Battery Raw Materials Market Size 2026-2030

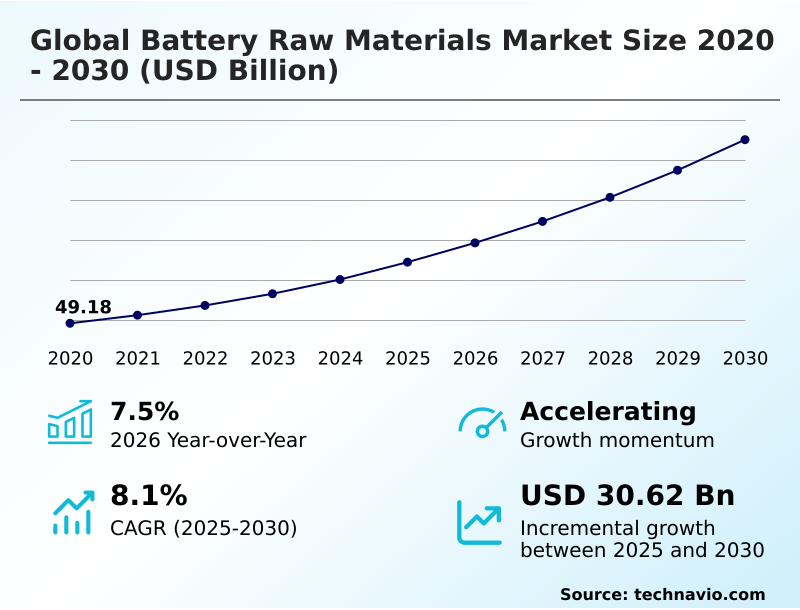

The battery raw materials market size is valued to increase by USD 30.62 billion, at a CAGR of 8.1% from 2025 to 2030. Global policy mandates and accelerated electrification of transport will drive the battery raw materials market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 46.8% growth during the forecast period.

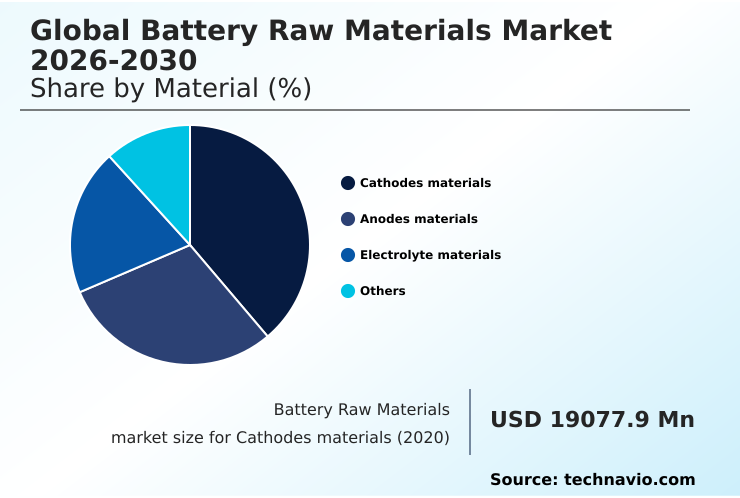

- By Material - Cathodes materials segment was valued at USD 23.84 billion in 2024

- By Application - Lead-acid battery segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 45.90 billion

- Market Future Opportunities: USD 30.62 billion

- CAGR from 2025 to 2030 : 8.1%

Market Summary

- The battery raw materials market is undergoing a period of intense transformation, driven by the global transition to electrification. The unprecedented demand for key minerals such as lithium, nickel, and cobalt is compelling a structural realignment of supply chains.

- A central theme is the strategic pivot from transactional procurement to deep-seated partnerships and vertical integration, where automotive OEMs are directly investing in mining and refining to de-risk production pipelines. For instance, an automaker might secure a long-term offtake agreement for lithium carbonate to hedge against extreme price volatility, a move critical for maintaining stable EV pricing and production schedules.

- This landscape is further shaped by technological diversification, with lithium iron phosphate (LFP) chemistries gaining ground for their cost and safety benefits, altering the demand profile for specific metals. Concurrently, geopolitical tensions are fostering resource nationalism and a push for regionalized supply networks, challenging the established global trade flows.

- The industry also grapples with intense ESG scrutiny, making ethical sourcing and the development of a circular economy through recycling essential for long-term operational viability and market acceptance. This dynamic environment requires market participants to navigate complex trade policies, technological shifts, and sustainability mandates.

What will be the Size of the Battery Raw Materials Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Battery Raw Materials Market Segmented?

The battery raw materials industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

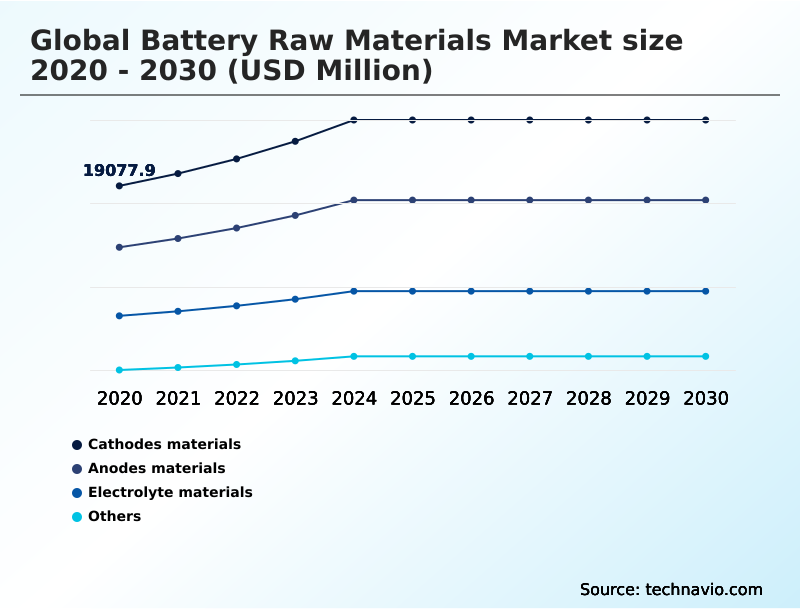

- Material

- Cathodes materials

- Anodes materials

- Electrolyte materials

- Others

- Application

- Lead-acid battery

- Lithium-ion battery

- Others

- End-user

- Secondary batteries

- Primary batteries

- Geography

- APAC

- China

- South Korea

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- France

- UK

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Material Insights

The cathodes materials segment is estimated to witness significant growth during the forecast period.

The market is segmented by material, with cathodes representing the most critical segment.

The performance of cathode active materials (CAM) dictates battery cost and energy density, with a notable industry split between high-purity nickel chemistries like nickel-manganese-cobalt (NMC) and iron-based alternatives.

Ensuring ethical sourcing standards for inputs like battery-grade cobalt is paramount, driven by battery passport regulation. Advanced hydrometallurgical recycling is emerging as a crucial source of secondary raw materials, with facilities demonstrating over 95% recovery rates.

Other segments include anodes, where silicon-carbon composites are being developed to boost capacity, and electrolytes, where compounds like lithium hexafluorophosphate (LiPF6) are essential for ionic conductivity and overall cell stability.

The Cathodes materials segment was valued at USD 23.84 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 46.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Battery Raw Materials Market Demand is Rising in APAC Get Free Sample

The geographic landscape is defined by strategic realignment. APAC continues to dominate midstream anode material graphitization and downstream processing capacity, but resource nationalism impacts are forcing diversification.

In contrast, North America and Europe are rapidly building regional supply chains, guided by policies like the critical raw materials act to mitigate geopolitical supply risk.

This has spurred massive capital expenditure in mining and refining, with a focus on developing local sources of nickel sulphate and spodumene concentrate.

For instance, investments in North American projects aim to increase domestic processing by over 40% in the coming years.

Technologies like high-pressure acid leaching (HPAL) in Indonesia and advanced raw material traceability systems are becoming standard, ensuring feedstock security across these evolving regional hubs.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the battery raw materials market now revolves around a complex matrix of interconnected factors, as highlighted by an lfp vs nmc cathode material cost analysis, which often dictates OEM platform choices. The long-term outlook is heavily influenced by solid-state battery raw material requirements, pushing R&D toward novel materials.

- Concurrently, advancements in black mass recycling technology are becoming central to supply strategies, with some firms reporting recovery rates over 20% higher than older methods, thereby enhancing the circular economy models for ev batteries. However, significant headwinds persist, including geopolitical risks in cobalt supply chains and graphite anode supply chain vulnerabilities.

- The impact of ira on battery material sourcing is forcing a regionalization of supply, while regulatory hurdles for new mine development continue to delay projects. Automaker investment in upstream mining is a direct response to these pressures, aiming to improve supply chain resilience for critical minerals.

- Debates over direct lithium extraction vs solar evaporation and the sustainability of lithium brine extraction reflect intense esg factors in raw material procurement. The price volatility effects on battery oems are profound, complicating capital investment for greenfield mining projects and highlighting the logistical challenges in mineral transport.

- Ultimately, technological diversification in battery chemistries, such as sodium-ion battery commercial viability and overcoming challenges in nickel laterite processing, will determine the market's future structure.

What are the key market drivers leading to the rise in the adoption of Battery Raw Materials Industry?

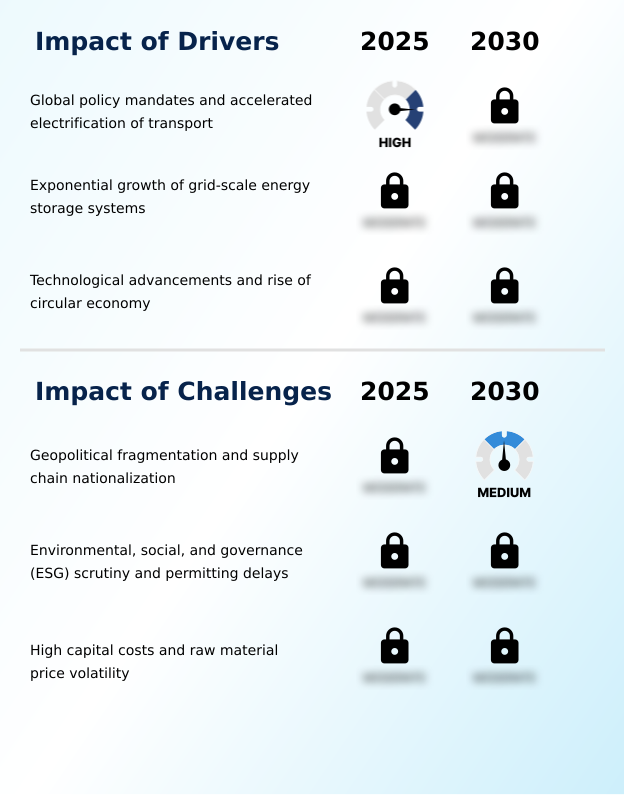

- Accelerated transport electrification, propelled by stringent global policy mandates, serves as a primary driver for market expansion and raw material demand.

- Technological advancement and the expansion of energy storage systems (ESS) are major market drivers.

- The rapid deployment of grid-scale energy storage is creating massive demand for specific chemistries like lithium iron phosphate (LFP), which is favored for its stability and cost-effectiveness.

- The risk of technological obsolescence is pushing R&D into diverse areas, including sodium-ion battery chemistry and advanced chemistry cells.

- The development of solid-state electrolytes promises enhanced safety and energy density, while innovations in direct lithium extraction (DLE) can improve lithium recovery efficiency by up to 40% compared to conventional methods.

- The demand for fast-charging battery materials and certain rare earth elements for specialized applications further diversifies the raw material requirements, fueling growth across multiple sub-segments.

What are the market trends shaping the Battery Raw Materials Industry?

- A strategic shift toward vertical integration is reshaping the market, as industry players increasingly pursue supply chain localization to secure upstream resources.

- A dominant market trend is the aggressive pursuit of supply chain localization and vertical integration. Companies are investing heavily in downstream processing capacity to convert raw minerals into high-value chemicals like lithium hydroxide and synthetic graphite. This strategic shift is designed to secure a closed-loop supply chain, reducing reliance on volatile global markets.

- As part of this, offtake agreement strategies are becoming more sophisticated, often involving direct equity stakes in mining operations. This aligns with national industrial goals, such as regional critical minerals strategy frameworks.

- Investments in urban mining infrastructure are also accelerating, with new facilities for black mass processing capable of recovering over 90% of materials, including essentials like polyvinylidene fluoride (PVDF), bolstering domestic supply.

What challenges does the Battery Raw Materials Industry face during its growth?

- The market's growth trajectory is constrained by geopolitical fragmentation and the rising trend of supply chain nationalization, which introduces supply uncertainty.

- The market faces significant challenges from geopolitical supply risk and the rising tide of resource nationalism impact, which can disrupt feedstock security. Navigating ESG compliance in mining has become a critical hurdle, with stringent permitting delays stalling projects and increasing capital expenditure in mining. For example, new mines can face approval timelines 50% longer than a decade ago.

- Price volatility hedging remains a persistent issue for both producers and consumers. Furthermore, technological hurdles in processes like high-pressure acid leaching (HPAL) for nickel extraction present operational risks.

