Application Modernization Services Market Size 2026-2030

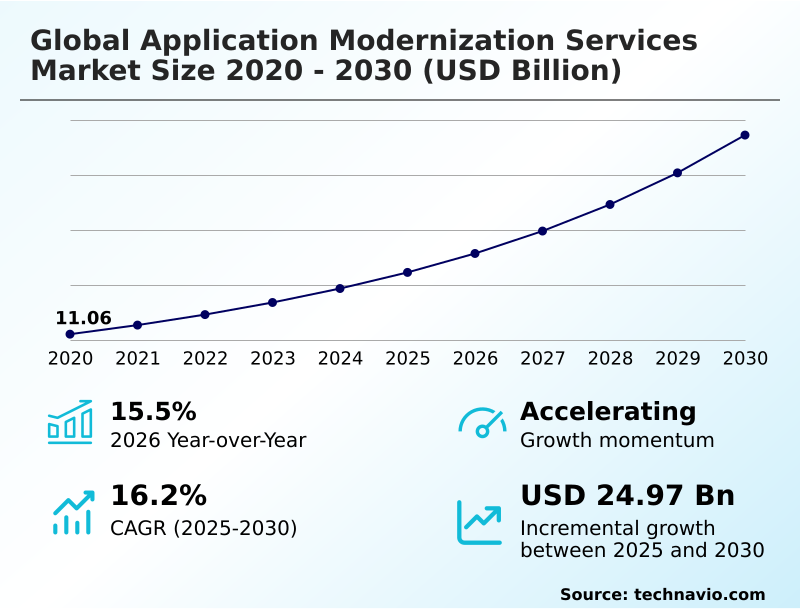

The application modernization services market size is valued to increase by USD 24.97 billion, at a CAGR of 16.2% from 2025 to 2030. Integration of generative AI into legacy frameworks will drive the application modernization services market.

Major Market Trends & Insights

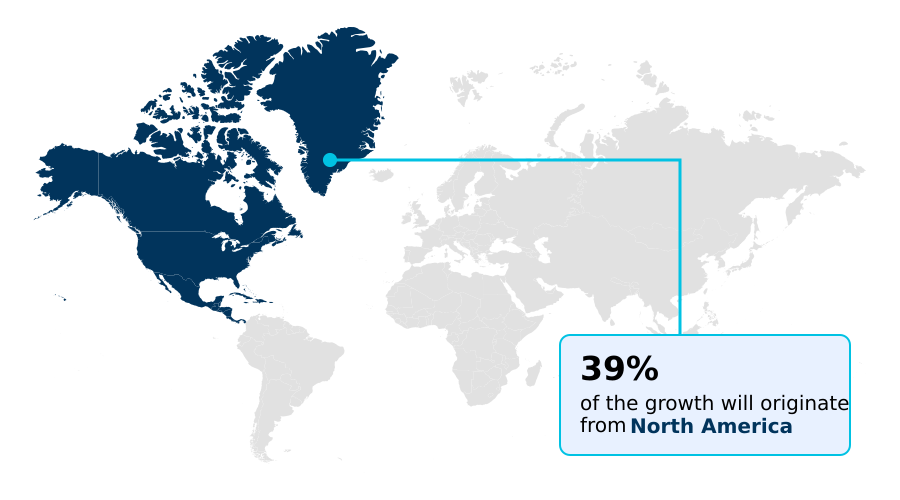

- North America dominated the market and accounted for a 38.6% growth during the forecast period.

