Aniline Market Size 2024-2028

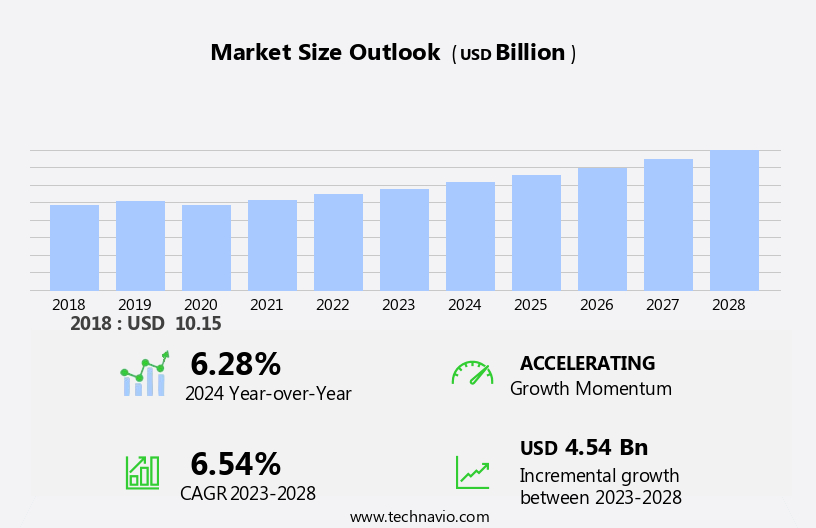

The aniline market size is forecast to increase by USD 4.54 billion at a CAGR of 6.54% between 2023 and 2028.

- The market is experiencing significant growth due to the increasing utilization of the polyurethane industry. This sector's expansion is driving market demand, as aniline is a crucial component in producing polyurethane foam and coatings. Another trend influencing the market is the shift towards bio-aniline, which is gaining popularity due to its eco-friendly nature and lower environmental impact. However, the market faces challenges from the volatility in prices of raw materials, such as benzene and phenol, which can significantly impact the cost structure of aniline production. Producers must navigate these price fluctuations to maintain profitability and meet customer demands. The market experiences strong growth due to its extensive applications. The market's growth is influenced by several factors, including the increasing demand for eco-friendly insulation materials, the expanding automotive industry, and the growing popularity of elastomers in various applications.

What will be the Size of the Market During the Forecast Period?

- The market dynamics surrounding aniline and its derivatives. Aniline, with the chemical formula C6H5NH2, is characterized by a benzene ring bearing an amino group. This versatile compound plays a pivotal role in numerous industries, including the production of dyes, rubber processing chemicals, and synthetic leather. In the realm of dyes and pigments, aniline derivatives are employed to produce a wide range of colors, catering to diverse industries such as textiles, plastics, and coatings.

- Furthermore, aniline's role in rubber chemical manufacturing is indispensable, contributing significantly to the rubber industry's growth. Synthetic aniline is primarily produced through the coal-tar derivatives process. The vapor-phase process, developed under METI (Ministry of Economy, Trade, and Industry), utilizes n-methyl compounds to improve efficiency in various industry verticals, including construction, where it supports initiatives like the Housing for All program to provide sustainable housing solutions. However, the market is witnessing a shift towards bio-based aniline, derived from renewable resources, as environmental concerns gain prominence. This eco-friendly alternative aligns with the global trend towards sustainable manufacturing processes. The demand for aniline in the production of rigid polyurethanes is substantial. These materials are extensively used in insulation, construction, and automotive applications. The automotive sector's growing demand for lightweight and fuel-efficient vehicles is expected to fuel the market's growth in the coming years.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- MDI

- Rubber processing chemicals and others

- Technology

- Vapor-phase process

- Liquid-phase process

- Geography

- APAC

- China

- Japan

- Europe

- Germany

- France

- North America

- US

- Middle East and Africa

- South America

- APAC

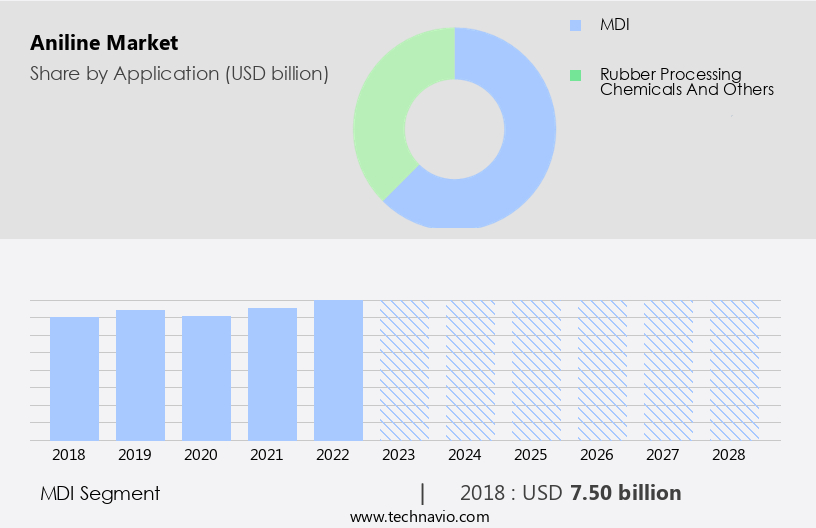

By Application Insights

- The MDI segment is estimated to witness significant growth during the forecast period.

