Ai Radiology Workflow Automation Software Market Size and Growth Forecast 2026-2030

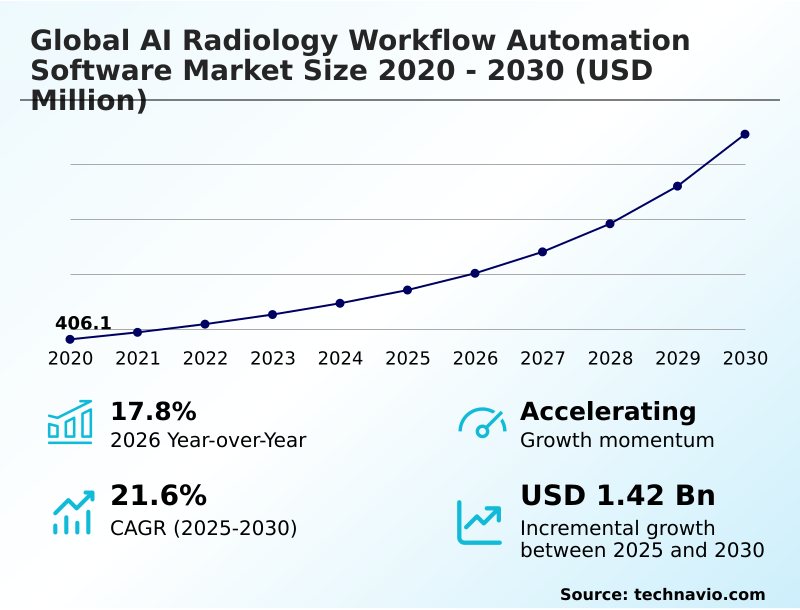

The Ai Radiology Workflow Automation Software Market size was valued at USD 854.4 million in 2025 growing at a CAGR of 21.6% during the forecast period 2026-2030.

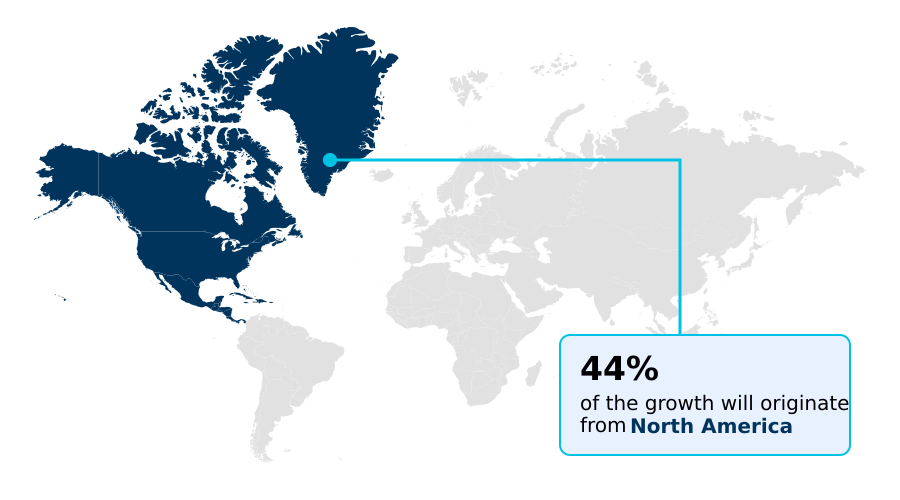

North America accounts for 44.4% of incremental growth during the forecast period. The Software segment by Component was valued at USD 434.6 million in 2024, while the WOO segment holds the largest revenue share by Application.

The market is projected to grow by USD 1.87 billion from 2020 to 2030, with USD 1.42 billion of the growth expected during the forecast period of 2025 to 2030.

