Varicose Vein Treatment Devices Market Size and Growth Forecast 2026-2030

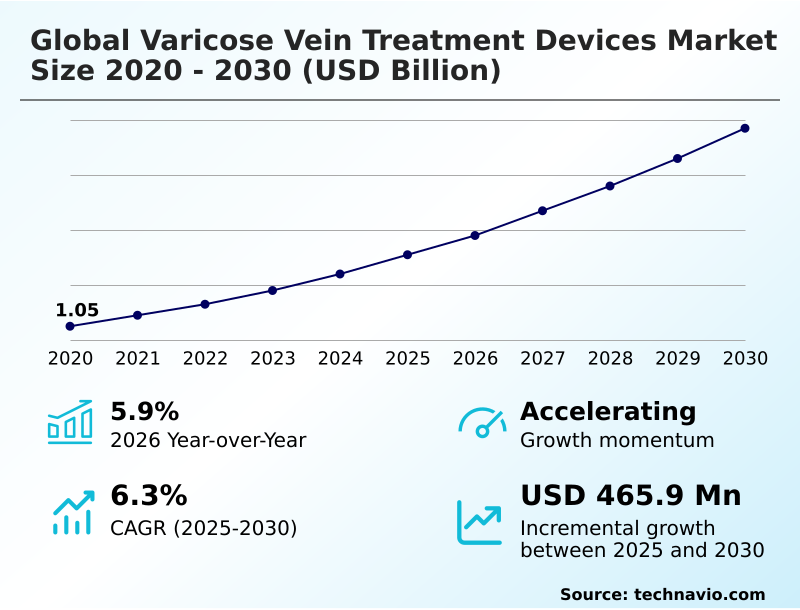

The Varicose Vein Treatment Devices Market size was valued at USD 1.31 billion in 2025 growing at a CAGR of 6.3% during the forecast period 2026-2030.

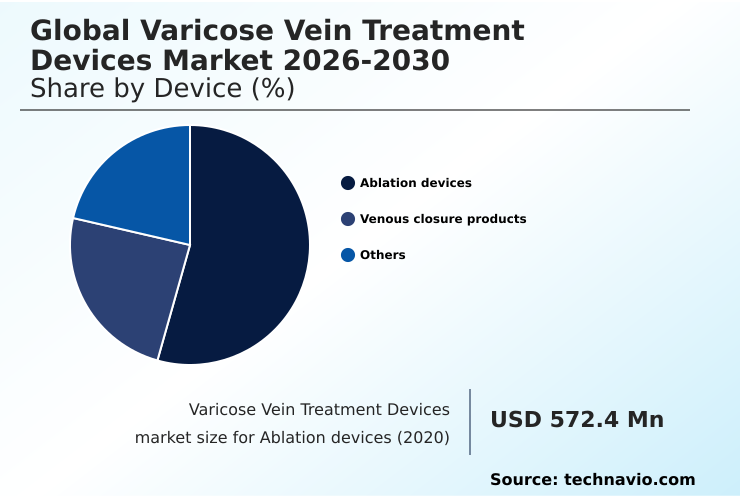

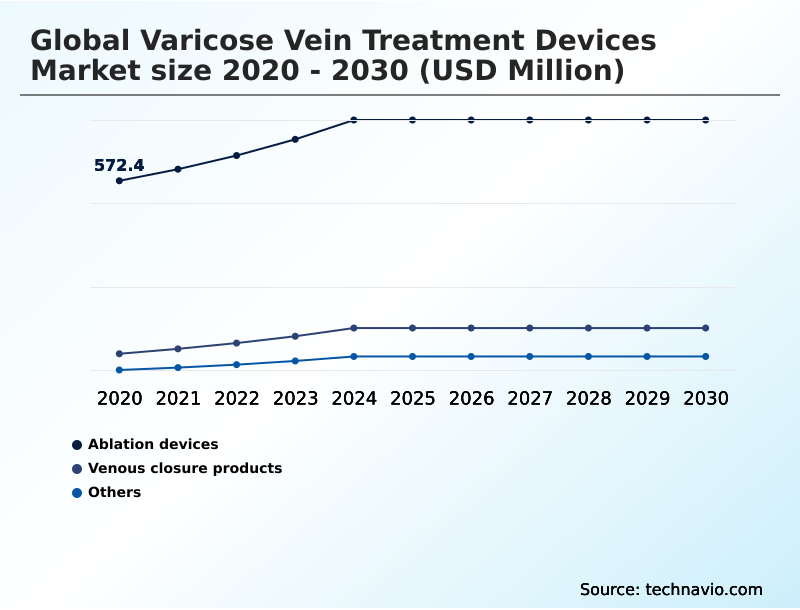

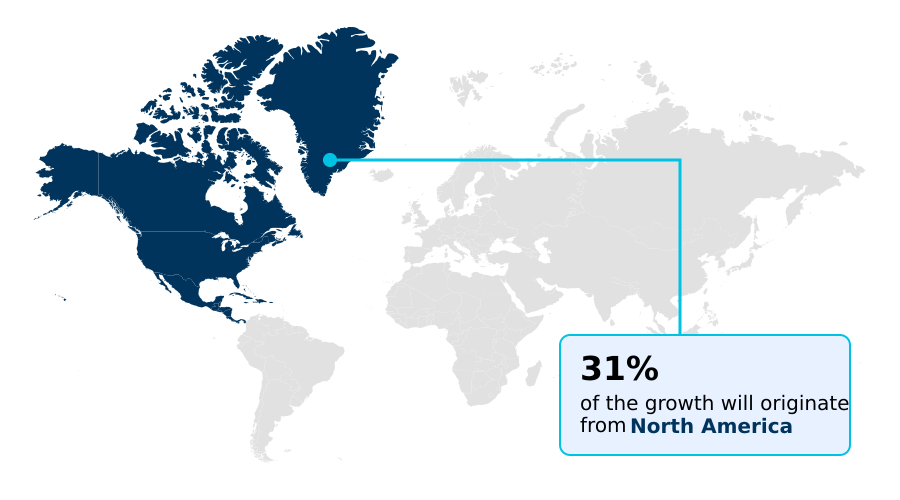

North America accounts for 31.2% of incremental growth during the forecast period. The Ablation devices segment by Device was valued at USD 683.9 million in 2024, while the Hospitals and clinics segment holds the largest revenue share by End-user.

The market is projected to grow by USD 720.4 million from 2020 to 2030, with USD 465.9 million of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Varicose Vein Treatment Devices Market Overview

The varicose vein treatment devices market is defined by a decisive shift toward minimally invasive procedures that improve patient outcomes and operational efficiency in clinical settings. Technologies such as endovenous thermal ablation and radiofrequency ablation have become standard, yet the field is rapidly advancing with non-thermal, non-tumescent options like cyanoacrylate adhesive closure and mechanochemical ablation. A typical ambulatory surgical center, by adopting a modern venous closure system for treating saphenous vein reflux, can increase patient throughput by reducing procedure and recovery times. This evolution is critical as North America alone is projected to contribute 31.2% of the market's incremental growth, reflecting high adoption of advanced endovascular therapy. The market's overall 5.9% year-over-year expansion is propelled by this innovation, which addresses conditions from chronic venous insufficiency to cosmetic concerns. The focus remains on refining catheter-based intervention and polidocanol foam sclerotherapy to minimize patient discomfort and enhance long-term efficacy, meeting demands for both medical and aesthetic-driven treatments in vascular surgery.

Drivers, Trends, and Challenges in the Varicose Vein Treatment Devices Market

Strategic decision-making for vein clinics increasingly revolves around balancing the cost of varicose vein treatment without insurance against clinical efficacy and patient satisfaction. The choice between mechanochemical ablation vs radiofrequency ablation, for instance, requires careful evaluation of upfront equipment costs, procedural consumables, and the potential for complications of endovenous laser ablation.

A key consideration is the varicose vein laser treatment recovery time, as faster recovery reduces patient downtime and improves clinic throughput. In a typical office-based setting, supplementing a primary procedure with an ultrasound-guided foam sclerotherapy procedure for residual varicosities can reduce the need for follow-up visits by over 50% compared to traditional methods.

This operational efficiency is critical for managing the best treatment for spider veins on legs and more complex conditions.

Furthermore, all devices must comply with tracking mandates like the FDA's UDI system to ensure traceability, which is vital for preventing deep vein thrombosis after vein surgery and managing the entire lifecycle of a venous closure system, including those utilizing cyanoacrylate glue for varicose veins.

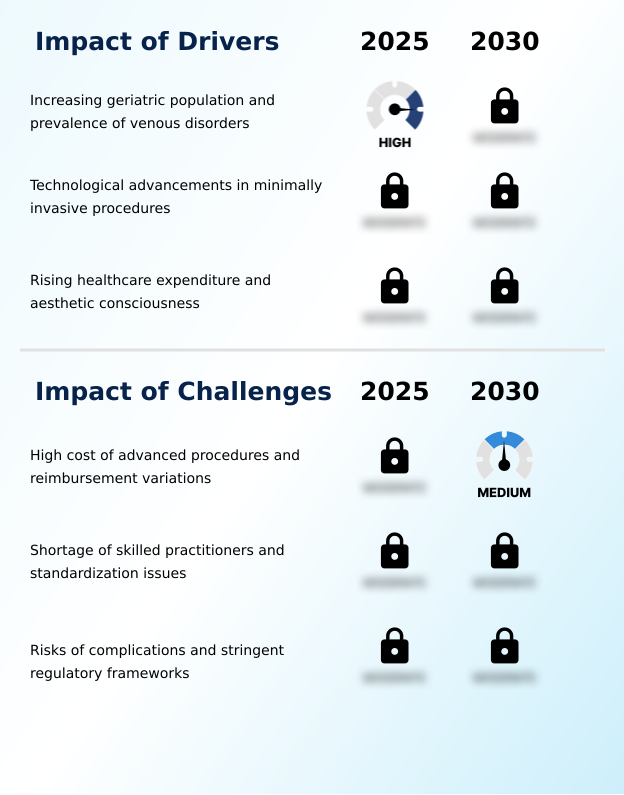

Primary Growth Driver: The primary market driver is the increasing geriatric population globally, coupled with a higher prevalence of venous disorders.

Market growth is propelled by the dual forces of a rising global geriatric population susceptible to chronic venous insufficiency and continuous technological advancements in minimally invasive procedures.

The development of endovenous thermal ablation and radiofrequency ablation has set a high standard for efficacy, creating a strong foundation for market expansion.

Demand is further amplified by lifestyle factors and a growing emphasis on aesthetics, expanding the patient pool beyond medical necessity to include cosmetic concerns.

This resilient demand structure supports sustained R&D in next-generation platforms, including high-intensity focused ultrasound and advanced venous stent system designs.

With Asia's market poised for a robust 7.6% CAGR, the global appetite for effective vein care solutions is creating significant opportunities for innovation in endovascular therapy.

Emerging Market Trend: A key market trend is the accelerated adoption of non-thermal and non-tumescent treatment modalities, which are displacing traditional thermal ablation techniques.

A defining market trend is the structural migration of procedures from hospitals to outpatient settings, including ambulatory surgical centers (ASCs) and office-based labs. This shift is enabled by the adoption of non-thermal, non-tumescent technologies like mechanochemical ablation and cyanoacrylate adhesive closure, which streamline workflows by eliminating the need for tumescent anesthesia.

As ASCs become a more prominent end-user segment, procurement is shifting toward portable, cost-effective devices. This includes advanced vascular access device solutions and integrated vein mapping technology to standardize procedures. The move toward office-based labs not only reduces healthcare system costs but also meets growing patient demand for convenient, minimally invasive endovenous therapy for both medical and cosmetic phlebology indications.

Key Industry Challenge: A key challenge affecting industry growth is the high cost of advanced procedures combined with significant variations in reimbursement policies.