Aniline is a significant chemical compound that serves as a precursor to MDI, or methylene diphenyl diisocyanate, which holds a substantial role in The market. Aniline's versatility is showcased through the various industries it caters to, with MDI being a crucial ingredient in the production of polyurethane foams. These foams are extensively utilized in the construction sector for insulation purposes in industrial, commercial, and residential buildings. The demand for energy-efficient and sustainable insulation solutions is driving the growth of the MDI market, accounting for a considerable market share in the global aniline industry. MDI's adaptability extends beyond the construction sector, as it is also employed in various other industries, such as automotive, textiles, and footwear.

Furthermore, the rubber chemical industry is another significant vertical that relies on MDI for the production of various elastomers and additives. Furthermore, aniline's derivatives, including salts and sulfur compounds, are essential components in the production of dyes and pigments. As a result, the market is expected to witness steady growth in the coming years.

Get a glance at the market report of share of various segments Request Free Sample

The MDI segment was valued at USD 7.50 billion in 2018 and showed a gradual increase during the forecast period.

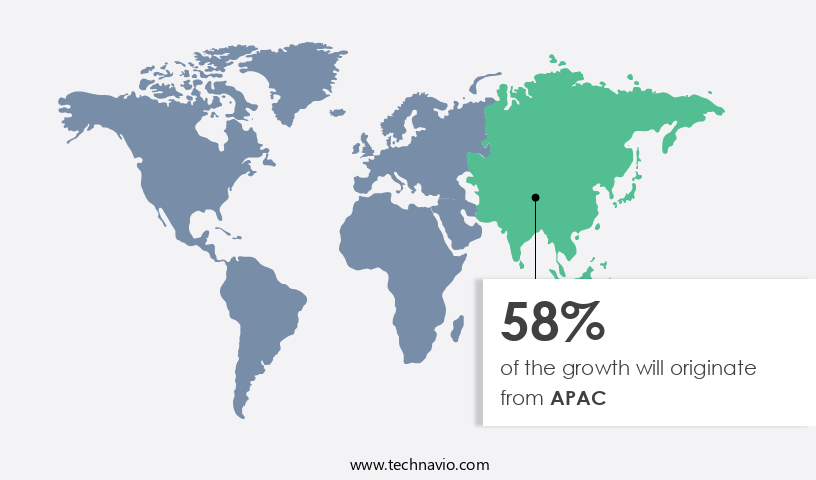

Regional Analysis

- APAC is estimated to contribute 58% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in the Asia-Pacific region (APAC) holds a significant position globally, driven by the region's strong industrialization and economic growth. The demand for Aniline is primarily driven by its extensive usage in the production of Synthetic Rubber. The chemical compound, with the formula C6H5NH2, consists of a Benzene ring and an Amino group. Aniline is a crucial ingredient in the manufacture of Polyurethane, a versatile polymer employed in various industries, including automotive, construction, and furniture. APAC's industrial expansion, particularly in countries like China and India, has led to a rise in demand for Aniline. The region's burgeoning manufacturing industries, which produce goods for both domestic and international markets, have increased the demand for Aniline. Furthermore, the expanding consumer base in APAC has fueled demand for Aniline in sectors such as pharmaceuticals and dyes.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of the Aniline Market?

Rising use in the polyurethane industry is the key driver of the market.

- Aniline, a crucial chemical compound with the chemical formula C6H5NH2, plays a significant role in the production of various industries' essential products. It is an amino derivative of benzene, featuring an aromatic benzene ring and an amino group. Aniline is a vital ingredient in the synthesis of MDI and TDI, key components for manufacturing synthetic rubber, such as polyurethane. This versatile polymer is extensively used in industries like automotive, construction, and plastics. In the automotive sector, aniline is employed in the production of vibrant colors for dyes and pigments. Moreover, it is used in the manufacturing of various medical devices, such as tubes, masks, and bags, due to its biocompatibility.

- The aniline market has experienced growth due to the increasing demand for polyurethane-based products. This trend is particularly prominent in the automotive industry, where aniline is used to produce lightweight components for car interiors and electric vehicles, contributing to improved fuel economy and reduced emissions. Furthermore, aniline is used in the production of insulating materials, sealants, and polyurethane foams, which are essential in construction and infrastructure. In the technology sector, aniline is used in the vapor-phase and liquid-phase processes for producing synthetic aniline. The market for bio-based aniline is also gaining traction due to environmental concerns and the growing demand for eco-friendly alternatives.

What are the market trends shaping the Aniline Market?

Shift towards bio aniline is the upcoming trend in the market.

