APAC Automotive OEM Coatings Market Size 2024-2028

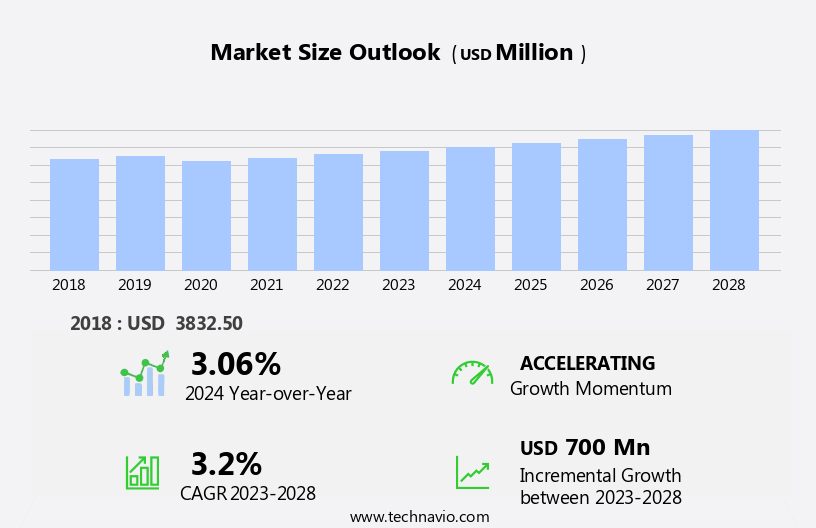

The APAC automotive OEM coatings market size is forecast to increase by USD 700 million at a CAGR of 3.2% between 2023 and 2028.

- The market is witnessing significant growth due to the availability of coatings designed for fuel-efficient automobiles. This trend aligns with the increasing focus on reducing carbon emissions and improving fuel economy In the region. Furthermore, the adoption of advanced coatings such as UV-curable coatings and nanocoatings is on the rise, driven by their superior protective properties and ability to enhance the aesthetic appeal of vehicles. Nanocoatings offer enhanced durability and corrosion resistance. However, stringent regulations regarding the use of volatile organic compounds (VOCs) and other harmful substances in coatings are posing challenges to market growth. Producers are responding by developing eco-friendly alternatives to meet these regulations while maintaining the performance and durability of their products.

What will be the size of the APAC Automotive OEM Coatings Market during the forecast period?

- The market is experiencing significant growth due to increasing vehicle production and sales. The market size is substantial, driven by the demand for various coatings types, including UV-curable, nanocoatings, specialty products, and both powder and liquid coatings. company selection is a critical factor as OEMs prioritize coatings that meet stringent regulations, such as those related to Volatile Organic Compounds (VOCs) and film thickness. Epoxy primer, clearcoat, basecoat, primer, e-coat, polyurethane, acrylic, epoxy, alkyd, and other coatings are widely used In the production of passenger cars and two-wheelers.

- Solvent-borne, high-solid, and UV-cured coatings are popular choices due to their environmental friendliness and performance benefits. The market is also witnessing the emergence of advanced coatings technologies, such as UV-curable and nano coatings, which offer improved durability, corrosion resistance, and reduced manufacturing costs. Overall, the market is dynamic and growing, driven by increasing vehicle production and the adoption of advanced coating technologies.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Technology

