India Agrochemicals Market Size 2026-2030

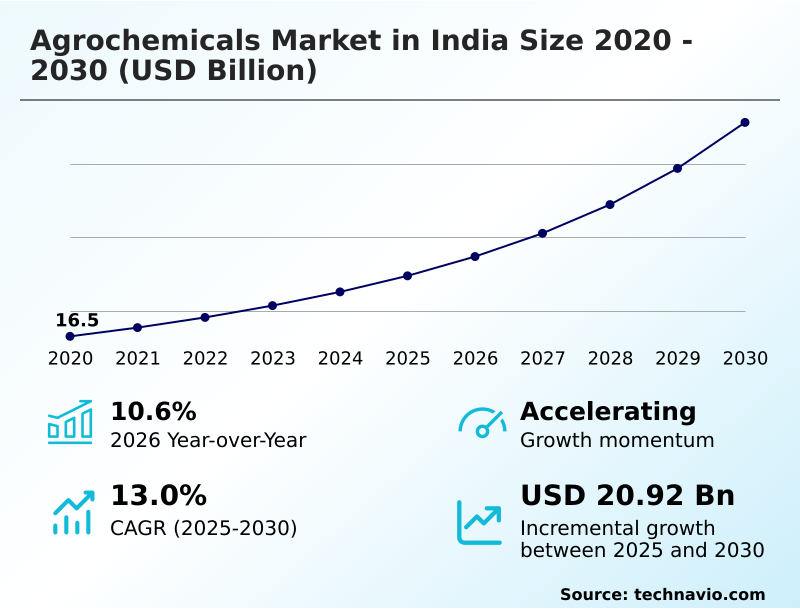

The India Agrochemicals Market size was valued at USD 24.75 billion in 2025, growing at a CAGR of 13% during the forecast period 2026-2030.

Major Market Trends & Insights

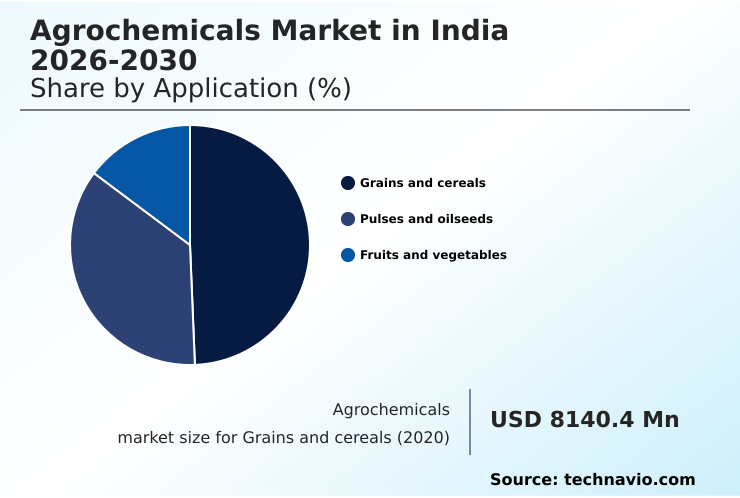

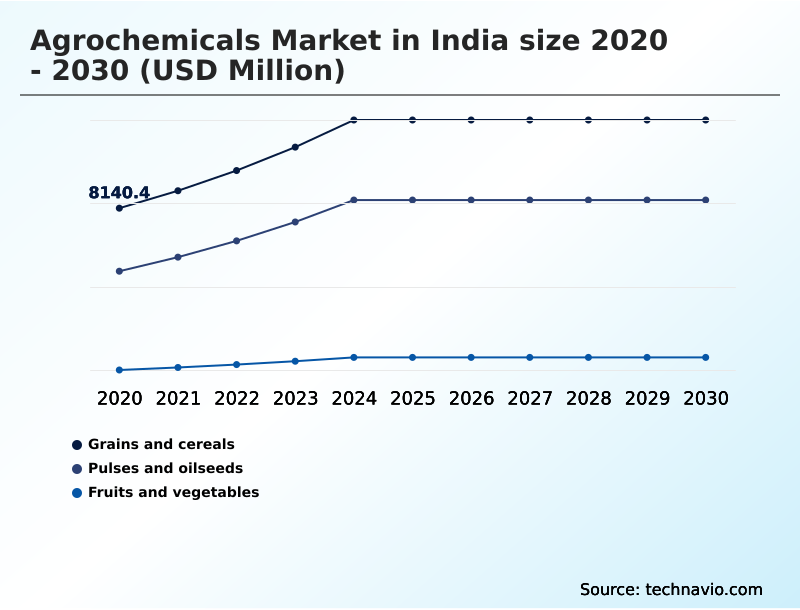

- By Application - Grains and cereals segment was valued at USD 11.25 billion in 2024

- By Product - Fertilizers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 29.18 billion

- Market Future Opportunities 2025-2030: USD 20.92 billion

- CAGR from 2025 to 2030 : 13%

Market Summary

- The agrochemicals market in India is defined by its direct correlation with agricultural cycles, with fertilizer consumption outpacing pesticide use by nearly 2:1 in terms of volume. This sector is fundamental to sustaining high crop yields and ensuring national food security.

- A key operational scenario involves manufacturers managing complex supply chains to align production with the highly concentrated demand windows of the Kharif and Rabi seasons, where a delay of even two weeks can lead to significant inventory mismatches.

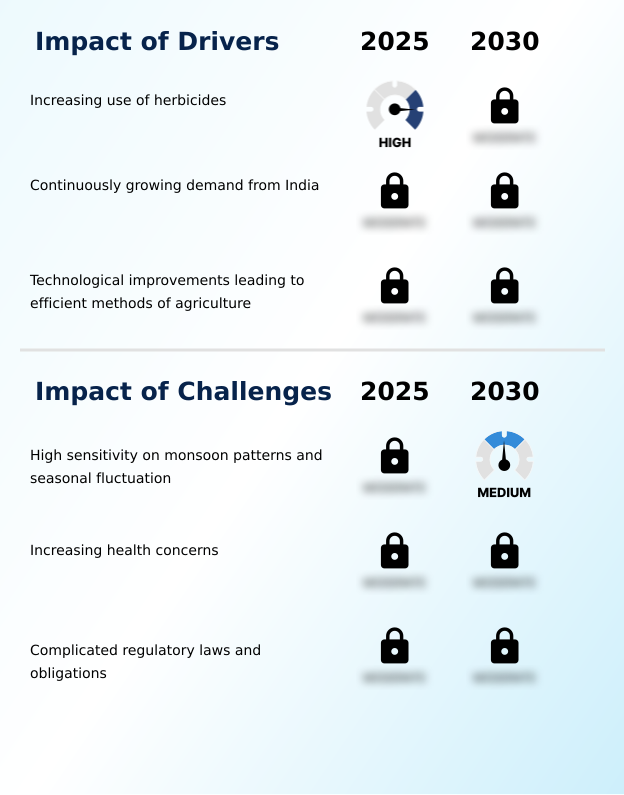

- The primary driver is the increasing use of herbicides, a response to rising rural labor costs which have grown by over 15% in the last five years. This shift allows for more efficient weed management and protects yield potential.

- Conversely, the market's greatest challenge is its high sensitivity to monsoon patterns, as deficient rainfall can shrink the addressable market by up to 30% in affected regions, creating significant demand volatility.

What will be the Size of the India Agrochemicals Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the India Agrochemicals Market Segmented?

The india agrochemicals industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Grains and cereals

- Pulses and oilseeds

- Fruits and vegetables

- Product

- Fertilizers

- Pesticides

- Type

- Potassic

- Nitrogenous

- Phosphatic

- Geography

- APAC

- India

- APAC

How is the India Agrochemicals Market Segmented by Application?

The grains and cereals segment is estimated to witness significant growth during the forecast period.

The grains and cereals segment is a cornerstone of the agrochemicals market in India, accounting for nearly 50% of total consumption due to the widespread cultivation of staple crops.

The use of specialized insecticides and nitrogenous fertilizers is essential for protecting high-yielding rice and wheat varieties, which has led to a 10% increase in yield protection compared to five years ago.

This segment's demand is characterized by high-volume, seasonal purchasing patterns directly linked to the Kharif and Rabi cycles. Consequently, manufacturers of formulated insecticides and granular solutions focus their supply chains on ensuring timely product availability in key grain-producing regions.

