AI In Luxury Brands Market Size 2025-2029

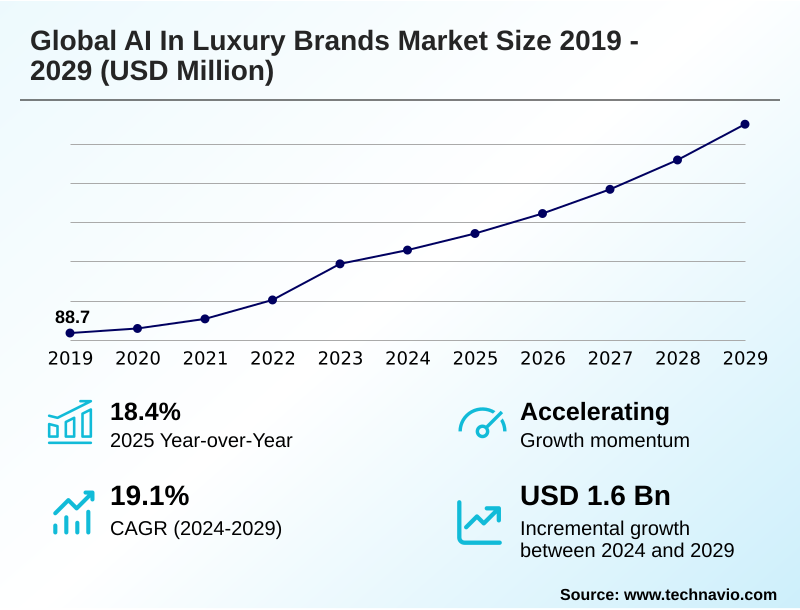

The ai in luxury brands market size is valued to increase by USD 1.60 billion, at a CAGR of 19.1% from 2024 to 2029. Enhanced personalization and customer experience will drive the ai in luxury brands market.

Major Market Trends & Insights

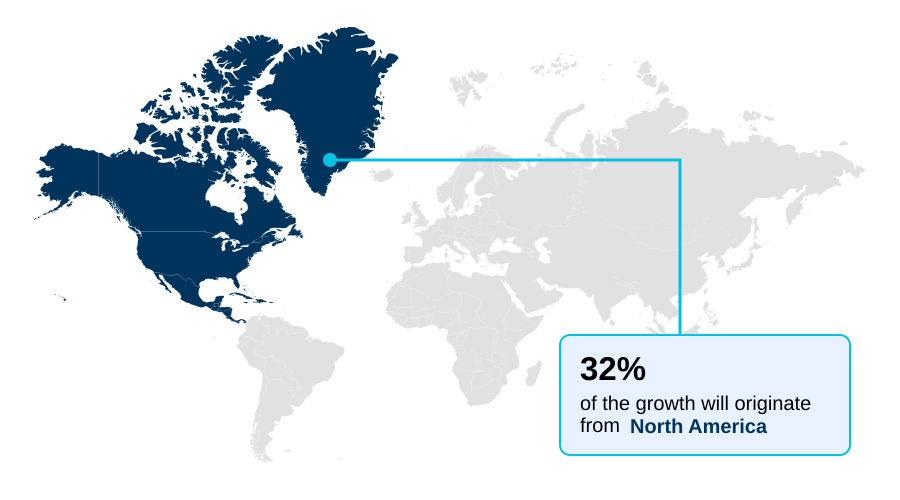

- North America dominated the market and accounted for a 32.2% growth during the forecast period.

