Polyurethane Foam Market Size 2025-2029

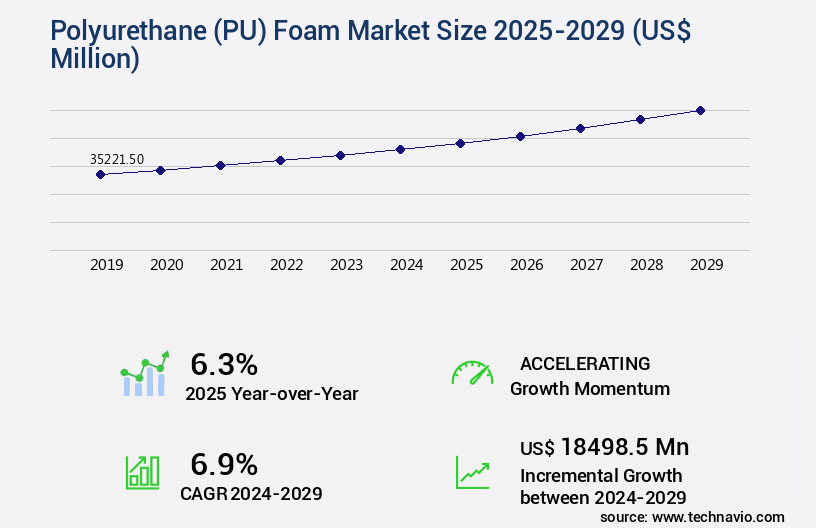

The polyurethane (PU) foam market size is forecast to increase by US $18.5 billion, at a CAGR of 6.9% between 2024 and 2029. The growing awareness of the environmental impact of foam production and disposal is fueling the search for more sustainable options.

Major Market Trends & Insights

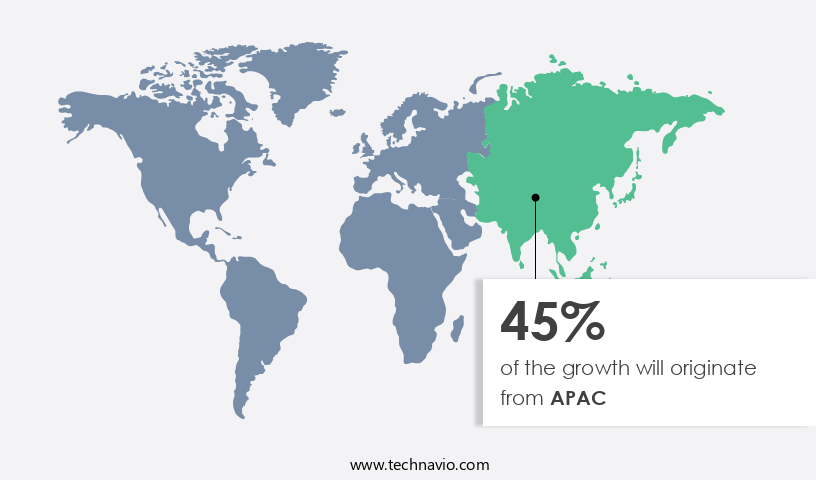

- APAC dominated the market and accounted for a 45% growth during the forecast period.

- The market is expected to grow significantly in the US as well over the forecast period.