- Aniline, a crucial chemical compound with the chemical formula C6H5NH2 and an amino group attached to a benzene ring, plays a significant role in various industries, including synthetic rubber production, dyes and pigments, pharmaceuticals, and plastics. The aniline market is diverse, spanning sectors such as automotive sales, construction and infrastructure, and the medical industry. Synthetic aniline is primarily produced through vapour-phase and liquid-phase processes, using benzene as a primary raw material. However, environmental concerns associated with conventional production methods have led to the emergence of bio-based aniline as a sustainable alternative. This eco-friendly approach involves producing aniline from renewable resources like biomass or agricultural feedstock, reducing greenhouse gas emissions, and promoting the effective use of renewable resources.

- Key industry players are actively investing in research and development to bring bio-based aniline manufacturing techniques to market. Bio-aniline is used in various applications, including the production of synthetic rubber for automotive interiors, electric vehicles, and insulating materials. It is also used in the manufacturing of vibrant dyes, analgesics, antibiotics, and polyurethane foams for seats, tubes, masks, bags, and other products. The firmness and lightweight properties of these foams make them ideal for use in construction and infrastructure projects. The shift towards bio-aniline is driven by increasing consumer awareness and regulatory pressure to reduce the environmental impact of industrial processes.

What challenges does the Aniline Market face during the growth?

Volatility in the prices of raw materials is a key challenge affecting market growth.

- The market is significantly influenced by the price fluctuations of its primary feedstock, benzene, which is derived from crude oil. The synthesis of aniline relies on the extraction of benzene rings and the addition of amino groups. This chemical compound is extensively used in various industry verticals, including synthetic rubber, dyes and pigments, plastics, and the medical industry. Aniline is a crucial component in the production of synthetic rubber, which is used to manufacture vibrant colors for textiles, coatings, and automotive sales. It is also employed in the synthesis of analgesics, antibiotics, and polyurethane foams for car interiors, electric vehicles, construction and infrastructure, insulating materials, sealants, and technology.

- The vapor-phase and liquid-phase processes are commonly used to produce aniline, with the former being more energy-efficient and environmentally friendly. The market dynamics are impacted by factors such as technological advancements, bio-based aniline, and the shift toward recycled materials. Environmental concerns have led to the development of synthetic and bio-based aniline, which is gaining traction in the market. Rigid polyurethanes, such as those used in medical devices, tubes, masks, bags, and PU foams for seats, require high-purity aniline. The market is diverse, with applications ranging from medical devices to automotive and construction industries. The firmness and lightweight properties of polyurethane foams make them ideal for use in various applications, including insulation, seating, and packaging.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast , partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ATAMAN Kimya AS

- BALAJI DYE CHEM

- BASF SE

- Chematek S.p.A.

- China Petrochemical Corp.

- Covestro AG

- Deepak Nitrite Ltd.

- Dow Chemical Co.

- EMCO Dyestuff Pvt. Ltd.

- GNFC Ltd.

- Huntsman International LLC

- Lanxess AG

- Mitsui Chemicals Inc.

- Par Industries

- R K Synthesis Ltd

- RX Marine International

- Shandong Jinling Group Co. Ltd.

- SP Chemicals Pte Ltd.

- Sumitomo Chemical Co. Ltd.

- Wanhua Chemical Group Co. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant player in the global chemical industry, with its applications extending to various sectors including synthetic rubber, dyes and pigments, pharmaceuticals, and polyurethanes. Aniline, a basic aromatic amine with the chemical formula C6H5NH2, is derived from the benzene ring through nitration and subsequent reduction. Synthetic rubber is a primary consumer of aniline, with its usage in the production of rubber chemicals such as di-aniline and diamine. These chemicals act as curing agents in the vulcanization process, enhancing the properties of synthetic rubber. The increasing demand for synthetic rubber in industries like automotive, construction, and infrastructure is driving the market growth.

Moreover, environmental concerns have emerged as a significant factor influencing the market. The production of aniline involves the use of benzene, a known carcinogen. However, efforts are being made to mitigate the environmental impact by introducing bio-based aniline derived from renewable resources. This shift towards sustainable production methods is expected to gain traction in the coming years. Aniline finds extensive applications in the production of dyes and vibrant colors. Its amino group acts as a building block in the synthesis of various dyes and pigments, contributing to the market's growth in the textile industry. Moreover, aniline is also used in the production of analgesics and antibiotics, further expanding its application scope.

Furthermore, the polyurethane industry is another significant consumer of aniline. Polyurethane foams are used in various applications such as car interiors, insulating materials, and seals. The increasing demand for lightweight and firm materials in the automotive industry and the growing focus on energy efficiency in construction and infrastructure are expected to fuel the growth of the market. Technological advancements in the aniline production process have led to the development of vapor-phase and liquid-phase processes. These methods offer advantages such as higher yield, reduced waste, and improved product quality. The adoption of these advanced production techniques is expected to enhance the competitiveness of market players and drive market growth.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.54% |

|

Market Growth 2024-2028 |

USD 4.54 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.28 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -