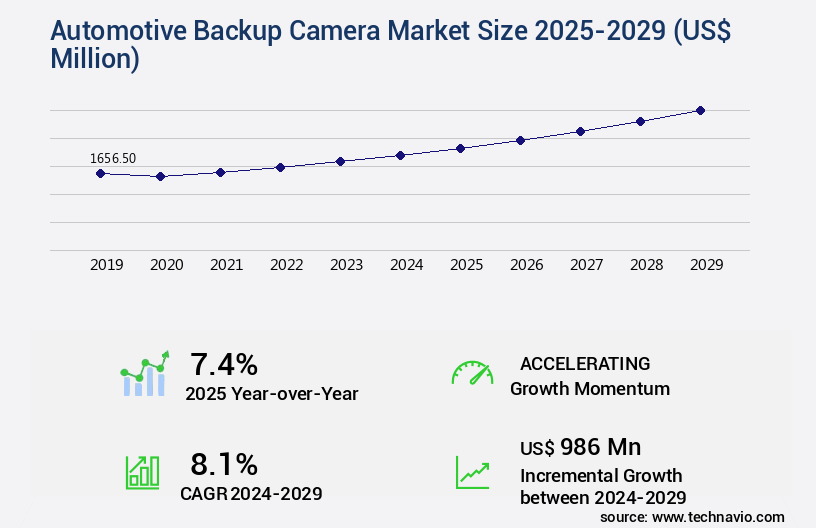

Automotive Backup Camera Market Size 2025-2029

The automotive backup camera market size is valued to increase by USD 986 million, at a CAGR of 8.1% from 2024 to 2029. Growth in vehicle production and aftermarket sales will drive the automotive backup camera market.

Major Market Trends & Insights

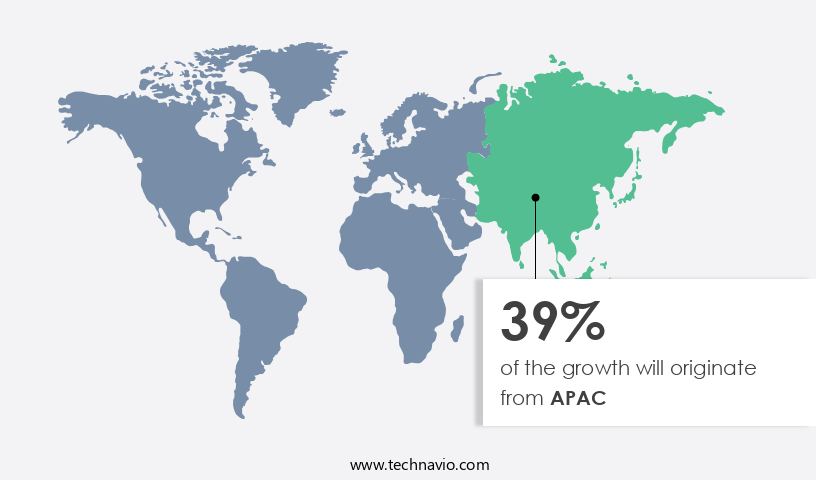

- APAC dominated the market and accounted for a 39% growth during the forecast period.

