Big Data Security Market Size 2026-2030

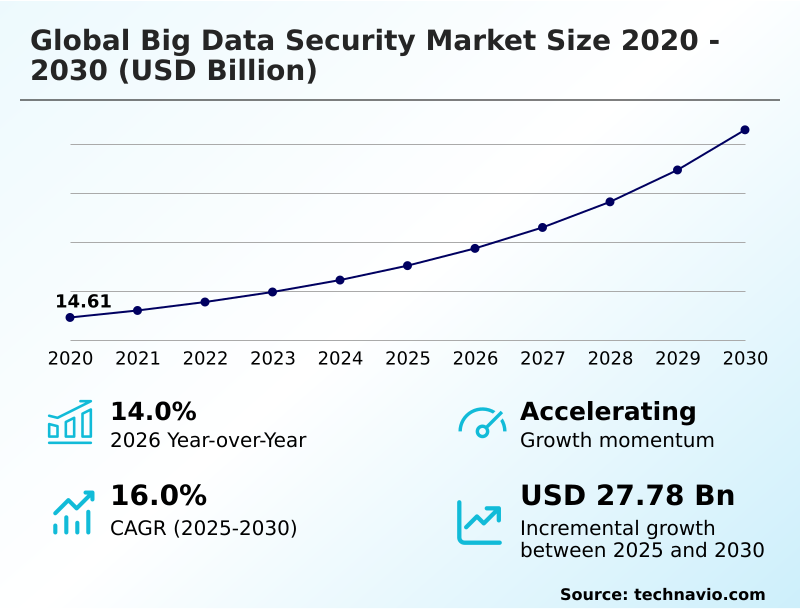

The big data security market size is valued to increase by USD 27.78 billion, at a CAGR of 16% from 2025 to 2030. Escalation of sophisticated AI driven cyber threats will drive the big data security market.

Major Market Trends & Insights

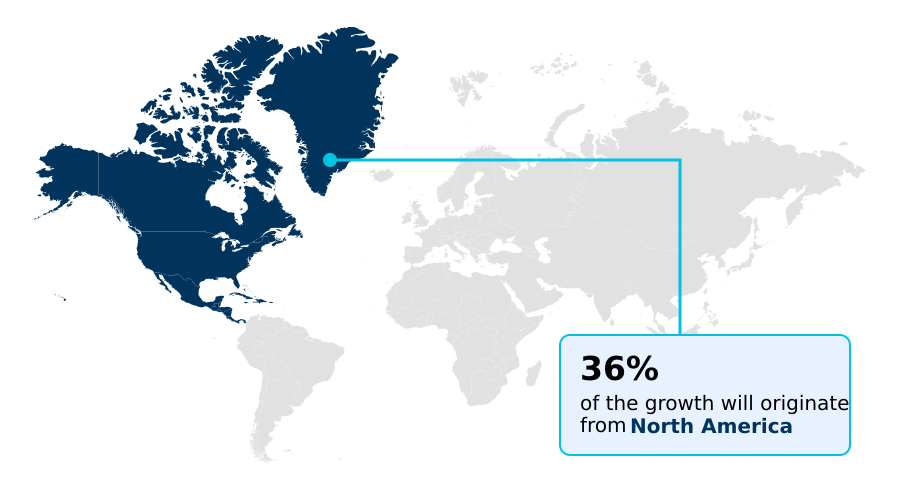

- North America dominated the market and accounted for a 36.2% growth during the forecast period.

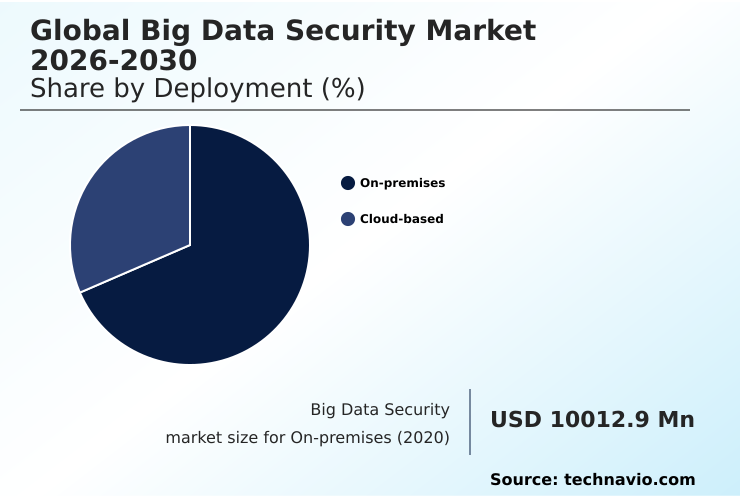

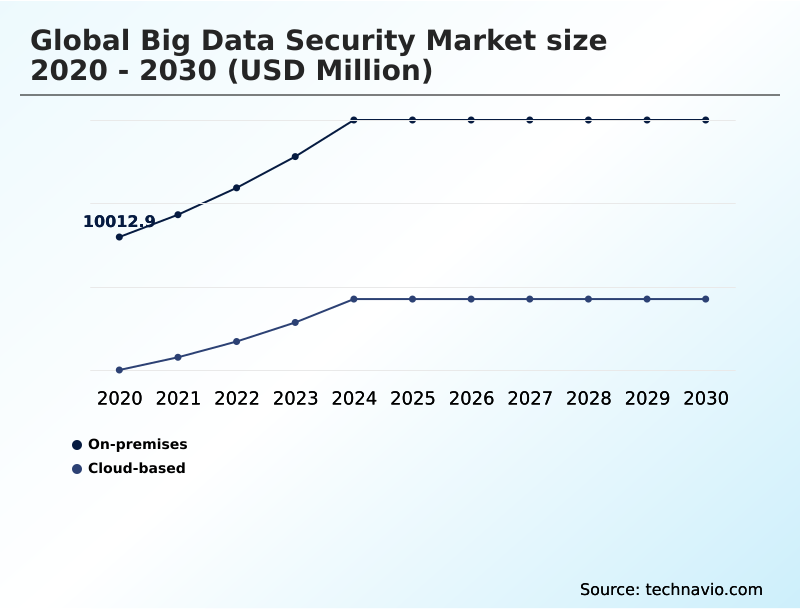

- By Deployment - On-premises segment was valued at USD 14.77 billion in 2024

- By End-user - Large enterprises segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 38.38 billion

- Market Future Opportunities: USD 27.78 billion

- CAGR from 2025 to 2030 : 16%

Market Summary

- The big data security market is defined by a critical need to protect massive, distributed datasets from unauthorized access and sophisticated exploitation. This specialized sector integrates advanced solutions like data encryption, identity and access management, and security information and event management (SIEM) systems tailored for cloud-native architectures.

- It implements multi-layered defense mechanisms across the entire data lifecycle, ensuring integrity and confidentiality for information both at rest and in transit. For instance, in financial services, these systems are pivotal for real-time fraud detection, analyzing petabytes of transaction data to identify anomalous patterns that indicate fraudulent activity.

- The primary market drivers include the rapid escalation of AI-driven cyber threats and an increasingly stringent global regulatory landscape, which mandates robust data protection and governance. Key trends involve a shift toward proactive, context-aware security ecosystems and the adoption of zero-trust principles.

- However, the industry grapples with the complexity of securing fragmented data architectures and a persistent shortage of specialized cybersecurity talent.

What will be the Size of the Big Data Security Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Big Data Security Market Segmented?

The big data security industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- On-premises

- Cloud-based

- End-user

- Large enterprises

- SMEs

- Solution

- Software

- Services

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- South America

- Brazil

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- North America

By Deployment Insights

The on-premises segment is estimated to witness significant growth during the forecast period.

The on-premises segment of the big data security market serves organizations that require absolute control over data sovereignty and security configurations, often within regulated sectors.

This deployment model is defined by localized management of security software, enabling robust data governance and adherence to strict data residency control.

It is critical for maintaining air-gapped environment security and integrating hardware-backed security modules, which are non-negotiable for high-value digital assets. The evolution of hyper-converged infrastructure security has simplified scaling secure big data workloads behind corporate firewalls.

Enterprises utilizing this model for their immutable data lake security report a 25% reduction in third-party data exposure risks, reinforcing the value of a data-centric security model independent of external provider policies.

The On-premises segment was valued at USD 14.77 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 36.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Big Data Security Market Demand is Rising in North America Get Free Sample

The geographic landscape of the big data security market is led by North America, which is forecast to contribute 36.2% of the incremental growth, driven by its mature technological infrastructure and early adoption of cloud-native security.

The region sees widespread implementation of multi-cloud security and unified threat management systems. Europe follows, with a strong focus on data residency control and regulatory compliance, where managed detection and response services have seen a 25% increase in adoption.

The APAC region is the fastest-growing market, characterized by rapid digital transformation and investments in endpoint security and cloud workload protection to secure expanding digital economies.

