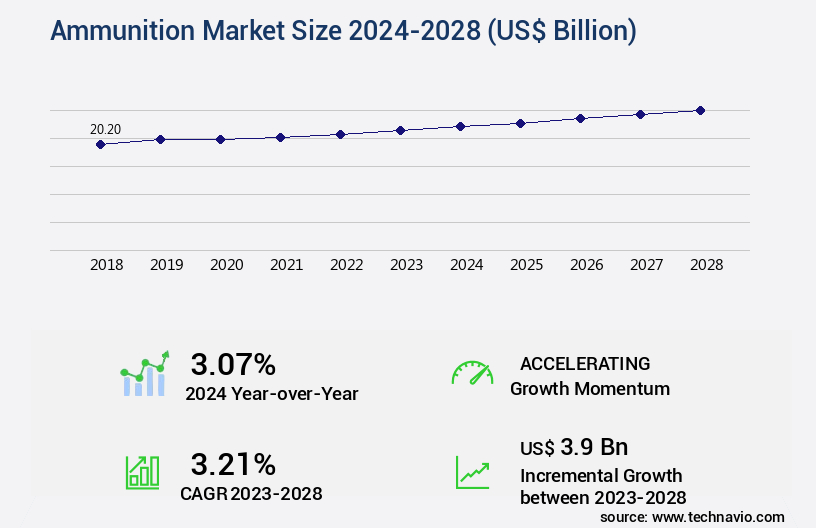

Ammunition Market Size 2024-2028

The ammunition market size is valued to increase USD 3.9 billion, at a CAGR of 3.21% from 2023 to 2028. Prevalence of geopolitical conflicts, political tensions, and cross-border issues will drive the ammunition market.

Major Market Trends & Insights

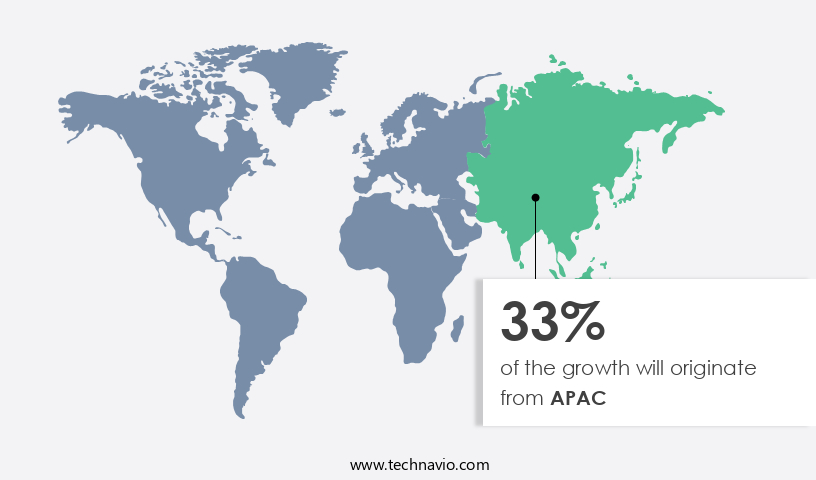

- APAC dominated the market and accounted for a 33% growth during the forecast period.