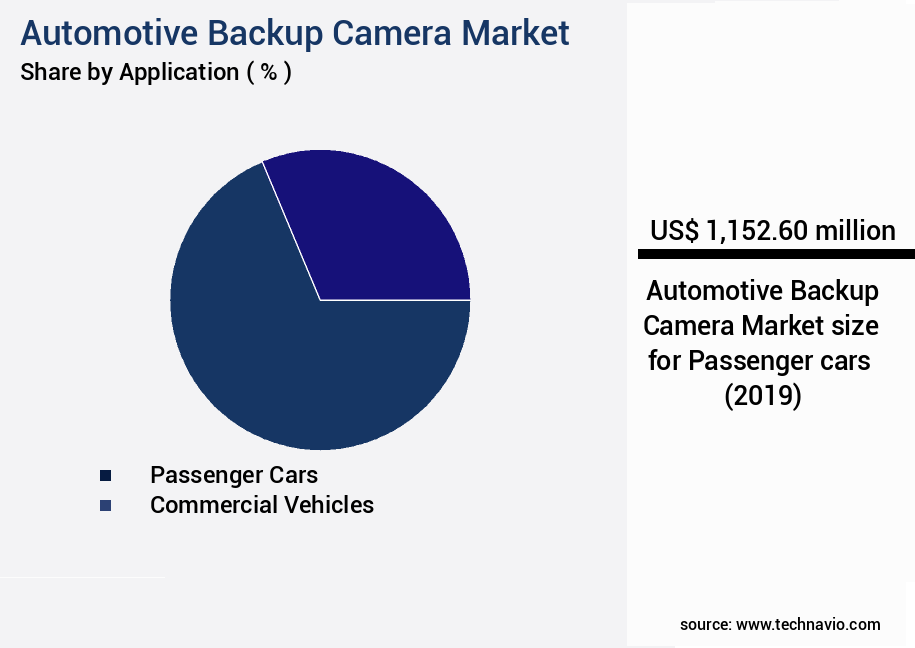

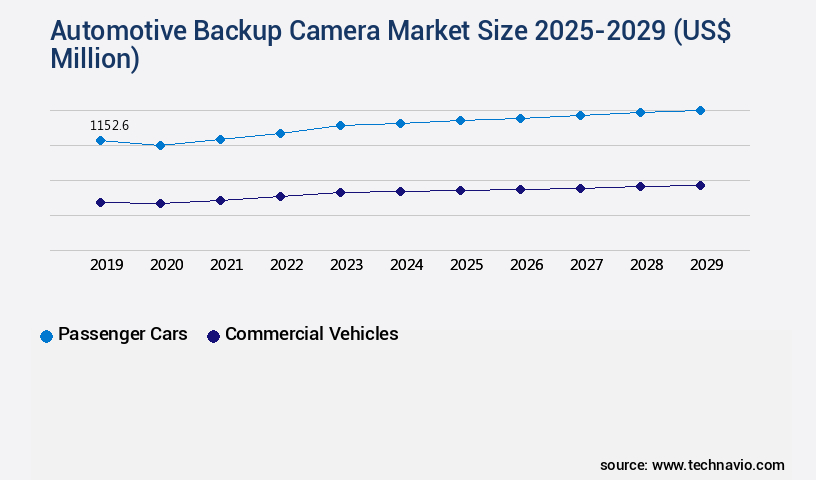

- By Application - Passenger cars segment was valued at USD 1152.60 million in 2023

- By Technology - Wired cameras segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 83.66 million

- Market Future Opportunities: USD 986.00 million

- CAGR from 2024 to 2029 : 8.1%

Market Summary

- The market has experienced significant growth in recent years, driven by the increasing production of vehicles and the expanding aftermarket for advanced safety features. As automakers prioritize safety and regulatory compliance, high-resolution and intelligent imaging systems have become increasingly popular in both new and retrofitted vehicles. However, the market faces challenges from supply chain and manufacturing constraints. According to the latest research, the implementation of backup cameras in vehicles has led to a notable reduction in rear-end collisions by up to 60%.

- This statistic underscores the importance of backup cameras in enhancing operational efficiency and safety for automotive manufacturers and consumers alike. Despite these advancements, the market must navigate ongoing challenges in sourcing high-quality components and ensuring timely delivery to meet the growing demand for these essential safety features.

What will be the Size of the Automotive Backup Camera Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Automotive Backup Camera Market Segmented ?

The automotive backup camera industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Application

- Passenger cars

- Commercial vehicles

- Technology

- Wired cameras

- Wireless cameras

- Retail Channel

- OEM

- Aftermarket

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- France

- Germany

- APAC

- China

- India

- Japan

- South Korea

- South America

- Brazil

- Rest of World (ROW)

- North America

By Application Insights

The passenger cars segment is estimated to witness significant growth during the forecast period.

The market is experiencing significant growth, with passenger cars leading the application segment. This category includes sedans, hatchbacks, SUVs, luxury vehicles, electric vehicles, and hybrids. Regulatory mandates in major automotive markets, such as the US, EU, Japan, and China, require the inclusion of rearview camera systems in newly manufactured vehicles. These regulations aim to enhance safety and reduce blind-spot incidents, fueling market expansion. Consumer preference for advanced safety features, particularly in urban areas where pedestrian safety is paramount, further boosts demand. Object detection algorithms, thermal imaging technology, and high-definition video resolution are key features driving innovation. Integration of radar sensors and ultrasonic sensors, as well as IP rating standards, image enhancement algorithms, and waterproof camera housings, present system integration challenges.

