Bancassurance Market Size 2026-2030

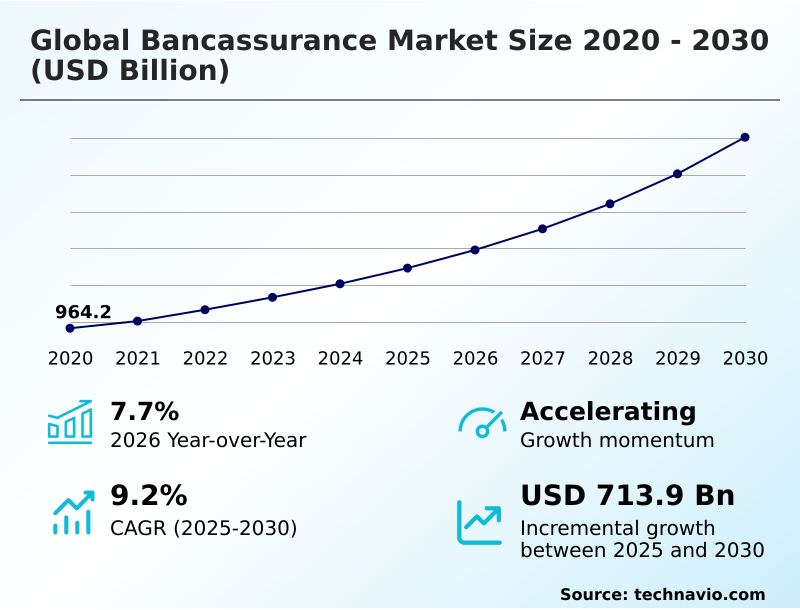

The bancassurance market size is valued to increase by USD 713.9 billion, at a CAGR of 9.2% from 2025 to 2030. Accelerated digital transformation and API Integration will drive the bancassurance market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 46.7% growth during the forecast period.

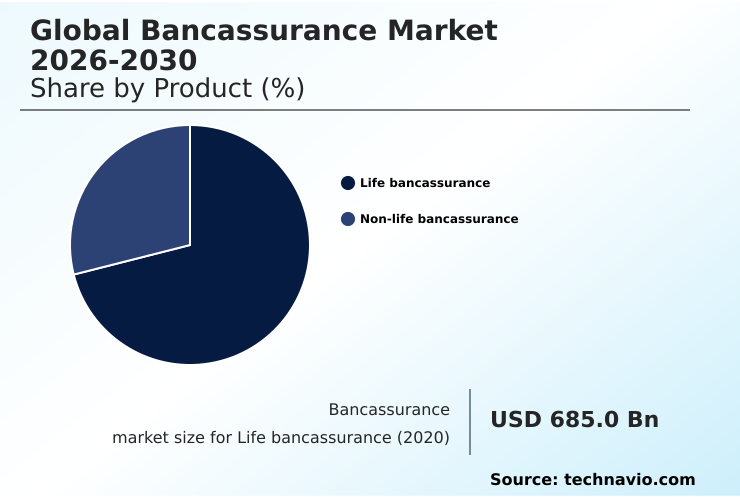

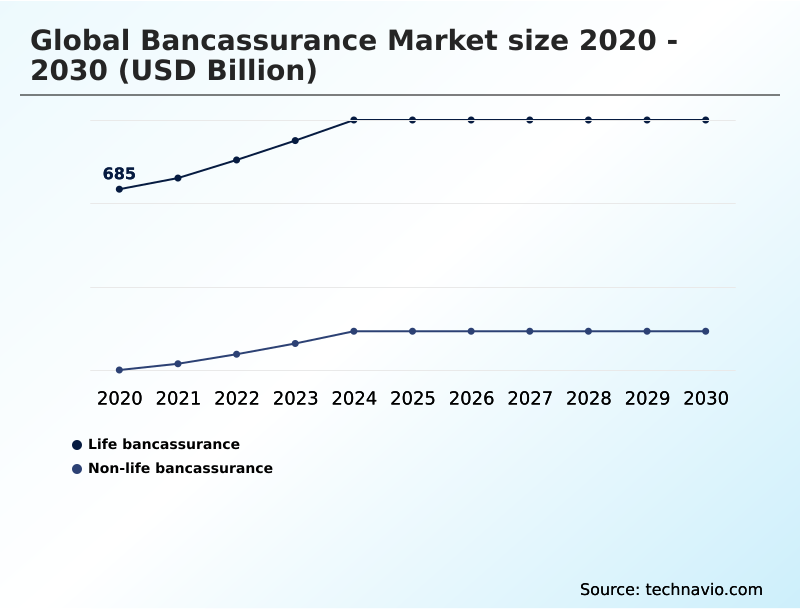

- By Product - Life bancassurance segment was valued at USD 840.3 billion in 2024

- By Type - Pure distributor segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1041.8 billion

- Market Future Opportunities: USD 713.9 billion

- CAGR from 2025 to 2030 : 9.2%

Market Summary

- The bancassurance market is undergoing a significant evolution, shifting from traditional product sales to a more integrated, advisory-led model. This transition is propelled by accelerated digital transformation, which enables the seamless embedding of insurance products into banking platforms through API ecosystems.

- Institutions are leveraging predictive analytics and generative AI to achieve hyper-personalization, offering contextual insurance products at key customer life moments. For example, a bank's system can analyze transactional data to identify a customer's recent home purchase and automatically trigger a tailored home insurance offer through their mobile banking application, streamlining the user experience and improving conversion rates.

- However, this deep integration presents challenges, including the need to modernize legacy infrastructure and navigate complex regulatory compliance and data sovereignty issues. Success hinges on bridging the cultural misalignment between banking and insurance to ensure a cohesive, customer-centric approach that enhances customer lifetime value and drives fee-based revenue while managing underwriting risk effectively.

What will be the Size of the Bancassurance Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Bancassurance Market Segmented?

The bancassurance industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Product

- Life bancassurance

- Non-life bancassurance

- Type

- Pure distributor

- Joint venture

- Excusive partnership

- Financial holding

- End-user

- Personal

- Business

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- France

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- UAE

- Saudi Arabia

- South Africa

- Rest of World (ROW)

- APAC

By Product Insights

The life bancassurance segment is estimated to witness significant growth during the forecast period.

The life bancassurance segment is driven by the integration of wealth management and insurance protection, encompassing products like term life, whole life, endowment plans, and unit-linked insurance plans.

A key driver is the trust customers place in banks for long-term financial planning and retirement planning.

Banks utilize a data-driven approach and customer relationship management systems to identify life events that trigger the need for insurance, such as marriage or mortgage approval, allowing for timely product positioning.

This strategic use of predictive analytics for contextual insurance offers enhances the customer lifetime value.

This segment accounts for nearly 70% of total premiums, reflecting the importance of investment-linked products and the demographic shift toward an aging population in developed economies, which fuels demand for retirement solutions.

This advice-led engagement model is supported by a seamless customer journey.

The Life bancassurance segment was valued at USD 840.3 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 46.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Bancassurance Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the bancassurance market is characterized by a distinct contrast between mature and emerging regions.

APAC is the primary growth engine, projected to contribute over 45% of the market's incremental growth, with its expansion rate being nearly 25% higher than that of North America.

This is fueled by a significant protection gap and rising demand for takaful insurance and microinsurance products delivered via digital channels. In Europe, the focus is on optimizing existing partnerships and adhering to strict regulations like the insurance distribution directive.

North America is seeing increased adoption of open architecture models to offer more choice.

This regional divergence requires tailored strategies, from offering simple credit-linked products in developing markets to sophisticated investment-linked products and managing fiduciary standards in developed ones, all while leveraging regtech solutions to ensure compliance.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global bancassurance market 2026-2030 is increasingly complex, shaped by a confluence of technological and regulatory pressures. Executives are evaluating the impact of APIs on bancassurance to determine the best path for digital transformation in insurance distribution, a process complicated by the need for overcoming legacy systems in finance.