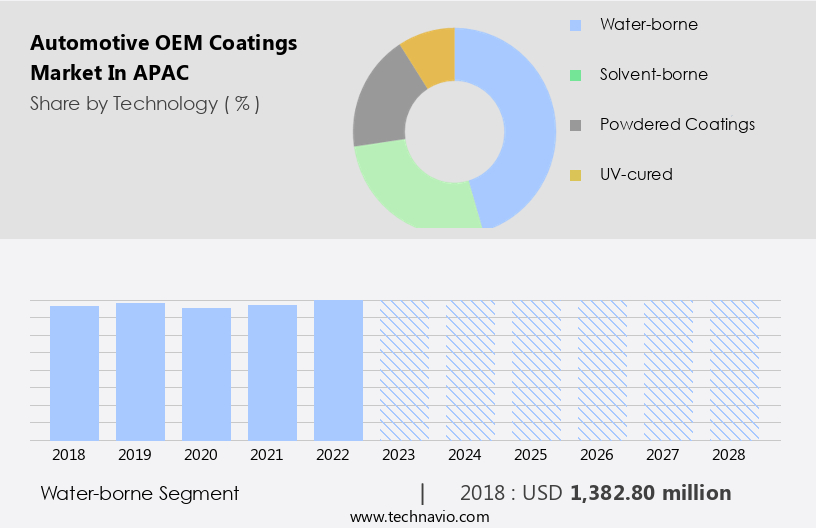

- Water-borne

- Solvent-borne

- Powdered coatings

- UV-cured

- Vehicle Type

- Passenger cars

- Light commercial vehicles

- Heavy commercial vehicles

- Geography

- APAC

- China

- India

- Japan

- South Korea

- APAC

By Technology Insights

- The water-borne segment is estimated to witness significant growth during the forecast period.

In the market, waterborne coatings are gaining popularity due to their eco-friendly properties. These coatings consist primarily of water as a solvent, with minimal additives of glycol ethers. The longer evaporation time of waterborne coatings, influenced by environmental conditions, is offset by their reduced environmental impact and ease of application. However, they may release volatile organic compounds (VOCs) when mixed with reducers, although in lower quantities than solvent-borne coatings. Automotive OEM coatings in APAC encompass a range of products, including UV-curable coatings, nanocoatings, specialty products, powder coatings, and liquid coatings. company selection is crucial for automakers In the luxury, middle-class, and upper-middle-class segments, as they prioritize energy-efficient transportation and address environmental concerns.

Coating manufacturers cater to the metal parts and plastic parts categories with offerings like Acrythane 4G, Hempaprime Shield 700 HS, epoxy primer, clearcoat, basecoat, primer, e-coat, polyurethane, acrylic, epoxy, and alkyd. commercial vehicles. and commercial utility vehicles also utilize coatings to enhance their durability and appearance. Macroeconomic growth and increasing motor vehicle registrations, particularly In the EU, New passenger Cars, and commercial vehicle segments, are driving market demand. As the industry evolves, there is a growing focus on energy-efficient transportation and reducing wastewater and paint sludge. High-solid coatings and UV-cured coatings are gaining traction due to their lower VOC content and faster curing times.

Get a glance at the market share of various segments Request Free Sample

The water-borne segment was valued at USD 1.38 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of APAC Automotive OEM Coatings Market?

The availability of coatings designed for fuel-efficient automobiles is the key driver of the market.

- The market is witnessing significant growth due to increasing environmental concerns and stricter emission norms. UV-curable coatings and nanocoatings are gaining popularity for their ability to reduce volatile organic compounds (VOCs) in coatings. Specialty products, such as high-solid coatings and powder coatings, are also being adopted for their lower film thickness and reduced wastewater and paint sludge generation. Coating manufacturers are focusing on the development of energy-efficient transportation solutions, including the use of Acrythane 4G in commercial vehicles and Commercial Utility Vehicles. In the passenger car segment, clearcoats, sun, and UV-resistant solvent-borne and waterborne coatings are in demand.

- The metal parts category continues to dominate the market, but plastic parts are increasingly being used for weight reduction. Key technologies include E-Coat, Polyurethane, Acrylic, Epoxy, Alkyd, and various other coatings such as Paints, Varnishes, Enamels, and Lacquers. Companies are focusing on innovation to meet the demands of the luxury, middle-class, and upper-middle-class automotive markets. Regulations, such as the Kyoto Protocol, are driving the market towards more sustainable and eco-friendly coatings.

What are the market trends shaping the APAC Automotive OEM Coatings Market?

Growing adoption of UV-curable coatings and nanocoatings is the upcoming trend In the market.

- In the market, UV-curable coatings are gaining traction due to their high performance and assembly-line advantages. The market is witnessing significant R&D investments in UV-curable coatings, which provide superior scratch and mar resistance. Although UV-curable coatings hold a small market share currently, their adoption is projected to rise due to the increasing number of automotive OEMs adopting these coatings. Nanocoatings and specialty products are other emerging categories in the market.

- Companies are focusing on developing high-performance coatings with low Volatile Organic Compounds (VOCs) and thin film thickness to meet environmental concerns and wastewater regulations. Coating manufacturers offer a wide range of products, including powder coatings, liquid coatings, clearcoats, basecoats, primers, E-Coat, polyurethane, acrylic, epoxy, and alkyd. The market caters to various segments, including passenger cars, commercial vehicles, and two-wheelers. The market is driven by macroeconomic growth, increasing motor vehicle registrations, and the shift towards energy-efficient transportation. The clearcoat category is a significant contributor to the market, with sun and UV resistance being critical factors.

What challenges does APAC Automotive OEM Coatings Market face during the growth?

Stringent regulations affecting market growth is a key challenge affecting the market growth.

- Automotive Original Equipment Manufacturer (OEM) coatings are essential for safeguarding automotive parts from environmental hazards and wear. These coatings enhance the durability and resistance of metal and plastic parts against extreme temperatures, weather conditions, and chemicals. The formulation of automotive OEM coatings includes various additives, such as UV-curable nanocoatings and specialty products, to improve their anti-corrosive, mechanical flexibility, and resistance to chemicals and heat. However, these additives can pose environmental concerns due to their toxic nature, which includes potential health risks related to components like silica, lead, and Volatile Organic Compounds (VOCs). Solvent-borne coatings, a common type of automotive OEM coatings, contain volatile chemicals that can negatively impact the environment.

- The production and application of these coatings generate wastewater and paint sludge, which require proper disposal to mitigate environmental harm. Coating manufacturers are addressing these concerns by introducing alternatives such as UV-cured, high solid, and powder coatings. Automotive OEM coatings are used extensively In the luxury, middle-class, and upper-middle-class automotive sectors. The clearcoat category, which includes coatings for sun and UV protection, is particularly popular In the luxury automotive segment. In the commercial vehicle sector, energy-efficient transportation and environmental concerns are driving the demand for coatings that offer improved durability and reduced VOC emissions.

Exclusive APAC Automotive OEM Coatings Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Akzo Nobel NV

- Axalta Coating Systems Ltd.

- BASF SE

- Berger Paints India Ltd

- Color Communications LLC

- Dai Nippon Toryo Co. Ltd.

- Grand Polycoats Co. Pvt. Ltd.

- Isamu Paint Co. Ltd.

- Jotun AS

- Kansai Paint Co. Ltd.

- KCC Co. Ltd.

- Nippon Paint Holdings Co. Ltd.

- PPG Industries Inc.

- ROCK PAINT Co. Ltd.

- RPM International Inc.

- S.Coat Co. Ltd.

- Savita Paints Pvt. Ltd.

- Solvay SA

- Tara Paints and Chemicals

- The Sherwin Williams Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market In the Asia Pacific (APAC) region is experiencing significant growth due to the increasing demand for vehicles In the region. This market encompasses a wide range of coatings, including UV-curable coatings, nanocoatings, and specialty products. The automotive industry in APAC is driven by the expanding middle-class and upper-middle-class populations, leading to an increase in motor vehicle registrations. The luxury automotive segment also contributes to the growth of the OEM coatings market, as consumers seek high-quality finishes for their vehicles. The coatings market caters to both metal and plastic parts In the automotive industry.

Moreover, UV-curable coatings and high solid coatings are popular choices for their energy efficiency and reduced volatile organic compound (VOC) emissions. However, solvent-borne coatings, such as acrythane 4G, continue to be used in certain applications due to their superior film thickness and durability. Coating manufacturers are focusing on developing innovative solutions to address environmental concerns. For instance, waterborne coatings and powder coatings are gaining popularity due to their lower VOC emissions and reduced wastewater generation. Coating manufacturers are also developing e-coat primers and clearcoats that offer improved corrosion resistance and better UV protection. The market is highly competitive, with several key players vying for market share.

Furthermore, coating manufacturers are investing in research and development to offer advanced coatings that cater to the specific needs of the automotive industry. The clearcoat category is a significant segment of the automotive OEM coatings market, as it provides a protective layer against the sun's UV rays and other environmental factors. UV-curable clearcoats offer superior UV protection and faster curing times, making them a popular choice among automakers. The use of coatings in commercial vehicles and commercial utility vehicles is also on the rise, as these vehicles are subjected to heavy usage and harsh operating conditions. Coatings with improved durability and corrosion resistance are preferred in this segment.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

173 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.2% |

|

Market Growth 2024-2028 |

USD 700 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.06 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -