CCUS Software Platforms Market Size 2026-2030

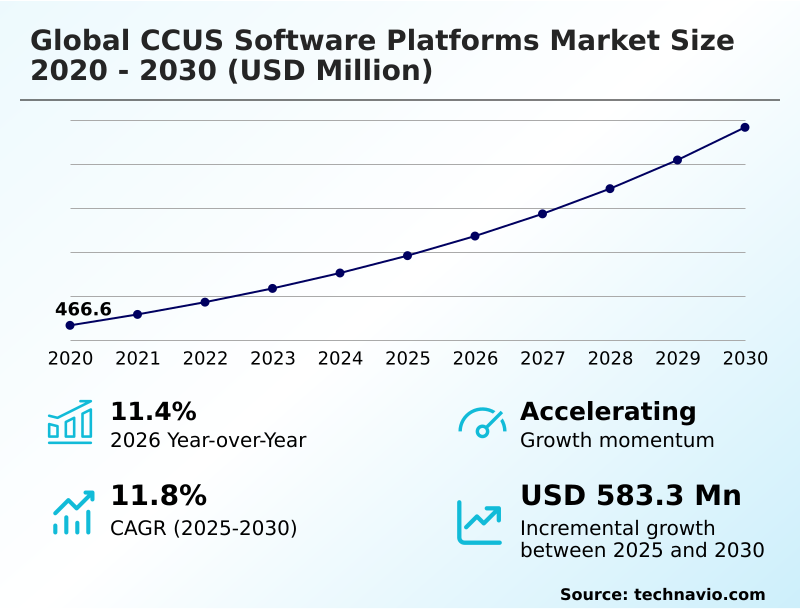

The ccus software platforms market size is valued to increase by USD 583.3 million, at a CAGR of 11.8% from 2025 to 2030. Stringent regulatory frameworks and evolution of carbon pricing mechanisms will drive the ccus software platforms market.

Major Market Trends & Insights

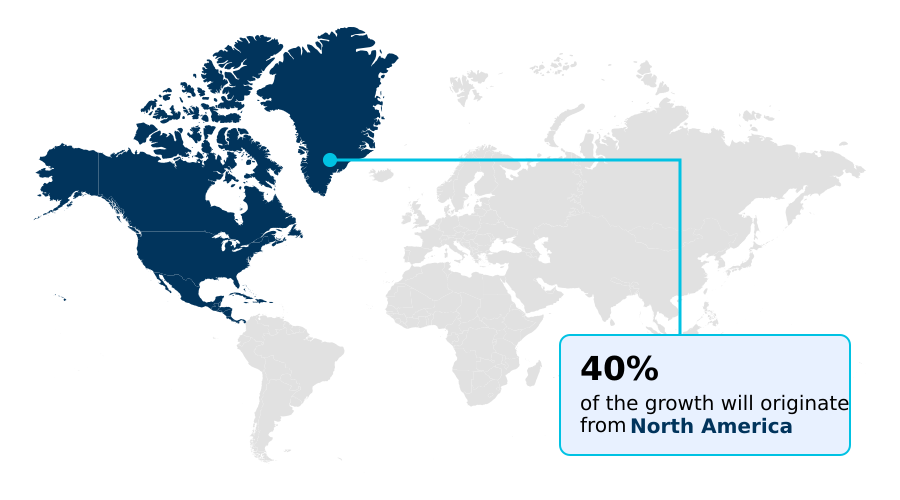

- North America dominated the market and accounted for a 40.2% growth during the forecast period.

