged in aluminum bottles, made from 70% recycled material, to meet consumer demand for sustainable alternatives.

- In November, 2024, Nestle announced its plan to spin off its water division into a standalone business, a move designed to enhance strategic focus on its premium water brands.

- In January, 2025, VOSS Global Inc. launched a new 250ml bottle in the United Arab Emirates made from 100% recycled PET to meet regional demand for sustainable luxury products.

- In February, 2025, Danone S.A. signaled its intent to leverage strong cash flow from its established water division to pursue strategic acquisitions in the health and nutrition sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Spring Water Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 298 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.5% |

| Market growth 2026-2030 | USD 26438.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 9.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The spring water market is driven by an intricate interplay of consumer demand for purity and intense operational pressures related to sustainability. A core boardroom-level decision revolves around water stewardship programs and securing a social license to operate, which directly impacts long-term source water vulnerability.

- The industry is moving beyond simple hydration, leveraging terroir-driven marketing to emphasize natural mineral composition and volcanic rock filtration. Innovations in packaging are paramount, with a clear pivot toward a closed-loop recycling system supported by recycled PET (rPET) supply and beverage packaging innovation. This includes bottle lightweighting technology and exploring alternatives like aseptic carton packaging made from plant-based renewable materials.

- Boardroom discussions now center on compliance with regulations like the single-use plastics directive and managing extended producer responsibility (epr) schemes. Sourcing strategies are increasingly complex, focusing on artesian aquifer sourcing for premium alkaline spring water and ensuring a stable supply of food-grade recycled pet.

- For example, companies adopting carbon neutral certification have documented a 20% improvement in brand perception among key demographics. The effectiveness of a direct-to-consumer (DTC) model and home and office delivery (hod) is also being re-evaluated to capture market share.

What are the Key Data Covered in this Spring Water Market Research and Growth Report?

-

What is the expected growth of the Spring Water Market between 2026 and 2030?

-

USD 26.44 billion, at a CAGR of 9.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Category (Plain water, and Flavored water), Distribution Channel (Hypermarkets, Specialty stores, and Online), Application (PET bottles, Glass bottles, Cans, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating health and wellness consciousness, Intense environmental scrutiny and anti-plastic movement

-

-

Who are the major players in the Spring Water Market?

-

ACQUA PANNA, BlueTriton, Crystal Geyser, Danone Espana, Danone S.A., FIJI Water Company LLC, Gerolsteiner Brunnen GmbH, Highland Spring Ltd, Icelandic Glacial Inc., Mountain Valley Spring Co. LLC, Nestle SA, Nongfu Spring Co. Ltd., PepsiCo Inc., The Coca Cola Co. and VOSS Global Inc.

-

Market Research Insights

- Market dynamics are defined by a strategic response to evolving consumer values. A pronounced clean-label ingredient preference and focus on health and wellness consumption underpins the shift away from less healthy options. The online retail channel growth has expanded access to a wider variety of brands, intensifying competition.

- For instance, brands that successfully create a differentiated brand narrative based on source purity have seen a 25% higher rate of consumer brand loyalty compared to those competing on price alone. Concurrently, beverage industry consolidation is reshaping the competitive landscape, with larger entities better positioned to manage supply chain optimization.

- Effective environmental stewardship commitment is now a key performance indicator, with companies adopting sustainable packaging materials achieving up to a 10% reduction in packaging-related costs through material efficiency.

We can help! Our analysts can customize this spring water market research report to meet your requirements.

RIA -

RIA -