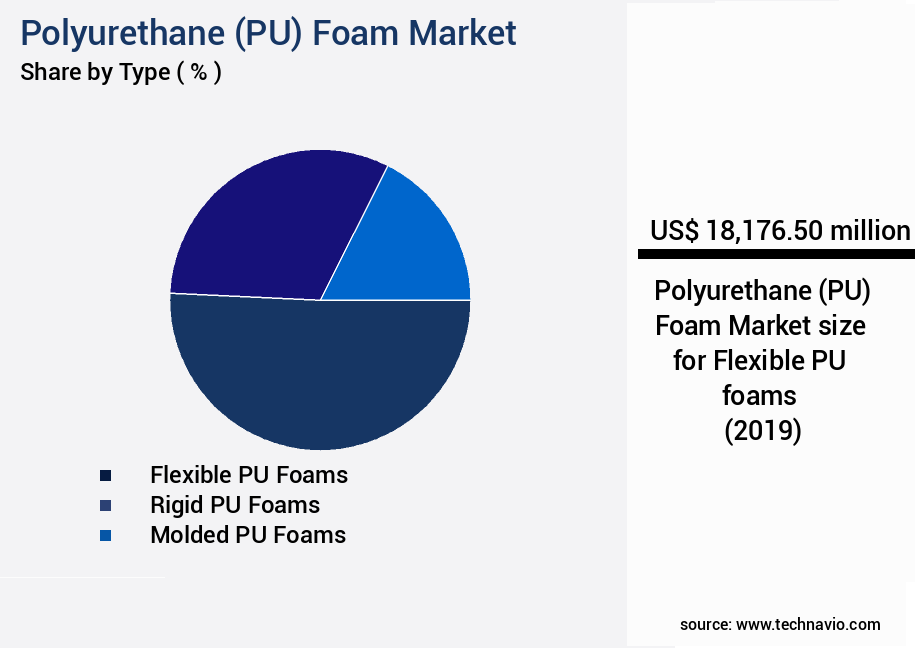

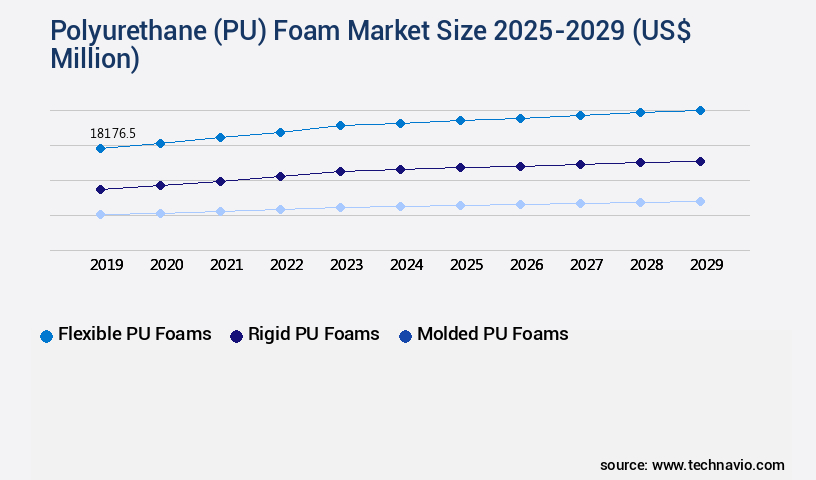

- By the Type, the Flexible PU foams sub-segment was valued at US $18.18 billion in 2023

- By the Application, the Furniture and bedding sub-segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: US $84.96 billion

- Future Opportunities: US $5 billion

- CAGR : 6.9%

- APAC: Largest market in 2023

- The market exhibits a significant level of dynamism, driven by the continuous expansion in various sectors. Notably, the demand for PU foams is on the rise in applications such as furniture and bedding due to their superior insulation properties and comfort. However, this trend is not without competition. Alternative foam types, like those based on methylal and hydrofluoroolefins (HFOs), are increasingly being adopted as substitutes for traditional PU foams that utilize hydrofluorocarbons (HFCs) and hydrochlorofluorocarbons (HCFCs). The shift towards these alternatives is primarily driven by stringent environmental regulations that aim to reduce the use of HFCs and HCFCs due to their high global warming potential.

- Despite the increasing popularity of alternatives, PU foams continue to dominate the market, accounting for a substantial market share. However, the competition is intensifying, with alternative foam types gaining ground in various applications. For instance, methylal-based foams are increasingly being used in the automotive industry due to their superior insulation properties and lower global warming potential. HFO-based foams, on the other hand, are gaining traction in the construction industry due to their excellent insulation properties and low ozone depletion potential.

