Automotive Filters Market Size 2024-2028

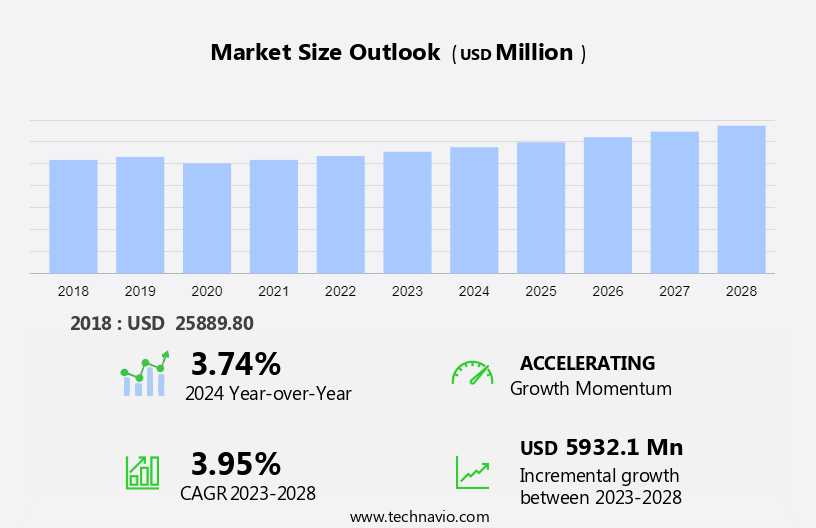

The automotive filters market size is forecast to increase by USD 5.93 billion at a CAGR of 3.95% between 2023 and 2028.

- The market is experiencing significant growth due to several key drivers. Emission regulations continue to tighten, leading to the increasing adoption of advanced filtration technologies such as particle filters and catalytic converters. The trend towards sustainability and fuel efficiency is also driving demand for novel filter materials, including nanofibers and synthetic fibers, which can improve fuel economy and reduce emissions.

- Additionally, the rising demand for electric vehicles (EVs) is expected to create new opportunities for filtration system providers, as EVs require specialized filters for battery cooling and air filtration. Overall, the market is poised for strong growth in the coming years, driven by these and other market trends.

Automotive Filters Market Analysis

How is this market segmented and which is the largest segment?-

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

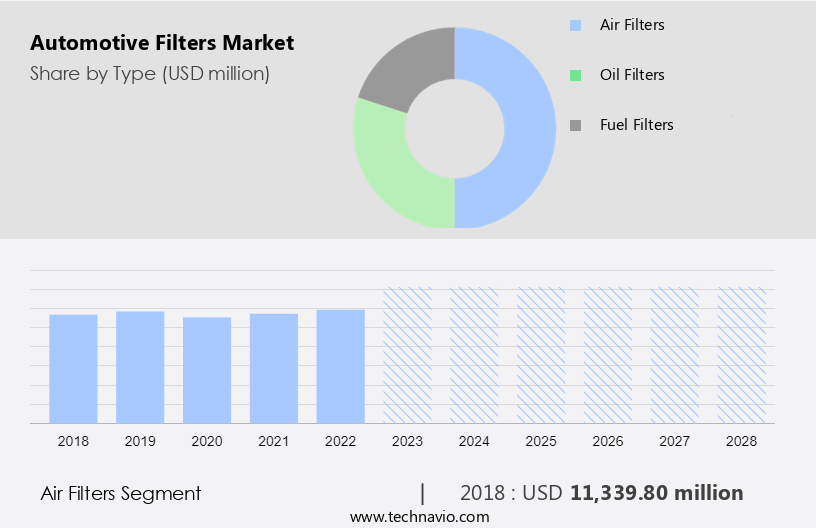

- Type

- Air filters

- Oil filters

- Fuel filters

- Distribution Channel

- Aftermarket

- OEM

- Geography

- APAC

- China

- India

- North America

- US

- Europe

- Germany

- UK

- South America

- Middle East and Africa

- APAC

By Type Insights

The air filters segment is estimated to witness significant growth during the forecast period. The market is experiencing significant growth due to the increasing demand for automobiles and the need to comply with stringent emissions regulations. Hydrocarbons (HC), nitrogen oxide (NOx), and carbon dioxide (CO2) are major pollutants that contribute to smog and poor air quality. To mitigate these emissions, automakers are integrating various types of filters in vehicles, including diesel particulate filters, gasoline particulate filters, and urea filters. In 2022, the passenger cars segment dominated The market due to the higher sales volume compared to commercial vehicles. Nitrogen oxides (NOx) are a significant concern for regulatory bodies, and the market for NOx filters is projected to grow at a strong rate.

Get a glance at the market share of various segments Request Free Sample

The Air filters segment accounted for USD 11.33 billion in 2018 and showed a gradual increase during the forecast period.