In South America and the Middle East and Africa, the focus is on strengthening foundational security, including intrusion detection systems and data lifecycle security, to combat rising cyber threats in emerging digital ecosystems.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Successfully securing heterogeneous distributed data architectures is a paramount goal for modern enterprises, necessitating real-time anomaly detection for big data to counter emerging threats. Achieving compliance with global data privacy regulations requires a unified security for hybrid cloud environments, a framework designed to protect data from AI-driven cyber threats.

- The security frameworks for cloud-native applications must be agile enough to handle the complexities of governing autonomous agent data interactions. This is complicated by the need for managing data sovereignty and residency laws, which often dictates the specifics of implementing post-quantum cryptographic standards.

- For many, the primary objective is securing industrial intellectual property data, which includes AI pipeline protection from data poisoning and preventing lateral movement in cloud networks. Data loss prevention for saas applications has become a standard requirement, pushing organizations toward identity-centric security for data lakes.

- As threat intelligence sharing across industries becomes more common, the challenges of managing cryptographic keys across jurisdictions and securing IoT data at the edge are amplified.

- Automated auditing for regulatory compliance and proactive vulnerability management in data infrastructure, guided by zero-trust principles for data access, are now considered foundational, with firms adopting these measures reporting up to a 40% faster incident response time compared to those with legacy systems.

What are the key market drivers leading to the rise in the adoption of Big Data Security Industry?

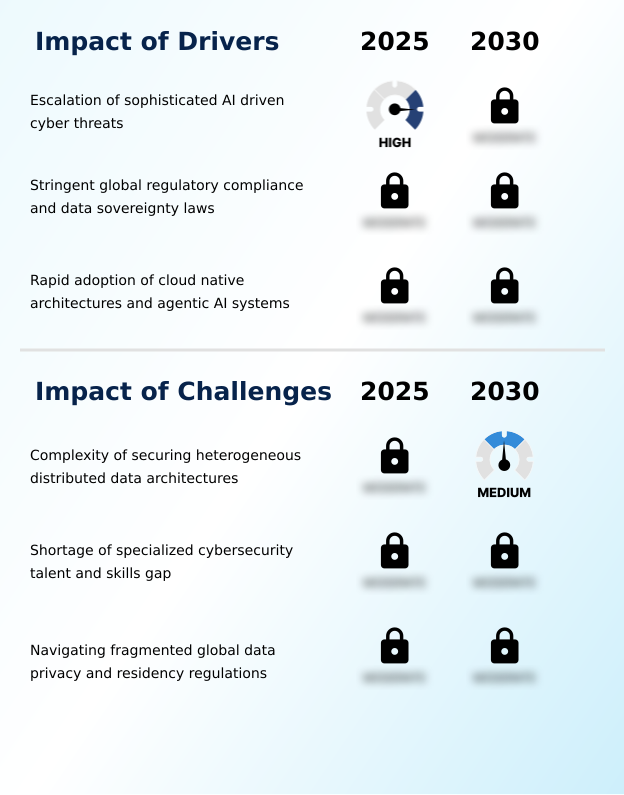

- The escalation of sophisticated, AI-driven cyber threats that automate and amplify attacks is a key driver for the big data security market.

- Market growth is primarily propelled by the escalation of sophisticated ai-driven cyber threats, which necessitates a move toward a zero-trust architecture.

- The adoption of cloud-native security is a key driver, as it provides the scalability required to protect distributed data ecosystems. Stringent global regulations mandate robust data encryption and data anonymization, making automated compliance auditing a critical business function.

- The integration of ai-powered threat detection and threat intelligence into security workflows has improved the identification of advanced persistent threats by up to 50%.

- As organizations embrace devops, devsecops integration ensures security is built into the secure software supply chain from the outset, significantly reducing downstream vulnerabilities.

- This holistic approach, focused on real-time fraud detection and preventing credential theft protection, is essential for maintaining business continuity.

What are the market trends shaping the Big Data Security Industry?

- The market is witnessing a proactive evolution toward context-aware and adaptive security systems. This transition moves beyond static rules to analyze data movement and user intent in real time.

- Key trends are reshaping the market toward intelligent, adaptive defense. The adoption of context-aware security, which analyzes user intent, has reduced false positive alerts by over 30% in complex environments. This proactive stance is enhanced by data security posture management, which provides continuous visibility into sensitive data.

- A major shift involves preparing for future threats through crypto-agility, enabling seamless transitions to post-quantum cryptography standards. The rise of agentic ai has spurred the development of specialized ai firewall implementations for ai model security, providing protection against sophisticated attacks.

- The integration of autonomous security operations and phishing-resistant credentials is becoming standard practice, with organizations reporting a 40% improvement in threat response times. This convergence of technologies ensures a resilient defense against evolving threats.