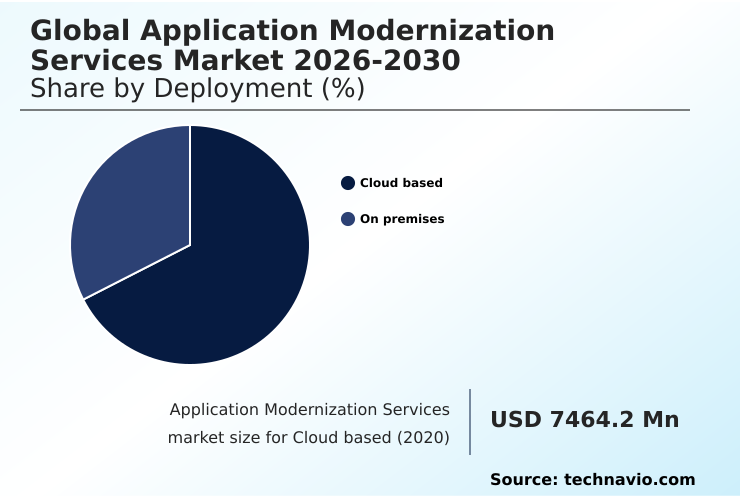

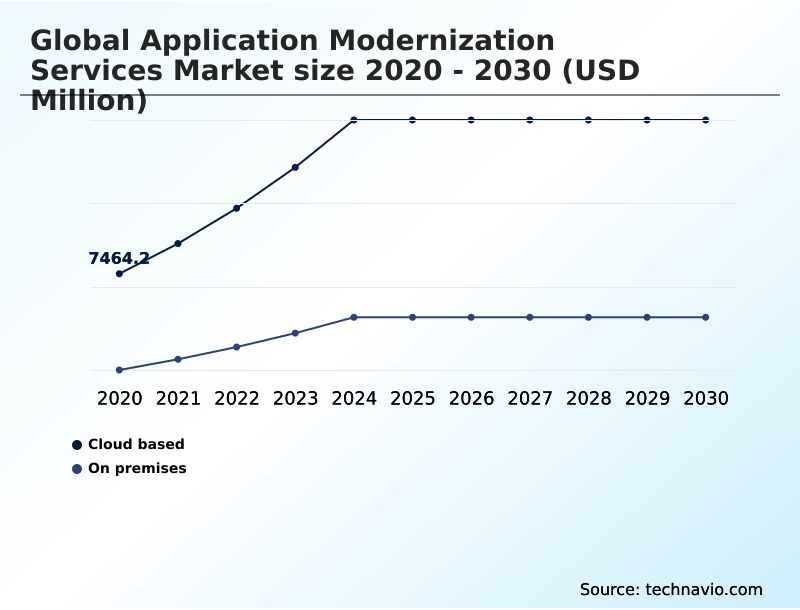

- By Deployment - Cloud based segment was valued at USD 13.64 billion in 2024

- By Business Segment - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 36.20 billion

- Market Future Opportunities: USD 24.97 billion

- CAGR from 2025 to 2030 : 16.2%

Market Summary

- The application modernization services market is undergoing a significant expansion as businesses pursue a digital transformation journey to replace outdated systems with agile, high-performance architectures. This shift is driven by the need for a cloud-native transformation to leverage advanced technologies.

- Key trends include the transition from monolithic to microservices, the adoption of a containerization strategy, and the use of serverless computing architecture to enhance scalability. A major driver is the strategic imperative for technical debt reduction and strengthening software supply chain security, as legacy systems are often vulnerable.

- However, organizations face challenges such as the it skills gap mitigation and the complexities of data integrity management during mainframe migration. For instance, a global logistics firm might undergo enterprise resource planning modernization to improve supply chain visibility improvement, enabling it to respond more effectively to market demands.

- This transformation, involving agile development methodologies and devops integration, is a fundamental business necessity for achieving a resilient software architecture.

What will be the Size of the Application Modernization Services Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Application Modernization Services Market Segmented?

The application modernization services industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud based

- On premises

- Business segment

- Large enterprises

- Small and medium enterprises

- End-user

- BFSI

- Retail and e-commerce

- IT and telecom

- Manufacturing

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- India

- Japan

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud based segment is estimated to witness significant growth during the forecast period.

The cloud-based segment is defined by a strategic shift from capital expenditure vs operational expenditure models, driving organizations toward a complete cloud-native transformation.

This approach prioritizes the adoption of serverless computing architecture and other serverless models to enhance IT operational efficiency and build a resilient software architecture.

The modernization journey involves legacy system reengineering and significant IT infrastructure upgrades to manage a hybrid cloud environment effectively. A key focus is on technical debt reduction and application portfolio rationalization, which minimizes legacy system maintenance costs.

This transition is critical for business continuity planning, as it avoids vendor lock-in and improves return on investment, with some firms reporting a 25% decrease in deployment failures post-migration.

The Cloud based segment was valued at USD 13.64 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 38.6% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Application Modernization Services Market Demand is Rising in North America Request Free Sample

The geographic landscape is shaped by varying paces of digital transformation journey, with mature markets focusing on advanced legacy replatforming and cloud-native application development. In contrast, emerging regions prioritize foundational IT infrastructure consulting and enterprise resource planning modernization.

The transition to cloud-native environments and the adoption of hybrid cloud strategies are common goals, enabling the use of real-time data analytics. Modernization efforts in critical sectors like healthcare EHR modernization and telecom network virtualization are widespread.

In North America, modernization of energy grid management software has led to a 15% improvement in grid stability.

The use of a software-defined data center and robust enterprise architecture planning are key to supporting these complex upgrades, including aerospace flight systems upgrades.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Enterprises are increasingly evaluating the cost of legacy system maintenance against the long-term benefits of microservices architecture. Key decisions revolve around how to modernize mainframe applications, a process fraught with challenges in large scale migration. A critical first step is understanding the risks of application modernization projects and choosing a cloud modernization partner with proven expertise.

- The rise of generative AI in code translation is lowering barriers, but a clear strategy for moving from on-premises to cloud is essential. The debate between a cloud native vs lift and shift approach depends on business objectives, with the former offering greater agility.

- Modernizing applications for digital sovereignty has become non-negotiable for regulated industries, forcing them to implement zero trust security in legacy systems. Measuring ROI of application modernization is now more sophisticated, moving beyond simple cost savings.

- For instance, in application modernization for financial services, success is also measured by a reduction in compliance-related incidents, with modernized platforms showing a 50% decrease in such events compared to their legacy counterparts. The impact of technical debt on business is well-documented, making application modernization best practices and integrating AI with legacy systems crucial.

- These services are no longer just for large corporations; application modernization services for smes are a growing segment. The role of devops in modernization, ensuring data integrity during cloud migration, and securing the software supply chain are all integral to a successful transformation.

What are the key market drivers leading to the rise in the adoption of Application Modernization Services Industry?

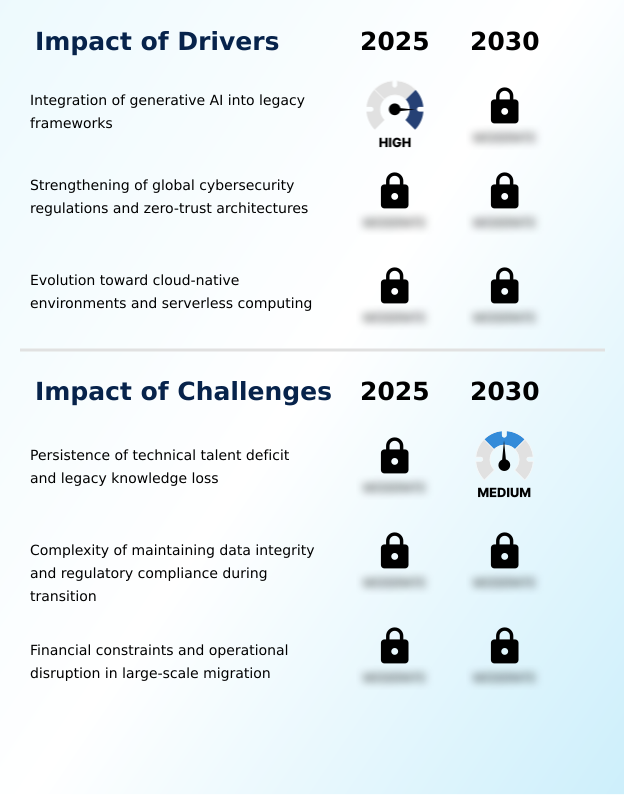

- The integration of generative AI into legacy frameworks is a key market driver, compelling enterprises to modernize their software stacks to remain competitive.

- Key market drivers include the widespread adoption of a containerization strategy and a cohesive multi-cloud strategy for enhanced flexibility. Enterprises are increasingly using AI-powered automation for mainframe migration and implementing multi-cloud managed services to streamline operations.

- The focus on a robust cybersecurity resilience framework is paramount, with DevOps integration and zero-trust security architecture becoming standard for mitigating risks in software supply chain security.

- The benefits of container orchestration are clear, as it aids in cloud migration risk management and provides effective disaster recovery solutions.

- This approach improves supply chain visibility, with early adopters reporting up to a 15% reduction in stock-out incidents, and ensures better IT service delivery while addressing regulatory compliance challenges.

What are the market trends shaping the Application Modernization Services Industry?

- The proliferation of generative AI in automated code conversion is a significant market trend, accelerating development cycles and transforming how organizations approach legacy system modernization.

- The market is witnessing a major trend in the use of generative AI code generation for automated code conversion, accelerating the shift from monolithic to microservices. This automated refactoring supports agile development methodologies and API-first design, enabling businesses to enhance customer experience.

- The adoption of low-code development platforms is also on the rise, addressing the IT talent deficit impact by allowing for faster development cycles. In e-commerce, the move toward a headless commerce architecture is gaining traction, with implementations showing a 30% improvement in page load times.

- This evolution requires effective change management in IT projects and the integration of application performance monitoring tools to facilitate data-driven decision making and support edge computing integration.

What challenges does the Application Modernization Services Industry face during its growth?

- The persistence of a technical talent deficit, coupled with the loss of legacy knowledge, presents a significant challenge to the growth of the application modernization services market.