Get Key Insights on Market Forecast (PDF) Request Free Sample

Ai Radiology Workflow Automation Software Market Overview

The AI radiology workflow automation software market is defined by the urgent need to manage immense diagnostic data volumes while enhancing clinical efficiency and patient outcomes. North America is set to contribute 44.4% of incremental growth, driven by advanced healthcare infrastructure and the strategic imperative to mitigate physician burnout. In a typical high-volume metropolitan hospital, the deployment of automated triage systems for emergency department CT scans reduces the average time-to-diagnosis for critical findings from hours to under 15 minutes, directly improving survival rates for conditions like stroke. This level of workflow optimization is achieved through sophisticated deep learning models and seamless PACS integration. Vendors are focusing on platforms that offer robust clinical decision support and ensure high diagnostic accuracy, addressing the core demands of modern healthcare providers. As health systems adopt value-based care models, the ability of these software tools to deliver measurable improvements in turnaround times and resource allocation becomes a critical factor in procurement decisions, shaping the competitive landscape.

Drivers, Trends, and Challenges in the Ai Radiology Workflow Automation Software Market

Strategic decision-making in the AI radiology workflow automation software market hinges on a clear understanding of the ROI of AI workflow automation in hospitals. This calculation involves weighing the benefits of AI for radiology workflow optimization against the significant interoperability challenges in radiology AI.

For instance, AI-driven triage for emergency radiology can slash diagnostic turnaround times, a critical factor in patient outcomes. However, facilities must choose between cloud vs on-premise AI radiology deployments, each with different implications for security, scalability, and adherence to regulations like HIPAA.

A key trend is the use of generative AI in radiology reporting, which can reduce report creation time by over 50% compared to traditional dictation methods, directly addressing the impact of AI on radiologist burnout. The regulatory pathways for medical AI software are becoming clearer but remain a complex hurdle.

Ultimately, the successful implementation of predictive analytics for radiology operations depends on a platform's ability to integrate seamlessly into existing clinical environments and deliver quantifiable improvements, justifying the investment beyond initial hype.

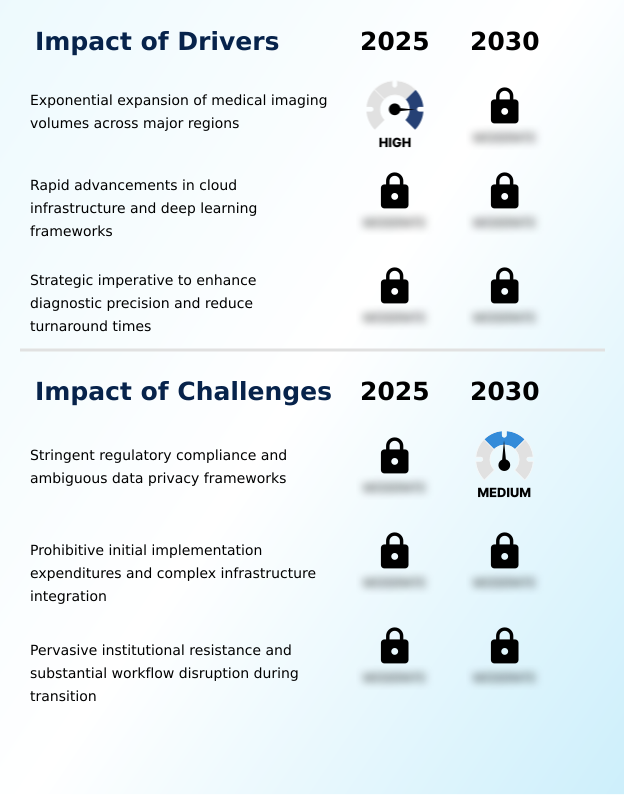

Primary Growth Driver: The exponential expansion of medical imaging volumes across major regions stands as a primary driver for market growth.

Market growth, accelerating at a 17.8% year-over-year rate, is propelled by the convergence of clinical necessity and technological maturity.

The primary driver is the exponential expansion of medical imaging volumes, which has rendered manual workflows unsustainable and heightened the need for workflow optimization to improve diagnostic accuracy.

This demand is met by the rapid advancements in cloud-native platform architecture and the sophistication of deep learning models, which now deliver near-human-level performance in image analysis.