- Ensuring a stable supply of intermediate products like mixed hydroxide precipitate (MHP) and low-carbon nickel is essential, but market fragmentation and trade barriers complicate procurement strategies, creating a complex operating environment for all participants.

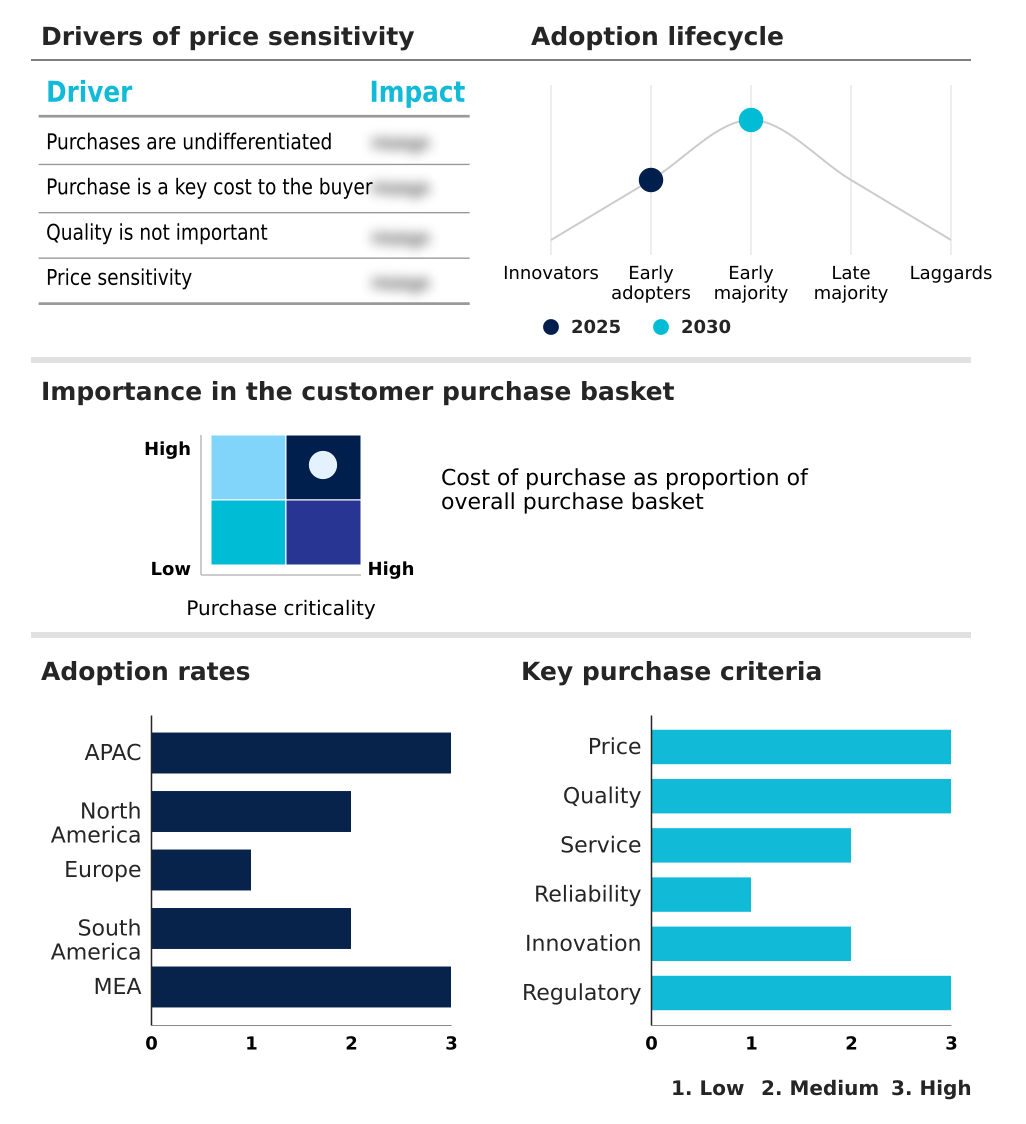

Exclusive Technavio Analysis on Customer Landscape

The battery raw materials market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the battery raw materials market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Battery Raw Materials Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, battery raw materials market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albemarle Corp. - Provides essential lithium compounds, including carbonate and hydroxide, sourced from diverse brine and hard rock deposits to support advanced battery manufacturing.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albemarle Corp.

- Arcadium Lithium

- BASF SE

- BHP Group Ltd.

- CMOC Group Limited

- Freeport McMoRan Inc.

- Ganfeng Lithium Group Ltd.

- Glencore Plc

- LG Chem Ltd.

- Pilbara Minerals Ltd.

- PJSC MMC Norilsk Nickel

- Rio Tinto Ltd.

- SQM S.A.

- Sumitomo Corp.

- Teck Resources Ltd.

- Tianqi Lithium Corp.

- Umicore SA

- Vale SA

- Zhejiang Huayou Cobalt Co., Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Battery raw materials market

- In August 2024, Tesla broke ground on a proprietary lithium refinery in Texas, aiming to produce battery-grade lithium hydroxide domestically to reduce logistical costs and secure its supply chain.

- In November 2024, BYD launched a compact electric vehicle powered by its second-generation sodium-ion battery pack, demonstrating the commercial viability of this alternative chemistry for cost-sensitive market segments.

- In January 2025, a leading Japanese automotive manufacturer revealed a prototype vehicle equipped with a proprietary solid-state battery, announcing plans for pilot production and signaling a future shift in material requirements.

- In April 2025, a consortium of major European truck manufacturers announced a joint venture to construct a dedicated battery cell production facility in Sweden, designed for heavy-duty applications and requiring substantial volumes of high-purity nickel.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Battery Raw Materials Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.1% |

| Market growth 2026-2030 | USD 30622.0 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.5% |

| Key countries | China, South Korea, Japan, India, Australia, Indonesia, US, Canada, Mexico, Germany, France, UK, The Netherlands, Spain, Italy, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The battery raw materials sector is in a state of strategic flux, defined by the dual pressures of accelerated electrification and geopolitical realignment. A primary focus is securing access to foundational inputs like lithium carbonate, lithium hydroxide, and spodumene concentrate.

- The industry is rapidly shifting from a commoditized supply model to one of deep vertical integration, where the control of cathode active materials (CAM) and high-purity nickel is paramount. This strategic imperative is compelling boardroom decisions to balance investments between new greenfield projects and urban mining infrastructure.

- Advanced hydrometallurgical recycling, which can recover up to 95% of battery-grade cobalt and other key metals from black mass processing, now offers a viable alternative to traditional extraction. This push toward circular economy principles is reinforced by battery passport regulation and the critical raw materials act.

- As the market diversifies with chemistries like lithium iron phosphate (LFP) and technologies like direct lithium extraction (DLE), navigating the complexities of synthetic graphite, silicon-carbon composites, solid-state electrolytes, and end-of-life battery management becomes essential for sustained competitive advantage and supply chain stability.

What are the Key Data Covered in this Battery Raw Materials Market Research and Growth Report?

-

What is the expected growth of the Battery Raw Materials Market between 2026 and 2030?

-

USD 30.62 billion, at a CAGR of 8.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Material (Cathodes materials, Anodes materials, Electrolyte materials, and Others), Application (Lead-acid battery, Lithium-ion battery, and Others), End-user (Secondary batteries, and Primary batteries) and Geography (APAC, North America, Europe, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Global policy mandates and accelerated electrification of transport, Geopolitical fragmentation and supply chain nationalization

-

-

Who are the major players in the Battery Raw Materials Market?

-

Albemarle Corp., Arcadium Lithium, BASF SE, BHP Group Ltd., CMOC Group Limited, Freeport McMoRan Inc., Ganfeng Lithium Group Ltd., Glencore Plc, LG Chem Ltd., Pilbara Minerals Ltd., PJSC MMC Norilsk Nickel, Rio Tinto Ltd., SQM S.A., Sumitomo Corp., Teck Resources Ltd., Tianqi Lithium Corp., Umicore SA, Vale SA and Zhejiang Huayou Cobalt Co., Ltd.

-

Market Research Insights

- Market dynamics are defined by a strategic push for supply chain resilience and technological diversification. The emphasis on supply chain localization is driving unprecedented capital expenditure in mining and downstream processing capacity. This is complemented by the rapid adoption of alternative chemistries, such as sodium-ion battery chemistry, to mitigate geopolitical supply risk associated with critical minerals like cobalt.

- The efficiency gains from new technologies are significant; advanced hydrometallurgical recycling plants now recover over 95% of key metals, creating a vital stream of secondary raw materials.

- Furthermore, stringent regulations, such as mandates requiring a 90% reduction in emissions for new heavy-duty vehicles, are accelerating the demand for advanced chemistry cells and forcing alignment with a closed-loop supply chain model, bolstering feedstock security for all participants.

We can help! Our analysts can customize this battery raw materials market research report to meet your requirements.

RIA -

RIA -