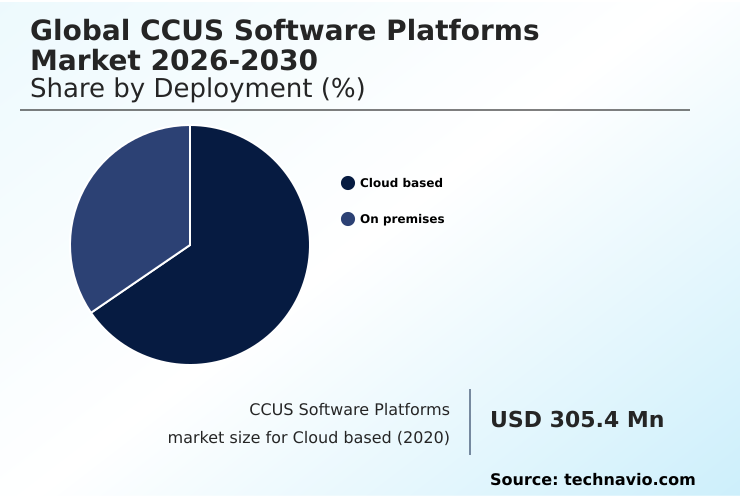

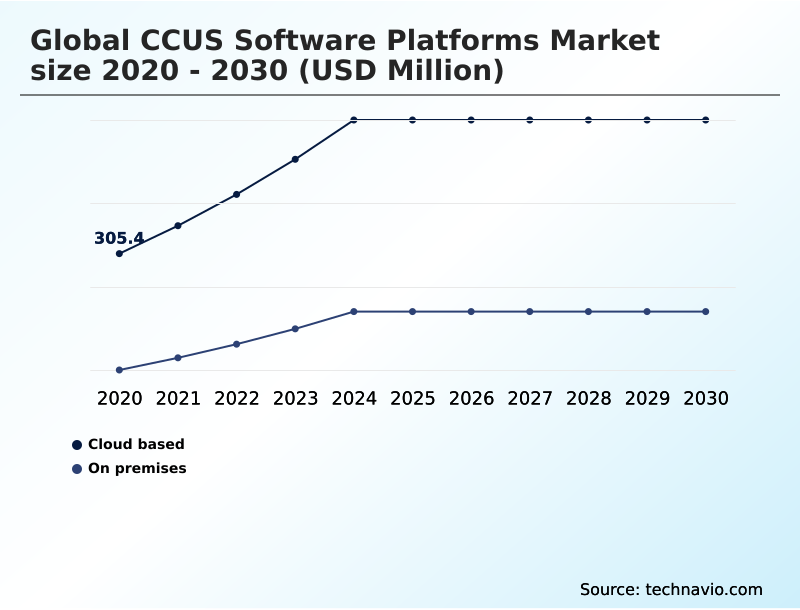

- By Deployment - Cloud based segment was valued at USD 471 million in 2024

- By Type - Monitoring and control platforms segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 900.1 million

- Market Future Opportunities: USD 583.3 million

- CAGR from 2025 to 2030 : 11.8%

Market Summary

- The CCUS software platforms market provides a sophisticated suite of digital tools for the end-to-end management of the carbon value chain. These platforms are engineered to facilitate the complex processes of capturing, transporting, and storing carbon dioxide, which is critical for heavy industries aiming to meet net-zero targets.

- Utilizing advanced analytics, these systems enable precise carbon capture modeling and efficient process control systems to minimize the energy penalty in facilities. Furthermore, they offer robust geological sequestration monitoring and carbon plume modeling to ensure the long-term integrity of storage sites.

- A key application involves an integrated emissions tracking software that automates regulatory compliance reporting for international frameworks, streamlining the verification of carbon credits. For instance, an operator of a large industrial cluster can leverage predictive maintenance modules to anticipate equipment failures in the transport network, preventing costly downtime and ensuring a continuous flow of CO2.

- The market is defined by its role in providing the data-driven precision required to make carbon management technologically viable, economically feasible, and environmentally secure. This digital infrastructure is indispensable for tracking atmospheric emissions and assessing the safety of sequestration projects, thereby building stakeholder confidence.

What will be the Size of the CCUS Software Platforms Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the CCUS Software Platforms Market Segmented?

