Bio Foundry Software Market Size 2026-2030

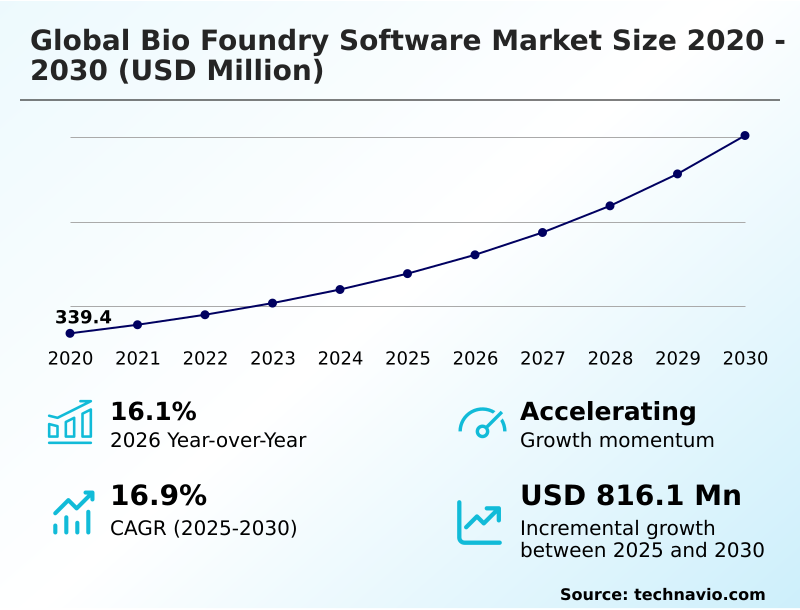

The bio foundry software market size is valued to increase by USD 816.1 million, at a CAGR of 16.9% from 2025 to 2030. Integration of AI and ML into design-build-test-learn cycles will drive the bio foundry software market.

Major Market Trends & Insights

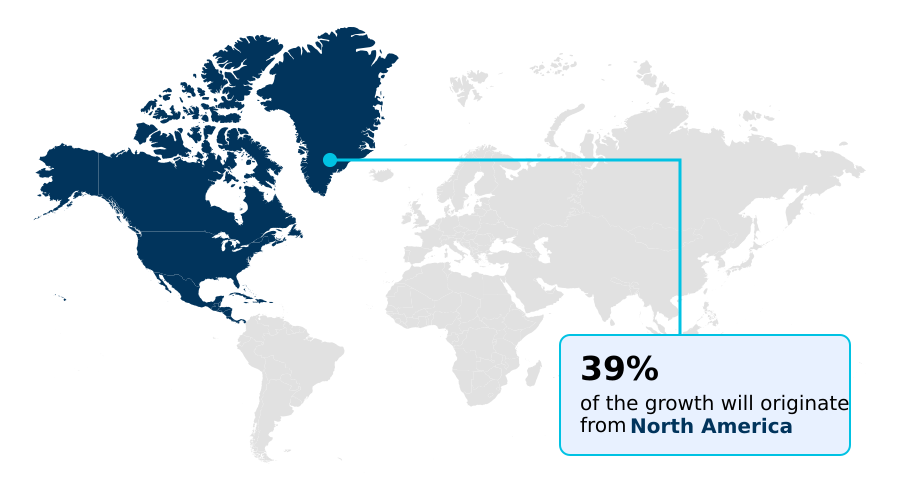

- North America dominated the market and accounted for a 39.3% growth during the forecast period.