A primary market challenge is the high capital cost of equipment for procedures like radiofrequency ablation, coupled with the recurring expense of single-use disposables for endovenous laser ablation. This financial barrier is magnified by inconsistent reimbursement policies and the rigorous pre-market approval processes of regulatory bodies such as the FDA and EMA.

A shortage of practitioners skilled in duplex ultrasound guidance for complex catheter-based intervention further constrains market growth, particularly in emerging economies. These factors create significant risk, as procedural complications like deep vein thrombosis not only pose patient safety issues but also expose manufacturers of even the most advanced venous stent systems to liability, potentially slowing the adoption of new technology.

Explore Full Market Dynamics Analysis Request Free Sample

Varicose Vein Treatment Devices Market Segmentation

The varicose vein treatment devices industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Device Segment Analysis

The ablation devices segment is estimated to witness significant growth during the forecast period.

The ablation devices segment dominates the varicose vein treatment devices market, primarily driven by the clinical shift from invasive surgery to minimally invasive thermal techniques.

This category, including radiofrequency ablation and endovenous laser ablation systems, leverages thermal energy for vein occlusion. These devices, integral to treating chronic venous insufficiency, are increasingly used in ambulatory phlebectomy.

The market for ablation devices stood at USD 726.6 million in 2025. Demand is bolstered by a preference for office-based procedures offering rapid recovery.

Manufacturers focus on improving catheter technology for navigating tortuous veins, a key factor in successful catheter-based intervention. The adoption of duplex ultrasound guidance ensures precision, solidifying this segment's leading position through superior outcomes in endovenous therapy.

The Ablation devices segment was valued at USD 683.9 million in 2024 and showed a gradual increase during the forecast period.

Varicose Vein Treatment Devices Market by Region: North America Leads with 31.2% Growth Share

North America is estimated to contribute 31.2% to the growth of the global market during the forecast period.

The global geographic landscape is characterized by varied growth trajectories and technology adoption rates.

Asia is set to expand at a 7.6% CAGR, the fastest globally, driven by rising healthcare investments and a large, underserved patient population seeking treatment for chronic vein disease.

In contrast, the mature markets of North America and Europe, which together represent nearly 60% of the market opportunity, focus on adopting next-generation technologies like high-intensity focused ultrasound and non-thermal venous closure systems.

Regulatory frameworks such as the European Union's Medical Device Regulation (MDR) create high barriers to entry, favoring established vendors with robust clinical data for their endovenous therapy devices.

This dynamic ensures that while growth in developed regions is steady, the most significant expansion potential resides in Asian markets.