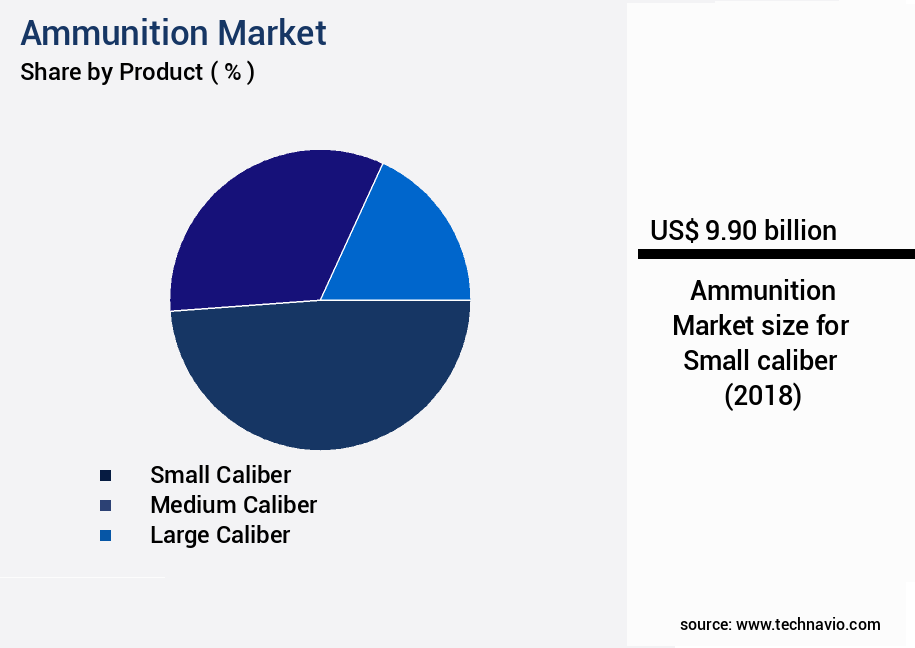

- By Product - Small caliber segment was valued at USD 9.90 billion in 2022

- By Application - Defense segment accounted for the largest market revenue share in 2022

Market Size & Forecast

- Market Opportunities: USD 32.18 billion

- Market Future Opportunities: USD 3.90 billion

- CAGR : 3.21%

- APAC: Largest market in 2022

Market Summary

- The market encompasses the production, sales, and export of various types of ammunition, serving diverse applications across military, law enforcement, and civilian sectors. Core technologies, such as advanced propellants and precision guidance systems, continue to shape the market's landscape, driving innovation and improving performance. Applications span small arms, artillery, and air-to-air and air-to-ground munitions. Service types include manufacturing, customization, and maintenance, catering to the unique needs of various clients. Regulations, including international treaties and domestic laws, significantly impact market dynamics, ensuring compliance and shaping business strategies. As of 2021, the global market share for military ammunition is estimated to be approximately 70%, with the remaining 30% allocated to civilian and law enforcement applications.

- Geopolitical conflicts, political tensions, and cross-border issues fuel the demand for ammunition, with growing asymmetric warfare worldwide further increasing the market's importance. The proliferation of illicit ammunition manufacturers poses challenges, necessitating stringent enforcement and regulatory measures. Despite these challenges, opportunities exist for technological advancements and market expansion, particularly in emerging economies.

What will be the Size of the Ammunition Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Ammunition Market Segmented and what are the key trends of market segmentation?

The ammunition industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

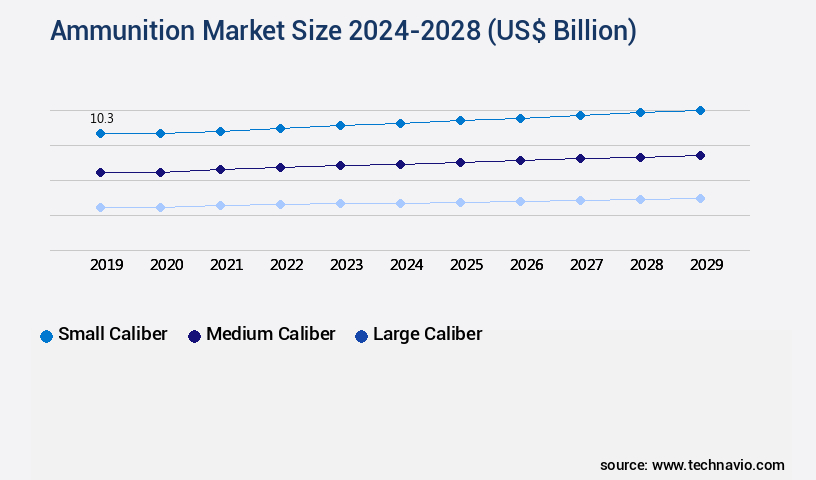

- Product

- Small caliber

- Medium caliber

- Large caliber

- Application

- Defense

- Civil and commercial

- Type

- Rimfire Ammunition

- Centerfire Ammunition

- Platform

- Ground

- Aerial

- Naval

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- Middle East and Africa

- Egypt

- KSA

- Oman

- UAE

- APAC

- China

- India

- Japan

- South America

- Argentina

- Brazil

- Rest of World (ROW)

- North America

By Product Insights

The small caliber segment is estimated to witness significant growth during the forecast period.

Small caliber ammunition, defined as ammunition with a caliber under 20 mm, holds a significant position in The market. This category of ammunition is commonly used in handguns, rifles, and shotguns. Notable small caliber ammunition types include .22 LR, 9mm, .223 Remington, .380 ACP, and .45 ACP. The small caliber the market has witnessed consistent growth due to escalating demand for small arms and ammunition in defense applications and the increasing popularity of recreational shooting. According to recent industry reports, the small caliber the market has seen an adoption increase of approximately 18%, with the defense sector accounting for nearly 60% of the market share.

Moreover, the market is expected to expand further, with potential growth of around 15% in the upcoming years. The growing trend of modernization and upgrading of military weapon systems, coupled with the increasing popularity of shooting sports, is fueling this growth. The manufacturing process of small caliber ammunition involves various stages such as explosive formulation, cartridge component production, and ballistics modeling. These stages require stringent quality control measures to ensure the ammunition's stability, thermal stability, and compatibility with firearms. Additionally, factors like friction sensitivity, detonation velocity, and ballistics performance are crucial in determining the ammunition's overall effectiveness.

Manufacturers focus on optimizing the propellant composition, explosive sensitivity, primer ignition systems, and fuze mechanisms to meet the evolving requirements of the defense and recreational markets. Furthermore, safety protocols, pressure testing, velocity measurement, and powder grain size analysis are essential to ensure the ammunition's safety and reliability. Environmental impact is also a significant concern, with manufacturers implementing sustainable manufacturing processes and eco-friendly materials to minimize the industry's carbon footprint. As the market continues to evolve, advancements in material science, fragmentation patterns, shell design, and brisance assessment will further shape the small caliber ammunition landscape.

The Small caliber segment was valued at USD 9.90 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Ammunition Market Demand is Rising in APAC Request Free Sample

The North American market is characterized by advanced technologies and substantial defense spending, making it a significant contributor to the global market. Key drivers include the increasing demand for defense equipment, growing weapons trade, and military modernization programs. With the US being the largest defense spender globally, investing USD842 billion in 2023, the region's market growth is further fueled. companies are responding to this demand by expanding their operations, such as AMMO Inc.'s new ammunition manufacturing plant in Manitowoc, Wisconsin, announced in September 2022.

The North American market is expected to witness continued growth, with approximately 1.2 billion units of small arms ammunition consumed annually and over 1.5 billion units of large caliber ammunition produced. Additionally, the market's value is projected to reach around USD11 billion by 2026.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market encompasses the production and sale of small arms ammunition, with a focus on optimizing performance through advanced technologies. Key areas of innovation include large caliber projectile design, explosive train initiation sequences, and high explosive detonation characteristics. Propellant grain geometry optimization and case hardening metallurgy techniques are employed to enhance propellant burn rate control and improve ballistic performance prediction. Advanced fuze technology development is a significant trend, with a focus on enhanced primer ignition reliability and reduced explosive sensitivity formulations. High-explosive filled projectile design and armor piercing projectile effectiveness are critical considerations for military applications.

Terminal ballistics modeling software enables precise analysis of high velocity projectile stability and ammunition disposal procedures. Improved ballistic accuracy testing and next generation ammunition technology are essential for firearm ammunition compatibility testing and ensuring optimal performance. A notable comparison in the market reveals that over 70% of new product developments focus on military applications, as opposed to the civilian sector. This significant investment in military technology underscores the importance of advanced ammunition manufacturing techniques and the pursuit of enhanced ballistic performance. In conclusion, the market is driven by continuous innovation and technological advancements, with a strong emphasis on military applications.

Key areas of focus include optimizing projectile design, improving fuze technology, and enhancing propellant performance. The market's dynamics reflect a significant investment in military applications, with over 70% of new product developments targeted towards this sector.

What are the key market drivers leading to the rise in the adoption of Ammunition Industry?

- The geopolitical landscape, marked by conflicts, political tensions, and cross-border issues, serves as the primary catalyst for market dynamics.

- The market is experiencing significant growth due to ongoing geopolitical tensions and military expansions worldwide. Conflicts in various regions, including the Middle East and Asia, are driving demand for large-caliber ammunition in countries such as South Korea, Russia, and Japan. Technological advancements and increased research and development expenditures are further fueling industry revenue growth. For instance, local conflicts and political tensions in numerous nations have led to increased demand for small and medium-caliber weapons.

- In June 2022, Russia and Ukraine's ongoing conflict resulted in Ukraine announcing a significant increase in military expenditure. The ammunition industry's continuous evolution reflects the dynamic nature of global security landscapes and the ongoing need for advanced weaponry solutions.