The ccus software platforms industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Deployment

- Cloud based

- On premises

- Type

- Monitoring and control platforms

- Optimization and simulation software

- Data analytics and reporting tools

- Integration and management platforms

- End-user

- Oil and gas

- Power generation

- Cement

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Deployment Insights

The cloud based segment is estimated to witness significant growth during the forecast period.

Cloud-based deployment models are transforming carbon management by providing scalable, collaborative ecosystems essential for modern industrial decarbonization. These platforms leverage high-performance computing for intensive tasks like subsurface data analytics and simulation, removing the need for significant on-premise hardware investment.

This approach supports a carbon as a service platform model, enabling smaller operators to access advanced tools for monitoring, reporting, and verification.

For large, multi-user carbon infrastructure projects, a cloud platform serves as a single source of truth, synchronizing data from industrial automation software and pipeline telemetry systems in real time. This ensures accurate carbon accounting verification and streamlines compliance.

Organizations utilizing this model have reported up to a 20% improvement in data accessibility for remote monitoring teams.

The Cloud based segment was valued at USD 471 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.2% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How CCUS Software Platforms Market Demand is Rising in North America Request Free Sample

North America dominates the market, propelled by robust regulatory incentives in the United States and Canada that mandate enterprise-grade carbon tracking.

The region accounts for over 40% of the incremental growth opportunity, with operators leveraging advanced software for enhanced oil recovery modeling and injection well optimization.

European hubs in the UK and Norway are pioneers in subsea sequestration monitoring, utilizing platforms that integrate real-time leakage detection and asset performance management for offshore infrastructure.

The APAC region, led by Australia, is rapidly adopting these digital tools to manage shared carbon infrastructure and enable decarbonization workflow automation.

This geographic disparity highlights a market where mature regions focus on optimizing existing operations, while emerging markets prioritize establishing the foundational digital frameworks for future large-scale projects.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic implementation of specialized digital tools is becoming central to navigating the complex landscape of carbon management. Platforms offering software for 45q tax credit compliance are essential for operators in the United States seeking to monetize decarbonization efforts.

- Technologically, the focus is on efficiency gains, with tools to optimize amine scrubbing with ai and automate direct air capture process control, which can reduce energy penalties. For storage, simulating co2 plume behavior in saline aquifers and integrating seismic data for reservoir selection are critical for long-term project viability.

- The logistics of managing multi-user carbon pipeline networks and coordinating cross-border carbon dioxide shipments are handled by integrated platforms that provide real-time telemetry for co2 pipelines. In offshore environments, real-time monitoring for subsea carbon storage and ai-powered caprock integrity analysis are non-negotiable for safety.

- Sector-specific applications, like a digital twin for natural gas power plant ccus or software for cement plant decarbonization, are gaining traction. These systems also facilitate new economic models, with tools for verifying carbon credits with blockchain and conducting lifecycle assessment for carbon utilization.

- Adherence to strict regulatory mandates, such as managing class vi injection well compliance and using reporting tools for eu emissions trading system, is another key function. Overall, companies using integrated platforms for calculating embodied carbon footprint in infrastructure have reported a more streamlined project planning process compared to those using disconnected tools.

What are the key market drivers leading to the rise in the adoption of CCUS Software Platforms Industry?