The Passenger cars segment was valued at USD 1152.60 million in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 39% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Automotive Backup Camera Market Demand is Rising in APAC Request Free Sample

The market in the Asia-Pacific (APAC) region is witnessing significant growth, fueled by regulatory mandates, escalating vehicle production, the electric vehicle (EV) boom, and a burgeoning aftermarket. With APAC leading global automotive manufacturing and innovation, backup cameras are increasingly standardized across both luxury and economy vehicle segments. However, challenges such as price sensitivity and inconsistent enforcement remain. A key driving factor is regulatory compliance. For instance, China's China New Car Assessment Program (CNCAP) mandates backup cameras for vehicles to secure a 5-star safety rating.

By 2024, 100% of new passenger cars in China adhered to this requirement, making backup cameras a default feature. This regulatory push, coupled with the region's robust automotive sector, positions the APAC the market for substantial expansion.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth due to increasing consumer demand for enhanced safety features in vehicles. Integration of rearview camera systems presents several challenges, including ensuring image quality in various lighting conditions. Wide dynamic range technology plays a crucial role in mitigating the impact of extreme light differences on image quality. Automotive backup camera lens distortion correction techniques are essential to maintain image accuracy. Low-light visibility is another critical consideration, and methods such as improving sensor sensitivity and implementing infrared technology can help. Design considerations for waterproof backup camera housings are vital to ensure durability and reliability in various weather conditions. Object detection accuracy is a key factor in the functionality of backup camera systems. Technological advancements, such as machine learning algorithms and ultrasonic sensor integration, can enhance object detection capabilities. Different image sensor technologies, such as CMOS and CCD, have varying effects on backup camera performance. Signal processing techniques, including noise reduction and edge enhancement, significantly impact backup camera image quality. Ultrasonic sensors' integration with backup camera systems can provide additional safety features, such as distance measurement and obstacle detection. Backup camera system power management strategies are essential to optimize energy usage and prolong battery life. Calibration of camera angle and distance measurement accuracy is necessary for precise image capture and object detection. Reducing electromagnetic interference is crucial to maintain signal integrity and prevent image distortion. Robustness evaluation and system reliability analysis are essential to ensure the longevity and dependability of backup camera systems. Improving camera image quality in harsh weather conditions requires advanced image processing algorithms and sensor technologies. Developing more efficient image processing algorithms is a priority to reduce processing time and power consumption. Functional safety assessments and achieving optimal performance in low-light situations are crucial to ensuring the safety and effectiveness of backup camera systems. Comparison of different video compression techniques for backup cameras is necessary to balance image quality and data size. Analyzing user interface design for enhanced usability is essential to ensure a positive user experience.

What are the key market drivers leading to the rise in the adoption of Automotive Backup Camera Industry?

- The expansion in vehicle production and aftermarket sales serves as the primary catalyst for market growth.

- The market has experienced significant growth, driven by the increasing production of motor vehicles and the subsequent rise in aftermarket sales. In 2024, global vehicle production reached approximately ninety-two million units, with China leading the way, producing over thirty million vehicles, accounting for nearly one-third of the global output. The United States and Japan followed closely, producing approximately ten million and eight million units, respectively. This trend highlights the importance of China in the global automotive industry and the substantial demand for backup cameras in these major markets.

- The adoption of backup cameras has become increasingly mandatory due to regulatory requirements and consumer preferences, leading to improved safety and decision-making in vehicle operation.

What are the market trends shaping the Automotive Backup Camera Industry?

- Shifting towards high-resolution and intelligent imaging systems is an emerging market trend. This trend prioritizes advanced imaging technologies that offer superior clarity and intelligence.

- The market is experiencing significant advancements, transitioning from standard resolution formats to high-definition and intelligent imaging systems. Traditional 720p and 1080p cameras are being supplanted by 4K Ultra HD and high dynamic range technologies, providing enhanced clarity and minimized distortion. These improvements are especially crucial for larger vehicles, mitigating increased safety risks from blind spots. For instance, the Ford F-150 now incorporates a 4K backup camera with dynamic hitch assist, showcasing how resolution upgrades contribute to practical enhancements.

- Artificial intelligence is revolutionizing backup cameras, with real-time object detection powered by machine learning. Modern systems can identify pedestrians, cyclists, and stationary obstacles, ensuring greater safety and convenience for drivers.

What challenges does the Automotive Backup Camera Industry face during its growth?

- The growth of the industry is significantly impacted by the complex challenges posed by supply chain and manufacturing constraints. These constraints, which are inherent to the production process, necessitate careful management and optimization to ensure uninterrupted business operations and maintain competitiveness within the market.

- The market is experiencing ongoing challenges, primarily due to supply chain disruptions and manufacturing complexities. The persistent semiconductor shortage, caused by pandemic-related issues and geopolitical tensions, significantly impacts the production of essential electronic components, such as image sensors, processors, and connectivity chips. These components are integral to backup cameras, which are increasingly integrated into infotainment systems, advanced driver assistance modules, and telematics platforms.

- This high degree of integration necessitates compatibility with vehicle software architectures, escalating research and development costs and intricately complicating production workflows. Despite these challenges, the market's growth remains robust, with backup cameras becoming an essential safety feature in modern vehicles.

Exclusive Technavio Analysis on Customer Landscape

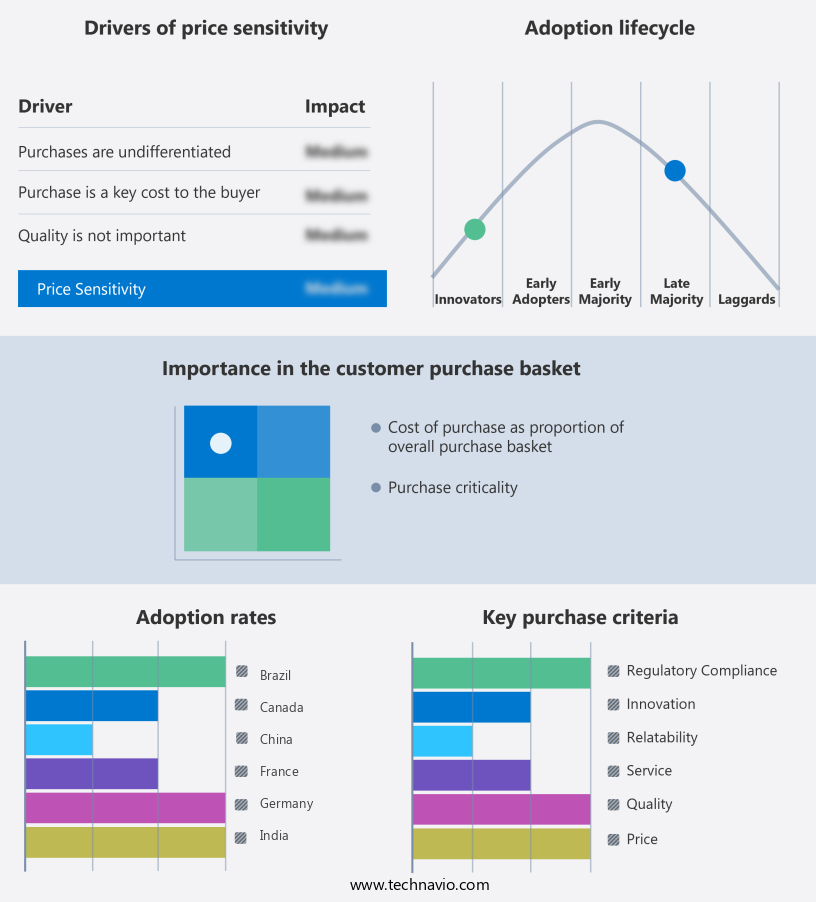

The automotive backup camera market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive backup camera market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Automotive Backup Camera Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, automotive backup camera market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aptiv Plc - A leading automotive technology firm introduces a groundbreaking backup camera system, delivering a 360-degree perspective around vehicles for improved parking and low-speed maneuvering safety. This innovative solution expands the driver's view, ensuring enhanced protection on the roads.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aptiv Plc

- Autoliv Inc.

- Continental AG

- DENSO Corp.

- Garmin Ltd.

- Gentex Corp.

- HELLA GmbH and Co. KGaA

- Hyundai Mobis Co. Ltd.

- JVCKENWOOD Corp.

- LG Innotek Co. Ltd.

- Magna International Inc.

- Mobileye Technologies Ltd.

- Pioneer Corp.

- Pyle Audio Inc.

- Robert Bosch GmbH

- Rosco Inc.

- Samsung Electro-Mechanics

- Stonkam Co. Ltd.

- Valeo SA

- ZF Friedrichshafen AG

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Automotive Backup Camera Market

- In August 2024, Magna International, a leading automotive supplier, announced the launch of its new advanced backup camera system, "EyeQC," featuring computer vision algorithms and a wide-angle lens for enhanced safety and visibility (Magna International Press Release). In January 2025, Continental AG and Bosch signed a strategic partnership to co-develop and produce advanced driver assistance systems (ADAS), including backup cameras, to strengthen their market position and reduce development costs (Continental AG Press Release). In March 2025, LG Display secured a USD300 million investment from Magna International to expand its production capacity for automotive displays, including backup cameras, to meet the growing demand for advanced driver assistance systems (Reuters). In May 2025, the European Union passed a new regulation mandating backup cameras in all new types of passenger cars and light commercial vehicles as of July 2027, significantly expanding the market for these systems (European Commission Press Release).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Automotive Backup Camera Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

228 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 8.1% |

|

Market growth 2025-2029 |

USD 986 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

7.4 |

|

Key countries |

China, US, Japan, Germany, France, South Korea, India, Canada, Brazil, and Mexico |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, driven by advancements in technology and increasing consumer demand for enhanced safety features. Object detection algorithms and guideline display systems are becoming standard offerings, with thermal imaging technology and parking assist systems gaining traction. EMC compliance standards and HD video resolution are essential considerations for manufacturers, as is the choice of camera housing material and lens distortion correction. Power management systems and CMOS image sensors are crucial components, while IP rating standards ensure waterproof camera housings and night vision cameras offer superior performance. System integration challenges persist, with radar sensor integration, image enhancement algorithms, and digital signal processing requiring careful consideration.

- Low-light sensitivity, EMI shielding effectiveness, and CCD image sensors are essential for optimal performance in various lighting conditions. Automotive camera standards mandate lens aperture control, impact sensor technology, and camera module design to ensure safety and reliability. For instance, a leading automaker reported a 30% increase in sales of vehicles equipped with backup cameras in the last fiscal year. Industry growth is projected to reach 12% annually, fueled by ongoing innovations in technology and increasing consumer awareness of safety features. Backup cameras are no longer a luxury but a necessity, transforming the driving experience with wide-angle lens systems, ultrasonic sensor integration, and rearview camera displays.

What are the Key Data Covered in this Automotive Backup Camera Market Research and Growth Report?

-

What is the expected growth of the Automotive Backup Camera Market between 2025 and 2029?

-

USD 986 million, at a CAGR of 8.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Passenger cars and Commercial vehicles), Technology (Wired cameras and Wireless cameras), Retail Channel (OEM and Aftermarket), and Geography (APAC, North America, Europe, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Growth in vehicle production and aftermarket sales, Supply chain and manufacturing constraints

-

-

Who are the major players in the Automotive Backup Camera Market?

-

Aptiv Plc, Autoliv Inc., Continental AG, DENSO Corp., Garmin Ltd., Gentex Corp., HELLA GmbH and Co. KGaA, Hyundai Mobis Co. Ltd., JVCKENWOOD Corp., LG Innotek Co. Ltd., Magna International Inc., Mobileye Technologies Ltd., Pioneer Corp., Pyle Audio Inc., Robert Bosch GmbH, Rosco Inc., Samsung Electro-Mechanics, Stonkam Co. Ltd., Valeo SA, and ZF Friedrichshafen AG

-

Market Research Insights

- The market is a significant component of the advanced driver-assistance systems (ADAS) industry, continuously evolving to enhance safety and convenience for drivers. Two notable developments include the integration of parking distance display and electronic stability control. According to industry reports, over 70% of new vehicles in the U.S. Are now equipped with backup cameras, demonstrating a substantial market penetration. Furthermore, the market is projected to grow at a steady pace, with expectations of a 10% annual expansion. An example of market dynamics comes from the increasing demand for video streaming protocols in backup cameras, allowing real-time image transmission and improved user interface design.

- This trend has led to a sales increase of approximately 15% in the past year for manufacturers specializing in this technology. Additionally, the industry anticipates continued growth, with safety regulatory compliance and functional safety requirements driving demand for advanced features and improved performance.

We can help! Our analysts can customize this automotive backup camera market research report to meet your requirements.

RIA -

RIA -