Ureteroscopy Devices Market Size 2026-2030

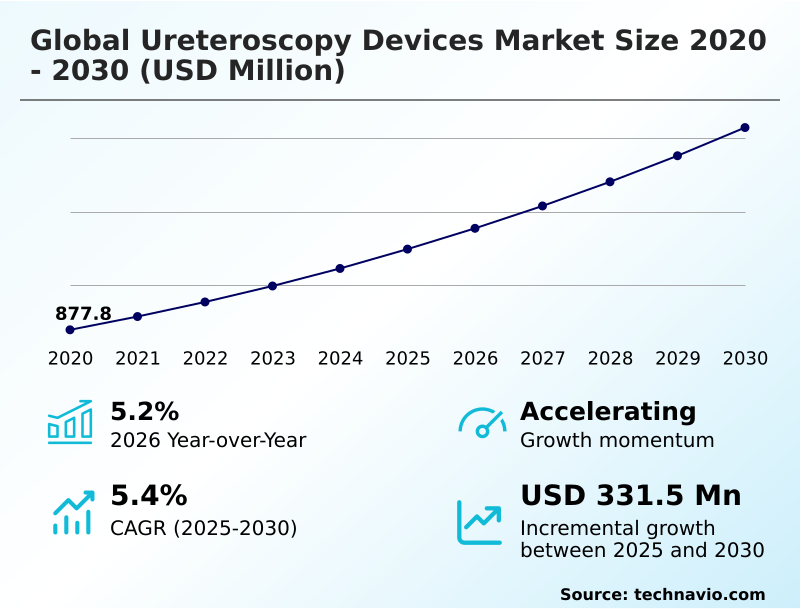

The ureteroscopy devices market size is valued to increase by USD 331.5 million, at a CAGR of 5.4% from 2025 to 2030. Growing prevalence of kidney stones and ureteral cancer will drive the ureteroscopy devices market.

Major Market Trends & Insights

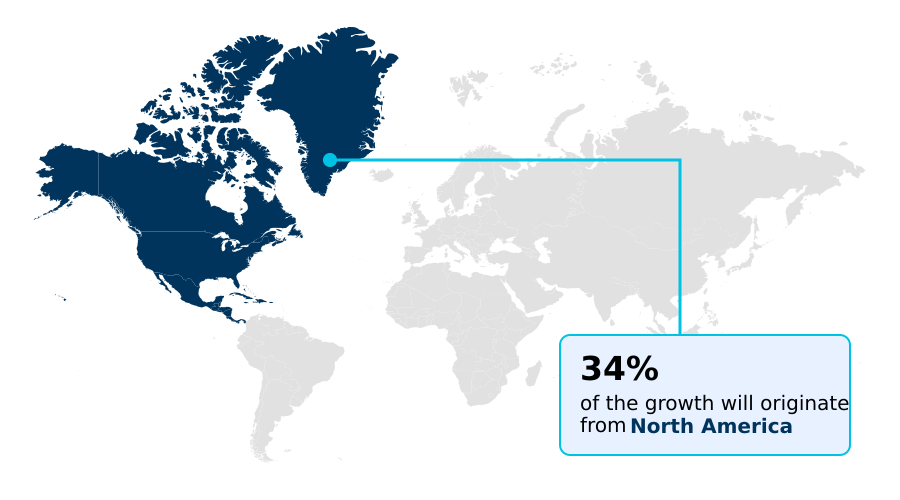

- North America dominated the market and accounted for a 34.3% growth during the forecast period.