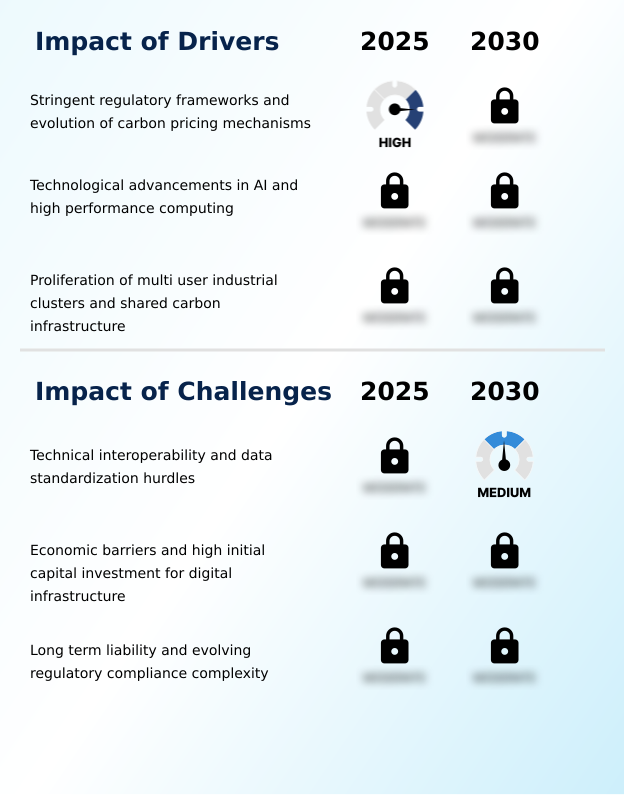

- Stringent regulatory frameworks and the evolution of carbon pricing mechanisms are the primary drivers propelling market expansion.

- Stringent regulations and carbon pricing, such as the carbon border adjustment mechanism, are primary market drivers.

- These policies necessitate the use of sophisticated software for lifecycle emissions calculation and transparent reporting, with integrated carbon credit generation tools directly linking decarbonization efforts to financial returns.

- Technologically, advancements in AI are transforming subsurface analysis, enabling automated geological fault identification and reducing site evaluation times by up to 40%.

- For operational efficiency, the proliferation of industrial hubs requires platforms with multi-tenant digital management and advanced injection pressure management capabilities.

- An environmental intelligence platform that provides a single, auditable record for all stakeholders is now essential for managing these collaborative, large-scale projects.

What are the market trends shaping the CCUS Software Platforms Industry?

- The integration of advanced digital twins and high-fidelity physics-based modeling is an influential trend. It provides a sophisticated bridge between physical assets and digital oversight for the entire project lifecycle.

- A dominant trend is the use of digital twins that leverage high-fidelity physics, including computational fluid dynamics and thermodynamic property modeling, to simulate the entire integrated carbon value chain. These platforms enhance operational oversight, with some systems improving energy efficiency in capture units by up to 10%.

- The application of AI and machine learning for interpreting massive datasets from IoT for carbon monitoring and microseismic sensor analysis is another key development. This is enabling automated geological modeling and enhancing the use of subsurface imaging platforms for rapid site characterization.

- The ability to predict CO2 behavior with greater than 95% accuracy in simulations is becoming a critical factor for securing project financing and regulatory approval.

What challenges does the CCUS Software Platforms Industry face during its growth?

- Technical interoperability issues and a lack of data standardization across the value chain present a significant challenge to seamless market growth.

- A significant challenge is the lack of technical interoperability, which fragments carbon lifecycle management and complicates the integration of subsurface models with process engineering data integration. This creates data silos that can impede real-time monitoring and holistic caprock stability assessment.

- The high initial capital required for sensors and computing infrastructure also presents a barrier, with implementation costs sometimes exceeding software license fees by a factor of three. Furthermore, evolving regulations demand robust digital solutions, such as asset integrity software incorporating tamper-proof data logs, to manage long-term liability.

- This complexity slows adoption, particularly for emerging applications like co2 mineralization software, which requires a seamless unified data environment to be effective.