The adoption of specific post-emergence herbicides and soil conditioners is driven by the need to maximize output from limited arable land and support national food security.

The Grains and cereals segment was valued at USD 11.25 billion in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the India Agrochemicals Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the agrochemicals market in India is increasingly shaped by crop-specific needs and regulatory frameworks. For instance, the approach to agrochemicals for grains and cereals cultivation differs significantly from that for horticultural crops, with the former showing a 20% higher consumption of nitrogenous fertilizers.

- Understanding the impact of herbicides on indian crop yield is critical for manufacturers, as product efficacy directly influences purchasing decisions and brand loyalty. The effect of fertilizer subsidies on indian agriculture continues to be a major factor, influencing affordability and the adoption rates of balanced fertilization practices among smallholder farmers.

- Supply chain planning must account for these subsidies, as they can cause demand spikes that are 30-40% higher than non-subsidized periods. Furthermore, evolving pesticide regulations for fruit and vegetable farming are compelling companies to invest more in developing products with lower residue levels.

- Finally, the inherent challenges of monsoon for agrochemical demand require robust forecasting models and agile distribution networks to prevent stockouts or oversupply, ensuring that essential products are available when farmers need them most.

What are the key market drivers leading to the rise in the adoption of India Agrochemicals Industry?

- The increasing utilization of herbicides is a key market driver, primarily fueled by rising labor costs and the agricultural sector's need for more efficient weed control solutions.

- The rising utilization of herbicides is a primary driver for the agrochemicals market in India, directly resulting from rural labor costs increasing by over 20% in the last decade.

- This economic pressure forces a shift from manual weeding to more efficient chemical weed control, which can improve crop yields by 15-25% by preventing nutrient competition. This evolution is particularly evident in large-scale cultivation where timely weed management is critical.

- The introduction of selective broad-spectrum herbicide products offers greater flexibility in managing weed growth.

- As mechanization in agriculture advances, the use of plant growth regulators and other crop protection chemicals is becoming integral to farm management, reducing time and labor dependency.

What are the market trends shaping the India Agrochemicals Industry?

- The implementation of integrated pest management represents an important emerging trend, signaling a market-wide shift toward more sustainable and holistic crop protection methods.

- A significant trend reshaping the agrochemicals market in India is the adoption of integrated pest management (IPM), a practice that can reduce reliance on conventional pesticides by up to 30%. This shift is driven by increasing demand for residue-free produce for both domestic and export markets, which now require 15% lower chemical traces than a decade ago.

- Consequently, companies are expanding their portfolios to include biological control agents and bio-fertilizers. This evolution toward sustainable agriculture necessitates greater farmer education on monitoring pest life cycles and using chemical interventions as a last resort. The focus is on achieving a balance between high crop yields and ecological preservation through the intelligent application of modern science and agri-input products.

What challenges does the India Agrochemicals Industry face during its growth?

- The market's high sensitivity to monsoon patterns and resulting seasonal fluctuations poses a significant challenge, creating demand unpredictability and impacting operational stability across the industry.

- A primary challenge confronting the agrochemicals market in India is its extreme sensitivity to monsoon patterns, with over 50% of the nation's farmland being rain-fed. A delay or deficit in monsoon rains can lead to a demand contraction of up to 40% for products like phosphatic fertilizers and fungicides in the crucial initial weeks of the sowing season.

- This unpredictability complicates demand forecasting for manufacturers, leading to inventory imbalances and price volatility. Seasonal fluctuations create narrow application windows, limiting the effective use of specialty nutrients and other time-sensitive treatments. To mitigate this, companies are developing climate-smart solutions and investing in custom synthesis manufacturing for weather-resilient products.

Exclusive Technavio Analysis on Customer Landscape

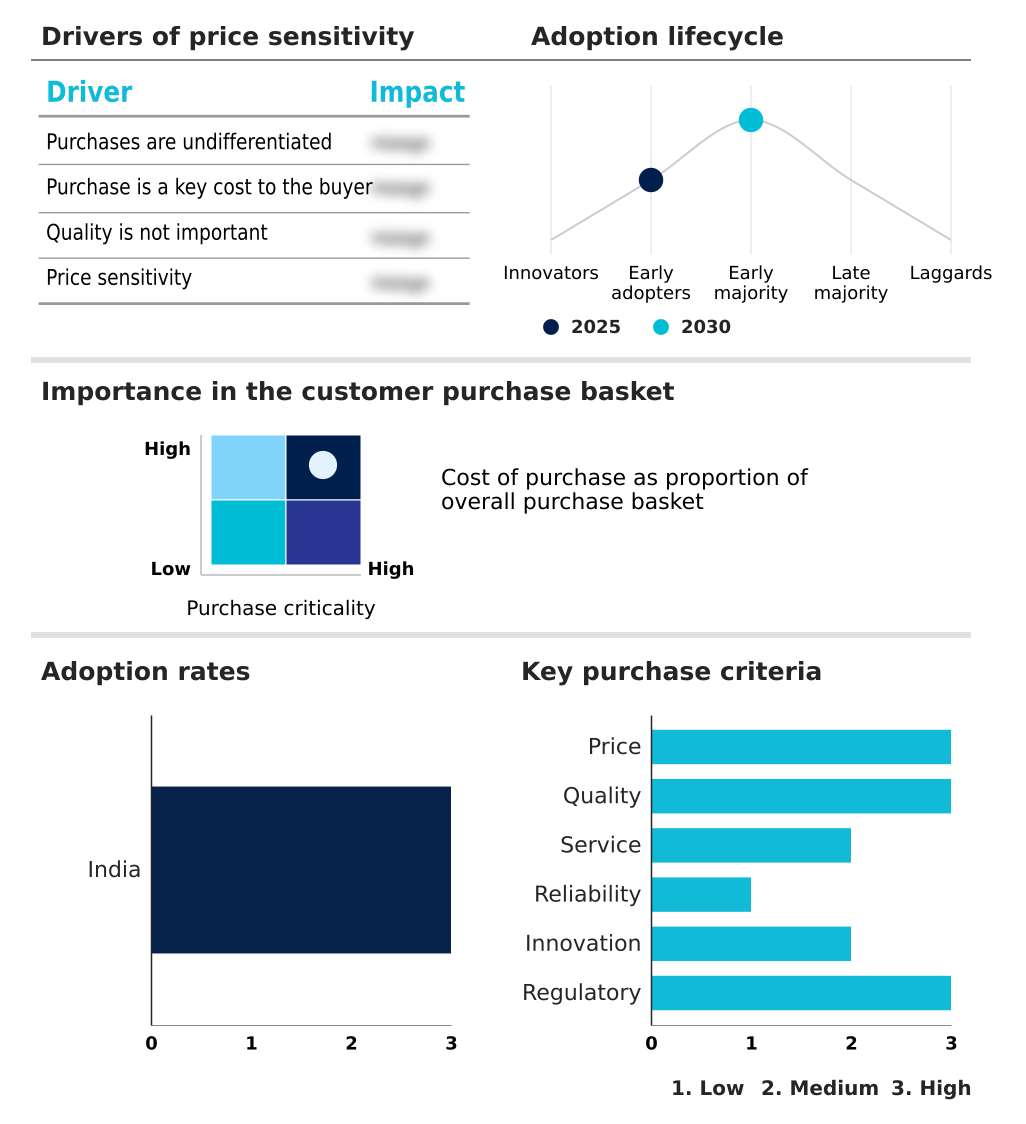

The india agrochemicals market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the india agrochemicals market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of India Agrochemicals Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, india agrochemicals market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Bayer AG - Analysis indicates a focus on comprehensive crop management solutions, including advanced herbicides, insecticides, fungicides, seed treatments, and integrated crop protection technologies for enhanced agricultural productivity.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Bayer AG

- Bharat Rasayan Ltd.

- Coromandel International Ltd.

- Corteva Inc.

- Crystal Crop Protection Ltd.

- Dhanuka Agritech Ltd.

- Gharda Chemicals Ltd.

- Godrej Agrovet Ltd.

- India Pesticides Ltd.

- Indofil Industries Ltd.

- National Fertilizers Ltd.

- PI Industries Ltd.

- Rallis India Ltd.

- Rashtriya Chemicals Ltd.