- High-performance coatings, such as thermal insulation and thermal barrier coatings, offer energy efficiency and cost savings over their life cycle. This trend is being driven by consumer preferences for eco-friendly and sustainable products. Additionally, the high production costs associated with PU foam manufacturing, particularly due to the use of raw materials and energy-intensive processes, pose a significant challenge to market participants. Companies seeking to capitalize on the opportunities presented by this market must focus on innovation, cost optimization, and sustainability to remain competitive. However, the market also faces challenges, including the increasing demand for alternatives to PU foams, such as natural and recycled materials. Crude oil and natural gas serve as the fundamental raw materials for producing these binders.

- The market's dynamics are further shaped by the evolving regulatory landscape and technological advancements. For example, the European Union's F-Gas Regulation, which sets strict limits on the production and use of HFCs, is driving the adoption of alternative foam types. Similarly, advancements in foam production technology are enabling the production of foams with improved insulation properties and lower environmental impact. In conclusion, the PU foam market is a dynamic and evolving landscape, shaped by various factors such as changing consumer preferences, regulatory requirements, and technological advancements. The ongoing competition from alternative foam types is intensifying, making it essential for market players to stay informed and adapt to the changing market conditions.

What will be the Size of the Polyurethane (PU) Foam Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market exhibits significant growth, with current industry penetration reaching approximately 12% of the global insulation materials market. Looking ahead, this sector is projected to expand by over 5% annually, driven by increasing demand for energy efficiency and improved product performance. Comparatively, the PU foam market's growth outpaces that of traditional insulation materials, which typically experience a yearly expansion of around 3%. This discrepancy can be attributed to several factors, including process optimization, coating applications, and regulatory compliance. For instance, PU foam's exceptional insulation properties, such as high thermal resistance and dimensional stability, make it a preferred choice for various industries.

- Furthermore, advancements in foam rheology and fire resistance ratings have led to the development of innovative blowing agents and raw material sourcing strategies, enhancing both durability assessment and safety standards. These improvements contribute to the market's continued evolution, with key numerical data demonstrating the sector's competitive edge. For example, PU foam's tear strength is approximately 30% higher than that of other insulation materials, while its cell size distribution offers superior energy efficiency. Additionally, its compression set and density variation are significantly lower, ensuring long-lasting performance and reduced environmental impact. In conclusion, the PU foam market's growth trajectory, coupled with its superior physical and mechanical properties, positions it as a strategic investment opportunity for businesses seeking to optimize their operations and minimize environmental impact.

How is this Polyurethane (PU) Foam Industry segmented?

The polyurethane (pu) foam industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Flexible PU foams

- Rigid PU foams

- Molded PU foams

- Application

- Furniture and bedding

- Building and construction

- Transport

- Appliances

- Others

- Material

- MDI-based

- TDI-based

- Bio-based

- Geography

- North America

- US

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The flexible PU foams segment is estimated to witness significant growth during the forecast period.

The Polyurethane (PU) Foam Market advances through innovations like polyurethane foam thermal conductivity testing and closed cell polyurethane foam insulation values for energy-efficient polyurethane foam insulation building applications. Open cell polyurethane foam acoustic performance enhances automotive uses, while polyurethane foam applications automotive industry improve comfort. Polyurethane foam flammability standards and polyurethane foam VOC emission standards ensure safety. Effect catalyst concentration foam properties and influence isocyanate index foam structure optimize quality, alongside polyurethane foam production process optimization. Raw material selection effect polyurethane foam quality, polyurethane foam water absorption properties, and chemical resistance polyurethane foam different solvents drive durability. Polyurethane foam recycling technologies, compressive strength polyurethane foam different density, tensile strength polyurethane foam temperature, different types blowing agents polyurethane foam, polyurethane foam surface modification techniques, and polyurethane foam adhesion various substrates fuel market growth.

Flexible polyurethane (PU) foams are a versatile class of materials, finding extensive applications in various industries due to their superior properties. These foams exhibit excellent uv and hydrolysis resistance, making them suitable for outdoor applications. In terms of acoustic properties, they provide effective sound absorption and vibration damping, making them ideal for use in transportation and building insulation. The elongation at break of PU foams can reach up to 800%, allowing for superior flexibility and adaptability. Polyol selection, catalyst optimization, and blowing agent selection play crucial roles in determining the final properties of PU foams. Rigid foam applications include thermal insulation for buildings and refrigeration, while flexible foam applications span across furniture and bedding, carpet cushioning, automotive seating, and textile laminates.

Voc emissions from PU foam production are a concern, but recycling methods such as chemical crosslinking and foam processing have been developed to mitigate this issue. Tensile strength testing, compressive strength, and water absorption rate are essential properties that determine the performance of PU foams in various applications. Flame retardant additives are often incorporated to enhance safety. PU foam synthesis involves the reaction of polyols and isocyanates, resulting in a cellular structure that can be open- or closed-cell. Aging properties, such as thermal conductivity and foam density control, significantly impact the insulation performance of PU foams. Resilience testing is crucial to ensure the foams maintain their shape and provide adequate cushioning.

Spray foam insulation and molding techniques are popular methods for producing PU foams. Market trends include the development of foams with improved thermal conductivity and better insulation performance. The industry is expected to grow significantly, with an estimated 20% increase in demand for PU foams in the coming years. This growth is driven by the increasing demand for energy-efficient insulation materials and the expanding use of PU foams in various industries.

The Flexible PU foams segment was valued at USD 18.18 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 45% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Polyurethane (PU) Foam Market Demand is Rising in APAC Request Free Sample

The market in Asia Pacific (APAC) is currently the largest consumer of PU foams, with significant contributions from countries like China, South Korea, India, and Japan. In 2024, APAC accounted for approximately 45% of the global PU foam market share. Flexible PU foams, which are primarily used in mattresses and cushions, dominate the market in this region. The growing population in APAC, particularly in countries like China and India, is driving the demand for furniture and bedding. This trend is expected to continue, leading to a significant increase in the demand for PU foams in the region during the forecast period.

Furthermore, the increasing construction activities and rising demand for electronic appliances in APAC are also contributing to the growing demand for PU foams. According to recent industry reports, the PU foam market in APAC is projected to grow by around 5% per year between 2025 and 2030. This growth is attributed to the increasing demand for PU foams in various end-use industries, including construction, automotive, and furniture. The market's expansion is also being fueled by advancements in technology, which are leading to the production of high-performance PU foams with improved insulation properties and enhanced durability. In conclusion, the PU foam market in APAC is experiencing significant growth, driven by the increasing demand for PU foams in various end-use industries and the growing population.

The market is expected to continue expanding at a steady pace during the forecast period, making it an attractive investment opportunity for businesses looking to capitalize on the region's growing demand for PU foams.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The Polyurethane Foam Market is growing steadily, driven by its widespread use in construction, automotive, furniture, packaging, and electronics. Leading companies such as BASF, Huntsman Corporation, Covestro, Dow, and Recticel are innovating in flexible and rigid PU foams, spray foams, and sustainable blowing agents (HCFCs and HFOs) to meet rising performance and environmental standards. Key properties like thermal conductivity, flammability resistance, tensile strength, compressive strength, and acoustic insulation play a crucial role in product adoption across industries. Advancements in aging testing methods, chemical resistance optimization, and plasma surface treatments are enhancing foam durability and adhesion. Recycling technologies, including mechanical and chemical recycling, are being integrated to reduce environmental impact and align with EPA and REACH compliance. Regionally, Asia-Pacific leads demand growth, supported by rapid urbanization and automotive expansion, while North America and Europe emphasize sustainability regulations. Overall, polyurethane foam innovations are creating opportunities for energy efficiency, comfort, and long-term material performance.

The polyurethane foam market encompasses a diverse range of applications, from insulation and automotive industries to acoustic performance and flame retardancy. In this dynamic industry, rigorous testing plays a crucial role in ensuring the optimal properties of polyurethane foam. Regarding thermal conductivity, testing is essential to determine the insulation values of closed-cell foam, which typically offer lower conductivity than open-cell foam. For instance, closed-cell foam can have a thermal conductivity of 0.035 W/m.K, whereas open-cell foam can reach 0.042 W/m.K. Effect catalyst concentration significantly influences foam properties, including flammability. Meeting flammability standards is critical in various industries, such as automotive, where closed-cell foam with a low concentration of catalysts can meet stringent standards. Acoustic performance is another key consideration, with open-cell foam often preferred due to its superior sound absorption properties. For instance, open-cell foam can absorb up to 90% of sound energy, making it an excellent choice for sound insulation applications.

Polyurethane foam's water absorption properties can also vary depending on its density and structure. For instance, high-density foam has a lower water absorption rate than low-density foam. Optimizing the production process, including raw material selection, can significantly impact foam quality. Polyurethane foam aging testing methods are essential to assess its long-term performance. For example, compressive strength can decrease by up to 30% over ten years, depending on the foam density. Recycling technologies, such as chemical and mechanical methods, are being explored to minimize waste and reduce environmental impact. Tensile strength and temperature resistance are also essential properties, with different solvents influencing these characteristics. For instance, using a solvent with a high boiling point can increase tensile strength at higher temperatures. Polyurethane foam's chemical resistance varies depending on the solvent used. For example, using a solvent with excellent chemical resistance, such as toluene, can enhance the foam's overall durability. In the automotive industry, polyurethane foam is used for seating and insulation applications, while in building applications, it is used for insulation and soundproofing. Different types of blowing agents, such as hydrochlorofluorocarbons (HCFCs) and hydrofluoroolefins (HFOs), are used to produce various foam densities and properties. Surface modification techniques, such as grafting and plasma treatment, can also enhance foam adhesion to various substrates. In conclusion, the polyurethane foam market is a complex and dynamic industry, requiring rigorous testing and optimization to meet various industry standards and applications. From thermal conductivity and flammability to acoustic performance and chemical resistance, each property plays a crucial role in ensuring the optimal performance of polyurethane foam.

What are the key market drivers leading to the rise in the adoption of Polyurethane (PU) Foam Industry?

- The significant increase in demand for PU foams, particularly in the furniture and bedding industries, serves as the primary market driver.

- PU (Polyurethane) Foam Market encompasses various applications, primarily in sectors like furniture and bedding, construction, and automotive. In terms of volume, the furniture and bedding application held a significant market share in 2024. Flexible PU foams are extensively utilized in this domain, contributing to the manufacturing of office chairs, stadium seats, auditorium seats, carpets, luxury beds, and other furniture. These foams exhibit desirable properties, such as softness, durability, shape retention, and support, making them an ideal choice for cushioning material. Flexible PU foams' versatility is evident in their wide application scope. They are lightweight, possess low odor, exhibit resilience, and can rapidly recover after compression.

- These attributes make them indispensable in upholstered furniture and bedding, offering consumers customizable solutions. The construction sector also benefits from PU foams, with rigid foams used for insulation purposes, while flexible foams serve as cushioning materials. In the automotive industry, PU foams are employed for seating comfort and safety, as well as in sound insulation and thermal insulation applications. Comparatively, the furniture and bedding application accounted for a larger market share compared to the construction and automotive sectors in 2024. However, the construction sector is expected to witness substantial growth due to the increasing demand for energy-efficient insulation materials.

- The automotive industry is also anticipated to expand, driven by the rising demand for lightweight and comfortable vehicle interiors. Overall, the PU Foam Market continues to evolve, with ongoing advancements in foam technology and expanding applications across various industries.

What are the market trends shaping the Polyurethane (PU) Foam Industry?

- The emerging market trend involves a greater adoption of methylal and hydrofluoro-olefins (HFOs) as substitutes for hydrofluorocarbons (HFCs) and chlorofluorocarbons (HCFCs).

- The market is a dynamic and evolving industry, characterized by continuous innovation and adaptation to changing market conditions. PU foam is a type of plastic foam used in various applications due to its insulating properties and durability. Methylal and hydrofluoroolefins (HFOs) are increasingly being adopted as blowing agents in the manufacturing of PU foams, replacing hydrochlorofluorocarbons (HCFCs) and hydrofluorocarbons (HFCs). These alternatives offer advantages such as lower global warming potential (GWP) content compared to HFCs and HCFCs. Methylal, a clear, colorless, and flammable liquid with a sweet odor and a relatively low boiling point, is gaining popularity as a blowing agent.

- It is moderately soluble in water and miscible with common organic solvents. Methylal is primarily used as a solvent in the production of adhesives, resins, paint strippers, perfumes, and protective coatings. The ban on HCFCs in the US and emerging European countries is expected to drive the demand for methylal in these regions. The increasing adoption of PU foams in various sectors, including construction, automotive, and packaging, is contributing to the market's growth. In the construction sector, PU foams are used as insulation materials due to their excellent insulating properties. In the automotive industry, they are used for seating, headliners, and other applications.

- In the packaging sector, PU foams are used for protective packaging due to their cushioning properties. The market for PU foams is expected to continue its growth trajectory, driven by the increasing demand for insulation materials, the adoption of eco-friendly alternatives, and the expanding applications across various industries. The ongoing shift towards sustainable manufacturing processes and the increasing focus on reducing carbon emissions are also expected to provide opportunities for market growth.

What challenges does the Polyurethane (PU) Foam Industry face during its growth?

- The escalating demand for sustainable alternatives to polyurethane (PU) foams poses a significant challenge to the industry's growth trajectory.

- The market encompasses a diverse range of applications due to the material's versatility and desirable properties. PU foam is widely used in sectors such as furniture and bedding, building and construction, automotive, and packaging. However, concerns regarding its environmental impact have led to the emergence of alternative foam types. Natural latex, cotton fiber foam, organic wool, plain cotton, short-staple polyester fiber, and polystyrene are among the substitutes for PU foams. These alternatives offer various advantages, including biodegradability, resistance to dust mites, mold, and mildew, and the absence of harsh chemicals during manufacturing. For instance, natural latex is a popular substitute due to its biodegradable nature and resistance to allergens.

- Coconut fiber foam is another eco-friendly alternative, as no dye, bleach, or chemical cleaning agents are used during its production. Despite the availability of these alternatives, PU foam continues to dominate certain applications due to its unique properties. PU foam's ability to insulate, cushion, and absorb shock makes it a preferred choice in various industries. However, the market for PU foam is not static. Instead, it is characterized by continuous innovation and the development of new applications. For example, PU foam is increasingly being used in the automotive industry for noise reduction and energy absorption in vehicle interiors.

- In the construction sector, PU foam is used as insulation material for buildings, contributing to energy efficiency and reduced carbon emissions. The comparison of these foam types in terms of production volume is not straightforward, as data varies depending on the source. However, it is evident that the demand for PU foam and its alternatives continues to grow, driven by the evolving needs of various industries and increasing environmental consciousness.

Exclusive Customer Landscape

The polyurethane (pu) foam market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the polyurethane (pu) foam market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Polyurethane (PU) Foam Industry

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, polyurethane (pu) foam market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- All Foam Products Co.

- Armacell International SA

- Changzhou Sanhe Plastic Rubber Co. Ltd.

- Clark Foam Products Corp.

- Dafa AS

- FoamPartner Switzerland AG

- Hira Industries LLC

- INOAC Corp.

- JSP Ltd.

- Mitsui Chemicals Inc.

- Orlando Products Inc.

- Palziv Inc.

- PAR Group Ltd.

- Pregis LLC

- PTI Rubber and Gaskets Inc.

- Rogers Foam Corp.

- Sealed Air Corp.

- Wisconsin Foam Products

- Zotefoams plc

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Polyurethane (PU) Foam Market

- In January 2024, BASF, a leading chemical producer, announced the expansion of its global polyurethane (PU) foam production capacity by 100,000 tons per year. This expansion, according to BASF's press release, was in response to growing demand in the construction and automotive industries (BASF, 2024).

- In March 2024, Covestro, another major PU foam manufacturer, entered into a strategic partnership with Tesla, the electric vehicle maker. Covestro would supply Tesla with raw materials for its new, more sustainable PU foam production process, which Tesla claimed would reduce carbon emissions by up to 30% (Covestro, 2024).

- In May 2024, Huntsman Corporation completed the acquisition of CVC Thermoset Specialties, a leading producer of specialty polyurethane systems. This acquisition, according to Huntsman's SEC filing, would expand Huntsman's presence in the high-performance PU foam market and increase its global market share (Huntsman, 2024).

- In February 2025, the European Union (EU) approved the use of certain types of PU foam in insulation applications, citing their contribution to reducing greenhouse gas emissions and improving energy efficiency (European Commission, 2025). This approval is expected to boost the demand for PU foam in the EU construction sector.

Research Analyst Overview

- The market encompasses a diverse range of applications and continuous evolution, driven by advancements in technology and industry demands. This market's dynamism is evident in the ongoing research and development of various foam properties, including uv resistance, hydrolysis resistance, and acoustic properties. Polyurethane foam's elongation at break and tensile strength are crucial factors in rigid foam applications, such as insulation and construction. In the realm of insulation, PU foam's thermal insulation properties are highly sought after, with the industry anticipating a 4.5% annual growth rate through 2026. Polyol selection plays a significant role in foam synthesis, as it influences the final product's characteristics.

- Catalyst optimization and blowing agent selection are essential aspects of foam processing, ensuring optimal foam density control and thermal conductivity. Voc emissions are a critical concern in the PU foam market, with ongoing efforts to minimize these emissions through improved manufacturing processes and the use of flame retardant additives. Recycling methods are also being explored to address the environmental impact of PU foam production. The market's focus on innovation extends to molding techniques, which enable the creation of complex shapes and designs. Flexible foam properties, such as vibration damping and sound absorption coefficient, are increasingly important in various industries, including automotive and aerospace.

- PU foam's cellular structure, whether closed-cell or open-cell, influences its performance in various applications. Chemical crosslinking and isocyanate chemistry are essential aspects of foam synthesis, ensuring the desired foam properties and ensuring the foam's aging properties remain consistent over time. Spray foam insulation's popularity continues to grow due to its ease of application and high insulation performance. The market's ongoing research and development efforts aim to improve foam processing techniques and enhance insulation performance, ensuring PU foam remains a key player in the global insulation market.

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Polyurethane (PU) Foam Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

227 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.9% |

|

Market growth 2025-2029 |

USD 18.49 billion |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

6.3 |

|

Key countries |

China, US, India, Japan, Germany, France, UK, South Korea, Brazil, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Polyurethane (PU) Foam Market Research and Growth Report?

- CAGR of the Polyurethane (PU) Foam industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, Middle East and Africa, and South America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the polyurethane (pu) foam market growth of industry companies

We can help! Our analysts can customize this polyurethane (pu) foam market research report to meet your requirements.

RIA -

RIA -