Exclusive Technavio Analysis on Customer Landscape

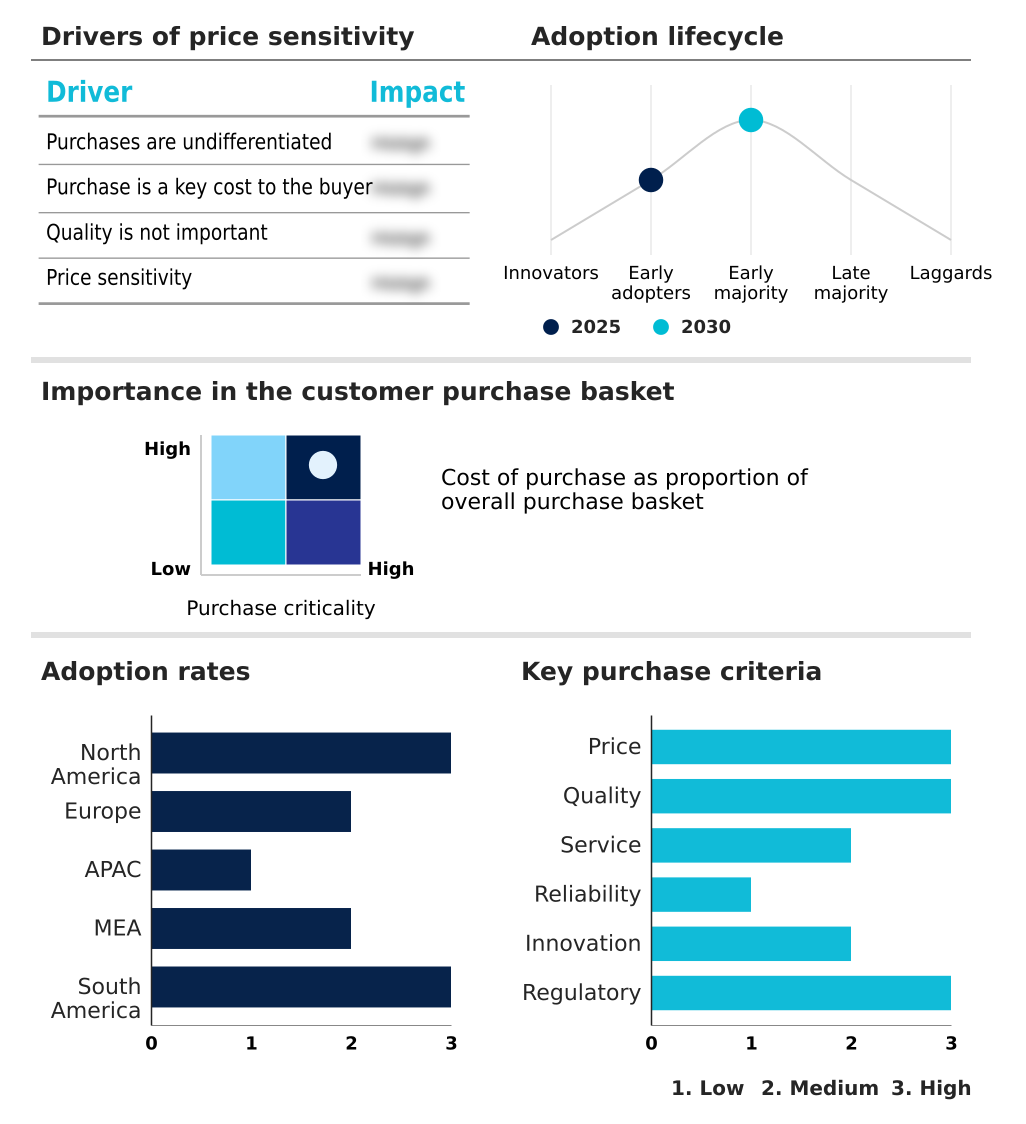

The ccus software platforms market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the ccus software platforms market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of CCUS Software Platforms Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, ccus software platforms market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ANSYS Inc. - Key offerings provide end-to-end digital orchestration for carbon value chains, integrating capture facility monitoring, transport logistics, and subsurface storage management through a unified data environment.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ANSYS Inc.

- AVEVA Group Ltd.

- Baker Hughes Co.

- Bentley Systems Inc.

- CGG SA

- Dassault Systemes SE

- DNV Group AS

- Emerson Electric Co.