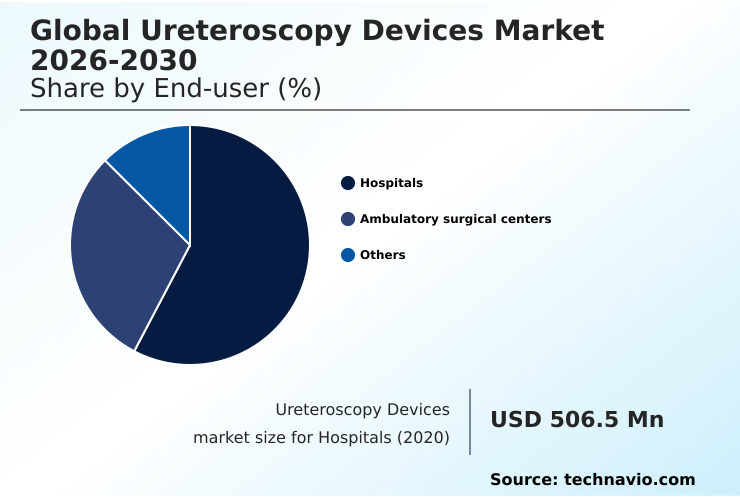

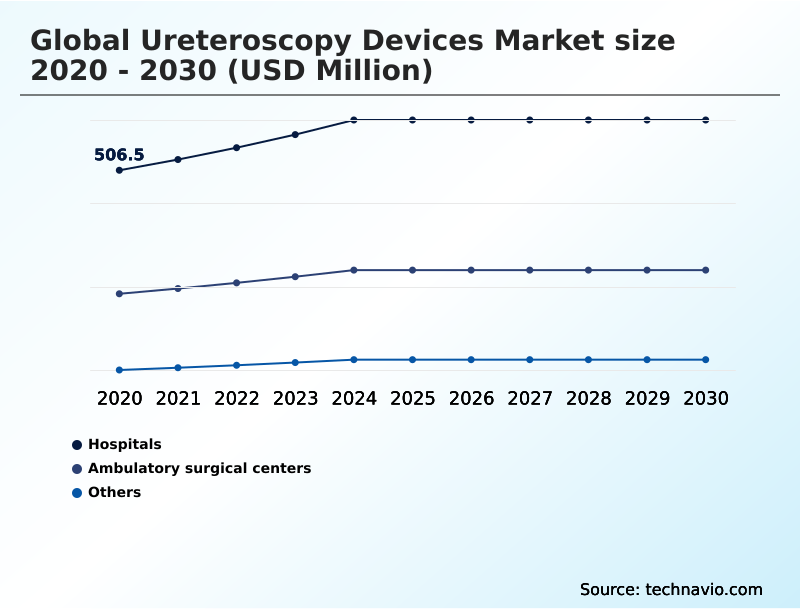

- By End-user - Hospitals segment was valued at USD 606.3 million in 2024

- By Product - Flexible ureteroscopes segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 551.6 million

- Market Future Opportunities: USD 331.5 million

- CAGR from 2025 to 2030 : 5.4%

Market Summary

- The ureteroscopy devices market is shaped by the rising global incidence of urological disorders, including kidney stones and upper tract urothelial carcinoma, which fuels demand for effective diagnostic and therapeutic interventions. A significant driver is the clinical shift toward minimally invasive urology, favoring procedures that reduce patient morbidity and shorten recovery times.

- Technological innovation remains a powerful force, with advancements in digital flexible ureteroscope design, such as chip-on-the-tip technology and superior active deflection capability, enabling surgeons to navigate complex anatomy with greater precision. The growing adoption of single-use flexible ureteroscope models addresses critical concerns around sterile reprocessing and cross-contamination risks.

- However, the high capital investment and repair costs associated with reusable systems, along with the per-procedure cost of disposables, present significant budget challenges for healthcare facilities.

- A key business scenario involves hospitals implementing hybrid procurement strategies; for instance, a facility might use durable reusable scopes for scheduled, low-risk cases while reserving single-use devices for emergency procedures or high-risk patients to optimize both instrument durability and infection control, thereby balancing operational costs with clinical imperatives. This strategic asset management is becoming crucial for sustainable endourology service delivery.

What will be the Size of the Ureteroscopy Devices Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Ureteroscopy Devices Market Segmented?

The ureteroscopy devices industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals

- Ambulatory surgical centers

- Others

- Product

- Flexible ureteroscopes

- Semi-rigid ureteroscopes

- Application

- Urolithiasis

- Urinary stricture

- Kidney cancer

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

Hospitals represent the primary end-user segment, driven by the need to manage a wide spectrum of urological cases, from routine diagnostic ureteroscopy to complex interventions.

Purchasing decisions are complex, balancing clinical demands for superior performance with administrative pressures for cost control. The debate over the cost-effectiveness of disposable scopes versus the total cost of ownership for a reusable flexible ureteroscope remains central.

Facilities are optimizing procedural ergonomics and urology procedure efficiency in urology hybrid operating rooms, with some achieving a 15% reduction in turnaround times by refining ureteroscope maintenance cycles and sterilization workflows.

Strict ureteroscope reprocessing protocols are critical, influencing the choice between devices based on instrument durability, working channel diameter, and compatibility with advanced systems like robotic-assisted ureteroscopy.

The Hospitals segment was valued at USD 606.3 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 34.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ureteroscopy Devices Market Demand is Rising in North America Get Free Sample

The geographic landscape is characterized by varied technology adoption rates.

North America leads due to high healthcare spending and rapid adoption of advanced laser lithotripsy, whereas parts of Asia Pacific represent the fastest-growing market, with a 34% share of the incremental growth.

In Europe, mature markets focus on optimizing kidney stone management through updated ureteroscopy guidelines, balancing the use of semi-rigid ureteroscope devices with flexible models for navigating tortuous ureters.

Emerging economies are improving access to urology clinic equipment but often prioritize durable, lower-cost options over disposables. Investments in pediatric ureteroscopy devices are also increasing globally.

Strategies for ureteroscope damage prevention and efficient use of electrosurgical instruments are universal concerns, impacting purchasing decisions. In some regions, ureteroscopy is gaining ground over percutaneous nephrolithotomy for specific indications, driven by improved stone fragmentation efficiency.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the ureteroscopy devices market requires a deep understanding of nuanced procedural factors. A critical consideration is the impact of ureteroscope diameter on patient outcomes, where smaller instruments are often preferred for less traumatic procedures. This is closely linked to innovations in portable ureteroscopy systems, which are expanding the viability of office-based procedures.

- Healthcare providers are intensely comparing reusable vs single-use ureteroscope costs, with analysis showing that high-volume centers can mitigate the higher per-case cost of disposables through operational efficiencies that improve throughput by over 10% compared to facilities reliant on reprocessing. The ureteroscopic management of ureteral strictures and ureteroscopy for upper tract tumor biopsy are growing applications demanding superior technology.

- Key technical debates include digital imaging versus fiber-optic ureteroscopy for improving visualization in ureteroscopy procedures and the cost-benefit analysis of thulium fiber lasers for stone treatment. Advancements in flexible ureteroscope deflection are crucial, as are best practices for ureteral access sheath use and optimizing irrigation flow in ureteroscopy.

- A focus on reducing ureteroscope damage during surgery, managing intrarenal pressure in ureteroscopy, and addressing infection risks with reprocessed ureteroscopes are vital for patient safety.

- Furthermore, ergonomic improvements in ureteroscope design, alongside better training methods for advanced flexible ureteroscopy, are essential for addressing challenges in semi-rigid ureteroscope navigation and enhancing performance in specialized areas like ureteroscopy in pediatric urology patients, while also considering the single-use ureteroscope environmental impact. The role of robotics in complex ureteroscopy continues to expand, promising to redefine standards of care.

What are the key market drivers leading to the rise in the adoption of Ureteroscopy Devices Industry?

- The growing prevalence of kidney stones and ureteral cancer is a key driver fueling the demand for ureteroscopy devices.

- Market growth is driven by the increasing preference for minimally invasive urology and technological advancements that improve outcomes. The adoption of a digital flexible ureteroscope with chip-on-the-tip technology enhances visualization for therapeutic ureteroscopy.

- Innovations in kidney stone fragmentation techniques, especially advanced laser lithotripsy using the thulium fiber laser, have increased stone-free rates by over 15% in complex cases. This supports the trend toward endoscopic stone treatment and minimally invasive stone removal.

- A focus on patient safety in endourology has also spurred the use of better procedural tools like the ureteral access sheath and stone retrieval basket.

- Furthermore, the high costs associated with flexible ureteroscope repair are pushing many institutions toward disposable options, with facilities noting a 40% reduction in their annual endoscope maintenance budgets.

What are the market trends shaping the Ureteroscopy Devices Industry?

- A notable upcoming market trend is the continuous stream of technological advancements in ureteroscopy devices. These innovations are enhancing procedural efficacy and expanding clinical applications.

- Key trends are centered on urology device innovation, particularly the shift toward single-use flexible ureteroscope models to enhance safety and efficiency. The advancement of endoscope camera technology, with CMOS imaging sensors replacing older fiber-optic ureteroscopes, has improved diagnostic accuracy in endoscopy by up to 25% in certain studies.

- Advanced visualization modalities such as narrow-band imaging are becoming standard for detecting upper tract urothelial carcinoma. The adoption of a robotic urology surgery platform is also accelerating, promising greater precision in complex endourology procedures.

- To support this technological shift, ureteroscopy training simulators are being integrated into residency programs, improving surgeon proficiency on new devices by 30% before they enter the operating room.

What challenges does the Ureteroscopy Devices Industry face during its growth?

- The high costs associated with ureteroscopes and their related procedures present a key challenge that affects the industry's growth trajectory.

- Primary market challenges revolve around single-use endoscope economics and the high cost of advanced systems. While high-definition imaging and superior active deflection capability are desirable, justifying the expense remains difficult for budget-constrained facilities, where adoption of new technology lags by up to three years compared to well-funded centers.

