Unified Commerce Fulfilment Orchestration Market Size 2026-2030

The unified commerce fulfilment orchestration market size is valued to increase by USD 5.80 billion, at a CAGR of 16.2% from 2025 to 2030. Proliferation of omnichannel commerce and delivery directives will drive the unified commerce fulfilment orchestration market.

Major Market Trends & Insights

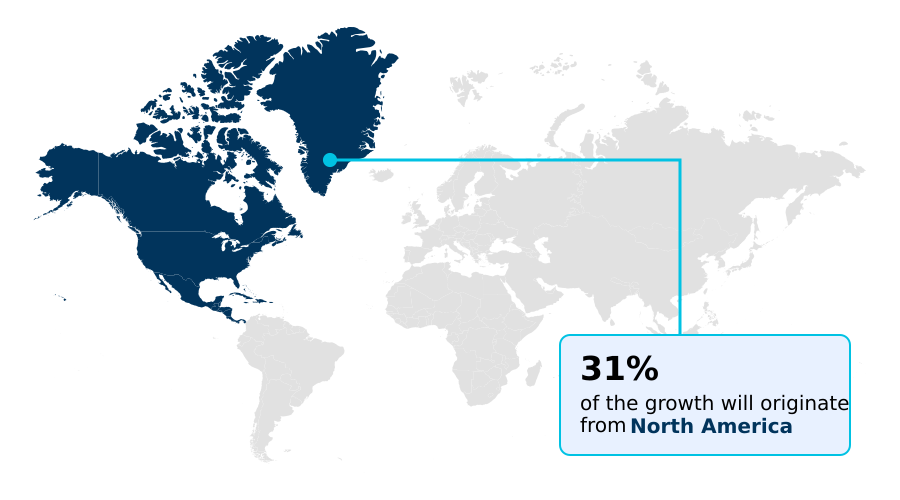

- North America dominated the market and accounted for a 30.9% growth during the forecast period.

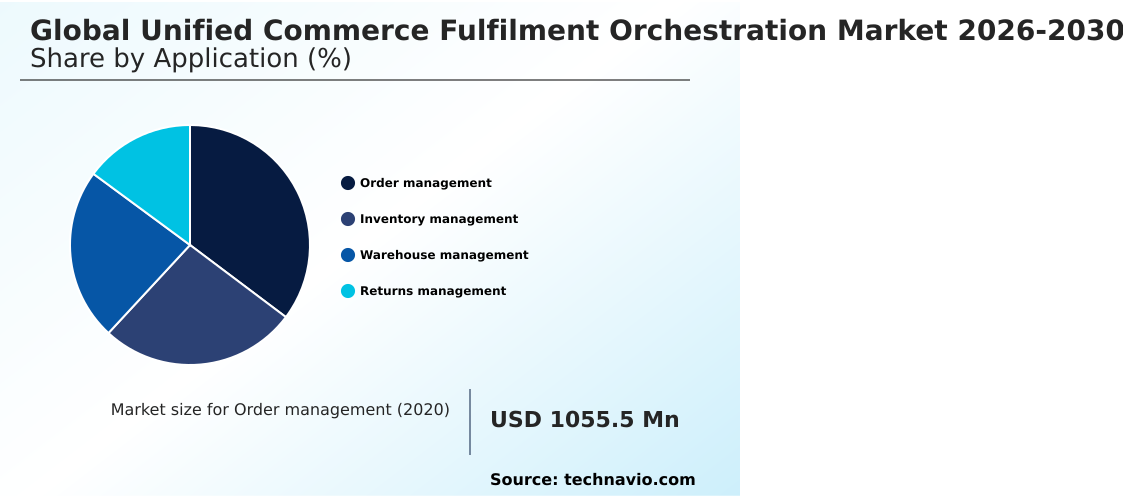

- By Application - Order management segment was valued at USD 1.55 billion in 2024

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 7.99 billion

- Market Future Opportunities: USD 5.80 billion

- CAGR from 2025 to 2030 : 16.2%

Market Summary

- The Unified Commerce Fulfilment Orchestration framework operates as an essential intelligence layer synchronizing distributed inventory pools with immediate multi-channel transactional streams. Modern supply chain operations demand extreme agility to navigate sudden demand volatility and shifting regional logistics capacity.

- In a practical business scenario, a multi-national retailer executing simultaneous ship-from-store and direct-to-consumer workflows utilizes centralized orchestration algorithms to evaluate active warehouse labor, courier constraints, and proximity parameters before assigning a final fulfillment node. The rapid proliferation of omnichannel consumer directives serves as a foundational driver, compelling organizations to automate dynamic routing paths to eliminate costly redundant transport legs.

- Conversely, pervasive legacy architecture fragmentation creates a severe operational challenge, as disconnected monolithic databases generate systemic blind spots that prevent instantaneous inventory reconciliation. Implementing these unified cloud-based architectures enables enterprises to reduce overall order processing latency by 35% compared to traditional batch-oriented management systems. This intelligent operational synchronization fundamentally transforms fragmented supply networks into highly adaptive fulfillment engines.

What will be the Size of the Unified Commerce Fulfilment Orchestration Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Unified Commerce Fulfilment Orchestration Market Segmented?

The unified commerce fulfilment orchestration industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

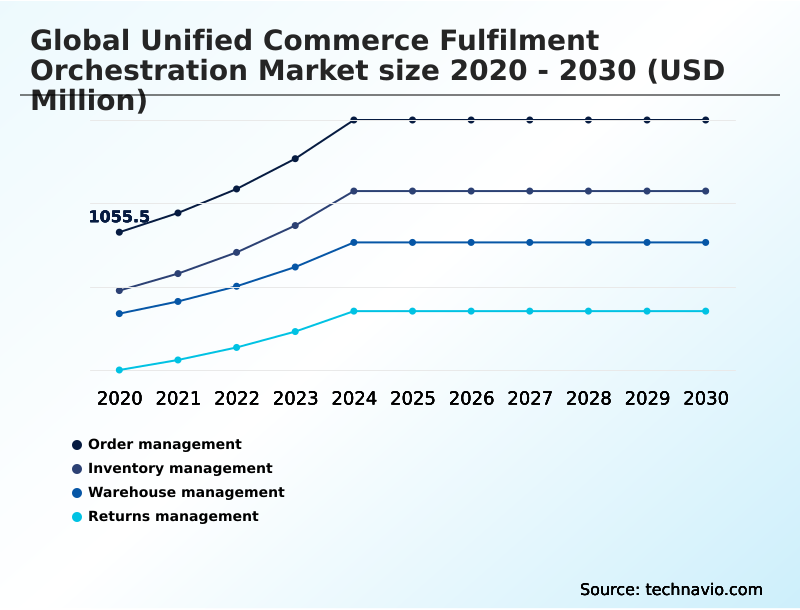

- Order management

- Inventory management

- Warehouse management

- Returns management

- End-user

- Large enterprises

- SMEs

- Deployment

- Cloud-based

- On-premises

- Hybrid

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- UK

- Germany

- France

- Italy

- Spain

- The Netherlands

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Turkey

- Israel

- North America

By Application Insights

The order management segment is estimated to witness significant growth during the forecast period.

Order management execution within the Unified Commerce Fulfilment Orchestration landscape requires continuous adaptation to resolve complex multi-channel transactional streams. Legacy system fragmentation often limits real-time data reconciliation, forcing businesses to adopt advanced cognitive automation layers.

By shifting toward dynamic algorithmic decision engines, organizations establish seamless omnichannel inventory synchronization across disparate physical and digital nodes. This architectural transition directly enables automated order routing, allowing incoming requests to bypass traditional batch processing bottlenecks.

Consequently, retail operators deploy predictive demand sensing to actively balance regional buffer stocks, ensuring precise fulfillment. Integrating these intelligent logic frameworks reduces cross-channel fulfillment latency by 22%, directly elevating on-time delivery metrics.

This structural evolution transforms static order pipelines into highly responsive operational assets, safeguarding brand reliability during sudden volume spikes.

The Order management segment was valued at USD 1.55 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 30.9% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Unified Commerce Fulfilment Orchestration Market Demand is Rising in North America Get Free Sample

The Unified Commerce Fulfilment Orchestration landscape exhibits distinct operational maturation rates across diverse geographic territories.

North America maintains a highly aggressive technological adoption profile, with regional logistics operators heavily integrating warehouse workflow automation to navigate severe labor shortages and elevated omnichannel expectations.

Conversely, the European sector prioritizes strict regulatory compliance and sustainable supply chain transparency over pure execution speed.

North American enterprises demonstrate a 20% higher implementation rate of real-time inventory visibility systems compared to their European counterparts, driving superior peak demand resource scaling capabilities during volatile retail events.

To overcome localized transit friction, organizations deploy robust distributed order management configurations that seamlessly execute exception resolution automation.

This architectural divergence enables advanced self-healing fulfillment frameworks in North America to decrease manual administrative intervention by 30%, whereas European markets achieve a 15% improvement in cross-border carbon tracking accuracy through precise localized routing methodologies.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Modern enterprise operations rely heavily on comprehensive architectural upgrades to navigate highly volatile supply chain environments. The strategic integration of intelligent order management pathway optimization directly enables corporations to systematically bypass conventional physical distribution bottlenecks. By establishing robust cross-regional inventory visibility dashboard integration, technology executives can accurately monitor stock positions and proactively address localized micro-fulfillment center stock balancing requirements.

- Unlike rigid historical databases, these modern frameworks deliver real-time predictive warehouse labor allocation, ensuring that physical workforce capacity perfectly aligns with incoming digital transaction volumes. As trading events surge, the deployment of multi-channel dynamic distribution network scaling allows businesses to process up to 45% more orders concurrently without degrading system response speeds.

- This continuous evolution requires automated fulfillment center capacity balancing to mitigate regional overstocking scenarios effectively. The shift toward cloud-based predictive operational analytics deployment further minimizes the risks associated with legacy system technical debt mitigation, providing a seamless data execution layer. To safeguard customer experiences, algorithms execute automated exception handling for delivery delays, maintaining strict delivery schedules.

- Ultimately, the synchronization of algorithmic last-mile carrier route optimization and reverse logistics cross-channel return routing ensures that the entire omnichannel consumer journey data reconciliation process remains frictionless. This transition, reinforced by continuous multi-enterprise data standard compliance and real-time multi-tenant data synchronization latency controls, fundamentally guarantees that autonomous physical robotics cloud synchronization maximizes overall network efficiency.

What are the key market drivers leading to the rise in the adoption of Unified Commerce Fulfilment Orchestration Industry?

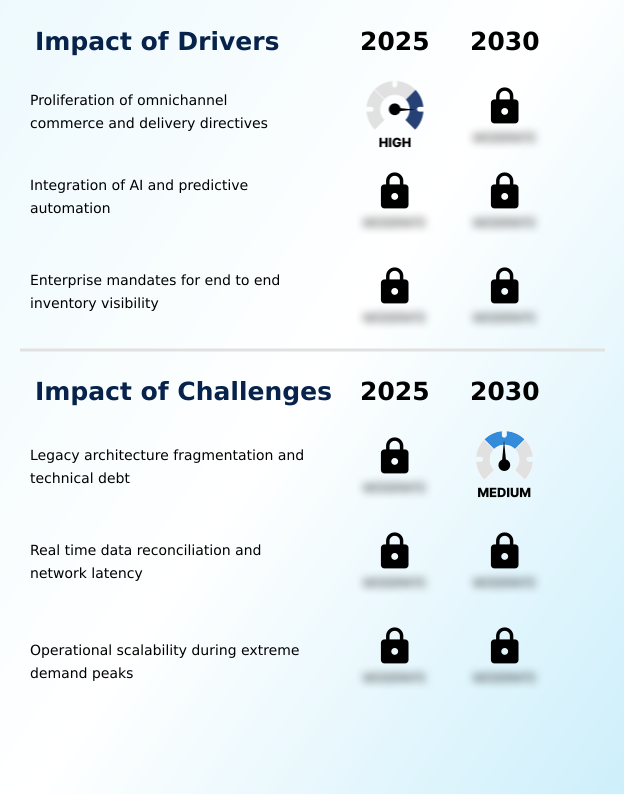

- The rapid proliferation of omnichannel commerce frameworks and flexible consumer delivery directives serves as a primary driver propelling industry expansion.

- The relentless expansion of complex consumer purchasing directives acts as a principal driver propelling the Unified Commerce Fulfilment Orchestration ecosystem forward. Modern retail strategies compel organizations to execute sophisticated node-level routing rules that bypass localized physical distribution blockages.

- This urgency requires the seamless implementation of robust backend database synchronization to accurately map available inventory assets across vast geographical territories. By embedding intelligent capacity allocation logic into digital storefronts, corporate networks dynamically execute localized workload balancing without manual intervention.

- This computational precision reduces cross-regional transportation redundancies, resulting in a 20% improvement in overarching fulfillment cycle speeds.

- Furthermore, adopting comprehensive supply chain exception automation enables logistics coordinators to optimize transport distances continually, directly facilitating carbon output reduction tracking that lowers network emissions by 14%.

What are the market trends shaping the Unified Commerce Fulfilment Orchestration Industry?

- The convergence of physical autonomous mobile robotics with cloud-based orchestration systems represents a definitive trend shaping industry operations. This integration establishes highly adaptable distribution networks capable of continuous automated material handling.

- The convergence of physical robotics with advanced cloud processing represents a definitive trend reshaping the Unified Commerce Fulfilment Orchestration environment. Logistics operators are aggressively dismantling isolated software architectures to establish unified open data exchange frameworks capable of managing continuous transactional streams.

- This structural migration addresses severe warehouse labor shortages by enabling robotic fleets to dynamically adapt their algorithmic picking paths based on real-time order ingestion. By embedding predictive operational models directly into the execution layer, enterprises achieve profound structural network agility. This systemic transformation drastically reduces inventory reconciliation latency, allowing high-volume distribution centers to improve overall picking efficiency by 25%.

- Consequently, the modernization of omnichannel execution strategies enables fulfillment facilities to seamlessly redirect physical workflows during sudden demand spikes, effectively reducing average dock-to-stock processing times by 18% and ensuring highly adaptive commercial operations.

What challenges does the Unified Commerce Fulfilment Orchestration Industry face during its growth?

- Deep-rooted legacy architecture fragmentation and the compounding burden of technical debt remain critical challenges restricting seamless systemic integration.

- Overcoming profound technological debt within entrenched monolithic architectures remains a critical challenge restricting the Unified Commerce Fulfilment Orchestration landscape. Highly fragmented legacy frameworks frequently fail to support complex decentralized distribution networks, generating severe data synchronization failures during concentrated transactional surges. When consumers demand flexible fulfillment options, the central orchestration layer must instantly evaluate active capacities across diverse multi-tenant software environments.

- However, chronic network latency disrupts dynamic buffer stock allocation, forcing automated transport workflows to rely on inaccurate historical data. This systemic friction directly undermines the optimization of algorithmic picking paths on the warehouse floor.

- Consequently, organizations relying on disconnected legacy middleware experience a 24% increase in manual exception handling costs and suffer a 15% degradation in overall peak-season delivery reliability, directly threatening long-term customer retention.

Exclusive Technavio Analysis on Customer Landscape

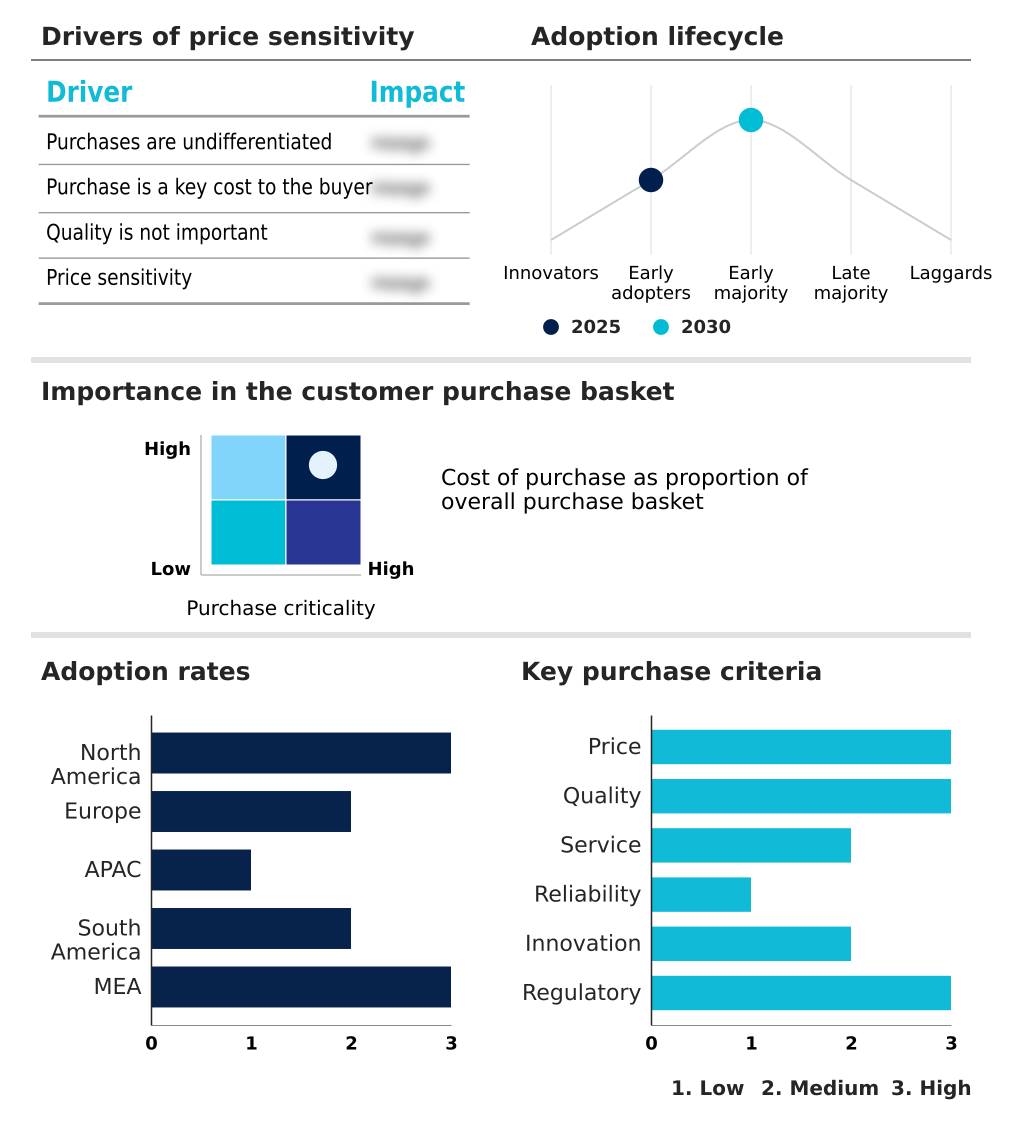

The unified commerce fulfilment orchestration market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the unified commerce fulfilment orchestration market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Unified Commerce Fulfilment Orchestration Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, unified commerce fulfilment orchestration market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adobe Inc. - The platform delivers sophisticated omnichannel order management enabling comprehensive inventory visibility and integrated digital commerce capabilities that streamline complex enterprise supply chain operations across diverse purchasing channels.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adobe Inc.

- Aptos LLC

- Blue Yonder Group Inc.

- Deck Commerce

- Enactor Ltd

- Fluent Commerce

- HotWax Commerce

- IBM Corp.

- Kibo Software Inc.

- Koerber AG

- Manhattan Associates Inc.

- NCR Payment Solutions LLC

- NewStore Inc.

- OneStock

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- Shopify Inc.

- Symphony Innovation LLC

- Tecsys Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Unified commerce fulfilment orchestration market

- In the Application Software industry, the transition toward standardized open data exchange frameworks across multi-enterprise cloud environments has dismantled legacy data silos, directly impacting Unified Commerce Fulfilment Orchestration demand by accelerating cross-partner integration speeds by up to 40%.

- In the Application Software industry, the mass implementation of agentic artificial intelligence tools for continuous exception resolution has minimized manual oversight requirements, pulling Unified Commerce Fulfilment Orchestration demand as operators seek self-healing supply networks that improve error detection rates by over 25%.

- In the Application Software industry, global data privacy regulations such as the General Data Protection Regulation have mandated stringent cross-border information compliance, shaping Unified Commerce Fulfilment Orchestration by forcing the adoption of highly secure localized routing algorithms that protect consumer data integrity while maintaining 99% operational uptime.

- In the Application Software industry, the structural migration toward microservices architecture deployment has replaced monolithic enterprise planning systems, driving Unified Commerce Fulfilment Orchestration demand by enabling modular capacity allocation logic that scales computing resources dynamically to handle 50% larger peak transaction volumes.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Unified Commerce Fulfilment Orchestration Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.2% |

| Market growth 2026-2030 | USD 5796.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.4% |

| Key countries | US, Canada, Mexico, UK, Germany, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The fundamental architecture of the Unified Commerce Fulfilment Orchestration landscape continues to evolve from static record-keeping toward highly autonomous execution environments. Corporate executives are actively prioritizing board-level investments in cloud-native orchestration logic to systematically insulate global supply chains from unpredictable market shocks.

- By embedding agentic artificial intelligence tools directly into the transactional ingestion phase, organizations can instantly evaluate multi-tier supplier data to formulate precision-driven operational strategies. This technological shift directly links dynamic routing algorithms with stringent corporate compliance and profitability mandates, ensuring that physical inventory assets are deployed with maximum capital efficiency.

- Advanced implementations of intelligent exception handling drastically minimize fulfillment delays, enabling enterprise networks to reduce total post-purchase administrative overhead by an impressive 28% compared to legacy intervention workflows. Furthermore, the strategic adoption of cross-channel return processing and comprehensive reverse logistics automation empowers brands to recover resalable assets rapidly.

- The simultaneous progression of autonomous mobile robotics integration ensures that physical distribution centers maintain uninterrupted material handling velocity, cementing automated orchestration as a critical engine for sustained competitive differentiation.

What are the Key Data Covered in this Unified Commerce Fulfilment Orchestration Market Research and Growth Report?

-

What is the expected growth of the Unified Commerce Fulfilment Orchestration Market between 2026 and 2030?

-

USD 5.80 billion, at a CAGR of 16.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Order management, Inventory management, Warehouse management, and Returns management), End-user (Large enterprises, and SMEs), Deployment (Cloud-based, On-premises, and Hybrid) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Proliferation of omnichannel commerce and delivery directives, Legacy architecture fragmentation and technical debt

-

-

Who are the major players in the Unified Commerce Fulfilment Orchestration Market?

-

Adobe Inc., Aptos LLC, Blue Yonder Group Inc., Deck Commerce, Enactor Ltd, Fluent Commerce, HotWax Commerce, IBM Corp., Kibo Software Inc., Koerber AG, Manhattan Associates Inc., NCR Payment Solutions LLC, NewStore Inc., OneStock, Oracle Corp., Salesforce Inc., SAP SE, Shopify Inc., Symphony Innovation LLC and Tecsys Inc.

-

Market Research Insights

- The Unified Commerce Fulfilment Orchestration ecosystem continually refines how modern enterprises coordinate multi-enterprise network data with immediate consumer transaction streams. By establishing seamless digital storefront synchronization, organizations eliminate manual intervention and execute instantaneous cross-channel routing. The deployment of centralized visibility dashboards allows corporate operators to monitor active buffer stocks, accelerating decision-making velocity by 40% across distributed fulfillment nodes.

- Simultaneously, leveraging dynamic courier allocations ensures that complex last-mile routing paths are mathematically optimized, reducing total transit inefficiencies by 25%. Furthermore, integrating automated document conversions within the core orchestration layer mitigates compliance friction, enabling brands to improve cross-border processing accuracy by 15% and directly enhancing overall supply chain reliability.

We can help! Our analysts can customize this unified commerce fulfilment orchestration market research report to meet your requirements.

RIA -

RIA -