- A key debate centers on the choice between joint venture vs exclusive partnership models, each with different implications for managing third-party risk in fintech partnerships. The role of AI in insurance personalization is paramount, as firms strive for hyper-personalization with predictive analytics to enhance customer lifetime value in bancassurance.

- Concurrently, generative AI use cases in bancassurance are being explored to improve the customer journey in digital banking. However, these advancements are constrained by significant regulatory challenges in bancassurance integration and pressing data sovereignty issues for global banks.

- Strategies for reducing bancassurance conduct risk are critical, as is the integration of regtech solutions for bancassurance compliance, which can reduce manual audit efforts by over 50%.

- Furthermore, understanding trends in embedded insurance products and the drivers of non-life bancassurance growth are essential for developing effective bancassurance strategies for emerging markets, where open banking impact on insurance sales and ESG integration in insurance products are becoming vital differentiators.

What are the key market drivers leading to the rise in the adoption of Bancassurance Industry?

- Accelerated digital transformation, coupled with deep API integration, is a key driver of growth in the bancassurance market.

- Market growth is primarily fueled by the accelerated adoption of digital transformation and the integration of open banking standards. This technological shift enables banks to offer hyper-personalized insurance recommendations, reducing client acquisition costs by up to 35%.

- A second major driver is the rising demand for customized wealth management and retirement planning solutions, especially for mass-affluent clients. This is prompting the design of hybrid investment-linked products that address both financial security and environmental social governance priorities.

- Finally, strategic government support and financial inclusion initiatives are expanding the market, with regulators encouraging the use of know your customer and anti-money laundering technology to streamline processes, which has cut onboarding times by half in some jurisdictions.

What are the market trends shaping the Bancassurance Industry?

- The accelerated integration of embedded insurance solutions is a primary market trend. This is largely facilitated by the development of sophisticated API ecosystems connecting banking and insurance platforms.

- Key trends are reshaping the market, centered on accelerated digital transformation and the expansion of digital wealth platforms. The integration of embedded insurance through sophisticated API ecosystems creates a seamless customer journey, with contextual offers at the point of sale improving conversion rates by over 200% compared to traditional methods.

- Hyper-personalization, driven by predictive analytics, allows for dynamic pricing models and bespoke product bundles, leading to a 25% uplift in customer retention. This shift toward holistic financial advice is also evident in the expansion into wealth management and retirement planning, with a focus on longevity risk and legacy planning.

- The adoption of a consultative approach and an advice-led engagement model is replacing outdated sales-push tactics, supported by the move toward a super-app environment.

What challenges does the Bancassurance Industry face during its growth?

- Escalating regulatory compliance burdens and data sovereignty complexities present a key challenge to the growth of the bancassurance industry.

- Significant challenges constrain market growth, led by escalating regulatory compliance and data sovereignty complexities. Adhering to divergent rules from banking and insurance authorities can increase operational costs by up to 20%.

- A second barrier is legacy infrastructure inertia, where the technical debt of outdated core banking systems clashes with the need for a modern user experience, causing over 50% of API integration projects to face significant delays. This creates friction and a disjointed digital claims portal.

- The third critical challenge is the strategic cultural misalignment and sales force capability gaps between banking and insurance, leading to conduct risk and low penetration rates. Overcoming these issues requires substantial investment in training and new third-party risk management frameworks.

