Wealth Management Market Size 2026-2030

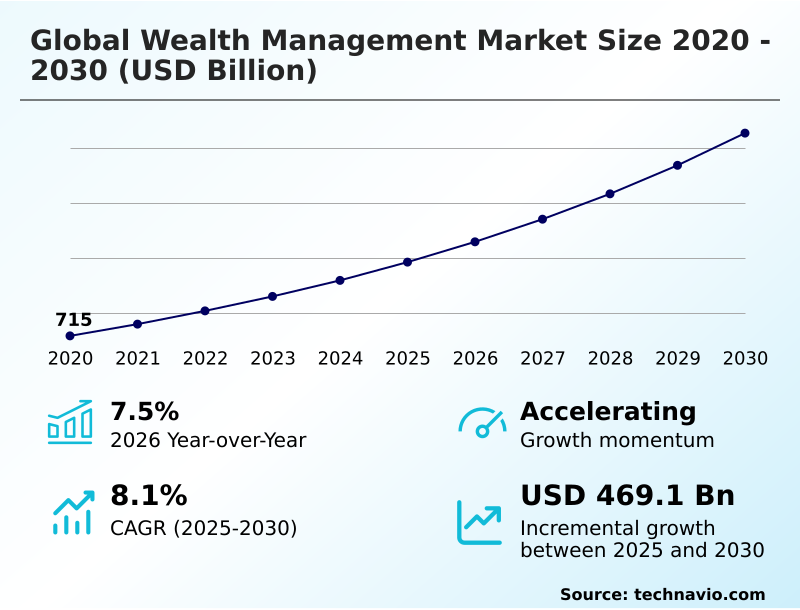

The wealth management market size is valued to increase by USD 469.1 billion, at a CAGR of 8.1% from 2025 to 2030. Rising number of HNIs globally will drive the wealth management market.

Major Market Trends & Insights

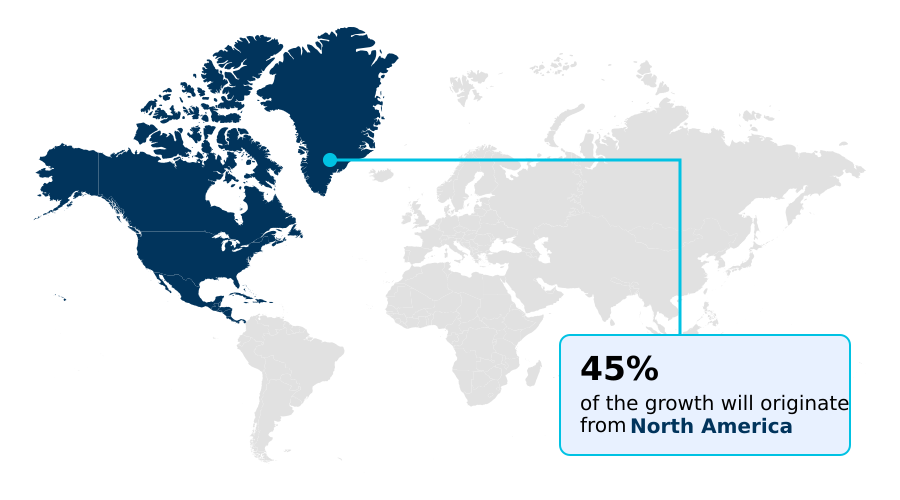

- North America dominated the market and accounted for a 44.7% growth during the forecast period.

