Automotive Variable Intake Air Control Valve Market Size 2024-2028

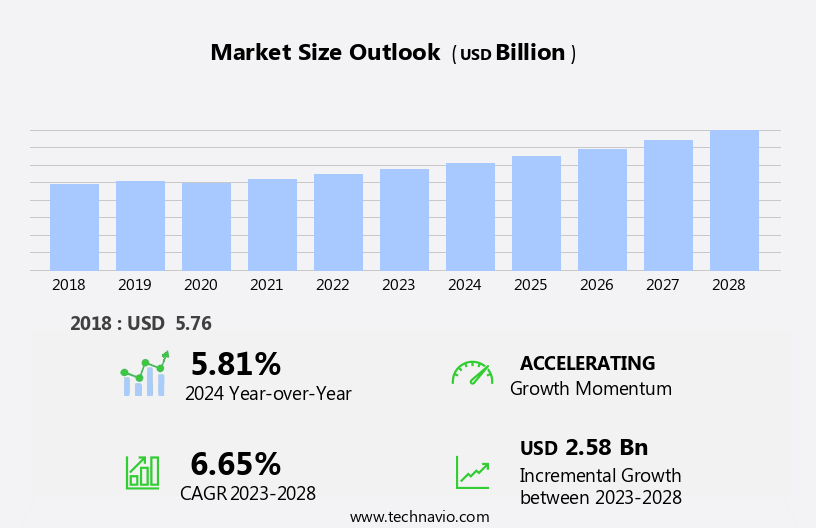

The automotive variable intake air control valve market size is forecast to increase by USD 2.58 billion at a CAGR of 6.65% between 2023 and 2028.

- The market is experiencing significant growth, driven by the increasing adoption of gasoline direct injection systems. This technology, which optimizes fuel combustion for improved engine performance and fuel efficiency, relies heavily on variable intake air control valves to manage the air-fuel mixture. Another trend shaping the market is the development of FreeValve engines, which utilize electronically controlled intake valves to optimize engine performance in real-time. Moreover, the burgeoning demand for electric vehicles (EVs) is creating new opportunities for the market. While EVs do not use traditional intake air control valves, the growing market share of these vehicles is driving research and development efforts to create more efficient and effective intake control systems for hybrid and plug-in hybrid vehicles.

- Companies seeking to capitalize on these trends and navigate market challenges must focus on innovating to meet evolving consumer demands and regulatory requirements. Additionally, strategic partnerships, mergers and acquisitions, and investments in research and development are essential for long-term success in this dynamic market.

What will be the Size of the Automotive Variable Intake Air Control Valve Market during the forecast period?

- The market is experiencing rapid acceleration, driven by technological advancements and the increasing adoption of advanced technologies in engine control systems. These innovations enable real-time adjustments to engine parameters, optimizing engine performance, efficiency, and emissions reduction. The market is witnessing significant growth due to the global shift towards fuel-efficient vehicles, electric vehicles, and eco-friendly automotive solutions. Manufacturing processes are evolving, incorporating lightweight materials and novel construction methods to improve durability and operating conditions. Emissions regulations continue to tighten, necessitating the integration of emissions control systems and the use of artificial intelligence in engine management. The middle class's growing preference for environmentally friendly norms further fuels market expansion.

- Automotive components, including variable intake air control valves, play a crucial role in engine efficiency and emissions management. Technological advancements in airflow management and engine design contribute to improved combustion processes and overall engine performance. As the industry dynamics evolve, the focus on connectivity, durability, and performance remains a priority for automotive solutions providers.

How is this Automotive Variable Intake Air Control Valve Industry segmented?

The automotive variable intake air control valve industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Application

- Passenger vehicles

- Commercial vehicles

- Type

- Solenoid valves

- Air operated valves

- Geography

- APAC

- China

- Japan

- Europe

- France

- UK

- North America

- US

- South America

- Middle East and Africa

- APAC

By Application Insights

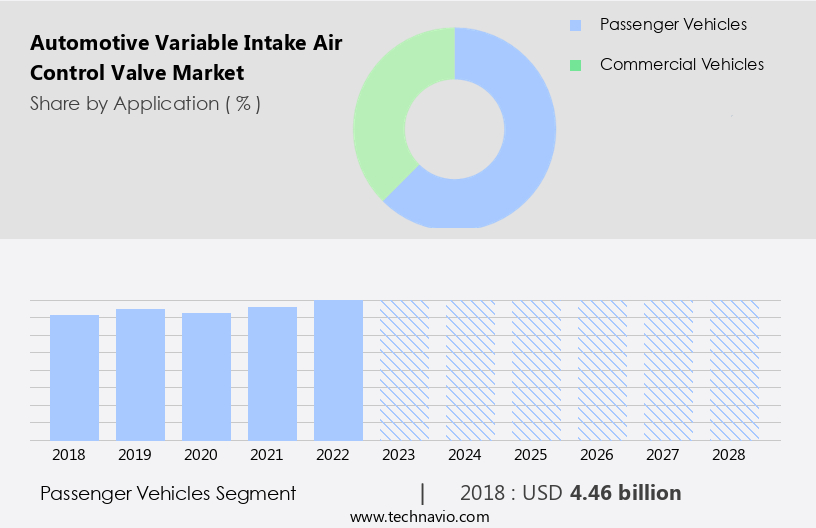

The passenger vehicles segment is estimated to witness significant growth during the forecast period.

The market experiences significant growth due to the increasing demand for clean transportation solutions and sustainable mobility. In the passenger vehicle segment, these valves play a crucial role in optimizing engine performance, fuel efficiency, and emission control. Manufacturers integrate advanced variable intake air control valve technologies to meet stringent emission regulations and fuel efficiency standards, making this market highly competitive. These valves adjust airflow into the engine based on operating conditions, enhancing overall vehicle performance. The focus on low-carbon transportation, hybrid car technology, and electric vehicle infrastructure further propels the market's growth. Additionally, the adoption of green automotive industry trends, such as eco-friendly car parts, advanced engine design, and lightweight vehicle design, contributes to the market's expansion.

Innovations in automotive design, emission reduction strategies, and connected car technology further fuel the market's growth. Sustainable manufacturing practices and smart mobility solutions are also key drivers, as the future of mobility increasingly s emission reduction and sustainability.

Get a glance at the market report of share of various segments Request Free Sample

The Passenger vehicles segment was valued at USD 4.46 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

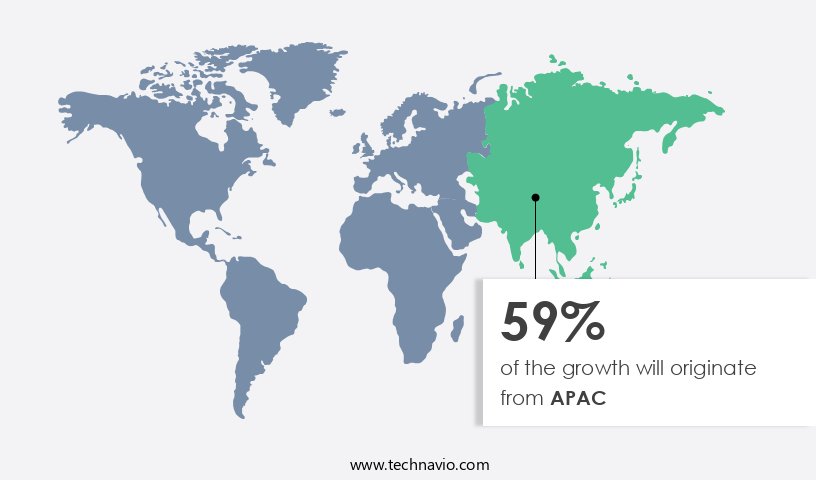

APAC is estimated to contribute 59% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in the Asia Pacific (APAC) region is driven by the increasing preference for clean and sustainable transportation solutions. With a focus on reducing vehicle emissions and promoting low-carbon transportation, the adoption of hybrid car technology, electric vehicle infrastructure, and alternative fuel vehicles is on the rise. India and China, in particular, account for a significant share of the market due to their large automotive production bases and the high demand for fuel-efficient vehicles. Consumers in these countries prioritize vehicles with advanced engine designs and emission control technology, making the automotive supply chain increasingly reliant on sophisticated solutions such as automotive variable intake air control valves.

Additionally, the next-generation automotive industry is witnessing innovation in areas such as autonomous driving technology, green automotive industry, and smart mobility solutions. Sustainable manufacturing practices and vehicle lifecycle analysis are also gaining importance as part of the global automotive trends. Overall, the market for automotive variable intake air control valves is expected to grow significantly during the forecast period, driven by the demand for fuel efficiency solutions, advanced engine technology, and eco-friendly car parts.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Automotive Variable Intake Air Control Valve Industry?

- Growing demand for gasoline direct injection systems is the key driver of the market.

- The automotive industry's focus on enhancing vehicle performance, fuel economy, and energy efficiency has led to the development of advanced fuel injection technologies, such as Gasoline Direct Injection (GDI). This system, also known as fuel-stratified injection (FSI) or spark-ignited direct injection (SIDI), atomizes and ignites fuel directly in the combustion chamber, increasing engine compression and resulting in greater efficiency. The integration of GDI with turbocharging and engine downsizing can potentially reduce fuel consumption and CO2 emissions by up to 10-15%.

- Strict emission norms in major markets, including North America and Europe, have compelled automotive Original Equipment Manufacturers (OEMs) to adopt GDI technology in their vehicles. This technology's adoption not only improves vehicle performance and fuel economy but also helps in reducing greenhouse gas emissions, making it a crucial component in the automotive industry's ongoing efforts towards sustainability.

What are the market trends shaping the Automotive Variable Intake Air Control Valve Industry?

- Development of FreeValve engines is the upcoming market trend.

- The introduction of FreeValve engines, which operate without a camshaft and use pneumatic, hydraulic, or electromagnetic actuators to control valves, is disrupting the traditional automotive industry. FreeValve engines, produced by Koenigsegg's business unit, offer several advantages over conventional engines, including increased torque by 47%, power by 45%, reduced fuel consumption by 15%, and emissions by 35%. These engines do not require automotive variable intake air control valves, leading to a decelerated growth in the global market. However, the superior efficiency and performance of FreeValve engines are anticipated to stimulate the demand for these valves as manufacturers seek to optimize engine performance in conventional engines.

- The benefits of improved torque, power, fuel efficiency, and emissions reduction are significant market drivers, making the market an essential component in the global automotive industry.

What challenges does the Automotive Variable Intake Air Control Valve Industry face during its growth?

- Increasing demand for EVs is a key challenge affecting the industry growth.

- The global market for Automotive Variable Intake Air Control Valves has gained significant traction due to the increasing adoption of electric vehicles (EVs) worldwide. Governments' emphasis on reducing carbon emissions and offering subsidies for EVs, coupled with the declining battery prices and the launch of cost-effective EV variants, have significantly boosted the demand for these vehicles. Furthermore, the expansion of EV charging infrastructure, rising consumer awareness, and partial or full bans on fuel-powered vehicles have also contributed to the market's growth.

- Notable markets for EVs include China, the US, Japan, Norway, and Germany. This trend is expected to continue as the world shifts towards sustainable energy and environment-friendly transportation solutions.

Exclusive Customer Landscape

The automotive variable intake air control valve market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the automotive variable intake air control valve market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, automotive variable intake air control valve market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BorgWarner Inc. - The company provides advanced automotive intake air control valves, featuring electronic throttle valves with DC motors, two-stage gear systems, non-contact position sensing, and fail-safe return springs. Aluminum bodies ensure durability and lightweight design. These innovative valves enhance engine performance and efficiency.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BorgWarner Inc.

- Continental AG

- DENSO Corp.

- Eagle Industry Co. Ltd

- Eaton Corp. Plc

- Hitachi Ltd.

- Mikuni Corp.

- Nidec Corp.

- Robert Bosch GmbH

- Rotex Automation Ltd.

- Standard Motor Products Inc.

- VOSS Automotive GmbH

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The automotive industry is undergoing a significant transformation as the global focus shifts towards cleaner and more sustainable transportation solutions. This transition is driven by various factors, including growing concerns over environmental sustainability, increasing adoption of electric vehicles (EVs), and advancements in technology. Variable intake air control valves (VICVs) play a crucial role in optimizing engine performance and fuel efficiency in modern vehicles. These valves adjust the amount of air that enters the engine based on driving conditions, allowing for improved combustion and reduced emissions. The market for VICVs is expected to grow significantly in the coming years due to several factors.

Firstly, the increasing demand for fuel efficiency and emission reduction strategies in the automotive industry is driving the adoption of advanced engine designs, which rely on VICVs to optimize performance. Moreover, the shift towards sustainable transportation and the growing popularity of electric and hybrid vehicles are also expected to boost the demand for VICVs. These vehicles require sophisticated solutions to manage their powertrains efficiently, and VICVs play a critical role in optimizing the performance of internal combustion engines used in hybrid vehicles. Another trend driving the growth of the VICV market is the increasing focus on lightweight vehicle design.

VICVs help reduce the weight of vehicles by eliminating the need for complex engine management systems, making them an attractive option for automakers looking to meet fuel efficiency regulations and reduce vehicle weight. Furthermore, the adoption of connected car technology and innovation in automotive manufacturing practices are also expected to create new opportunities for VICV suppliers. Connected cars generate vast amounts of data that can be used to optimize engine performance and fuel efficiency in real-time, making VICVs an essential component of these systems. In addition, the trend towards sustainable manufacturing practices in the automotive industry is expected to drive the adoption of VICVs.

These valves help reduce the carbon footprint of vehicle production by optimizing engine performance and reducing the need for excessive fuel consumption during the manufacturing process. The future of mobility is expected to be characterized by advanced engine technology, emission reduction strategies, and a focus on sustainability. VICVs are expected to play a crucial role in enabling these trends by optimizing engine performance, reducing emissions, and improving fuel efficiency. In , the market for variable intake air control valves is poised for significant growth in the coming years due to various factors, including the increasing demand for fuel efficiency and emission reduction strategies, the shift towards sustainable transportation, and the adoption of advanced engine designs and connected car technology.

The market is expected to be driven by innovation, sophistication, and a focus on sustainability, making it an exciting space for suppliers and investors alike.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 6.65% |

|

Market growth 2024-2028 |

USD 2.58 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

5.81 |

|

Key countries |

US, China, Japan, UK, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Automotive Variable Intake Air Control Valve Market Research and Growth Report?

- CAGR of the Automotive Variable Intake Air Control Valve industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the automotive variable intake air control valve market growth of industry companies

We can help! Our analysts can customize this automotive variable intake air control valve market research report to meet your requirements.

RIA -

RIA -