- The cost-effectiveness of disposable scopes is a complex calculation, as the per-procedure expense must be weighed against eliminating ureteroscope maintenance cycles and complex reprocessing protocols. Stringent urological device sterilization rules add to the operational burden of reusables. Furthermore, the availability of lower-cost alternatives like shock wave lithotripsy for certain stone types can limit procedural volume.

- The high price of a portable visualization system, for example, can be a significant barrier for smaller clinics aiming to establish in-office procedures.

Exclusive Technavio Analysis on Customer Landscape

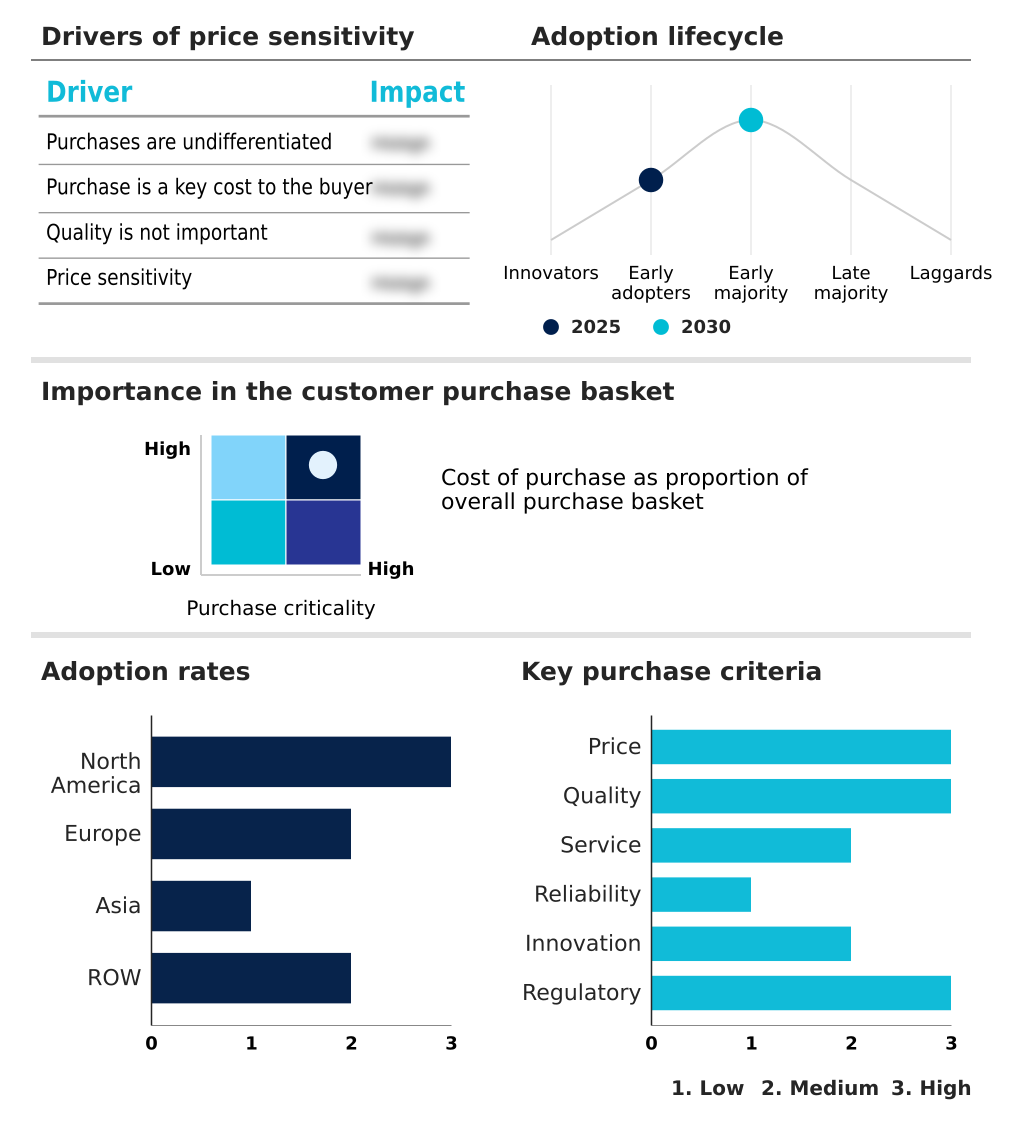

The ureteroscopy devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ureteroscopy devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ureteroscopy Devices Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ureteroscopy devices market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AdvaMed - The organization provides advocacy and policy support for innovative ureteroscopes and imaging technologies, fostering advancements in urological diagnostics and stone management within the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AdvaMed

- Advin Health Care

- B.Braun SE

- Becton Dickinson and Co.