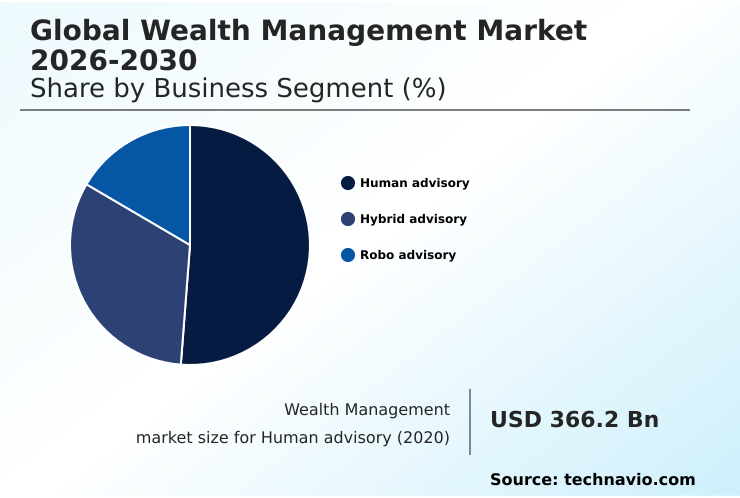

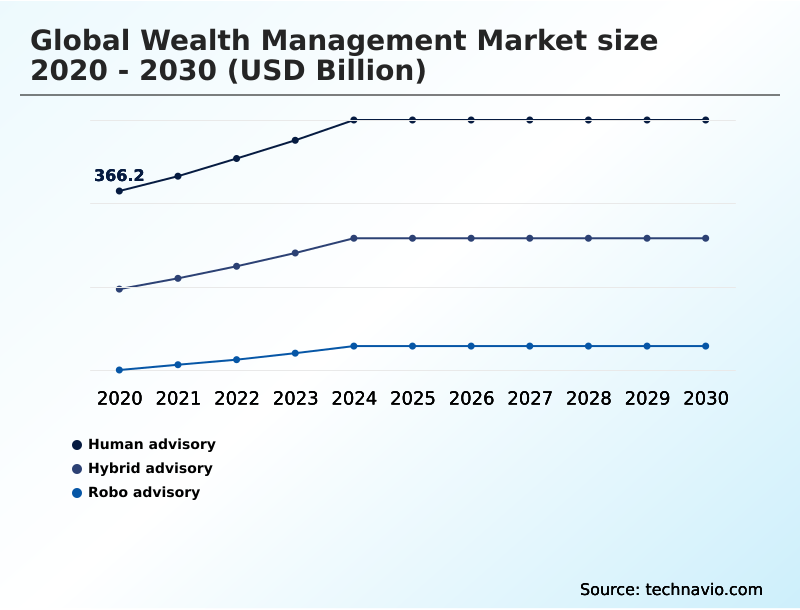

- By Business Segment - Human advisory segment was valued at USD 464.5 billion in 2024

- By End-user - Banks segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 737.3 billion

- Market Future Opportunities: USD 469.1 billion

- CAGR from 2025 to 2030 : 8.1%

Market Summary

- The wealth management market is undergoing a significant structural transformation, driven by technological integration and evolving client expectations. Firms are moving beyond traditional advisory to provide hyper-personalized services at scale, increasingly leveraging unified client platforms that consolidate diverse financial data.

- The deployment of generative ai is becoming instrumental in this shift, enabling advisors to automate complex tasks and focus on high-value strategic guidance. For instance, an advisory firm can utilize an integrated platform to model a client's complete financial lifecycle, simulating outcomes based on various market conditions, tax implications, and personal goals in real time.

- This enhances operational efficiency and allows for proactive, data-driven decision-making. The industry is also contending with challenges such as fee compression and the need for robust cybersecurity measures.

- To remain competitive, participants are focusing on delivering holistic solutions that encompass not just investment management but also comprehensive financial wellness, adapting to the demands for transparency and digital-first engagement from a new generation of investors.

What will be the Size of the Wealth Management Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Wealth Management Market Segmented?

The wealth management industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Business segment

- Human advisory

- Hybrid advisory

- Robo advisory

- End-user

- Banks

- Trading and exchange firms

- Investment management firms

- Brokerage firms

- Others

- Service

- Asset management

- Portfolio management

- Others

- Geography

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Europe

- Germany

- UK

- France

- South America

- Brazil

- Argentina

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Business Segment Insights

The human advisory segment is estimated to witness significant growth during the forecast period.

The human advisory segment is adapting through holistic life-goal orchestration, especially for managing intergenerational wealth transfer. Advisors now leverage sophisticated platforms providing private market access and tools for cross-border tax treatments, enabling them to deliver high-conviction advice.

The integration of low-code ai tools and embedded finance strategies facilitates the creation of customized portfolios incorporating active fixed-income and smart beta products. This evolution supports complex digital asset management and multi-jurisdictional regulatory compliance, addressing client needs for geographic diversification.

By using data-driven esg assessment, advisors are also managing systematic withdrawal plans more effectively, with top-tier firms demonstrating client retention rates exceeding 95%. This approach increasingly involves planning for digital executors, reflecting the modern complexities of wealth.

The Human advisory segment was valued at USD 464.5 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Wealth Management Market Demand is Rising in North America Get Free Sample

The geographic landscape is shifting as firms adopt new strategies to meet diverse regional demands. In North America, the platformization of asset strategies is enabling the delivery of active outcome-oriented solutions.

In Europe, semi-liquid evergreen fund structures are gaining traction, while separately managed accounts and direct indexing are preferred for customization. The emphasis on financial model interoperability facilitates the seamless integration of systematic investment plans and mobile-centric financial tools.

Firms in APAC are seeing a 30% faster adoption of such platforms.

Meanwhile, in the Middle East, a focus on sharia-compliant wealth management and discretionary portfolio management is expanding the market for specialized financial products, including esg-compliant portfolios and impact investing, often accessed through cross-border investment platforms that ensure auditable provenance.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The wealth management market is rapidly evolving due to several interconnected dynamics. The rise of ai-augmented advisors for wealth management is changing service delivery, while a strong focus on sustainable investing in wealth management reflects new investor priorities. Key technological advances in wealth management are enabling diversified wealth management service offerings that increasingly include alternative investments in wealth portfolios.

- These changes are fueled by the rising high net worth individuals globally, though the fintech company growth impact creates a more competitive environment. This necessitates a focus on personalized digital client experiences to mitigate pricing pressure on wealth managers.

- The market is segmenting, with robo advisory for retail investors gaining share, while hybrid advisory models for affluents and traditional human advisory for ultra-high-net-worth clients continue to be refined. The banks role in wealth management is shifting, as are the strategies for trading firms in a wealth ecosystem and investment management firms strategies.

- The brokerage firms advisory evolution toward holistic planning is notable. Innovations in asset management product innovation and portfolio management hyper-personalization are critical. This includes advanced solutions for estate planning for digital assets and tax planning for mobile hnw is.

- Firms are also strengthening compliance for cross-border wealth and integrating private markets into portfolios to meet demand, navigating the impact of regulation on advisory. Ultimately, the expanded use of ai for investment decision-making is central to the ongoing digital transformation in private banking, reducing time-to-insight by more than half compared to legacy methods.

What are the key market drivers leading to the rise in the adoption of Wealth Management Industry?

- The rising number of high-net-worth individuals globally is a key driver propelling market growth.

- Market growth is propelled by the deployment of advanced technology to enhance client engagement and operational efficiency. The adoption of enterprise-grade ai systems is enabling the creation of unified client platforms that serve as a unified client brain for advisors.

- These platforms utilize predictive analytics and generative ai to power ai copilots that assist with complex scenario modeling and provide conversational user interfaces.

- This technological push is also facilitating an open banking framework, which supports the proliferation of democratized investment tools. The integration of ai-driven compliance programs within these systems is essential for managing the complexities of cross-border transactions.

- Deployment of such platforms has shown to increase cross-selling opportunities by 35%, while the use of ai copilots for scenario modeling reduces report generation time by over 50%.

What are the market trends shaping the Wealth Management Industry?

- Technological advances are reshaping the industry, representing a significant upcoming trend in the wealth management market.

- Key market trends are centered on balancing high-touch services with scalable technology. The industry is seeing a sophisticated blend of human-centric advisory and high-velocity technological integration, driven by persistent fee compression. The deployment of agentic artificial intelligence is moving beyond experimentation to become a core operational layer ai for wealth lifecycle management.

- This enables firms to offer institutional-grade infrastructure and democratize access to alternative assets, including private equity and hedge funds. Firms utilizing this approach have reported a 25% reduction in client onboarding time.

- Furthermore, the development of digital asset custodial frameworks is crucial for providing lifestyle-related financial advice and executing real-time investment actions, enhancing efficiency by automating up to 40% of routine middle-office tasks.

What challenges does the Wealth Management Industry face during its growth?

- Intense pressure on the pricing structures of wealth management companies presents a key challenge affecting industry growth.

- Firms face significant challenges in modernizing front-office operations to meet demands for digital-first engagement while managing costs. Integrating advanced tools for real-time portfolio analysis, such as those for esg-integrated investing and cross-border wealth structuring, strains IT budgets.

- The operational complexities are significant; for instance, integrating multi-asset capabilities for the tokenization of real-world assets and fractional exchange-traded funds can increase IT spending by 15-20%. The need to offer ai-augmented advisory services and specialized family office services further complicates the technology stack. Addressing the private savings gap through open finance initiatives requires robust yet flexible platforms.

- Furthermore, the demand for digital-first engagement requires firms to enhance cybersecurity, raising compliance costs by an average of 10% annually.

Exclusive Technavio Analysis on Customer Landscape

The wealth management market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the wealth management market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Wealth Management Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, wealth management market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ameriprise Financial Inc. - Delivering financial planning and investment advisory solutions tailored to address the comprehensive needs of individuals and institutional clients.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ameriprise Financial Inc.

- Banco Santander SA

- Bank of America Corp.

- Bank of New York Mellon Corp.

- Barclays PLC

- Citigroup Inc.

- DBS Group Holdings Ltd.

- HSBC Holdings Plc

- Jones Financial Companies LLLP

- JPMorgan Chase and Co.

- Lombard Odier Group

- Morgan Stanley

- Nomura Holdings Inc.

- Northern Trust Corp.

- Pictet Group

- Raymond James Financial Inc.

- The Charles Schwab Corp.

- The Goldman Sachs Group Inc.

- UBS Group AG

- Wells Fargo and Co.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Wealth management market

- In October 2025, HSBC Private Bank unveiled its Wealth Intelligence platform, an in-house tool leveraging large language models to provide advisors with real-time, customized investment advice.

- In January 2026, The UK's Financial Conduct Authority finalized the Consumer Composite Investments regime, set to replace the previous PRIIPs framework, offering product manufacturers greater flexibility in customer communications.

- In February 2026, Nuveen reached a definitive agreement to acquire Schroders plc for approximately $13.5 billion, creating a global asset management entity with nearly $2.5 trillion in assets under management.

- In May 2025, The UAE and the United States announced an AI Acceleration Partnership, a move designed to catalyze deep technological cooperation and foster innovation in AI applications within the financial services sector.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Wealth Management Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 310 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.1% |

| Market growth 2026-2030 | USD 469.1 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.5% |

| Key countries | US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, Germany, UK, France, Italy, Spain, The Netherlands, Brazil, Argentina, Chile, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market is undergoing a structural pivot defined by high-velocity technological integration and a strategic shift toward alternative assets like private equity and hedge funds. The democratization of private markets is being realized through institutional-grade infrastructure, including semi-liquid evergreen fund structures that make non-traditional investments accessible.

- This evolution is powered by agentic artificial intelligence and enterprise-grade ai systems, which facilitate everything from predictive analytics to ai-driven compliance programs for complex cross-border transactions and multi-jurisdictional regulatory compliance. Firms are building unified client platforms to deliver a seamless omnichannel client experience, leveraging generative ai for front-office operations and real-time portfolio analysis.

- The move toward platformization of asset strategies supports active outcome-oriented solutions, with separately managed accounts and direct indexing offering deep personalization. Technology is also enabling the tokenization of real-world assets and the management of tokenized assets, on-chain cash, and fractional exchange-traded funds through advanced multi-asset capabilities with auditable provenance.

- In a key boardroom-level decision, firms are prioritizing financial model interoperability to support this ecosystem. This technological adoption enables a 15% improvement in the efficiency of portfolio rebalancing and supports holistic life-goal orchestration, which is crucial for managing intergenerational wealth transfer and providing high-conviction advice.

What are the Key Data Covered in this Wealth Management Market Research and Growth Report?

-

What is the expected growth of the Wealth Management Market between 2026 and 2030?

-

USD 469.1 billion, at a CAGR of 8.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Business Segment (Human advisory, Hybrid advisory, and Robo advisory), End-user (Banks, Trading and exchange firms, Investment management firms, Brokerage firms, and Others), Service (Asset management, Portfolio management, and Others) and Geography (North America, APAC, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, APAC, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Rising number of HNIs globally, Pressure on pricing structure of wealth management companies

-

-

Who are the major players in the Wealth Management Market?

-

Ameriprise Financial Inc., Banco Santander SA, Bank of America Corp., Bank of New York Mellon Corp., Barclays PLC, Citigroup Inc., DBS Group Holdings Ltd., HSBC Holdings Plc, Jones Financial Companies LLLP, JPMorgan Chase and Co., Lombard Odier Group, Morgan Stanley, Nomura Holdings Inc., Northern Trust Corp., Pictet Group, Raymond James Financial Inc., The Charles Schwab Corp., The Goldman Sachs Group Inc., UBS Group AG and Wells Fargo and Co.

-

Market Research Insights

- The market is being reshaped by a focus on comprehensive wealth lifecycle management to counter persistent fee compression. Key strategies include developing digital asset custodial frameworks for real-time investment actions and offering lifestyle-related financial advice through operational layer ai. The use of ai copilots for advanced scenario modeling is becoming standard.

- Firms are deploying democratized investment tools with conversational user interfaces, all powered by a unified client brain that integrates with the broader open banking framework. This shift enables enhanced family office services with a focus on esg-integrated investing and complex cross-border wealth structuring to address the private savings gap.

- An emphasis on open finance supports digital-first engagement, with ai-augmented advisory services becoming crucial. Firms adopting these strategies report up to a 20% increase in client engagement and a 30% reduction in administrative overhead.

We can help! Our analysts can customize this wealth management market research report to meet your requirements.

RIA -

RIA -