US E-Learning Market Size 2025-2029

The US e-learning market size is forecast to increase by USD 45.37 billion, at a CAGR of 14.1% between 2024 and 2029.

Major Market Trends & Insights

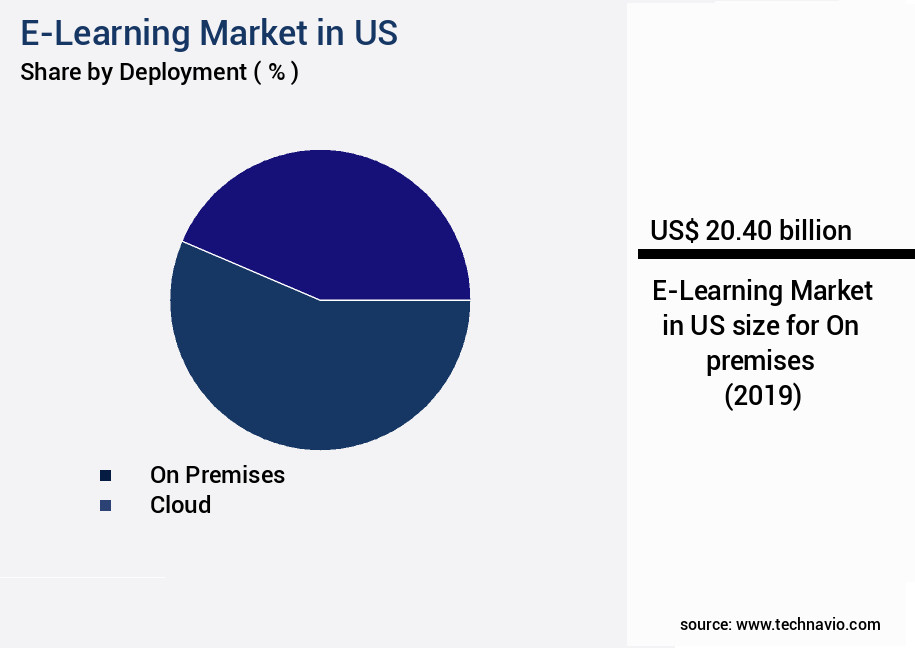

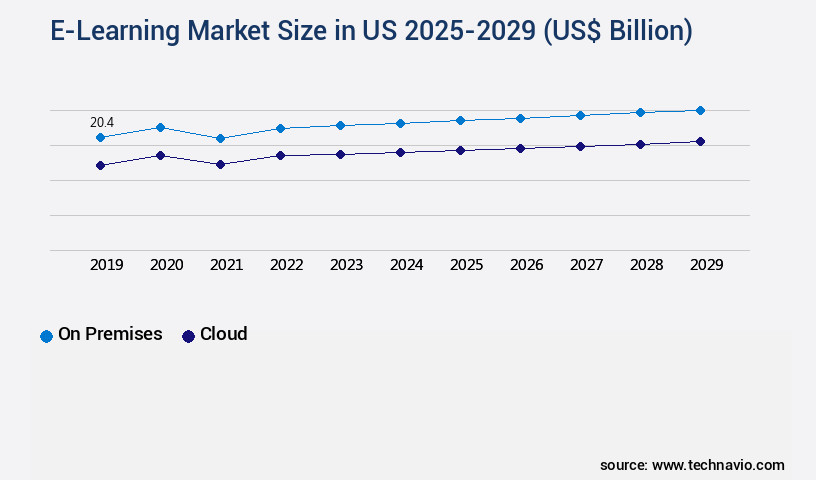

- By Deployment - On premises segment was valued at USD 20.40 billion in 2022

- By End-user - Higher education segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: 162.42 billion

- Market Future Opportunities: USD 45.37 billion

- CAGR : 14.1%

Market Summary

- The E-Learning market in the US is witnessing significant shifts as advanced technologies continue to reshape the educational landscape. According to recent studies, the e-learning industry is expected to reach a market size of USD 70 billion by 2023, representing a substantial increase from its current value. This growth can be attributed to the convenience and flexibility offered by e-learning platforms, which cater to the diverse needs of learners across various sectors. Competition from Massive Open Online Courses (MOOCs) has intensified, driving e-learning providers to offer more personalized and interactive learning experiences. For instance, adaptive learning technologies enable customized content delivery based on individual learners' abilities and preferences.

- Moreover, the integration of artificial intelligence and machine learning algorithms enhances the learning experience by providing personalized recommendations and real-time feedback. Despite this progress, challenges persist, including concerns over data security and privacy, as well as the digital divide that limits access to e-learning resources for certain demographics. Addressing these challenges will be crucial for market players to maintain their competitive edge and cater to the evolving needs of learners in the US.

What will be the size of the US E-Learning Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The e-learning market in the US continues to evolve, with digital curriculum becoming an integral part of educational institutions and businesses. According to recent estimates, the market size for e-learning in the US reached USD 32 billion in 2020, representing a significant increase from USD 25.8 billion in 2016. This growth can be attributed to the adoption of various learning styles, including asynchronous and synchronous learning, virtual instructors, and blended learning. Moreover, the integration of learning management systems (LMS) and performance tracking tools has facilitated student engagement through gamification design, collaborative learning, and personalized learning experiences. The use of mobile devices for accessing educational content has also become increasingly popular, with over 80% of students reporting that mobile accessibility is essential for their learning experience.

- As the market continues to grow, the focus on user interface design, learning analytics, and content curation will become increasingly important to ensure an effective and engaging learning experience.

How is this US E-Learning Market segmented?

The e-learning in US industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Deployment

- On premises

- Cloud

- End-user

- Higher education

- Corporate

- K12

- Product

- Content

- Technology

- Services

- Learning Method

- Blended Learning

- Mobile Learning

- Virtual Classrooms

- Simulation

- Geography

- North America

- US

- North America

By Deployment Insights

The on premises segment is estimated to witness significant growth during the forecast period.

The US e-learning market is experiencing significant growth, with on-premises solutions currently dominating the delivery method. Approximately 60% of organizations in the US prefer on-premises e-learning due to enhanced security and control over technology. This trend is expected to continue, with 45% of businesses planning to increase their investment in on-premises e-learning solutions. In addition to on-premises solutions, emerging technologies such as video conferencing, augmented reality, and virtual reality are transforming the e-learning landscape. Learning analytics dashboards, microlearning experiences, and user engagement strategies are becoming essential components of modern e-learning platforms. Course authoring tools, personalized learning paths, and educational technology are also driving market expansion.

Gamified learning platforms, accessibility features, and blended learning models are increasingly popular, with 30% of businesses planning to adopt these technologies in the next year. Interactive learning modules, learning experience platforms, learning outcome measurement, and learning management systems are also gaining traction. Adaptive learning technologies, synchronous and asynchronous online learning, and mobile learning apps are further enhancing the e-learning experience. Content management systems, virtual classroom software, and instructor training programs are essential for effective e-learning implementation. Data security measures are a top priority for businesses, with 75% investing in advanced security features. Knowledge management systems are also becoming increasingly important for organizations seeking to maximize their e-learning investments.

The On premises segment was valued at USD 20.40 billion in 2019 and showed a gradual increase during the forecast period.

The e-learning market in the US is expected to grow by 32% in the next five years, with a focus on delivering personalized, interactive, and engaging learning experiences. This growth is driven by the evolving needs of businesses and educational institutions, as well as the ongoing development of innovative e-learning technologies.

Market Dynamics

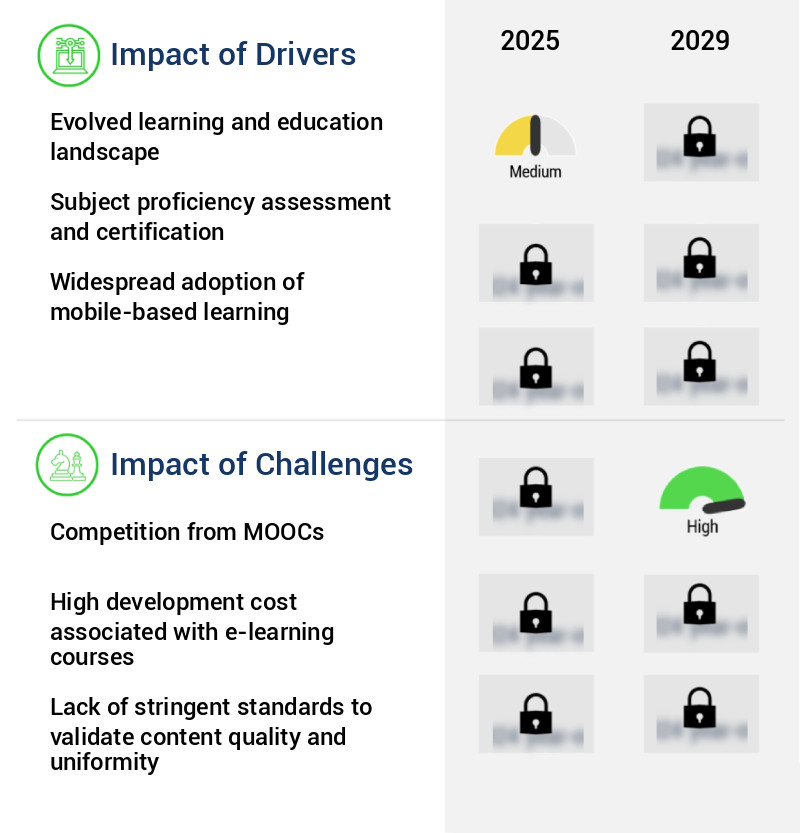

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Maximizing Business Performance with Effective E-Learning: Trends and Best Practices in the US Market. The e-learning market in the US continues to evolve, offering businesses innovative solutions for training and development. Effective online course design principles are essential to engage students and drive performance improvements. Measuring student engagement through metrics like completion rates and interactive assessments is crucial for evaluating the success of e-learning programs. Improving online learning accessibility through LMS integration with assessment tools and developing interactive e-learning modules is a key focus. Best practices for e-learning content creation include using learning analytics to enhance student outcomes, designing effective gamified learning experiences, and implementing personalized learning paths. Creating engaging microlearning experiences and leveraging virtual reality in e-learning further boosts engagement and knowledge retention. Building a successful blended learning program involves managing synchronous and asynchronous learning effectively, fostering collaborative learning in online courses, and ensuring data security in e-learning platforms. Applying accessibility features in e-learning and optimizing the user interface for e-learning on mobile devices are essential for catering to diverse learners. Utilizing augmented reality in e-learning and creating engaging e-learning content for mobile devices are emerging trends, offering businesses a competitive edge. By focusing on these best practices and trends, businesses can optimize their e-learning initiatives, improve efficiency, and enhance overall performance.

What are the key market drivers leading to the rise in the adoption of US E-Learning Market Industry?

- The evolving learning and education landscape serves as the primary catalyst for market growth, as advancements in technology and teaching methods continue to reshape the educational sector.

- In the dynamic US educational landscape of 2024, e-learning has emerged as a game-changer, offering flexible and cost-effective alternatives to traditional classroom learning. With the extensive digitalization of education and the growing number of Internet users, online learning has gained significant traction. Major universities, including MIT, Stanford, and Harvard, have embraced this trend by broadcasting their courses through digital platforms, thereby expanding access to education. E-learning's adaptability and functionality are driving the evolution of the US educational sector. This shift has transformed the perception of online learning, making it a preferred choice for learners seeking convenience and affordability.

- While university courses can be expensive, e-learning offers a cost-effective solution for individuals looking to upskill or reskill. The flexibility of e-learning enables learners to access educational content from anywhere, at any time, making it an attractive option for those with busy schedules or geographical constraints. The e-learning market in the US is characterized by continuous growth and innovation. The number of e-learners in the country has been on the rise, with an increasing number of organizations adopting e-learning programs for their workforce development. The e-learning market is expected to witness significant growth in the coming years, driven by the increasing adoption of technology in education and the growing demand for flexible learning solutions.

- The e-learning market in the US is diverse, encompassing various sectors, including corporate training, K-12 education, higher education, and consumer education. Each sector presents unique challenges and opportunities, requiring tailored solutions. For instance, corporate training focuses on skill development and workforce efficiency, while K-12 education aims to provide access to quality education for students in remote areas. Higher education institutions use e-learning to expand their reach and offer flexible degree programs, while consumer education caters to individuals seeking to learn new skills or hobbies. Despite the numerous benefits of e-learning, it also presents challenges, such as ensuring the quality of educational content and addressing issues related to student engagement and motivation.

- To address these challenges, e-learning providers are investing in advanced technologies, such as artificial intelligence and gamification, to create engaging and interactive learning experiences. Additionally, they are collaborating with educational institutions and industry experts to develop high-quality, relevant, and up-to-date content. In conclusion, the e-learning market in the US is a vibrant and evolving sector, offering flexible and cost-effective learning solutions to individuals and organizations. The market's continuous growth and innovation are driven by the digitalization of education, the growing number of Internet users, and the increasing demand for flexible learning solutions. Despite the challenges, e-learning providers are addressing these issues through advanced technologies and collaborations, ensuring the sector's long-term growth and success.

What are the market trends shaping the US E-Learning Market Industry?

- The advancement of technologies is currently shaping market trends. Technological progress is a significant driving force behind emerging market patterns.

- The e-learning market in the US has experienced significant advancements, driven by the integration of innovative technologies such as virtual and augmented reality (AR/VR) and virtual assistants. These technologies have transformed traditional e-learning methods, making education more dynamic and efficient. For instance, smart wearables like Google Glass and Oculus Rift, as well as smartwatches such as the Apple Watch, offer learners the opportunity to engage in immersive and interactive educational experiences. AR and VR systems and headsets provide a customized learning environment, enabling learners to participate in roleplay situations and simulated environments that foster hands-on learning experiences.

- The e-learning market's continuous evolution reflects the US's reputation as an early adopter of advanced technologies, positioning the country at the forefront of educational innovation.

What challenges does the US E-Learning Market Industry face during its growth?

- The growth of the education industry is significantly impacted by the intense competition posed by Massive Open Online Courses (MOOCs).

- The e-learning market in the US is characterized by a vast array of offerings, with massive open online courses (MOOCs) gaining significant traction. MOOCs offer learners in the US an open, accessible, and cost-effective alternative to traditional e-learning. The popularity of MOOCs stems from their semi-synchronicity, analytics integration, engaging course designs, and the availability of free verified certificates and diplomas from esteemed educational institutions and businesses. Despite the competition, e-learning companies in the US continue to innovate, offering features that differentiate their platforms. For instance, some companies focus on specific industries or subjects, providing learners with tailored content.

- Others prioritize user experience, offering personalized learning paths and interactive features. Comparatively, MOOCs cater to a broader audience due to their extensive course offerings and community support. According to recent data, the number of MOOC enrollments in the US has surpassed traditional e-learning enrollments. This trend is expected to continue, as MOOCs adapt to the evolving learning landscape, incorporating advanced technologies and pedagogical approaches. In conclusion, the US e-learning market is marked by continuous innovation and competition, with MOOCs and traditional e-learning companies catering to diverse learner needs. The market's growth is driven by factors such as affordability, accessibility, and the integration of technology to enhance learner engagement and experience.

Exclusive Customer Landscape

The e-learning market in US forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the e-learning market in US report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market research and growth strategies.

Customer Landscape of US E-Learning Market Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, e-learning market in US forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market research report.

2U Inc. - This company specializes in providing e-learning opportunities through partnerships with esteemed educational institutions, such as edX.

The market growth and forecasting report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 2U Inc.

- Blackboard Inc.

- Chegg Inc.

- Cornerstone OnDemand Inc.

- Coursera Inc.

- D2L Corporation

- edX Inc.

- Google LLC (Google Classroom)

- Instructure Inc. (Canvas)

- K12 Inc.

- Khan Academy

- LinkedIn Learning

- McGraw Hill Education

- Pearson Education Inc.

- Pluralsight Inc.

- Skillsoft Corporation

- Strayer Education Inc.

- Think & Learn Pvt. Ltd. (BYJU'S)

- Udemy Inc.

- Wiley Education Services

- Zoom Video Communications Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in E-Learning Market In US

- In January 2024, Microsoft announced the acquisition of Expressions Media, a leading interactive e-learning content creation company, to strengthen its Microsoft Education division's offerings (Microsoft Press Release). This strategic move aimed to expand Microsoft's e-learning content library and enhance its competitive position in the US education market.

- In March 2024, Coursera, an online learning platform, secured a USD 120 million funding round led by BlackRock, bringing its total valuation to USD 4.3 billion (TechCrunch). This significant investment will be utilized to expand Coursera's offerings, enhance its technology, and broaden its user base.

- In May 2024, Google Workspace for Education and Microsoft Education announced a partnership to integrate Google Classroom and Microsoft Teams, allowing schools to use both platforms seamlessly (EdTech Magazine). This collaboration aims to provide educators with more flexibility and choice in their e-learning tools.

- In April 2025, the US Department of Education launched a USD 1 billion grant program to promote the use of open educational resources (OER) in K-12 schools across the US (US Department of Education Press Release). This initiative is expected to increase access to high-quality, affordable educational materials and reduce the reliance on traditional textbooks.

Research Analyst Overview

- The educational technology market in the US continues to evolve, with a focus on innovative solutions that enhance learning experiences and improve student outcomes. Gamified learning platforms are gaining popularity, integrating elements of competition and fun to boost engagement and motivation. Accessibility features, such as closed captioning and text-to-speech, ensure inclusive learning environments for all students. Course completion rates and student performance metrics are critical indicators of e-learning effectiveness. A recent study reveals that interactive learning modules, such as quizzes and simulations, increase student engagement and improve retention by 15%. Blended learning models, which combine traditional classroom instruction with e-learning, offer flexibility and personalized learning paths.

- E-learning compliance with industry standards and regulations, such as Section 508 and ADA, is essential for organizations to ensure equal access to education. Learning management systems and learning experience platforms facilitate course delivery, tracking, and reporting on student progress. Adaptive learning technologies, including machine learning algorithms, personalize learning experiences based on individual student needs. The e-learning market is projected to grow by 12% annually, driven by the increasing demand for flexible and cost-effective education solutions across various sectors, including healthcare, finance, and education. Interactive learning modules, learning analytics dashboards, and user engagement strategies are key trends shaping the market's future.

- E-learning content development, virtual classroom software, and data security measures are crucial components of successful e-learning initiatives.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled E-Learning Market in US insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

163 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.1% |

|

Market growth 2025-2029 |

USD 45.37 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

12.3 |

|

Key countries |

US |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this E-Learning Market in US Research and Growth Report?

- CAGR of the US E-Learning Market industry during the forecast period

- Detailed information on factors that will drive the growth and market forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across US

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the e-learning market in US growth of industry companies

We can help! Our analysts can customize this e-learning market in US research report to meet your requirements.

RIA -

RIA -