- Halliburton Co.

- Honeywell International Inc.

- IBM Corp.

- Kongsberg Gruppen ASA

- Microsoft Corp.

- Rockwell Automation Inc.

- S and P Global Inc.

- SAP SE

- Schlumberger Ltd.

- Siemens AG

- TGS ASA

- Yokogawa Electric Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Ccus software platforms market

- In August 2025, Halliburton introduced an updated version of its subsurface modeling software that incorporates generative artificial intelligence to automate the creation of high-resolution geological models for carbon sequestration.

- In May 2025, the International Organization for Standardization finalized a revised framework for digital data exchange in carbon sequestration projects to address fragmentation issues.

- In October 2025, the Northern Lights project in Norway activated a new multi-tenant digital management interface to coordinate the arrival and injection schedules of carbon dioxide shipments from diverse industrial emitters across Northern Europe.

- In April 2025, the United States Department of Energy finalized a new set of digital reporting standards for federally funded carbon management projects, requiring the use of interoperable software platforms.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled CCUS Software Platforms Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 316 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 11.8% |

| Market growth 2026-2030 | USD 583.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 11.4% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The CCUS software platforms market is evolving from niche engineering tools to integrated, enterprise-level digital ecosystems. The convergence of operational technology and information technology is driving this shift, with platforms now combining subsurface reservoir simulation for site selection with real-time process control systems for amine scrubbing optimization.

- A key trend is the deployment of physics-based digital twins that encompass the entire value chain, from carbon capture modeling and supercritical co2 modeling for transport to geological sequestration monitoring. These systems provide a holistic view, enabling predictive maintenance modules that improve asset uptime by over 15%.

- Boardroom decisions are increasingly influenced by the capabilities of emissions tracking software to provide transparent carbon accounting verification, which is essential for accessing green financing and ensuring regulatory adherence. The integration of subsurface data analytics for reservoir integrity assessment and real-time leakage detection is now a standard requirement, transforming long-term risk management from a reactive to a proactive discipline.

What are the Key Data Covered in this CCUS Software Platforms Market Research and Growth Report?

-

What is the expected growth of the CCUS Software Platforms Market between 2026 and 2030?

-

USD 583.3 million, at a CAGR of 11.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Deployment (Cloud based, and On premises), Type (Monitoring and control platforms, Optimization and simulation softwar, Data analytics and reporting tools, and Integration and management platforms), End-user (Oil and gas, Power generation, Cement, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Stringent regulatory frameworks and evolution of carbon pricing mechanisms, Technical interoperability and data standardization hurdles

-

-

Who are the major players in the CCUS Software Platforms Market?

-

ANSYS Inc., AVEVA Group Ltd., Baker Hughes Co., Bentley Systems Inc., CGG SA, Dassault Systemes SE, DNV Group AS, Emerson Electric Co., Halliburton Co., Honeywell International Inc., IBM Corp., Kongsberg Gruppen ASA, Microsoft Corp., Rockwell Automation Inc., S and P Global Inc., SAP SE, Schlumberger Ltd., Siemens AG, TGS ASA and Yokogawa Electric Corp.

-

Market Research Insights

- Market dynamics are shaped by the critical need for digital orchestration for ccus, enabling complex coordination across the value chain. Platforms leveraging high-fidelity physics modeling allow operators to achieve a 15% increase in storage site selection accuracy. The adoption of integrated solutions supports net-zero industrial act compliance, with automated reporting features reducing audit preparation times by over 25%.

- These systems are essential for managing logistical challenges, such as cross-border carbon transport, by providing a unified interface for multi-jurisdictional regulatory adherence. The shift towards shared infrastructure models is compelling organizations to invest in scalable, cloud-native platforms to maintain a competitive edge in a rapidly decarbonizing industrial landscape.

We can help! Our analysts can customize this ccus software platforms market research report to meet your requirements.

RIA -

RIA -