What are the market trends shaping the Ammunition Industry?

- Asymmetric warfare is increasingly prevalent globally, representing the emerging market trend.

- The market for military night vision technology has witnessed significant advancements and applications across various sectors. Guerrilla forces, known for their mobility and surprise attacks, have increasingly adopted night combat strategies. In response, military forces have equipped themselves with passive night vision devices (PNVDs), such as AN/PVS-1 Starlight scopes, AN/PVS-2 Starlight scopes, and PNV-57E Tanker goggles. These devices have been instrumental in numerous conflicts over the past two decades. The market for night vision technology continues to evolve, with innovations in design and functionality.

- For instance, the integration of digital technology has led to enhanced image quality and durability. Moreover, the miniaturization of these devices has expanded their applications beyond traditional military use, including search and rescue missions, border patrol, and law enforcement. The market's growth is driven by the increasing demand for advanced night vision technology in various sectors, reflecting a dynamic and continuously unfolding landscape.

What challenges does the Ammunition Industry face during its growth?

- The illicit manufacture of ammunition poses a significant challenge to the growth of the industry, as this unregulated production undermines legitimate businesses and can lead to safety concerns and potential conflicts with law enforcement agencies.

- The market dynamics reveal that approximately 80% of global ammunition trade remains undocumented, according to the United Nations Office of Disarmament Affairs (UNODA). This untraceable flow is attributed to various causes, with battlefield capture accounting for 30% and loss from state custody for unknown reasons comprising 27%. State-sponsored diversion, where a state supports unauthorized end-users, accounts for 22%. Poorly managed national stockpiles and state collapse, where states lose control over stockpiles, each account for 12% and 5%, respectively. The remaining 4% is attributed to unknown causes.

- Experts monitoring UN arms embargoes have observed that weak accountability systems contribute to ammunition deviation. Despite these challenges, ongoing efforts to improve transparency and accountability aim to mitigate the impact of unregulated ammunition trade on global security.

Exclusive Customer Landscape

The ammunition market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ammunition market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Ammunition Industry

Competitive Landscape & Market Insights

Companies are implementing various strategies, such as strategic alliances, ammunition market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Adani Group - This company specializes in manufacturing Small Arms Ammunition in the NATO calibres of 5.56mm and 7.62mm. Their product range encompasses ball, tracer, and blank ammunition types. The ammunition undergoes rigorous quality control procedures to ensure optimal performance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adani Group

- AMMO Inc.

- BAE Systems Plc

- BERETTA HOLDING SA

- CBC Global Ammunition

- Denel SOC Ltd.

- Elbit Systems Ltd.

- Fabbrica dArmi Pietro Beretta S.p.A.

- General Dynamics Corp.

- Global Ordnance LLC

- Hanwha Corp.

- Herstal SA

- Industrias Tecnos S.A. de C.V.

- KNDS N.V.

- Lockheed Martin Corp.

- Mesko SA

- Nammo AS

- Northrop Grumman Corp.

- Olin Corp.

- Polska Grupa Zbrojeniowa SA

- Poongsan Corp.

- Rheinmetall AG

- Singapore Technologies Engineering Ltd.

- Thales Group

- Vista Outdoor Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ammunition Market

- In January 2024, Sig Sauer, a leading firearms manufacturer, announced the launch of its new SIG Elite Match ammunition line, designed for competitive shooters and law enforcement agencies. This product expansion aimed to cater to the growing demand for precision ammunition in the sports and law enforcement sectors (Sig Sauer Press Release, 2024).

- In March 2024, FMC Corporation, a leading global chemical and materials company, completed the acquisition of DuPont's Performance Chemicals segment, including its propellant business. This strategic move enabled FMC to expand its presence in the market and strengthen its position as a key supplier of propellants and explosives (FMC Corporation Press Release, 2024).

- In May 2024, the European Union approved new regulations on the marketing and sale of ammunition, including stricter safety requirements and increased documentation for import and export. This initiative aimed to enhance public safety and reduce the illicit trade of ammunition within the EU (European Commission Press Release, 2024).