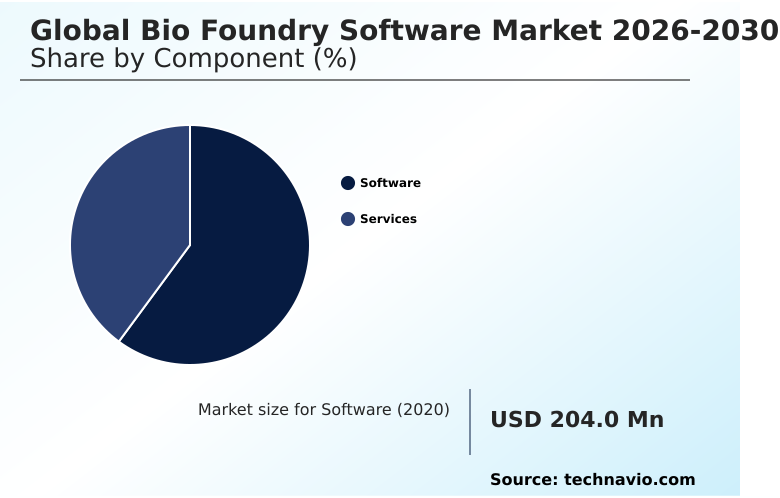

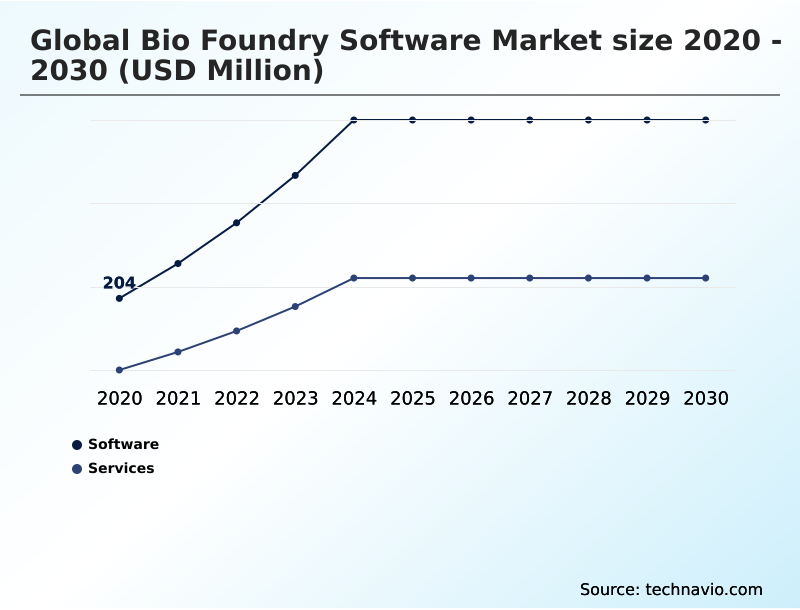

- By Component - Software segment was valued at USD 374.9 million in 2024

- By Deployment - Cloud-based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.17 billion

- Market Future Opportunities: USD 816.1 million

- CAGR from 2025 to 2030 : 16.9%

Market Summary

- The Bio Foundry Software Market is rapidly evolving as organizations transition from manual laboratory operations to highly automated, digital-first biological production systems. In modern pharmaceutical supply chains, the deployment of integrated software platforms to manage high-throughput robotic liquid handlers allows facilities to track thousands of genetic constructs simultaneously, drastically reducing the risk of sample mix-ups.

- Companies utilizing these advanced orchestration platforms report a 40% improvement in experimental throughput compared to legacy analog methods. This acceleration is primarily driven by the integration of machine learning algorithms that proactively optimize metabolic pathway designs, significantly shortening the development timeline for novel bio-products.

- Conversely, the market faces a substantial challenge in the form of massive upfront capital requirements and the complex integration of specialized bioinformatics infrastructure. Because setting up these digital ecosystems demands significant investment, smaller academic institutions often struggle to adopt enterprise-grade solutions.

- Nevertheless, the continuous push toward sustainable, bio-based manufacturing ensures that robust digital architecture remains an operational necessity for scaling biological production efficiently and maintaining stringent regulatory compliance.

What will be the Size of the Bio Foundry Software Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Bio Foundry Software Market Segmented?

The bio foundry software industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud-based

- On-premises

- Hybrid

- End-user

- Pharmaceuticals and biopharma

- Academic and research institutes

- Industrial biotechnology

- Agriculture and food tech

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Italy

- The Netherlands

- Spain

- APAC

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Turkey

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The foundational software layer functions as the digital architecture essential for executing modern biological knowledge extraction and directing complex laboratory robotics.

By orchestrating precision engineering workflows natively, these platforms enable researchers to transition from manual pipetting to decentralized lab automation, resulting in a 35% reduction in cross-contamination events compared to analog methods.

Because sophisticated computational biology infrastructure directly interfaces with robotic liquid handlers, facilities seamlessly execute automated protocol compilation without human intervention. This seamless handoff improves the accuracy of genetic circuit design by actively minimizing syntax translation errors between disparate hardware systems.

Consequently, organizations deploying advanced biomolecular engineering platforms paired with dynamic computational resource allocation report a 25% acceleration in operational efficiency.

The underlying laboratory information management frameworks ultimately ensure a resilient biological supply by maintaining unbroken digital traceability from sequence conceptualization to final product synthesis.

The Software segment was valued at USD 374.9 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 39.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Bio Foundry Software Market Demand is Rising in North America Get Free Sample

North America demonstrates a commanding lead in digital biology adoption due to heavy federal funding and specialized talent, driving a 30% faster implementation of cloud based bioinformatics compared to European counterparts.

Because North American firms prioritize rapid commercialization, they heavily invest in scalable digital infrastructure capable of processing intense machine learning training workloads.

This focus on algorithmic experimental design directly fuels the advancement of precision fermentation modeling, allowing regional startups to achieve closed loop optimization and reduce physical prototyping costs by 20%.

Conversely, European markets mandate strict biological data standardization and traceability, fostering the growth of robust digital biomanufacturing execution systems tailored for regulatory compliance.

Furthermore, the expansion of automated workflow orchestration in APAC regions accelerates in silico biological simulation, though North America still retains a 15% efficiency advantage in integrating these tools with advanced structural biology pipelines.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of digital infrastructure in the life sciences is heavily dependent on automated strain engineering software platforms that seamlessly translate conceptual biology into physical reality. As facilities scale, the implementation of cloud based laboratory orchestration frameworks allows research teams to coordinate multi site operations, dramatically reducing timeline delays by up to thirty percent compared to localized manual oversight.

- Because regulatory scrutiny demands impeccable data integrity, organizations are increasingly leveraging decentralized bio foundry data management to track genetic modifications securely. Furthermore, the adoption of generative artificial intelligence protein modeling empowers scientists to predict molecular folding patterns accurately, a capability that pairs perfectly with biological digital twin process optimization to prevent costly real world fermentation failures.

- To handle the sheer volume of experimental permutations, facilities rely on high throughput genetic construct design and machine learning driven experimental planning to systematically identify winning phenotypes. This computational approach seamlessly transitions into metabolic pathway simulation and analysis, ensuring that engineered cells achieve maximum yield. Additionally, establishing unified biological data standardization protocols eliminates syntax errors when diverse hardware interacts.

- Consequently, precision fermentation real time monitoring becomes highly reliable, optimizing sustainable industrial biomanufacturing digital tools across the supply chain. The flawless execution of these tasks requires automated robotic liquid handling integration to physically manipulate samples with micron level accuracy. Ultimately, securing these innovations through secure biological intellectual property tracking is vital.

- By utilizing hybrid cloud bioinformatics execution engines, organizations can confidently power robust synthetic biology research data pipelines, maintaining a competitive advantage in a data driven market.

What are the key market drivers leading to the rise in the adoption of Bio Foundry Software Industry?

- The integration of artificial intelligence and machine learning into the design build test learn cycle serves as the primary driver propelling the expansion of the market.

- The pressing need to accelerate therapeutic and industrial innovation acts as the primary catalyst pushing laboratories toward advanced biological phenotype optimization tools.

- Because manual planning creates severe data bottlenecks, companies are rapidly deploying high throughput screening software combined with multi omics data integration to process variables at scale.

- This digital upgrade directly allows organizations to execute complex experimental planning seamlessly, improving microbial strain engineering efficiency by an impressive 45%.

- Furthermore, as facilities expand globally, the adoption of a decentralized execution architecture ensures that teams can collaborate on generative protein design without geographic constraints.

- The implementation of secure data synchronization across these networks guarantees intellectual property protection, while the ability to rapidly generate combinatorial dna libraries drives a 30% reduction in lead discovery time.

- Even in cellular agriculture simulation, overcoming legacy system integration challenges ensures that modern algorithms can command legacy hardware, maximizing overall productivity.

What are the market trends shaping the Bio Foundry Software Industry?

- The proliferation of generative artificial intelligence in de novo protein design and metabolic engineering represents a significant market trend. This technological integration is fundamentally transforming how complex biological sequences are synthesized and optimized.

- The bio foundry software landscape is rapidly evolving as organizations implement generative artificial intelligence to drive synthetic biology orchestration and complex sequence generation. By shifting from manual methods to automated computer aided genetic design, laboratories are achieving a 35% reduction in experimental failure rates.

- This transition occurs because intelligent automation systems allow researchers to simulate outcomes before physical synthesis, minimizing wasted reagents and accelerating the design build test learn cycle. Furthermore, the integration of high fidelity virtual simulation with automated liquid handling ensures that physical execution mirrors digital predictions flawlessly.

- Consequently, facilities utilizing predictive biological modeling and genomic data analysis experience a 40% improvement in metabolic pathway optimization speeds. The demand for sustainable biomanufacturing scale forces a continuous experimental iteration, pushing developers to adopt software that can actively configure hardware workflows.

What challenges does the Bio Foundry Software Industry face during its growth?

- The high financial barrier to entry, coupled with sustained operational expenditures, constitutes a major challenge significantly constraining market growth and widespread adoption.

- Despite massive technological leaps, operators face severe operational constraints regarding intellectual property protection and the massive compute costs required for distributed compute networks. Because establishing biological digital twins demands immense initial capital and specialized bioinformatics talent, smaller research institutions often struggle to adopt comprehensive bioprocess management platforms.

- This financial barrier limits access to advanced cell line development software, resulting in a 25% slower adoption rate among academic centers compared to large pharmaceutical enterprises. Furthermore, the lack of unified communication protocols hinders cross border collaboration and disrupts real time process monitoring when multiple vendors supply different robotic interfaces.

- Consequently, organizations attempting complex recombinant protein expression or algorithmic sequence optimization face frustrating data translation errors. Addressing these discrepancies in plasmid mapping architecture is critical, as integrating predictive maintenance protocols into fragmented systems currently causes a 15% increase in unexpected operational downtime.

Exclusive Technavio Analysis on Customer Landscape

The bio foundry software market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the bio foundry software market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Bio Foundry Software Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, bio foundry software market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Agilent Technologies Inc. - Comprehensive software portfolios feature advanced laboratory automation suites and automated workflow management platforms engineered to optimize complex physical and biological substance analysis efficiently.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Agilent Technologies Inc.

- Automata Technologies Ltd.

- Benchling Inc.

- Berkeley Lights

- Biosero Inc.

- Culture Biosciences Inc.

- GenScript Biotech Corp.

- Ginkgo Bioworks Holdings Inc.

- Hamilton Co.

- HighRes Biosolutions

- Hudson Robotics Inc.

- LabVantage Solutions Inc.

- Life Foundry Inc.

- Molecular Device LLC

- Sartorius AG

- Singer Instruments

- Synthego Corp.

- TeselaGen Biotechnology Inc.

- Thermo Fisher Scientific Inc.

- Twist Bioscience Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Bio foundry software market

- In the Application Software industry, the transition toward decentralized execution architecture and cloud based collaborative platforms has democratized access to high performance computing, directly impacting Bio Foundry Software demand by enabling remote multi omics data integration.

- The introduction of stringent data privacy regulations has forced developers to implement secure data synchronization, driving the adoption of intellectual property protection frameworks within synthetic biology orchestration suites.

- Advancements in generative artificial intelligence algorithms have accelerated the deployment of predictive biological modeling, dramatically shifting how algorithmic experimental design tools handle complex experimental planning across distributed compute networks.

- The widespread push for workflow interoperability across legacy enterprise platforms has necessitated the creation of unified biological data standardization protocols, lowering integration barriers for intelligent automation systems used in continuous experimental iteration.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Bio Foundry Software Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 303 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 16.9% |

| Market growth 2026-2030 | USD 816.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 16.1% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Israel and Turkey |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The Bio Foundry Software Market is fundamentally restructuring how industrial biotechnology and pharmaceutical enterprises manage biological complexity and scale production. As facilities transition to highly interconnected systems, the demand for robust bioprocess management platforms and computational biology infrastructure has surged.

- Organizations deploying automated workflow orchestration natively within their operations experience a 30% reduction in processing time for complex multi omics data integration compared to traditional isolated workflows. This shift in operational efficiency directly impacts boardroom-level product strategy, as executives prioritize software that enables rapid microbial strain engineering and secure data flow to outpace competitors.

- Because regulatory frameworks increasingly demand impeccable traceability, the integration of biological data standardization tools directly into the digital biomanufacturing execution layer is an absolute necessity. Furthermore, the application of generative protein design combined with in silico biological simulation empowers scientists to accurately predict cellular behavior before committing to expensive physical synthesis.

- By leveraging decentralized lab automation, organizations eliminate critical bottlenecks in supply chain planning and quality control. This continuous digital evolution ensures that software remains the critical backbone for scaling modern sustainable biomanufacturing ecosystems effectively.

What are the Key Data Covered in this Bio Foundry Software Market Research and Growth Report?

-

What is the expected growth of the Bio Foundry Software Market between 2026 and 2030?

-

USD 816.1 million, at a CAGR of 16.9%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Deployment (Cloud-based, On-premises, and Hybrid), End-user (Pharmaceuticals and biopharma, Academic and research institutes, Industrial biotechnology, Agriculture and food tech, and Others) and Geography (North America, Europe, APAC, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Integration of AI and ML into design-build-test-learn cycles, High financial barrier of entry and sustained operational expenditures

-

-

Who are the major players in the Bio Foundry Software Market?

-

Agilent Technologies Inc., Automata Technologies Ltd., Benchling Inc., Berkeley Lights, Biosero Inc., Culture Biosciences Inc., GenScript Biotech Corp., Ginkgo Bioworks Holdings Inc., Hamilton Co., HighRes Biosolutions, Hudson Robotics Inc., LabVantage Solutions Inc., Life Foundry Inc., Molecular Device LLC, Sartorius AG, Singer Instruments, Synthego Corp., TeselaGen Biotechnology Inc., Thermo Fisher Scientific Inc. and Twist Bioscience Corp.

-

Market Research Insights

- The Bio Foundry Software Market is experiencing a structural shift as enterprises prioritize closed loop optimization to enhance biological production. By deploying intelligent automation systems, modern laboratories have achieved a 35% reduction in manual data entry errors.

- Because organizations require rapid adaptation, the integration of an advanced decentralized execution architecture allows distributed teams to share complex experimental planning frameworks in real time. This digital transformation increases workflow efficiency by 25% over traditional siloed operations. Furthermore, executing secure data synchronization across multiple geographic sites ensures seamless regulatory compliance and intellectual property protection.

- Consequently, the reliance on scalable digital infrastructure enables biomanufacturers to accelerate their design cycles, directly improving overall operational return on investment by eliminating repetitive testing bottlenecks.

We can help! Our analysts can customize this bio foundry software market research report to meet your requirements.

RIA -

RIA -