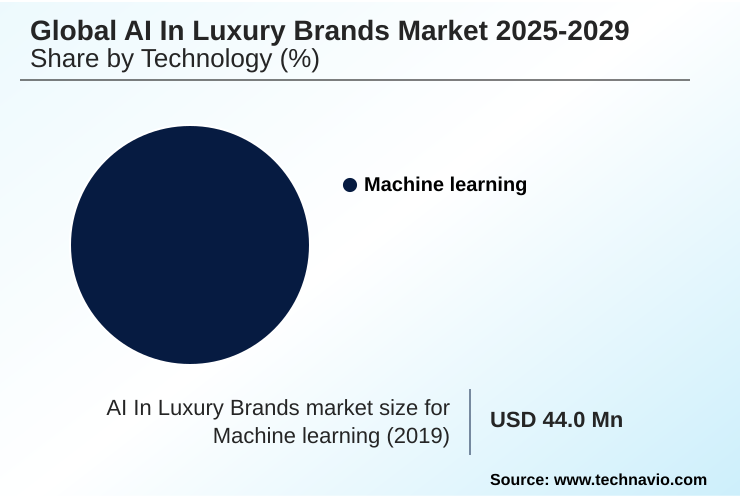

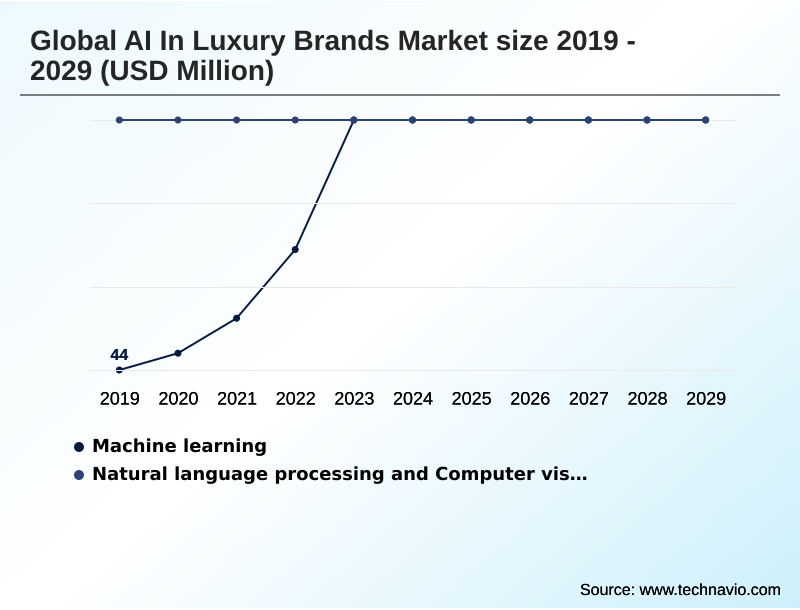

- By Technology - Machine learning segment was valued at USD 465.6 million in 2023

- By Application - Trend forecasting segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 2.66 billion

- Market Future Opportunities: USD 1.60 billion

- CAGR from 2024 to 2029 : 19.1%

Market Summary

- The AI in luxury brands market is undergoing a significant strategic expansion, moving beyond exploratory phases into deep operational integration. This evolution is driven by the necessity for hyper-personalization, a key expectation of the modern luxury consumer. By leveraging technologies to analyze vast datasets, brands now deliver bespoke recommendations and curated content with unprecedented accuracy.

- A key application is in optimizing the supply chain, where machine learning models enable more accurate demand forecasting. For instance, by analyzing trends from social media and sales data, firms can mitigate the risks of overproduction and excess inventory, a crucial step toward greater sustainability.

- This data-driven approach allows for more agile and responsive production cycles, ensuring products are available where and when they are most desired. However, this technological shift presents a challenge in maintaining the human touch and exclusivity that define luxury, requiring a strategic balance to ensure AI enhances, rather than supplants, the core brand identity.

What will be the Size of the AI In Luxury Brands Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the AI In Luxury Brands Market Segmented?

The ai in luxury brands industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Technology

- Machine learning

- Natural language processing

- Computer vision

- Application

- Trend forecasting

- Customer service chatbots

- Virtual try-on and fitting rooms

- Personalization and recommendation engines

- Others

- End-user

- Apparel

- Footwear

- Accessories

- Cosmetics

- Jewelry

- Geography

- North America

- US

- Canada

- Europe

- UK

- Germany

- France

- APAC

- China

- Japan

- South Korea

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- Rest of World (ROW)

- North America

By Technology Insights

The machine learning segment is estimated to witness significant growth during the forecast period.

The machine learning sub-segment is foundational to the AI in luxury brands market, fundamentally reshaping personalization and operational strategy. Machine learning algorithms are integral to hyper-personalization engines, enabling brands to move beyond generic interactions.

By using predictive analytics, firms can now deliver uniquely tailored digital content and AI-powered product recommendations, which significantly enhance the bespoke customer journey.

A recent survey revealed that 73% of fashion executives are prioritizing generative AI models, a subset of machine learning, for their business strategies.

This focus is driven by the demand for seamless, individualized digital experiences and the need for more efficient AI-based inventory management.

The technology also underpins AI-driven trend prediction, allowing for more agile and responsive product development cycles through smart store analytics and real-time data analysis.

The Machine learning segment was valued at USD 465.6 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 32.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How AI In Luxury Brands Market Demand is Rising in North America Get Free Sample

The geographic landscape for AI in luxury brands is led by North America, which accounts for approximately 32.2% of the market's incremental growth, driven by a tech-savvy consumer base and early adoption.

This is closely followed by the APAC region, contributing around 29.4% to growth, with markets like China and South Korea demonstrating rapid innovation in AI-powered retail.

The strategic importance of this technology is underscored by a 79% increase in AI spending by luxury brands in recent years.

This investment is directed toward AI-powered authentication and computer vision technology to enhance both the customer experience and operational efficiency.

Deployments of a virtual styling suite and AI-assisted design ideation are becoming more common as brands globally compete to offer the most advanced and personalized services through their digital and physical channels.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The successful deployment of AI in the luxury sector requires a nuanced understanding of how AI-driven personalization versus human touch impacts consumer perception. While machine learning for hyper-personalized recommendations is becoming a standard for enhancing online engagement, the core challenge remains the impact of AI on brand exclusivity.

- Strategically, firms are leveraging AI for predictive trend forecasting in fashion to align collections with emerging consumer desires, thereby minimizing financial risk. Simultaneously, the role of AI in luxury brand storytelling is expanding, with narrative-driven platforms creating deeper emotional connections. Behind the scenes, the ROI of AI implementation in luxury retail is most evident in operational advancements.

- This includes using AI to optimize luxury inventory levels and developing AI-powered tools for sustainable luxury sourcing. The technical hurdle of AI integration with legacy ERP systems is significant, yet overcoming it is crucial for creating resilient supply chains. Platforms now demonstrate over 99% accuracy in counterfeit detection, a substantial improvement that protects brand integrity.

- Furthermore, leveraging AI for phygital luxury experiences is proving essential for creating a cohesive omnichannel journey, where virtual try-on accuracy in luxury apparel directly influences purchasing decisions and reduces returns, blending digital convenience with the assurance of a perfect fit.

What are the key market drivers leading to the rise in the adoption of AI In Luxury Brands Industry?

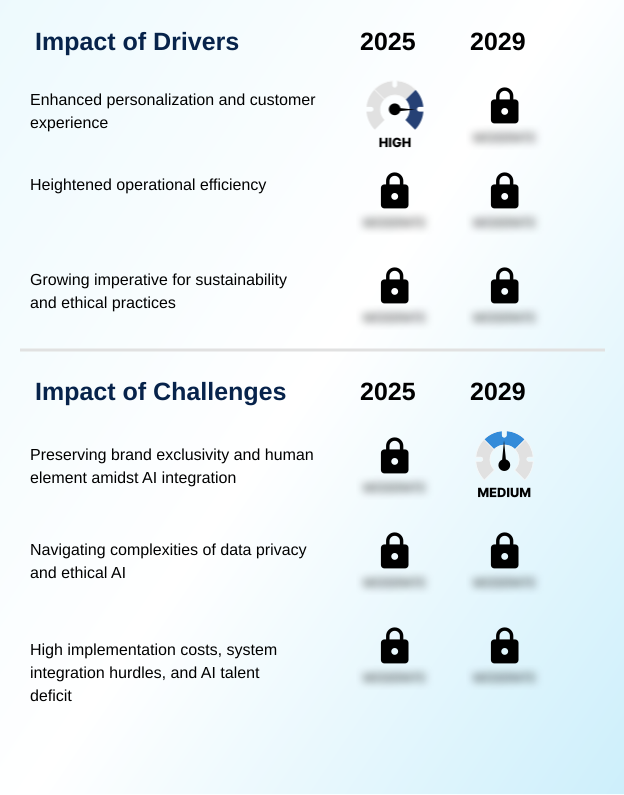

- The drive to provide enhanced personalization and a superior customer experience is a primary factor propelling market growth.

- Market growth is primarily fueled by the pursuit of enhanced personalization and heightened operational efficiency.

- The adoption of AI is driven by its ability to create a seamless connected visitor experience, with investment in AI technologies increasing by 79% over the past three years.

- This commitment is validated by consumer behavior, as nearly half of luxury shoppers indicate a willingness to spend more for AI-powered customization.

- Technologies such as AI skin analysis and AI-based inventory management enable brands to deliver tailored recommendations and optimize stock levels effectively.

- The push for operational excellence also involves leveraging AI-driven demand forecasting and robotic process automation (RPA) to streamline complex global supply chains, reduce waste, and improve profitability, making AI an indispensable tool for modern luxury operations.

What are the market trends shaping the AI In Luxury Brands Industry?

- The imperative for hyper-personalization is becoming a defining market trend. This is driving brands to deliver elevated and highly individualized customer experiences across all touchpoints.

- Key trends in the market are centered on elevating the customer journey and fortifying brand integrity through advanced technology. The imperative for a hyper-personalized bespoke customer journey is driving the adoption of AI-powered chatbots and virtual personal shopper tools, which are now capable of nuanced, brand-aligned interactions.

- In parallel, sustainable manufacturing optimization and AI-enhanced quality control are gaining traction, supported by technologies that improve supply chain transparency. A critical development is the use of computer vision for counterfeit authentication; AI-driven platforms report over 99% accuracy in identifying fakes by scrutinizing microscopic details.

- This trend is reinforced as proactive AI controls now block the vast majority of fraudulent listings before they are even seen, demonstrating a powerful defense of brand value. The use of a virtual makeup artist is also a growing trend in the beauty sector.

What challenges does the AI In Luxury Brands Industry face during its growth?

- A key challenge affecting industry growth is the need to preserve brand exclusivity and the human element while strategically integrating AI technologies.

- A paramount challenge facing the market is balancing technological integration with brand exclusivity, alongside the complexities of ethical AI governance and the high cost of implementation. The scarcity of specialized talent and difficulties in merging AI platforms with legacy systems create significant operational hurdles.

- Successfully navigating data privacy regulations is critical for maintaining consumer trust, necessitating the use of federated learning techniques and robust data security. Overcoming these obstacles is essential for increasing technology adoption, with some leading markets aiming to boost AI utilization rates from under 3% to over 30% in the retail sector.

- Strategic partnerships with tech startups are emerging as a key strategy to mitigate high initial investment costs and access specialized expertise in areas like AI-powered size recommendation and conversational commerce platforms.

Exclusive Technavio Analysis on Customer Landscape

The ai in luxury brands market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai in luxury brands market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of AI In Luxury Brands Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ai in luxury brands market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Balenciaga SA - Offerings include AI-generated digital experiences and predictive trend forecasting, designed to redefine consumer engagement and optimize product strategy in the luxury sector.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Balenciaga SA

- Burberry Group Plc

- Cartier SA

- Chanel Ltd.

- Christian Dior SE

- Compagnie Financiere Richemont SA

- Google LLC

- Guccio Gucci SpA

- IBM Corp.

- Kering SA

- LVMH Moet Hennessy

- Microsoft Corp.

- Moncler S.P.A.

- Oracle Corp.

- Perfect Corp.

- Revieve Inc.

- The Estee Lauder Companies

- The LVMH group

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ai in luxury brands market

- In December, 2024, Centric Software launched an AI-powered tool for fashion inspiration, demonstrating continuous innovation in the tech ecosystem that supports the luxury sector.

- In January, 2025, Hugo Boss integrated AI-generated product content, including a video, across its global e-commerce platforms as part of its digital strategy to enhance product storytelling.

- In February, 2025, Red Sea Global announced a partnership with Globant to create a Connected Visitor Experience at The Red Sea destination, utilizing AI and IoT for hyper-personalized services.

- In March, 2025, Amorepacific revealed it is building an AI Beauty Counselor app using Microsoft Azure AI to provide personalized advice and an online skin diagnosis tool for consumers.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled AI In Luxury Brands Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 19.1% |

| Market growth 2025-2029 | USD 1601.8 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 18.4% |

| Key countries | US, Canada, UK, Germany, France, Italy, China, Japan, South Korea, India, Brazil, Argentina, Saudi Arabia and UAE |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The AI in luxury brands market is defined by its strategic integration into core business functions, moving from peripheral applications to central operational roles. The deployment of natural language processing and computer vision technology is becoming standard for creating differentiated customer experiences.

- Firms are leveraging machine learning algorithms and predictive analytics to power everything from AI-driven demand forecasting to AI-powered product recommendations and supply chain optimization. This technological shift is also addressing critical industry vulnerabilities, with advanced counterfeit detection systems now blocking over 99% of suspected fraudulent listings before they can impact consumers.

- The rise of generative AI models facilitates everything from AI-driven visual merchandising to personalized marketing at scale. A key boardroom consideration is navigating ethical AI and data privacy regulations, which directly influences the architecture of hyper-personalization engines and AI-driven clienteling tools. Success hinges on using these technologies to augment, not replace, the core tenets of luxury service and craftsmanship.

What are the Key Data Covered in this AI In Luxury Brands Market Research and Growth Report?

-

What is the expected growth of the AI In Luxury Brands Market between 2025 and 2029?

-

USD 1.60 billion, at a CAGR of 19.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Technology (Machine learning, Natural language processing and Computer vision), Application (Trend forecasting, Customer service chatbots, Virtual try-on and fitting rooms, Personalization and recommendation engines and Others), End-user (Apparel, Footwear, Accessories, Cosmetics and Jewelry) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Enhanced personalization and customer experience, Preserving brand exclusivity and human element amidst AI integration

-

-

Who are the major players in the AI In Luxury Brands Market?

-

Balenciaga SA, Burberry Group Plc, Cartier SA, Chanel Ltd., Christian Dior SE, Compagnie Financiere Richemont SA, Google LLC, Guccio Gucci SpA, IBM Corp., Kering SA, LVMH Moet Hennessy, Microsoft Corp., Moncler S.P.A., Oracle Corp., Perfect Corp., Revieve Inc., The Estee Lauder Companies and The LVMH group

-

Market Research Insights

- The market is being reshaped by the strategic deployment of AI, with a focus on delivering a seamless omnichannel retail integration and immersive brand experience. The implementation of conversational commerce platforms and data anonymization protocols is becoming standard as brands seek to build trust while personalizing interactions.

- The effectiveness of these technologies is clear; AI-driven counterfeit detection systems now achieve over 99% accuracy in identifying fraudulent goods, directly protecting brand revenue and reputation. Moreover, the use of predictive customer segmentation and AI-driven content generation has led to significant operational gains, with some brands achieving a remarkable 38% reduction in customer acquisition costs.

- This fusion of digital intelligence with a phygital retail strategy is central to achieving a competitive edge.

We can help! Our analysts can customize this ai in luxury brands market research report to meet your requirements.

RIA -

RIA -