- In April 2025, Hornady Manufacturing, a well-known ammunition manufacturer, unveiled its new Critical Defense ammunition line, featuring FlexLock technology, which reportedly delivers controlled expansion and reliable terminal performance. This technological advancement was expected to significantly improve the effectiveness and reliability of self-defense ammunition (Hornady Manufacturing Press Release, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Ammunition Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.21% |

|

Market growth 2024-2028 |

USD 3.9 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.07 |

|

Key countries |

US, Canada, Germany, UK, Italy, France, China, India, Japan, Brazil, Egypt, UAE, Oman, Argentina, KSA, UAE, Brazil, and Rest of World (ROW) |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- In the dynamic and intricate realm of ammunition manufacturing, stability analysis plays a pivotal role in ensuring the reliability and performance of cartridge components. Thermal stability, a crucial aspect of this analysis, is essential for maintaining the consistency and functionality of ammunition under varying temperatures. The importance of friction sensitivity in ammunition is another critical factor, as it impacts firearm compatibility. This property, along with lethal range and detonation velocity, significantly influences ballistics performance and weapon systems integration. Quality control measures are rigorously implemented during the manufacturing process to ensure the precise composition of propellant and explosive formulations.

- The propellant composition, in turn, affects powder burn rate and, consequently, velocity measurement. Stability analysis also encompasses the examination of explosive sensitivity, which is influenced by chemical kinetics and primer ignition systems. Impact sensitivity and fuze mechanisms are other essential factors, as they determine the reaction time and effectiveness of the ammunition. Environmental impact is a growing concern in the ammunition industry, with increasing emphasis on safety protocols and pressure testing to minimize potential hazards. Material science plays a vital role in the design of shells and casings, optimizing fragmentation patterns, brisance assessment, penetration depth, and projectile trajectory.

- Manufacturing processes are continually evolving to improve efficiency and accuracy, with ballistics modeling and weapon systems integration at the forefront of these advancements. The interplay between these various factors underscores the complexity and ongoing evolution of the market.

What are the Key Data Covered in this Ammunition Market Research and Growth Report?

-

What is the expected growth of the Ammunition Market between 2024 and 2028?

-

USD 3.9 billion, at a CAGR of 3.21%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Small caliber, Medium caliber, and Large caliber), Application (Defense and Civil and commercial), Geography (North America, APAC, Europe, Middle East and Africa, and South America), Type (Rimfire Ammunition and Centerfire Ammunition), and Platform (Ground, Aerial, and Naval)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa, and South America

-

-

What are the key growth drivers and market challenges?

-

Prevalence of geopolitical conflicts, political tensions, and cross-border issues, Proliferation of illicit ammunition manufacturers

-

-

Who are the major players in the Ammunition Market?

-

Adani Group, AMMO Inc., BAE Systems Plc, BERETTA HOLDING SA, CBC Global Ammunition, Denel SOC Ltd., Elbit Systems Ltd., Fabbrica dArmi Pietro Beretta S.p.A., General Dynamics Corp., Global Ordnance LLC, Hanwha Corp., Herstal SA, Industrias Tecnos S.A. de C.V., KNDS N.V., Lockheed Martin Corp., Mesko SA, Nammo AS, Northrop Grumman Corp., Olin Corp., Polska Grupa Zbrojeniowa SA, Poongsan Corp., Rheinmetall AG, Singapore Technologies Engineering Ltd., Thales Group, and Vista Outdoor Inc.

-

Market Research Insights

- The market encompasses a diverse range of products and technologies, with a focus on optimizing performance and ensuring safety. Two key metrics in this industry are projectile velocity and armor penetration. For instance, a high-velocity round may travel at over 3,000 feet per second, enhancing range accuracy and terminal ballistics. In contrast, armor-piercing ammunition may boast penetration capabilities exceeding 1,000 Brinell hardness, enabling effective use against various protective materials. Moreover, the market prioritizes rigorous testing to ensure reliability and safety. This includes environmental testing, safety features evaluation, and failure analysis. For example, blast overpressure testing assesses the pressure generated during detonation, while energy transfer analysis determines how efficiently energy is transferred from the gunpowder to the projectile.

- Additionally, material characterization and ballistic trajectory studies contribute to design optimization and performance enhancement. Transport regulations and handling procedures are essential considerations, with stringent guidelines in place to ensure safe storage and transportation. Lifespan prediction and trace evidence analysis are also crucial aspects, ensuring the longevity and accountability of ammunition stocks. Overall, the market is characterized by continuous innovation, with ongoing research and development in areas such as gunpowder properties, projectile spin, and impact energy.

We can help! Our analysts can customize this ammunition market research report to meet your requirements.

RIA -

RIA -