Customer Landscape Analysis for the Varicose Vein Treatment Devices Market

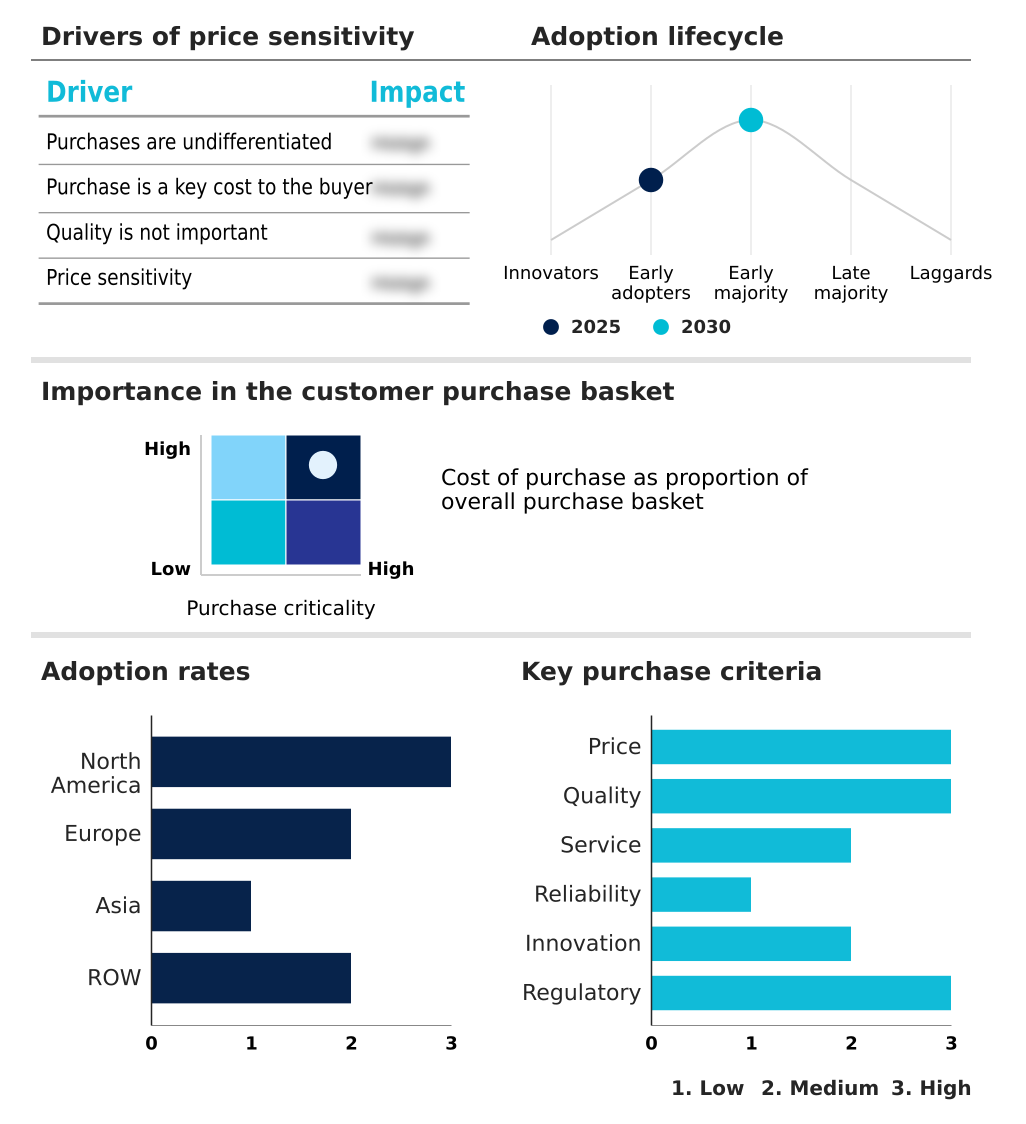

The varicose vein treatment devices market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the varicose vein treatment devices market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Varicose Vein Treatment Devices Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the varicose vein treatment devices market industry.

AngioDynamics Inc. - Key offerings range from endovenous thermal ablation catheters and non-thermal adhesive systems to transdermal lasers for aesthetic vein treatment, addressing diverse clinical and cosmetic needs.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AngioDynamics Inc.

- Becton Dickinson and Co.

- biolitec AG

- Boston Scientific Corp.

- Candela Corp.

- Cook Group Inc.

- Cutera Inc.

- Cynosure LLC

- Dornier MedTech GmbH

- Eufoton srl

- Fotona d.o.o

- Lasotronix

- LeMaitre Vascular Inc.

- Lumenis Be Ltd.

- Medtronic Plc

- Merit Medical Systems Inc.

- Quanta System S.p.A.

- Teleflex Inc.

- Terumo Corp.

- VVT Medical

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Varicose Vein Treatment Devices Market

- In May 2025, MedVasc AB announced the successful completion of an approximately USD 1 million funding round to advance its catheter-based device designed to enhance anesthetic procedures in varicose vein treatment and support its FDA submission process.

- In January 2025, Stryker announced a definitive agreement to acquire Inari Medical Inc., a move designed to strengthen its position in the venous thromboembolism segment by integrating Inari's peripheral vascular intervention technologies.

- In October 2025, THERACLION provided a strategic update on Sonovein, its robotic HIFU platform, announcing the completion of the VEINRESET pivotal US clinical trial, which reported a 96.8% 12-month occlusion rate and confirmed strong safety and efficacy.

- In February 2025, the Health Sciences Authority in Singapore granted regulatory approval for a next-generation mechanochemical ablation catheter from Vascular Dynamics Corp., expanding access to minimally invasive options for patients with complex venous anatomies.

Research Analyst Overview: Varicose Vein Treatment Devices Market

The varicose vein treatment devices market is driven by a fundamental clinical migration away from invasive surgery toward less traumatic endovenous techniques. Although ablation devices remain the dominant segment, the focus of innovation has shifted to non-thermal, non-tumescent (NTNT) technologies such as mechanochemical ablation and cyanoacrylate adhesive closure, which eliminate the need for tumescent anesthesia.

This trend directly impacts boardroom decisions on capital expenditure and portfolio strategy, as vendors must align with stringent regulatory pathways like the European Union's Medical Device Regulation (MDR) to prove the safety and efficacy of novel venous closure systems. While the market exhibits a 5.9% year-over-year expansion, competition is intensifying.

Success now hinges on demonstrating superior outcomes in treating chronic venous insufficiency and related conditions like deep vein thrombosis, forcing providers of endovenous thermal ablation and radiofrequency ablation to innovate or risk being displaced by more efficient catheter-based intervention methods.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Varicose Vein Treatment Devices Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 292 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.3% |

| Market growth 2026-2030 | USD 465.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 5.9% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Russia, China, India, Japan, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, UAE, South Africa, Saudi Arabia and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Varicose Vein Treatment Devices Market: Key Questions Answered in This Report

-

What is the expected growth of the Varicose Vein Treatment Devices Market between 2026 and 2030?

-

The Varicose Vein Treatment Devices Market is expected to grow by USD 465.9 million during 2026-2030, registering a CAGR of 6.3%. Year-over-year growth in 2026 is estimated at 5.9%%. This acceleration is shaped by increasing geriatric population and prevalence of venous disorders, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Device (Ablation devices, Venous closure products, and Others), End-user (Hospitals and clinics, and Ambulatory surgical centers), Application (Endovenous ablation, Sclerotherapy, and Surgical ligation and stripping) and Geography (North America, Europe, Asia, Rest of World (ROW)). Among these, the Ablation devices segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, Asia and Rest of World (ROW). North America is estimated to contribute 31.2% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, Russia, China, India, Japan, South Korea, Indonesia, Thailand, Singapore, Australia, Brazil, UAE, South Africa, Saudi Arabia and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is increasing geriatric population and prevalence of venous disorders, which is accelerating investment and industry demand. The main challenge is high cost of advanced procedures and reimbursement variations, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Varicose Vein Treatment Devices Market?

-

Key vendors include AngioDynamics Inc., Becton Dickinson and Co., biolitec AG, Boston Scientific Corp., Candela Corp., Cook Group Inc., Cutera Inc., Cynosure LLC, Dornier MedTech GmbH, Eufoton srl, Fotona d.o.o, Lasotronix, LeMaitre Vascular Inc., Lumenis Be Ltd., Medtronic Plc, Merit Medical Systems Inc., Quanta System S.p.A., Teleflex Inc., Terumo Corp. and VVT Medical. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Varicose Vein Treatment Devices Market Research Insights

Market dynamics are increasingly shaped by regulatory frameworks and site-of-service economics. The FDA's Unique Device Identification (UDI) system, for instance, adds a layer of tracking and compliance for all vascular access device products, influencing procurement decisions in interventional radiology departments.

In practice, an office-based laboratory's choice between thermal and non-thermal endovenous therapy is driven by capital cost, reimbursement rates, and patient demand for cosmetic phlebology. While North America's market opportunity at 31.19% slightly outpaces Asia's 29.1%, the latter exhibits faster adoption of cost-effective solutions for chronic vein disease.

This geographic divergence reflects differing priorities between mature and emerging healthcare systems in their approach to vascular medicine and venous ulcer management.

We can help! Our analysts can customize this varicose vein treatment devices market research report to meet your requirements.

RIA -

RIA -