- A primary challenge involves the complexity of legacy code refactoring and maintaining data integrity management during the transition to a microservices-based architecture. Ensuring data lineage requirements and cyber resilience act compliance adds significant overhead. Organizations must undertake business process reengineering and application portfolio optimization to manage these transformations effectively, with a growing focus on green computing metrics to address sustainability.

- The necessity for data sovereignty compliance often complicates digital platform integration, especially in financial services modernization and public sector digital transformation. Managing IT budget optimization while mitigating the IT skills gap and updating manufacturing execution systems remains a delicate balancing act for many firms. Projects often see a 20% budget overrun due to unforeseen complexities.

Exclusive Technavio Analysis on Customer Landscape

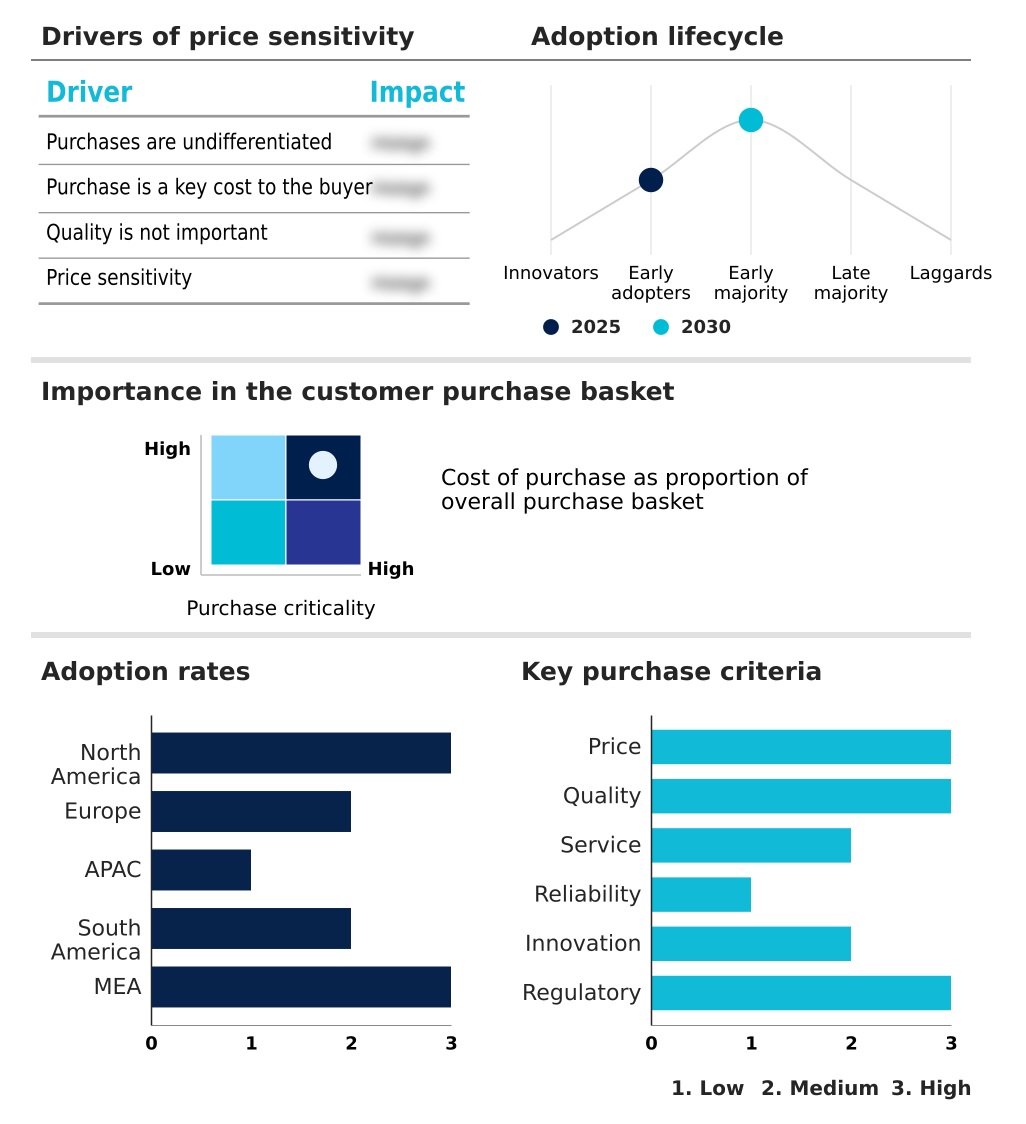

The application modernization services market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the application modernization services market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Application Modernization Services Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, application modernization services market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Accenture Plc - Delivers cloud-native transformation through legacy replatforming and AI-powered accelerators, focusing on portfolio rationalization and modern engineering to reduce technical debt and enhance agility.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Accenture Plc

- Atos SE

- Capgemini Service SAS

- Cisco Systems Inc.

- Cognizant Technology Solution

- Deloitte Touche Tohmatsu Ltd.

- DXC Technology Co.

- Ernst and Young Global Ltd.

- Fujitsu Ltd.

- HCL Technologies Ltd.

- IBM Corp.

- Infosys Ltd.

- LTIMindtree Ltd.

- NTT DATA Corp.

- Oracle Corp.

- PricewaterhouseCoopers LLP

- Tata Consultancy Services

- Tech Mahindra Ltd.

- Virtusa Corp.

- Wipro Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Application modernization services market

- In April 2025, a consortium of major financial institutions in North America announced the completion of a multi-year pilot program that leveraged automated code translation to move core banking functions into a vector-based database environment.

- In July 2025, the European Union began the full enforcement of the Cyber Resilience Act, which mandates that all digital products sold within the region must adhere to strict security-by-design principles throughout the product lifecycle.

- In August 2025, a consortium of major telecommunications providers in South America launched a regional edge-computing initiative designed to modernize the legacy customer portals of the firms to comply with local performance and data residency standards.

- In October 2025, a partnership between major energy utility providers in Northern Europe resulted in the successful migration of several legacy grid management systems to a cloud-native platform, allowing for better integration of renewable energy sources.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Application Modernization Services Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 307 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.2% |

| Market growth 2026-2030 | USD 24974.9 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 15.5% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Russia, Spain, China, India, Japan, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is driven by a strategic imperative to address technical debt reduction through a comprehensive cloud-native transformation. This involves the transition from monolithic to microservices, facilitated by AI-powered automation and generative AI code generation for automated code conversion and automated refactoring.

- A successful containerization strategy, alongside DevOps integration and agile development methodologies, is critical for legacy code refactoring and legacy system reengineering. Organizations are adopting hybrid cloud strategies and multi-cloud strategies, often with multi-cloud managed services, to optimize their application portfolio and achieve application portfolio rationalization.

- The modernization of IT infrastructure, including IT infrastructure upgrades and the shift to cloud-native environments and serverless models, is essential. Key boardroom decisions now focus on managing the transition to a zero-trust security architecture, ensuring cyber resilience act compliance and strengthening software supply chain security.

- This focus on security has led to a 30% reduction in vulnerability patching times for modernized applications. The adoption of green computing metrics is also influencing hybrid cloud environment designs and microservices-based architecture choices, reflecting a broader commitment to sustainability.

What are the Key Data Covered in this Application Modernization Services Market Research and Growth Report?

-

What is the expected growth of the Application Modernization Services Market between 2026 and 2030?

-

USD 24.97 billion, at a CAGR of 16.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud based, and On premises), Business Segment (Large enterprises, and Small and medium enterprises), End-user (BFSI, Retail and e-commerce, IT and telecom, Manufacturing, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of generative AI into legacy frameworks, Persistence of technical talent deficit and legacy knowledge loss

-

-

Who are the major players in the Application Modernization Services Market?

-

Accenture Plc, Atos SE, Capgemini Service SAS, Cisco Systems Inc., Cognizant Technology Solution, Deloitte Touche Tohmatsu Ltd., DXC Technology Co., Ernst and Young Global Ltd., Fujitsu Ltd., HCL Technologies Ltd., IBM Corp., Infosys Ltd., LTIMindtree Ltd., NTT DATA Corp., Oracle Corp., PricewaterhouseCoopers LLP, Tata Consultancy Services, Tech Mahindra Ltd., Virtusa Corp. and Wipro Ltd.

-

Market Research Insights

- The market dynamics are defined by a strategic pursuit of operational agility, compelling enterprises to prioritize application portfolio rationalization and adopt hybrid cloud environments. This transition supports a shift from capital expenditure vs operational expenditure models, with organizations that implement serverless models reporting up to a 40% reduction in infrastructure management costs.

- The focus on a robust cybersecurity resilience framework is also critical, as modern architectures enable firms to align with new regulatory compliance challenges more effectively than legacy systems. Adopting open-source frameworks has become a key strategy for avoiding vendor lock-in.

- Moreover, successful modernization projects demonstrate a clear return on investment, with some companies achieving a 2:1 improvement in their deployment frequency-to-failure ratio.

We can help! Our analysts can customize this application modernization services market research report to meet your requirements.

RIA -

RIA -