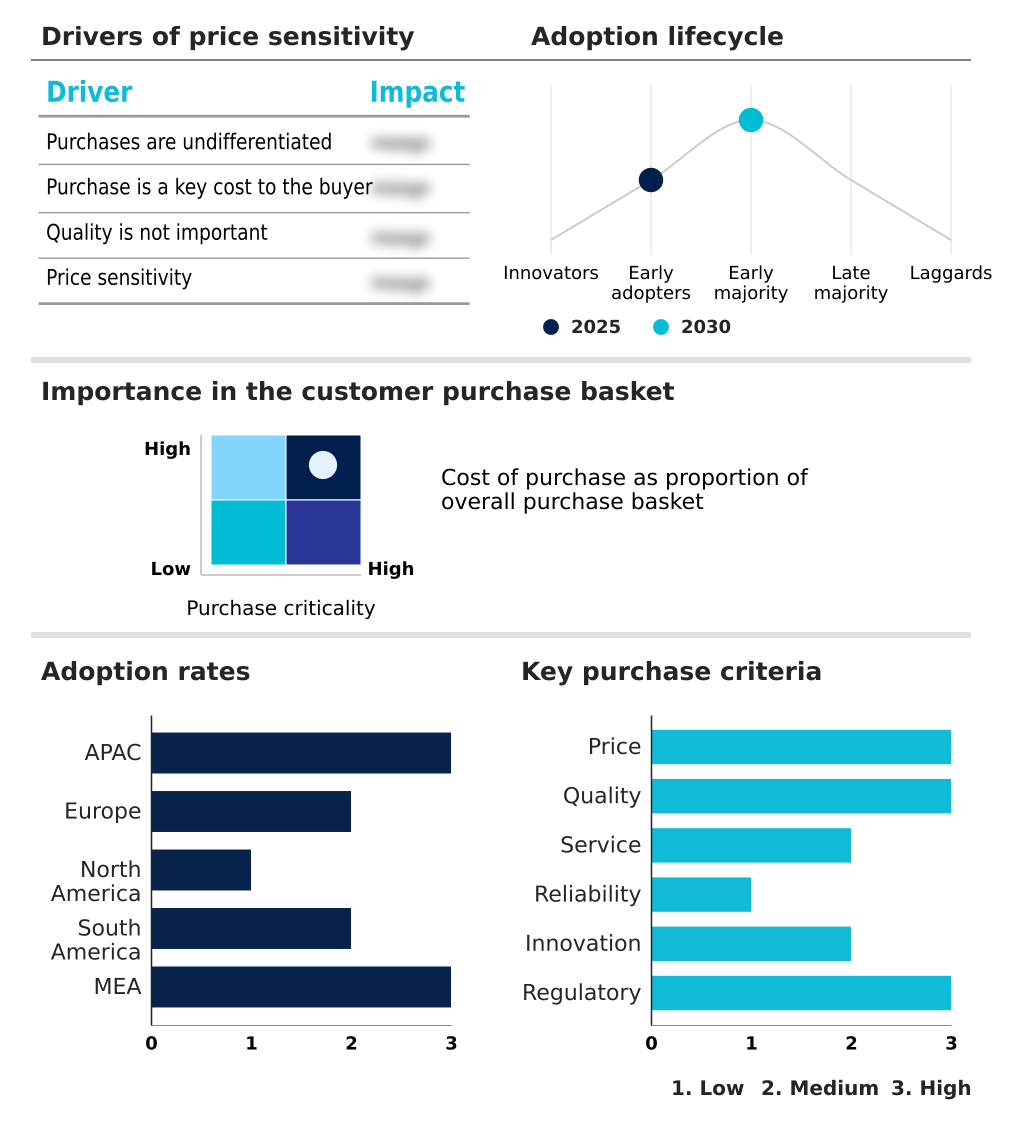

Exclusive Technavio Analysis on Customer Landscape

The bancassurance market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bancassurance market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Bancassurance Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, bancassurance market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABN AMRO Group NV - Key offerings focus on integrating life, non-life, and income protection insurance directly into primary banking and private wealth management channels to enhance client financial security.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABN AMRO Group NV

- American Express Co.

- ANZ Banking Group Ltd.

- AXA Group

- Banco Bradesco SA

- Banco Santander SA

- Barclays Bank Plc

- Citigroup Inc.

- CNA Financial Corp.

- Credit Agricole SA

- Credit Mutuel group

- HSBC Holdings Plc

- ING Groep NV

- Intesa Sanpaolo Spa

- Lloyds Banking Group Plc

- Metlife Inc.