What challenges does the Big Data Security Industry face during its growth?

- The complexity of securing heterogeneous, distributed data architectures across multi-cloud and hybrid environments remains a key challenge for the industry.

- A primary challenge remains the complexity of securing heterogeneous data architectures, where data fragmentation complicates unified security management. The struggle to prevent data exfiltration prevention is magnified in environments with poor API security, which can lead to a 60% higher risk of data breaches.

- Navigating the fragmented global landscape of data privacy regulations adds significant operational overhead, requiring advanced data masking and forensic reporting capabilities. The shortage of skilled cybersecurity professionals hampers the ability of organizations to effectively utilize advanced tools for threat hunting automation and managing zero-trust network access.

- Furthermore, the risk of data poisoning and the difficulty of shadow data discovery in large data lakes require sophisticated network micro-segmentation and continuous monitoring, with misconfigurations in infrastructure as code security contributing to 20% of all cloud data breaches.

Exclusive Technavio Analysis on Customer Landscape

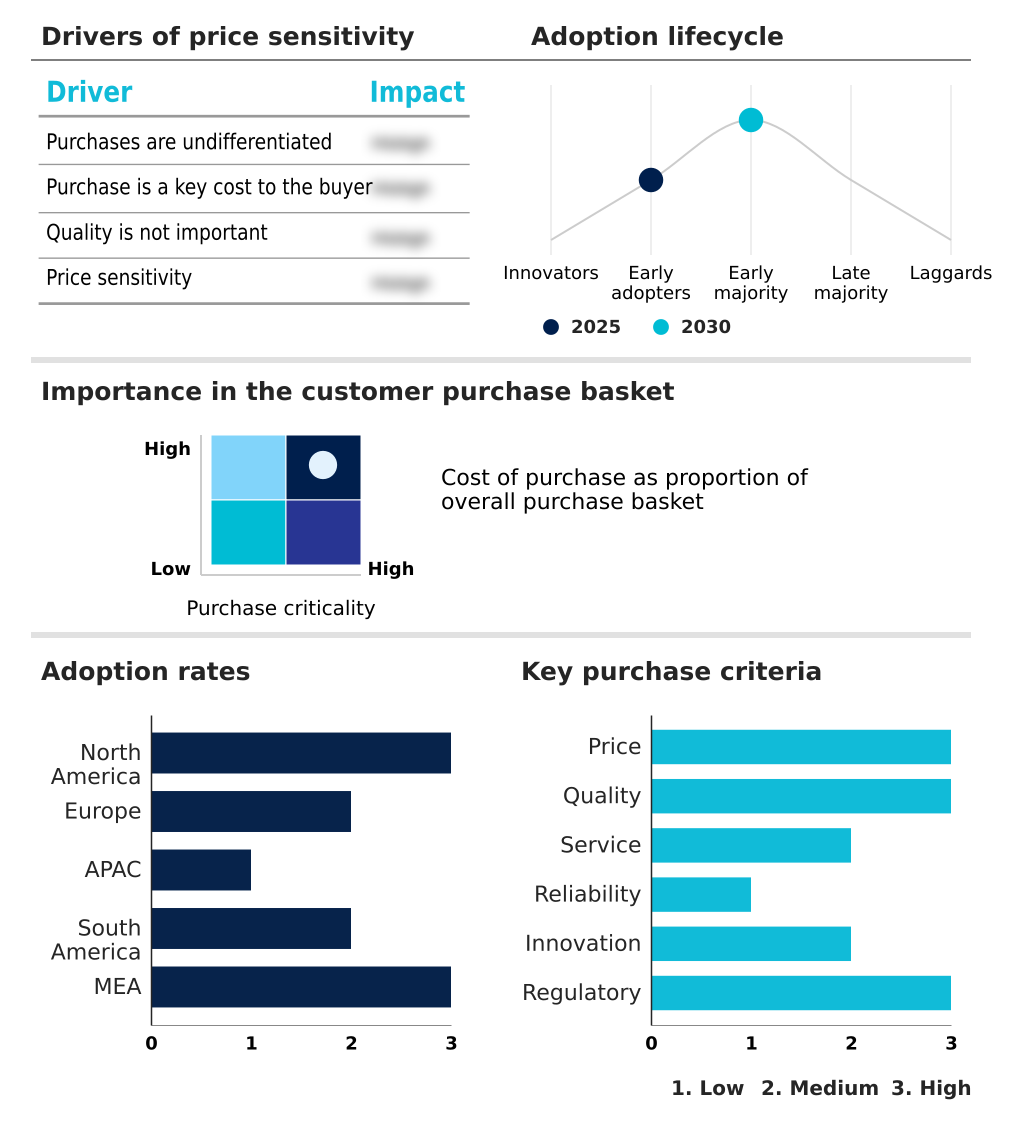

The big data security market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the big data security market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Big Data Security Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, big data security market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

BigID Inc. - Vendors provide unified data intelligence platforms integrating data loss prevention and enterprise security solutions for comprehensive protection and governance.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BigID Inc.