- Sharda Cropchem Ltd.

- Syngenta Crop Protection AG

- Tagros Chemicals India Ltd.

- UPL Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Fertilizers and Agricultural Chemicals industry, there is a significant regulatory push toward sustainable agriculture, mandating lower chemical residue limits and promoting the use of bio-fertilizers and integrated pest management techniques, directly impacting product development in the agrochemicals market in India.

- The adoption of digital advisory service platforms and precision application technologies has accelerated, allowing for more efficient use of inputs like water-soluble products and reducing environmental contamination, thereby altering farmer purchasing behavior.

- A strategic emphasis on expanding domestic manufacturing capacity for technical-grade pesticides and active ingredients is reducing reliance on imports, which helps stabilize the supply chain and mitigate price volatility caused by external market fluctuations and supports food security.

- Growing consumer demand for organic and residue-free produce is creating new opportunities for specialty nutrients and biological control agents, compelling manufacturers to diversify their portfolios beyond traditional synthetic chemicals to meet evolving market requirements for soil health.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled India Agrochemicals Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 172 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 13% |

| Market growth 2026-2030 | USD 20918.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 10.6% |

| Key countries | India |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ecosystem of the agrochemicals market in India operates through a multi-layered value chain, with the grains and cereals segment alone driving nearly 50% of total demand. The process begins with raw material suppliers providing chemical intermediates to manufacturers like Bayer AG and Corteva Inc. These companies focus on R&D to produce a diverse portfolio of fertilizers and pesticides.

- The next layer consists of an extensive distribution network of over 300,000 retailers and cooperative societies that ensure products reach end-users—the farmers. Regulatory bodies impose stringent guidelines on product formulation and application, influencing manufacturing processes. Supporting this ecosystem are logistics partners managing complex supply chains and R&D institutions collaborating on sustainable solutions.

- The entire framework is designed to support the country's agricultural output, with a focus on improving nutrient use efficiency and crop protection.

What are the Key Data Covered in this India Agrochemicals Market Research and Growth Report?

-

What is the expected growth of the India Agrochemicals Market between 2026 and 2030?

-

The India Agrochemicals Market is expected to grow by USD 20.92 billion during 2026-2030, registering a CAGR of 13%. Year-over-year growth in 2026 is estimated at 10.6%%. This acceleration is shaped by increasing use of herbicides, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Grains and cereals, Pulses and oilseeds, and Fruits and vegetables), Product (Fertilizers, and Pesticides), Type (Potassic, Nitrogenous, and Phosphatic) and Geography (APAC). Among these, the Grains and cereals segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers APAC. Country-level analysis includes India, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is increasing use of herbicides, which is accelerating investment and industry demand. The main challenge is high sensitivity on monsoon patterns and seasonal fluctuation, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the India Agrochemicals Market?

-

Key vendors include Bayer AG, Bharat Rasayan Ltd., Coromandel International Ltd., Corteva Inc., Crystal Crop Protection Ltd., Dhanuka Agritech Ltd., Gharda Chemicals Ltd., Godrej Agrovet Ltd., India Pesticides Ltd., Indofil Industries Ltd., National Fertilizers Ltd., PI Industries Ltd., Rallis India Ltd., Rashtriya Chemicals Ltd., Sharda Cropchem Ltd., Syngenta Crop Protection AG, Tagros Chemicals India Ltd. and UPL Ltd.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape of the agrochemicals market in India is fragmented, with over 18 major players, yet consolidated at the top, where the top five companies account for nearly 40% of the market share. Key vendors like UPL Ltd. and Dhanuka Agritech are actively shaping the market through strategic initiatives.

- For instance, the launch of a digital advisory service to provide real-time weather data helps farmers mitigate risks from erratic monsoons, which can impact crop cycles by up to three weeks. Similarly, the introduction of new broad-spectrum herbicides for critical crops like cotton and soybean directly addresses the need for long-duration weed management.

- These innovations are a direct response to the operational challenges farmers face, particularly labor scarcity and climate unpredictability. The industry's adaptation hinges on developing climate-smart solutions and integrated digital platforms to stabilize farm output.

We can help! Our analysts can customize this india agrochemicals market research report to meet your requirements.

RIA -

RIA -