Application Management Services Market Size 2026-2030

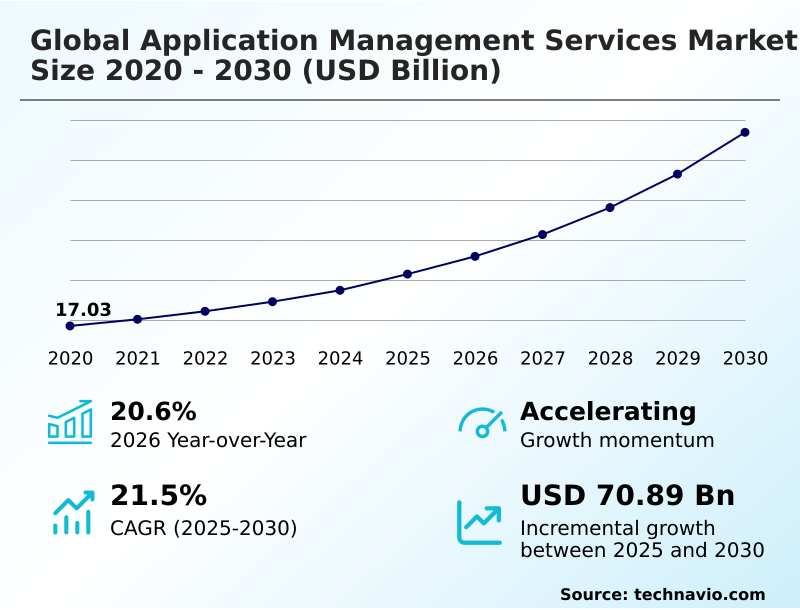

The application management services market size is valued to increase by USD 70.89 billion, at a CAGR of 21.5% from 2025 to 2030. Pervasive imperative of digital transformation and application modernization will drive the application management services market.

Major Market Trends & Insights

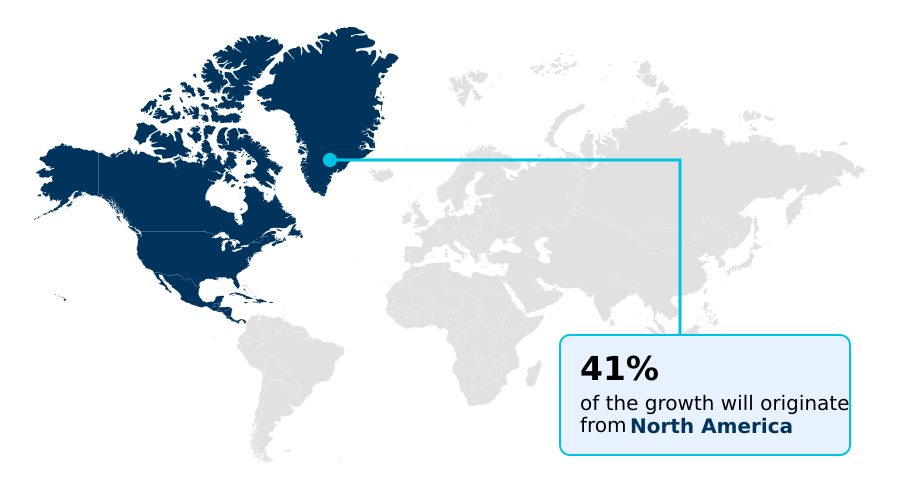

- North America dominated the market and accounted for a 41.2% growth during the forecast period.

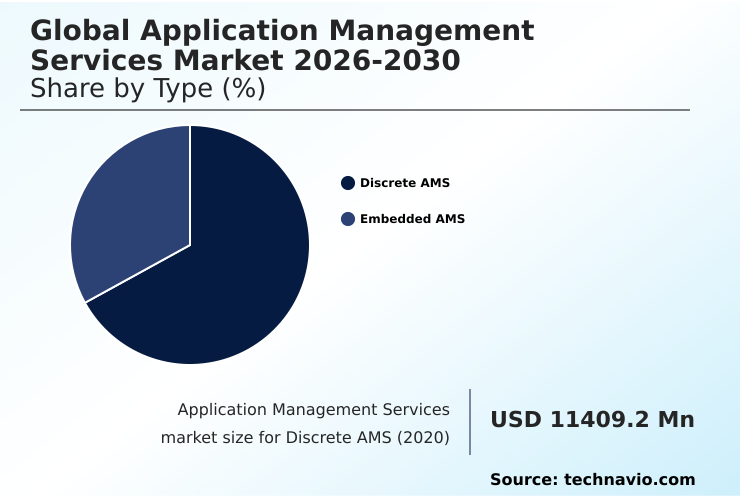

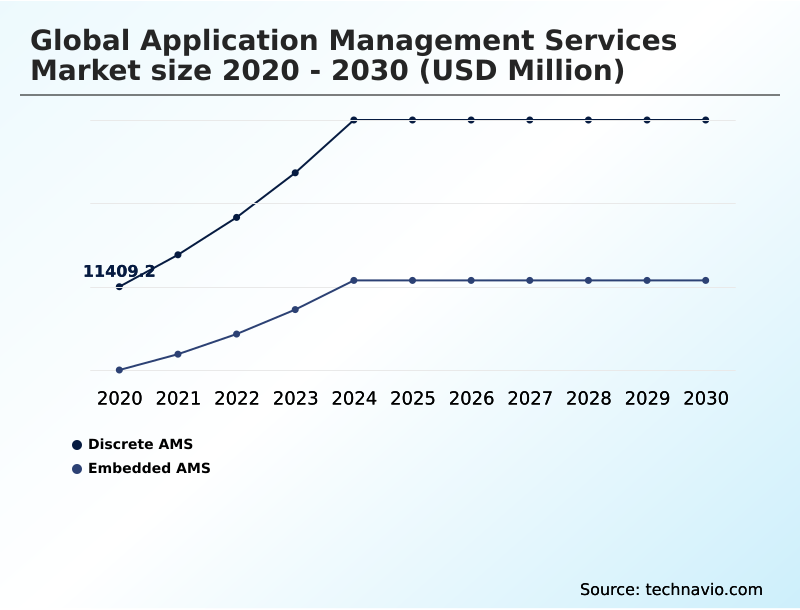

- By Type - Discrete AMS segment was valued at USD 23.00 billion in 2024

- By End-user - Small and medium enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 96.81 billion

- Market Future Opportunities: USD 70.89 billion

- CAGR from 2025 to 2030 : 21.5%

Market Summary

- The application management services market is defined by its role in governing the complete lifecycle of an organization's software portfolio. Beyond traditional break-fix support, it encompasses proactive monitoring, maintenance, and continuous enhancement to ensure optimal performance and security. A primary driver is the enterprise-wide pursuit of digital transformation, which necessitates the modernization of legacy applications that hinder agility.

- For example, a global retail enterprise must ensure its e-commerce platform remains highly available and scalable during peak holiday seasons, a task that requires specialized expertise in cloud-native architectures and performance tuning. By outsourcing application management, the company can leverage a provider's established frameworks for cloud migration and DevOps methodologies.

- This partnership allows the internal IT team to shift its focus from routine operational tasks to strategic, value-generating projects like developing new personalized customer experiences.

- The market is also propelled by the need to bridge the widening technical skills gap, as managing a complex hybrid portfolio of on-premises, cloud, and SaaS applications demands a broad spectrum of expertise that is difficult to maintain in-house, making external service providers a critical enabler of business continuity and innovation.

What will be the Size of the Application Management Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Application Management Services Market Segmented?

The application management services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Discrete AMS

- Embedded AMS

- End-user

- Small and medium enterprises

- Large enterprises

- Deployment

- Hosted

- On-premises

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- North America

By Type Insights

The discrete ams segment is estimated to witness significant growth during the forecast period.

The global application management services market segments by type, end-user, deployment, and geography. By type, the market includes Discrete AMS and Embedded AMS. The end-user segment comprises Small and Medium Enterprises and Large Enterprises.

Deployment is categorized into Hosted and On-premises. Geographically, the market is divided into North America, APAC, Europe, the Middle East and Africa, and South America. North America is the largest region, while APAC shows the fastest growth, driven by digitalization.

A key driver across segments is the adoption of DevOps methodology. For instance, a focus on application portfolio rationalization allows for strategic technical debt reduction. Providers use AI-driven application support services to manage complex hybrid IT environments effectively.

Utilizing proactive performance monitoring helps maintain service level agreement management, and software composition analysis is crucial for securing the application lifecycle in the cloud.

This approach to managing application portfolios has led to a 20% improvement in resource utilization for firms that adopt a product-centric delivery model.

The Discrete AMS segment was valued at USD 23.00 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 41.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Application Management Services Market Demand is Rising in North America Get Free Sample

The global application management services market is geographically dominated by North America, which accounts for over 41% of the market's incremental growth, driven by its mature digital infrastructure and focus on optimizing application portfolios.

This region excels in proactive issue resolution and has a high adoption rate of agile and DevOps practices. In contrast, the APAC region is the fastest-growing market, fueled by rapid economic expansion and widespread digitalization, particularly in China and India.

Europe remains a significant market, with a strong emphasis on regulatory compliance, where service providers help organizations maintain over 99% adherence to data protection mandates like GDPR. Key activities include application performance tuning and navigating complex hybrid IT environments.

The Middle East and Africa and South America are emerging markets, showing increasing demand for application modernization and cloud migration services to support their developing digital economies and enhance business agility across various sectors.

Market Dynamics

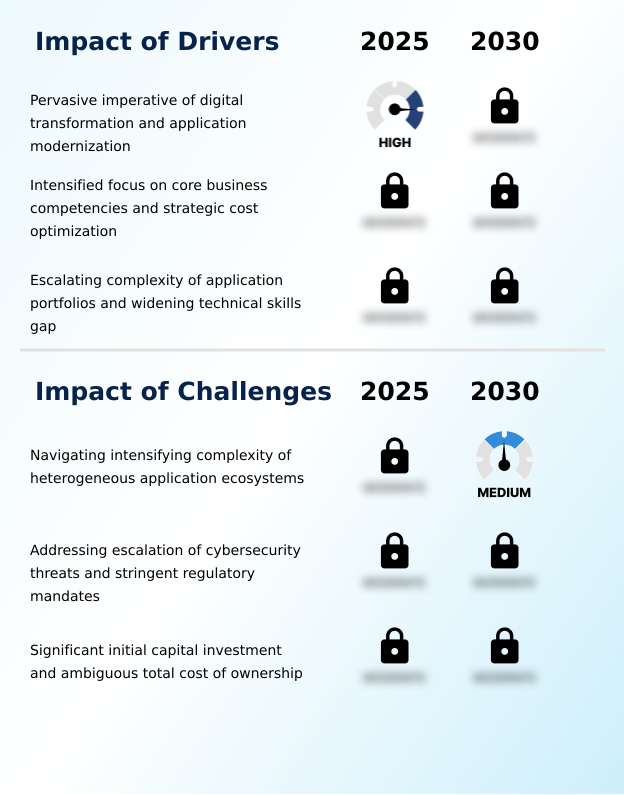

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the application management services market is increasingly focused on long-term value and operational resilience. A primary consideration is managing the application lifecycle in the cloud, which involves more than just migration; it requires continuous optimization and governance.

- Organizations are adopting AI-driven application support services to move from reactive to predictive maintenance, a shift that is critical for business continuity. A key goal for CFOs is optimizing application total cost of ownership, which involves a careful analysis of both direct and indirect expenses over the application's lifespan.