This technological readiness provides a compelling incentive for healthcare institutions to invest in solutions that promise significant turnaround time reduction. The strategic imperative to enhance diagnostic precision and deliver value-based care solidifies the business case for adopting these automated systems.

Emerging Market Trend: The integration of generative AI for automated reporting represents a pivotal market trend. This technology is also being leveraged to enhance patient communication by translating complex medical terminology.

The market is evolving beyond simple anomaly detection toward holistic operational management, driven by key technological shifts. The integration of generative AI is automating the creation of structured reporting, significantly reducing the time radiologists spend on documentation. Concurrently, a focus on predictive analytics allows for optimized modality fleet management and resource allocation, forecasting demand surges to prevent bottlenecks.

There is also a pronounced shift toward company-neutral AI orchestration platforms and greater adherence to interoperability standards like FHIR. This enables healthcare systems to build modular, best-of-breed ecosystems, avoiding vendor lock-in and seamlessly deploying various triage algorithms. These trends collectively address the core challenges of efficiency and physician burnout in high-volume diagnostic settings.

Key Industry Challenge: Stringent regulatory compliance and ambiguous data privacy frameworks present a key challenge affecting industry growth.

Despite strong drivers, market adoption is constrained by significant operational and regulatory hurdles. Prohibitive initial implementation costs and the technical complexities of RIS integration into legacy hospital IT systems present a primary financial barrier.

On the regulatory front, navigating the stringent and often ambiguous data privacy frameworks of HIPAA and GDPR is a major challenge, particularly concerning data anonymization for training deep learning models. This is compounded by clinician hesitancy, as the 'black box' nature of some algorithms and the risk of algorithmic drift create trust issues.