- Nordes Bank Abp

- Wells Fargo and Co.

- Yes Bank Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Bancassurance market

- In March 2025, JPMorgan Chase announced a strategic expansion of its digital bancassurance capabilities by integrating a proprietary generative AI engine across its North American mobile platform to automate customized insurance offers.

- In May 2025, Allianz and Unicredit unveiled a pan-European initiative to offer a new suite of climate-resilient investment-linked insurance products targeting mass-affluent clients in Germany and Italy.

- In November 2024, HSBC announced an upgrade to its digital wealth platforms in Hong Kong, integrating enhanced insurance planning tools directly into its mobile banking application to help customers visualize protection gaps.

- In September 2024, DBS Bank expanded its AI-driven financial planning tool, utilizing advanced algorithms to analyze customer cash flow patterns and automatically recommend tailored insurance coverage amounts.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Bancassurance Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 301 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.2% |

| Market growth 2026-2030 | USD 713.9 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.7% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, US, Canada, Mexico, Brazil, Argentina, Colombia, UAE, Saudi Arabia, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The bancassurance market is defined by a strategic shift toward technology-led distribution and hyper-personalization. The core of this evolution is the use of embedded insurance and API ecosystems, enabling financial institutions to move beyond simple fee-based revenue models. Boardroom decisions now center on investments in predictive analytics and generative AI to create dynamic pricing models and deliver contextual insurance.

- This data-driven approach, leveraging open banking standards, facilitates the sale of life bancassurance and non-life bancassurance products like credit-linked products and unit-linked insurance plans. Success depends on choosing the right operating structure, whether a pure distributor model, a joint venture model, or an exclusive partnership under a financial holding company.

- These models must manage underwriting risk while enhancing customer lifetime value. Navigating complex regulatory compliance, data sovereignty, and fiduciary standards requires advanced regtech solutions.

- Institutions that successfully address cultural misalignment and overcome legacy infrastructure, achieving a 60% reduction in policy issuance times, will gain a significant competitive advantage in offering sophisticated wealth management and retirement planning solutions through an open architecture.

What are the Key Data Covered in this Bancassurance Market Research and Growth Report?

-

What is the expected growth of the Bancassurance Market between 2026 and 2030?

-

USD 713.9 billion, at a CAGR of 9.2%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Life bancassurance, and Non-life bancassurance), Type (Pure distributor, Joint venture, Excusive partnership, and Financial holding), End-user (Personal, and Business) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Accelerated digital transformation and API Integration, Escalating regulatory compliance and data sovereignty complexities

-

-

Who are the major players in the Bancassurance Market?

-

ABN AMRO Group NV, American Express Co., ANZ Banking Group Ltd., AXA Group, Banco Bradesco SA, Banco Santander SA, Barclays Bank Plc, Citigroup Inc., CNA Financial Corp., Credit Agricole SA, Credit Mutuel group, HSBC Holdings Plc, ING Groep NV, Intesa Sanpaolo Spa, Lloyds Banking Group Plc, Metlife Inc., Nordes Bank Abp, Wells Fargo and Co. and Yes Bank Ltd.

-

Market Research Insights

- Market dynamics are shaped by a strategic push toward a seamless customer journey, driven by mobile banking applications and digital wealth platforms. Institutions are leveraging know your customer data and anti-money laundering frameworks to refine cross-selling opportunities, with some achieving a 35% higher attachment rate for insurance on new loans through integrated digital disclosure tools.

- This advice-led engagement, a departure from traditional sales, focuses on holistic financial advice and longevity risk management. The adoption of environmental social governance criteria is also influencing product design, with sustainable offerings seeing 15% faster uptake among mass-affluent clients.

- As a result, the super-app environment is becoming a key battleground, where a superior user experience directly impacts customer retention and profitability.

We can help! Our analysts can customize this bancassurance market research report to meet your requirements.

RIA -

RIA -