- Implementing DevSecOps for enterprise application security is no longer optional but a baseline requirement to mitigate threats in an increasingly complex digital landscape. Furthermore, a well-defined application modernization for digital transformation strategy is essential for businesses looking to maintain a competitive edge. This is often coupled with a comprehensive legacy application portfolio management strategy to systematically reduce technical debt.

- The effectiveness of these initiatives is measured by clear service level agreements in AMS. For instance, companies that effectively implement a strategy for managing enterprise application integration complexity report a twofold improvement in their ability to launch new integrated services compared to those without a formal approach. This demonstrates the tangible link between expert application management and business agility.

- The focus extends to ensuring high availability for critical business applications and providing proactive IT support for business process continuity, making AMS a cornerstone of modern enterprise operations.

What are the key market drivers leading to the rise in the adoption of Application Management Services Industry?

- The pervasive imperative for digital transformation and application modernization is a key driver for market growth.

- The primary driver for the application management services market is the enterprise-wide imperative for digital transformation, compelling organizations to pursue legacy system modernization.

- By engaging service providers, companies can reduce technical debt and re-architect monolithic systems into agile microservices architectures, a process that internal teams often lack the specialized skills to manage.

- This strategic outsourcing allows businesses to reallocate up to 35% of their internal IT talent toward value-generating innovation. Another key driver is the pursuit of cost optimization through a predictable operational expenditure model, which leverages a provider's economies of scale.

- The widening technical skills gap further fuels demand, as managing complex hybrid IT environments with container orchestration and multi-cloud strategies requires expertise that is scarce and expensive to hire, making application portfolio rationalization through a partner an efficient solution.

What are the market trends shaping the Application Management Services Industry?

- The ascendancy of hyperautomation and artificial intelligence for IT operations (AIOps) is a transformative trend. It is reshaping application management from reactive support to a proactive and predictive operational framework.

- A transformative trend in the application management services market is the integration of hyperautomation and AI-Ops platforms. This shift from reactive to predictive operational frameworks is redefining service delivery, with automated root cause analysis improving issue resolution times by up to 45%.

- Organizations are adopting platform engineering principles to build robust, self-service internal developer platforms, which has been shown to boost developer productivity by over 30%. This product-centric delivery model, supported by continuous integration and continuous delivery (CI/CD) pipelines, accelerates feature deployment.

- Furthermore, the pervasive integration of security through DevSecOps methodologies is critical, embedding software composition analysis and other automated controls early in the lifecycle. This 'shift-left' approach significantly reduces remediation costs and enhances the overall security posture of applications under management.

What challenges does the Application Management Services Industry face during its growth?

- Navigating the intensifying complexity of heterogeneous application ecosystems presents a key challenge to industry growth.

- A formidable challenge in the application management services market is navigating the escalating complexity of heterogeneous application portfolios. These ecosystems, comprising legacy systems, cloud-native services, and SaaS platforms, create significant integration and governance hurdles, with integration failures accounting for nearly 50% of critical business disruptions.

- The relentless pace of technological change requires providers to constantly adapt to new paradigms like serverless computing. Another critical challenge is the dual pressure of a sophisticated cybersecurity landscape and stringent regulatory mandates. Providers must embed proactive security measures and ensure compliance with rules like GDPR, which can increase project costs by 15% if not managed proactively.

- Finally, the ambiguity surrounding the total cost of ownership, including high initial transition costs and unpredictable long-term fees, acts as a significant restraint on market adoption, particularly for small and medium-sized enterprises.

Exclusive Technavio Analysis on Customer Landscape

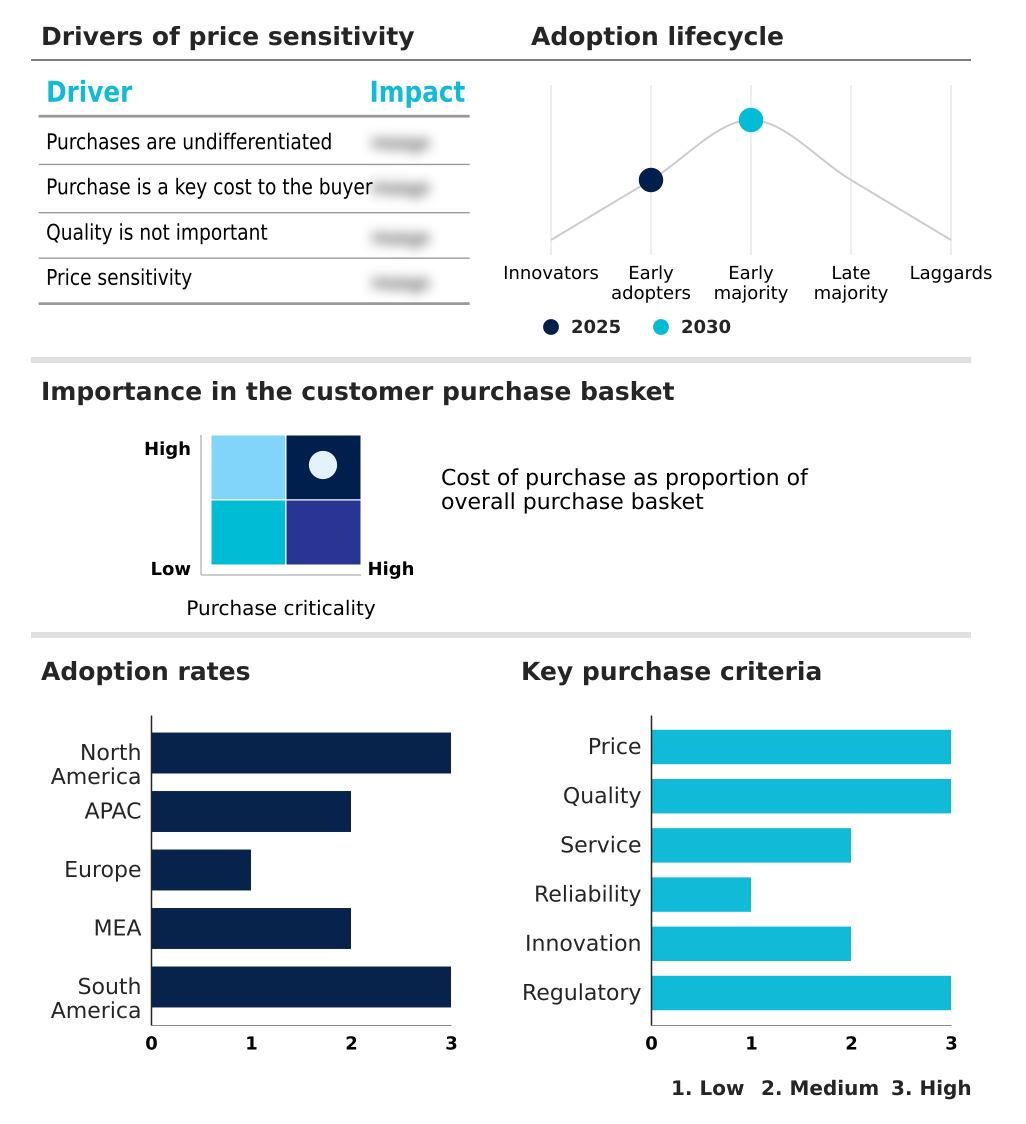

The application management services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the application management services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Application Management Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, application management services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Providers deliver comprehensive application lifecycle governance, ensuring optimal performance, security, and alignment with strategic business goals through outsourced expertise.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Atos SE

- Capgemini SE

- Cognizant Technology Solution

- Deloitte Touche Tohmatsu Ltd.

- DXC Technology Co.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- Hexaware Technologies Ltd.

- IBM Corp.

- Infosys Ltd.

- LTIMindtree Ltd.

- Mphasis Ltd.

- NTT DATA Corp.

- Oracle Corp.

- SAP SE

- ScienceSoft USA Corp.

- Tata Consultancy Services

- Unisys Corp.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Application management services market

- In January 2025, IBM Corp. acquired Applications Software Technology to bolster its capabilities in Oracle Cloud transformation services, reflecting the strategic importance of cloud expertise in the North American market.

- In February 2025, Infosys Ltd. announced a strategic partnership with Lufthansa to drive digital transformation within the aviation industry, focusing on modernizing its application landscape.

- In May 2025, Amazon Web Services pledged an investment of over USD 4 billion to establish a new cloud region in Chile, significantly enhancing digital infrastructure and accelerating cloud-native application adoption in South America.

- In October 2025, DXC Technology Co. launched Assure Broking Essentials, an AI-powered SaaS platform designed for the insurance brokerage industry, highlighting the trend toward industry-specific, technology-driven solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Application Management Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 327 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 21.5% |

| Market growth 2026-2030 | USD 70891.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 20.6% |

| Key countries | US, Canada, Mexico, China, Japan, India, Australia, South Korea, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, UAE, Saudi Arabia, South Africa, Israel, Egypt, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The application management services market is fundamentally evolving from a cost-saving utility to a strategic enabler of business innovation. Central to this shift is the widespread adoption of legacy system modernization and application portfolio rationalization. Organizations are leveraging DevOps methodology and microservices architecture to dismantle monolithic structures, thereby reducing technical debt and enhancing agility.

- Boardroom decisions are now directly influenced by the need for continuous integration and continuous delivery (CI/CD) to accelerate speed-to-market. For instance, companies embracing platform engineering have demonstrated a 40% faster rollout of new digital products. This is achieved through a product-centric delivery model, where AI-Ops platforms and container orchestration provide the foundation for resilient and scalable systems.

- Service level agreement management has become more sophisticated, focusing on business outcomes rather than simple uptime metrics. The integration of software composition analysis into the development pipeline is a non-negotiable aspect of risk management, addressing vulnerabilities in open-source components proactively.

- This holistic approach, combining proactive performance monitoring with a robust multi-cloud management strategy, is critical for navigating today's complex hybrid IT environment and unlocking true business value from technology investments.

What are the Key Data Covered in this Application Management Services Market Research and Growth Report?

-

What is the expected growth of the Application Management Services Market between 2026 and 2030?

-

USD 70.89 billion, at a CAGR of 21.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Discrete AMS, and Embedded AMS), End-user (Small and medium enterprises, and Large enterprises), Deployment (Hosted, and On-premises) and Geography (North America, APAC, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Pervasive imperative of digital transformation and application modernization, Navigating intensifying complexity of heterogeneous application ecosystems

-

-

Who are the major players in the Application Management Services Market?

-

Accenture Plc, Atos SE, Capgemini SE, Cognizant Technology Solution, Deloitte Touche Tohmatsu Ltd., DXC Technology Co., Fujitsu Ltd., HCL Technologies Ltd., Hexaware Technologies Ltd., IBM Corp., Infosys Ltd., LTIMindtree Ltd., Mphasis Ltd., NTT DATA Corp., Oracle Corp., SAP SE, ScienceSoft USA Corp., Tata Consultancy Services, Unisys Corp. and Wipro Ltd.

-

Market Research Insights

- The market is undergoing a significant shift from tactical support to strategic, value-driven partnerships. Organizations are leveraging automated root cause analysis and integrating IT service management to enhance operational efficiency. This focus on total cost of ownership modeling and business process outsourcing allows for better resource allocation.

- Adopting a product-centric delivery model, supported by robust platform engineering principles, has enabled companies to achieve an 18% improvement in aligning IT outputs with business goals. Furthermore, a multi-cloud management strategy is becoming standard, with firms reporting up to a 25% reduction in cloud spend through optimized governance and FinOps practices.

- This evolution highlights a clear move toward agile, outcome-based engagements.

We can help! Our analysts can customize this application management services market research report to meet your requirements.

RIA -

RIA -