- Broadcom Inc.

- Cisco Systems Inc.

- Cloudera Inc.

- CrowdStrike Inc.

- Databricks Inc.

- Dell Technologies Inc.

- Fortinet Inc.

- Hewlett Packard Enterprise Co.

- IBM Corp.

- Immuta Inc.

- Imperva Inc.

- Informatica Inc.

- Microsoft Corp.

- Open Text Corp.

- Palantir Technologies Inc.

- Privacera Inc.

- Securonix Inc.

- Talend Inc.

- Varonis Systems Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Big data security market

- In August 2024, IBM Corp. released its latest X-Force Threat Intelligence Index, revealing a 44% increase in attacks exploiting public-facing applications, driven by AI-enabled vulnerability discovery.

- In February 2025, Microsoft Corp. enhanced its Azure platform by mandating transport layer security 1.2 as the minimum protocol, hardening core data infrastructure against legacy encryption vulnerabilities.

- In March 2025, Palo Alto Networks Inc. advanced its AI security with Prisma AIRS 3.0, a solution designed to secure the agentic artificial intelligence lifecycle from observation to autonomous execution.

- In May 2025, Microsoft Corp. inaugurated its new cloud region in Chile, providing local organizations with advanced tools for data residency, enhanced security controls, and localized data processing.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Big Data Security Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16% |

| Market growth 2026-2030 | USD 27783.6 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 14.0% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Chile, Colombia, Saudi Arabia, UAE, South Africa, Israel and Egypt |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The big data security market is evolving from perimeter defense to an intrinsic, data-centric paradigm, driven by the need for advanced threat intelligence and real-time behavioral analytics. Boardroom decisions now heavily factor in data sovereignty and the implementation of a robust zero-trust architecture, recognizing that data security posture management is fundamental to corporate risk mitigation.

- The adoption of agentic AI necessitates sophisticated identity and access management and credential theft protection to secure autonomous processes. A critical focus is on crypto-agility and the proactive integration of post-quantum cryptography to future-proof data against decryption risks. Organizations are leveraging data encryption, tokenization, and data anonymization, alongside vigilant shadow data discovery, to achieve comprehensive data governance.

- With the rise of cloud-native security, securing ephemeral workloads and serverless functions through API-driven controls and preventing lateral movement have become standard. This integrated approach, which includes everything from prompt injection defense to air-gapped environment security and intrusion detection systems, has enabled leading firms to reduce security policy misconfigurations by over 60%.

What are the Key Data Covered in this Big Data Security Market Research and Growth Report?

-

What is the expected growth of the Big Data Security Market between 2026 and 2030?

-

USD 27.78 billion, at a CAGR of 16%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (On-premises, and Cloud-based), End-user (Large enterprises, and SMEs), Solution (Software, and Services) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalation of sophisticated AI driven cyber threats, Complexity of securing heterogeneous distributed data architectures

-

-

Who are the major players in the Big Data Security Market?

-

BigID Inc., Broadcom Inc., Cisco Systems Inc., Cloudera Inc., CrowdStrike Inc., Databricks Inc., Dell Technologies Inc., Fortinet Inc., Hewlett Packard Enterprise Co., IBM Corp., Immuta Inc., Imperva Inc., Informatica Inc., Microsoft Corp., Open Text Corp., Palantir Technologies Inc., Privacera Inc., Securonix Inc., Talend Inc. and Varonis Systems Inc.

-

Market Research Insights

- Market dynamics are shaped by a strategic shift toward autonomous security operations, enabling organizations to manage digital risk protection with greater efficiency. The adoption of AI-powered threat detection has improved real-time fraud detection rates by up to 40% in some sectors.

- Furthermore, DevSecOps integration is reducing vulnerabilities in production environments by an average of 30% by embedding security into the development lifecycle. This focus on automated compliance auditing and secure software supply chains reflects a broader move toward proactive, data-centric security models.

- As organizations implement managed detection and response, they gain access to advanced threat hunting automation, which is critical in a landscape where machine identity management has become as important as securing human access. This evolution supports a resilient infrastructure against sophisticated data exfiltration prevention and insider threats.

We can help! Our analysts can customize this big data security market research report to meet your requirements.

RIA -

RIA -