- Boston Scientific Corp.

- Coloplast AS

- Cook Group Inc.

- Erbe Elektromedizin GmbH

- HOYA CORP.

- KARL STORZ SE and Co. KG

- Olympus Corp.

- OPCOM Medical Inc.

- PENTAX Medical Co.

- ProSurg Inc.

- Richard Wolf GmbH

- Stryker Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ureteroscopy devices market

- In May 2025, OPCOM Medical Inc. announced it had received U.S. FDA approval for its single-use flexible ureteroscope system, marking its entry into this competitive market segment.

- In September 2025, Olympus announced an exclusive global distribution agreement with MacroLux Medical Technology to distribute a range of single-use urology products, including ureteroscopes.

- In April 2025, Medtronic is slated to present late-breaking data from its Expand URO clinical trial for the Hugo robotic-assisted surgery (RAS) system, following its submission to the U.S. Food and Drug Administration (FDA).

- In October 2025, Johnson and Johnson is expected to highlight advancements in its MONARCH Platform for Urology, which leverages AI-driven simulation to enhance robotic-assisted procedures.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ureteroscopy Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 295 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 5.4% |

| Market growth 2026-2030 | USD 331.5 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.2% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Malaysia, Brazil, Saudi Arabia, Turkey, South Africa, UAE, Colombia, Argentina and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ureteroscopy devices market is defined by a dynamic interplay between technological innovation and clinical necessity. The evolution from reusable flexible ureteroscope models to single-use flexible ureteroscope options is reshaping purchasing decisions, driven by concerns over sterile reprocessing and instrument durability.

- Core technologies like chip-on-the-tip technology and CMOS imaging sensors have revolutionized endoscopic visualization, providing high-definition imaging that surpasses traditional fiber-optic ureteroscopes. This improved clarity is critical for both diagnostic ureteroscopy and therapeutic ureteroscopy, particularly in procedures like laser lithotripsy. The choice between a holmium laser and a thulium fiber laser is now a key consideration, impacting stone fragmentation efficiency.

- For complex cases, robotic-assisted ureteroscopy is gaining traction, offering enhanced procedural ergonomics. Devices are further specialized with features like narrow-band imaging for detecting upper tract urothelial carcinoma and intrarenal pressure monitoring for safety.

- The performance of a digital flexible ureteroscope is judged by its active deflection capability and working channel diameter, which determines compatibility with tools like stone retrieval baskets and electrosurgical instruments for tissue coagulation.

- In minimally invasive urology, these advancements are pivotal for effective kidney stone management, with some facilities reporting a 20% reduction in difficult cases requiring conversion to more invasive procedures like percutaneous nephrolithotomy, a testament to the enhanced capabilities of modern endourology procedures.

What are the Key Data Covered in this Ureteroscopy Devices Market Research and Growth Report?

-

What is the expected growth of the Ureteroscopy Devices Market between 2026 and 2030?

-

USD 331.5 million, at a CAGR of 5.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, Ambulatory surgical centers, and Others), Product (Flexible ureteroscopes, and Semi-rigid ureteroscopes), Application (Urolithiasis, Urinary stricture, Kidney cancer, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Growing prevalence of kidney stones and ureteral cancer, High costs associated with ureteroscopes and related procedures

-

-

Who are the major players in the Ureteroscopy Devices Market?

-

AdvaMed, Advin Health Care, B.Braun SE, Becton Dickinson and Co., Boston Scientific Corp., Coloplast AS, Cook Group Inc., Erbe Elektromedizin GmbH, HOYA CORP., KARL STORZ SE and Co. KG, Olympus Corp., OPCOM Medical Inc., PENTAX Medical Co., ProSurg Inc., Richard Wolf GmbH and Stryker Corp.

-

Market Research Insights

- Market dynamics are heavily influenced by the compelling economics of single-use endoscopes and a focus on patient safety in endourology. Institutions are scrutinizing flexible ureteroscope repair costs, which can account for up to 25% of a device's initial purchase price annually.

- The shift towards disposable models is driven by enhanced ureteroscopy infection control, with facilities reporting a near-total elimination of cross-contamination incidents. This transition directly impacts the urological surgical workflow, with some ambulatory centers achieving a 15% improvement in case turnover times by eliminating reprocessing delays.

- The economic models demonstrate that while per-procedure costs are higher, the avoidance of repair expenses and potential infection-related litigation makes the total cost of ownership favorable in high-volume settings.

We can help! Our analysts can customize this ureteroscopy devices market research report to meet your requirements.

RIA -

RIA -