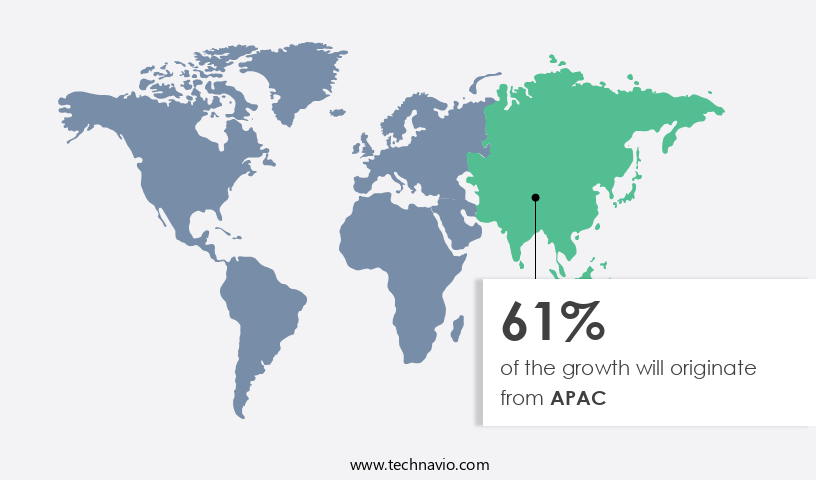

Will Increasing automobile adoption make APAC become the largest contributor to the Automotive Filters Market?

APAC is estimated to contribute 61% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing significant growth due to the increasing adoption of automobiles, particularly commercial vehicles, in countries such as China, India, and South Korea. China is currently the largest market for automotive filters in APAC, accounting for a substantial revenue share. The proliferation of new automotive Original Equipment Manufacturers (OEMs) in the region has led to an increase in automobile sales, thereby driving the demand for automotive filters. The production of automotive filters in APAC is contingent upon the manufacturing and sales of both passenger cars and commercial vehicles, as well as the escalating demand for export-oriented production of automotive components.

The primary focus of automotive filters in this market is on reducing harmful emissions, including hydrocarbons (HC), nitrogen oxides (NOx), and carbon dioxide (CO2). Technologies such as diesel particulate filters, gasoline particulate filters, and urea filters are increasingly being adopted to mitigate smog and NOx emissions in commercial vehicles.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Dynamics

- The market is witnessing significant growth due to the increasing demand for filtration media in various applications, including heavy duty engines for heavy trucks and battery electric vehicles (BEVs), as well as passenger cars running on alternative fuels. Synthetic media, electrostatic material, and particle filters are popular choices for filtration media in the automotive industry. Heavy duty engines require heavy-duty filters such as electrostatic filters for effective emission control, meeting greenhouse emission standards. In the case of BEVs and Plug-in Hybrid Electric Vehicles (PHEVs), EMI/EMC filters are essential for ensuring efficient power transmission and reducing electromagnetic interference. Air filters, oil filters, fuel filters, coolant filters, and dryer cartridges are crucial components for maintaining engine efficiency and vehicle longevity in the automobile sector.

- The adoption of novel filter materials, such as advanced ceramics and nanofibers, is expected to improve filtration efficiency and contribute to sustainability and fuel economy. Emission regulations continue to drive the demand for filtration technologies in the automotive industry, with a focus on reducing emissions and improving fuel efficiency. Catalytic converters and particle filters are essential components in meeting these regulations while ensuring optimal engine performance.

What are the key market drivers leading to the rise in adoption of Automotive Filters Market ?

Increasing demand for road transportation is the key driver of the market.

- The market is witnessing significant growth due to the increasing demand for filtration media in various automotive applications. Synthetic media, Electrostatic material, and other advanced filtration technologies are gaining popularity in the market. Heavy duty engines used in heavy trucks and battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) require efficient filtration systems for optimal engine performance and emissions reduction. Heavy-duty vehicles, particularly in emerging economies like China and India, are experiencing a wave in demand due to the growing preference for road transportation for last-mile delivery. In China, heavy trucks transporting cargo from Inner Mongolia to Beijing face heavy traffic congestion due to the limited availability of rail freight services.

- As a result, light commercial vehicles (LCVs), medium commercial vehicles (M-HCVs), and heavy commercial vehicles (H-HCVs) are extensively used for cargo transportation, leading to a higher demand for automotive filters. Moreover, the increasing adoption of advanced technologies in the automotive industry, such as EMI/EMC filters and dryer cartridges, is expected to further fuel the growth of the market.

What are the trends shaping the Automotive Filters Market?

Rising demand for multilayer filtration systems is the upcoming trend in the market.

- Automotive filters serve a vital function in safeguarding the efficiency and durability of automotive components by obstructing contaminants from accessing engines, transmissions, and vehicle cabins. Multilayer filters, in particular, employ multiple filtration stages with varying pore sizes, amplifying the total filtration effectiveness. These filters are proficient in capturing smaller particles and pollutants, thereby providing enhanced protection to essential engine components. The multilayer filtration setup enables the trapping of a more extensive array of contaminants prior to replacement, thereby diminishing maintenance frequency and costs for vehicle proprietors. Additionally, multilayer filters contribute to optimized engine performance and fuel economy by ensuring cleaner air and fluids flow through the engine.