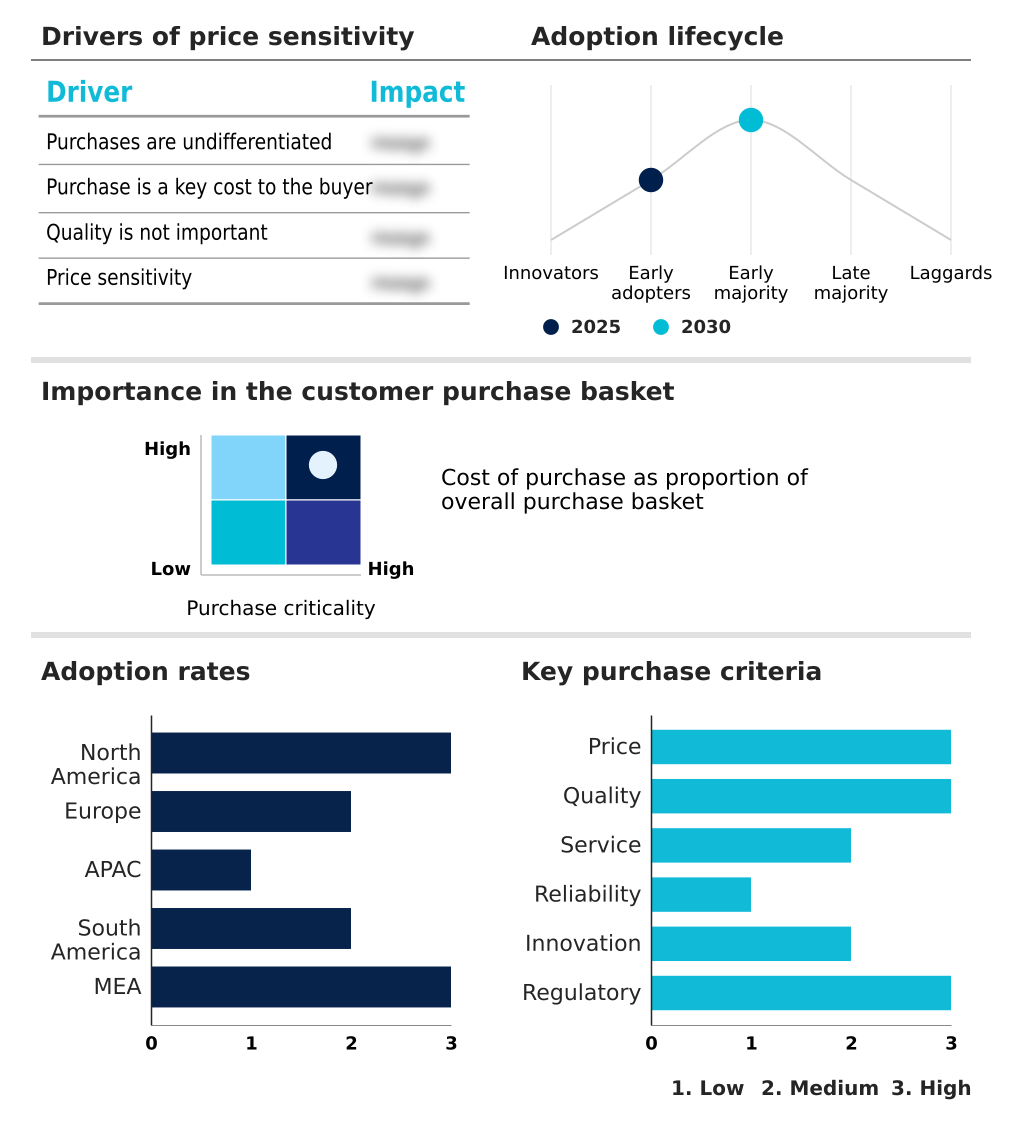

Overcoming this pervasive institutional resistance requires transparent, user-centric design and a clear demonstration of how these tools will augment, not replace, clinical expertise, a critical factor given the 'High' price sensitivity noted among buyers.

Explore Full Market Dynamics Analysis Request Free Sample

Ai Radiology Workflow Automation Software Market Segmentation

The ai radiology workflow automation software industry research report provides comprehensive data including region-wise segment analysis, with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

Component Segment Analysis

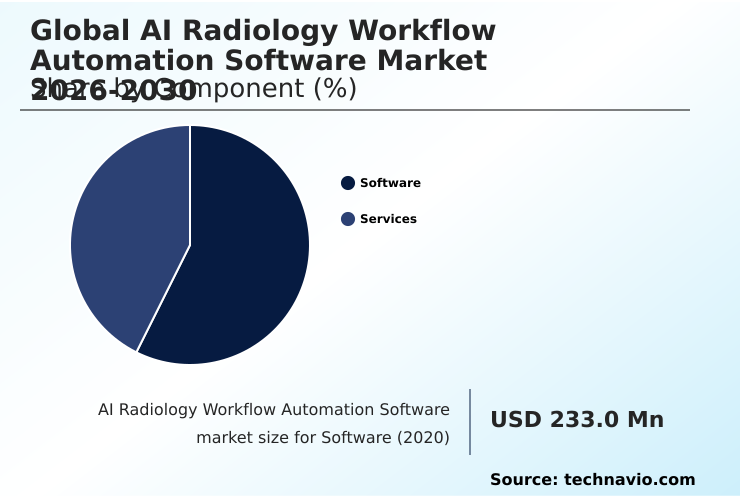

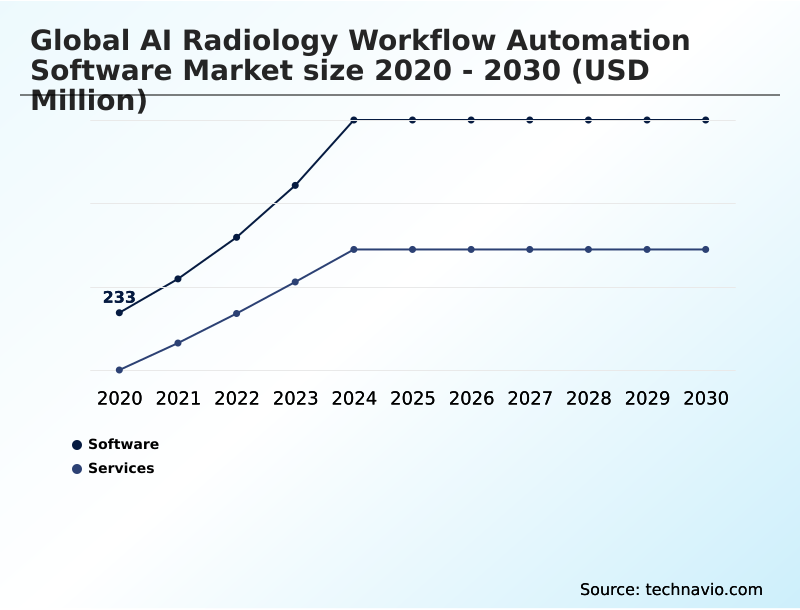

The software segment is estimated to witness significant growth during the forecast period.

The software segment is the foundational core of the AI radiology workflow automation software market, with a forecast value of 522.0 million in 2025.

These advanced solutions are engineered for deep PACS integration, utilizing deep learning models to enable automated triage and enhance diagnostic accuracy. Medical facilities are moving beyond basic RIS integration to adopt comprehensive platforms that offer sophisticated AI orchestration capabilities.

These systems leverage computer vision and neural networks to perform complex image segmentation, which is crucial for precise clinical decision support.

The primary objective is workflow optimization, which addresses physician burnout by automating routine tasks, allowing specialists to focus on complex interpretations and improving overall patient outcomes through faster, more reliable diagnostics.

The Software segment was valued at USD 434.6 million in 2024 and showed a gradual increase during the forecast period.

Ai Radiology Workflow Automation Software Market by Region: North America Leads with 44.4% Growth Share

North America is estimated to contribute 44.4% to the growth of the global market during the forecast period.

The geographic landscape of the AI radiology workflow automation software market is defined by varied adoption rates and regulatory environments.

North America, contributing 44.4% of incremental growth, leads due to its mature healthcare IT infrastructure and the pressing need to enhance diagnostic efficiency under frameworks like HIPAA.

In Europe, which is governed by the GDPR and the Medical Device Regulation (MDR), there is a strong emphasis on data anonymization and federated learning models to ensure regulatory compliance.

The APAC region is the fastest-growing, with a 23.4% CAGR, as nations like China and India invest heavily in digital health to manage vast patient populations and overcome shortages of specialized personnel.

Across all regions, the expansion of teleradiology networks is a common driver, increasing demand for cloud-native platforms that can support remote diagnostics and automated case prioritization.

Customer Landscape Analysis for the Ai Radiology Workflow Automation Software Market

The ai radiology workflow automation software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ai radiology workflow automation software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Competitive Landscape of the Ai Radiology Workflow Automation Software Market

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the ai radiology workflow automation software market industry.

Aidoc Medical Ltd. - The AI-powered care coordination platform automates the detection and triage of time-critical conditions such as strokes and pulmonary embolisms, enhancing enterprise radiology workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aidoc Medical Ltd.

- Blackford Analysis

- Carestream Health Inc.

- DeepHealth

- FUJIFILM Holdings Corp.

- GE HealthCare Technologies

- GLEAMER

- Koninklijke Philips NV

- Lunit Inc.

- Microsoft Corp.

- Optum Inc.

- Qure.ai Technologies Pvt. Ltd.

- Rad AI

- RapidAI

- Sectra AB

- Siemens Healthineers AG

- Subtle Medical Inc.

- TeraRecon Inc.

- Visage Imaging

- Viz.ai Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Developments in the Ai Radiology Workflow Automation Software Market

- In February 2025, DeepHealth announced the launch of a new suite of AI-powered radiology informatics and population screening solutions, including a cloud-native platform designed to unify imaging workflows, at the European Congress of Radiology 2025.

- In November 2024, GE HealthCare entered into a definitive agreement to acquire Intelerad, a prominent provider of medical imaging and workflow software solutions, for approximately $2.3 billion to expand its enterprise imaging portfolio.

- In October 2024, MedVision AI announced the acquisition of Radiometrics Cloud, a company specializing in real-time imaging analytics and workflow orchestration technologies, to enhance its AI platform's capabilities.

- In September 2024, Siemens Healthineers entered into a strategic collaboration with Apollo Hospitals in India to co-develop and deploy AI-driven imaging workflows focused on early liver disease detection and management.

Research Analyst Overview: Ai Radiology Workflow Automation Software Market

The market is moving decisively toward integrated platforms, compelling a strategic re-evaluation of procurement away from siloed algorithmic tools. Boardroom decisions now center on the total cost of ownership of either committing to a single-vendor ecosystem, such as the Edison platform, or managing a multi-vendor environment through an AI orchestration layer like the Sectra Amplifier.

This choice has profound implications for long-term scalability and mitigating risks like algorithmic drift. With the software segment commanding a dominant market share, the focus is on systems offering robust PACS integration and adherence to the DICOM standard.

Compliance with frameworks like the EU's Medical Device Regulation (MDR) is non-negotiable, influencing the design of triage algorithms and the architecture of neural networks. The value proposition is no longer just image analysis but comprehensive clinical decision support, leveraging technologies from computer vision for image segmentation to the aiOS platform for enterprise-wide workflow management.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ai Radiology Workflow Automation Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 297 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.6% |

| Market growth 2026-2030 | USD 1416.8 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 17.8% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Ai Radiology Workflow Automation Software Market: Key Questions Answered in This Report

-

What is the expected growth of the Ai Radiology Workflow Automation Software Market between 2026 and 2030?

-

The Ai Radiology Workflow Automation Software Market is expected to grow by USD 1.42 billion during 2026-2030, registering a CAGR of 21.6%. Year-over-year growth in 2026 is estimated at 17.8%%. This acceleration is shaped by exponential expansion of medical imaging volumes across major regions, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Application (WOO, Triage and prioritization, Reporting and documentation, and Others), Deployment (Cloud, and On premises) and Geography (North America, Europe, APAC, South America, Middle East and Africa). Among these, the Software segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers North America, Europe, APAC, South America and Middle East and Africa. North America is estimated to contribute 44.4% to market growth during the forecast period. Country-level analysis includes US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is exponential expansion of medical imaging volumes across major regions, which is accelerating investment and industry demand. The main challenge is stringent regulatory compliance and ambiguous data privacy frameworks, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Ai Radiology Workflow Automation Software Market?

-

Key vendors include Aidoc Medical Ltd., Blackford Analysis, Carestream Health Inc., DeepHealth, FUJIFILM Holdings Corp., GE HealthCare Technologies, GLEAMER, Koninklijke Philips NV, Lunit Inc., Microsoft Corp., Optum Inc., Qure.ai Technologies Pvt. Ltd., Rad AI, RapidAI, Sectra AB, Siemens Healthineers AG, Subtle Medical Inc., TeraRecon Inc., Visage Imaging and Viz.ai Inc.. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Ai Radiology Workflow Automation Software Market Research Insights

Market dynamics are heavily influenced by regulatory pathways and economic models driving healthcare. The rigorous FDA clearance process shapes vendor development cycles, while the broader shift toward value-based care compels providers to adopt solutions that demonstrably improve diagnostic accuracy and facilitate better resource allocation. This focus is critical for addressing physician burnout, a key operational concern.

Seamless EHR integration and RIS integration are no longer optional but are fundamental requirements for any new platform deployment. This pressure ensures that software solutions deliver tangible efficiencies in turnaround time reduction and workflow optimization, ultimately justifying the investment in a climate of high price sensitivity and complex procurement evaluations.

We can help! Our analysts can customize this ai radiology workflow automation software market research report to meet your requirements.

RIA -

RIA -