- Synthetic media, Electrostatic material, and other advanced filtration technologies, including EMI/EMC filters and dryer cartridges, are increasingly being adopted in heavy-duty engines powering heavy trucks, battery electric vehicles (BEVs), and plug-in hybrid electric vehicles (PHEVs). These filters are essential for ensuring the reliable operation of these complex powertrains and meeting stringent emissions regulations.

What challenges does Automotive Filters Market face during the growth?

Rising demand for EVs is a key challenge affecting the market growth.

- The market is witnessing significant growth due to the increasing adoption of advanced filtration media, such as Synthetic media and Electrostatic material, in heavy duty engines of heavy trucks, buses, and battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). These filtration media enhance engine performance, improve fuel efficiency, and reduce emissions.

- The demand for heavy-duty filtration systems is increasing due to the stringent emission norms and regulations set by various governments. Moreover, the growing popularity of electric vehicles is driving the demand for EMI/EMC filters and dryer cartridges to ensure efficient charging and battery performance.The increasing awareness among consumers about the importance of filtration systems in maintaining engine health and enhancing vehicle performance is also fueling the market growth.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

A. Kayser Automotive Systems GmbH: The company offers automotive filters such as air filters with OBD interface and fuel filters.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- A. Kayser Automotive Systems GmbH

- Ahlstrom Holding 3 Oy

- ALCO Filters Ltd.

- Cummins Inc.

- DENSO Corp.

- Donaldson Co. Inc.

- ELOFIC INDUSTRIES Ltd.

- First Brands Group

- Ford Motor Co.

- Hengst SE

- MAHLE GmbH

- MANN HUMMEL International GmbH and Co. KG

- Parker Hannifin Corp.

- Purofil Auto India Pvt Ltd

- Robert Bosch GmbH

- Sogefi Spa

- Toyota Motor Corp.

- UFI filters SPA

- Valeo SA

- Zenith Auto Industries Pvt. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is witnessing significant growth due to the increasing focus on engine efficiency, vehicle longevity, and emission regulations. Filtration media, such as synthetic media and electrostatic material, are widely used in various types of automotive filters, including air filters, oil filters, fuel filters, coolant filters, and crankcase ventilation filters. Heavy duty engines in commercial vehicles, such as heavy trucks, buses, and construction equipment, require specialized filters like diesel particulate filters, gasoline particulate filters, and urea filters to meet stringent greenhouse emission standards. The automobile sector is also witnessing a shift towards battery electric vehicles (BEVs), plug-in hybrid vehicles (PHEVs), alternative fuels, and novel filter materials like nanofibers and synthetic fibers to reduce air pollution and improve fuel economy.

Automotive filters are essential for improving engine performance, reducing emissions, and ensuring human health. They help in trapping hydrocarbons (HC), nitrogen oxide (NOx), carbon dioxide (CO2), and other pollutants from the exhaust gases. The market for automotive filters is expected to grow significantly in the coming years due to the increasing demand for cleaner and more efficient transportation. The market is also driven by the growing popularity of passenger cars, including sedans, hatchbacks, SUVs, and crossovers, and the increasing focus on cabin air filtration and battery cooling filters in electric vehicles. Filter media technology continues to evolve, with new materials and designs being developed to improve filtration efficiency and reduce maintenance costs.

Some filters are now non-replaceable, while aftermarket filters offer cost-effective alternatives for vehicle owners. In conclusion, the market is a critical component of the global automotive industry, with a significant impact on engine performance, fuel efficiency, vehicle longevity, and sustainability. The market is expected to grow significantly in the coming years due to the increasing focus on emission regulations, alternative fuels, and the growing popularity of electric vehicles.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

175 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.95% |

|

Market growth 2024-2028 |

USD 5.93 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.74 |

|

Regional analysis |

APAC, North America, Europe, South America, and Middle East and Africa |

|

Performing market contribution |

APAC at 61% |

|

Key countries |

China, US, India, Germany, and UK |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

A. Kayser Automotive Systems GmbH, Ahlstrom Holding 3 Oy, ALCO Filters Ltd., Cummins Inc., DENSO Corp., Donaldson Co. Inc., ELOFIC INDUSTRIES Ltd., First Brands Group, Ford Motor Co., Hengst SE, MAHLE GmbH, MANN HUMMEL International GmbH and Co. KG, Parker Hannifin Corp., Purofil Auto India Pvt Ltd, Robert Bosch GmbH, Sogefi Spa, Toyota Motor Corp., UFI filters SPA, Valeo SA, and Zenith Auto Industries Pvt. Ltd. |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -