Cellular Glass Market Size 2025-2029

The cellular glass market size is valued to increase by USD 137.9 million, at a CAGR of 4.1% from 2024 to 2029. Increasing demand for energy-efficient building materials will drive the cellular glass market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 35.1% growth during the forecast period.

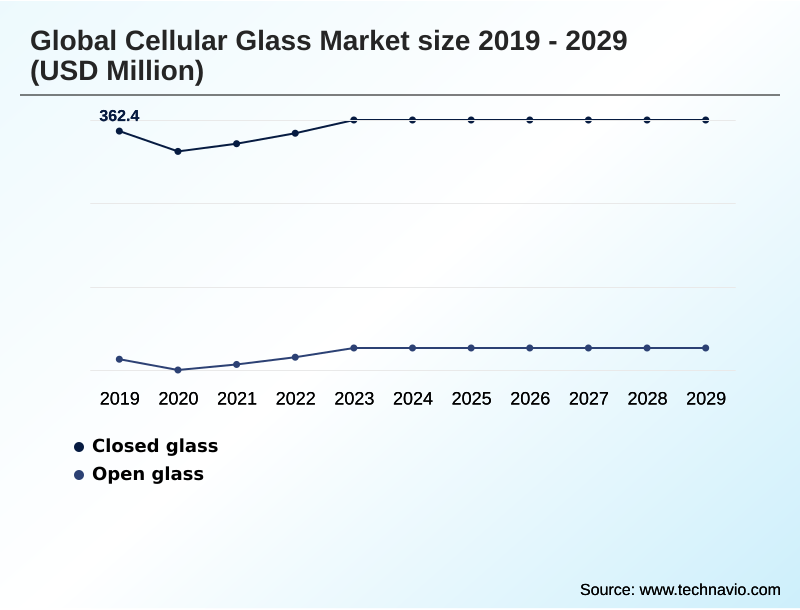

- By Type - Closed glass segment was valued at USD 369.6 million in 2023

- By Product Type - Block and shell segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 176.3 million

- Market Future Opportunities: USD 137.9 million

- CAGR from 2024 to 2029 : 4.1%

Market Summary

- The cellular glass market is expanding, driven by the need for high-performance, sustainable insulation. Its unique combination of properties—thermal efficiency, fire resistance, water impermeability, and high compressive strength—makes it essential for demanding applications. In construction, it contributes to green building certifications and long-term energy savings.

- The industrial sector relies on it for insulating cryogenic and high-temperature systems, where material failure is not an option. For instance, a facility manager overseeing a new cold storage plant must balance the higher upfront cost of cellular glass against its lifecycle benefits, including lower energy bills and zero risk of moisture-related degradation, which could compromise the entire facility.

- The material's composition from recycled glass also aligns with corporate ESG goals, further propelling its adoption. The cellular glass market continues to evolve as manufacturers innovate to enhance its properties and reduce production costs, broadening its applicability across various sectors.

What will be the Size of the Cellular Glass Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Cellular Glass Market Segmented?

The cellular glass industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Closed glass

- Open glass

- Product type

- Block and shell

- Foam glass gravel

- End-user

- Construction

- Industrial

- Others

- Geography

- Europe

- UK

- Germany

- France

- North America

- US

- Canada

- Mexico

- APAC

- China

- Japan

- India

- Middle East and Africa

- South Africa

- Saudi Arabia

- UAE

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- Europe

By Type Insights

The closed glass segment is estimated to witness significant growth during the forecast period.

The closed glass segment, which accounts for over 62% of the market, is defined by its superior material properties.

This type of cellular glass insulation utilizes a closed-cell structure of hermetically sealed cells, providing exceptional thermal performance and creating an effective vapor barrier. Its inherent moisture impermeability makes it a preferred moisture-resistant insulation for creating a high-performance building envelope.

Products like cellular glass block are engineered for high compressive strength, qualifying them as compressive-strength insulation. Made from recycled glass content, this non-combustible material offers excellent thermal insulation properties and is crucial for applications requiring robust and reliable performance.

The material's characteristics also make it suitable for a wide range of building applications where both structural support and insulation are required.

The Closed glass segment was valued at USD 369.6 million in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 35.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cellular Glass Market Demand is Rising in North America Get Free Sample

The global market landscape is led by Europe and North America, with APAC projected to have the fastest growth. North America is set to contribute over 35% of the market's incremental growth, driven by stringent building codes and industrial expansion.

Europe's market is mature, focused on sustainable construction material and renovation projects that require high-performance, rot-proof material. In this region, inorganic insulation is prized for its longevity.

Key applications include sub-slab insulation and lightweight structural fill for infrastructure, where its properties as a closed-pore glass foam prevent moisture issues. This load-bearing thermal insulation is also crucial for cold storage insulation and flat roof insulation systems.

The material's zero ozone depletion potential and low moisture vapor transmission rate support its use in environmentally sensitive projects, boosting its cellular glass r-value proposition for specifiers.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- When evaluating insulation options, a common comparison is cellular glass vs mineral wool. While both offer thermal benefits, the unique benefits of foam glass gravel include its role as a lightweight fill for civil engineering and its excellent drainage capacity, making it ideal for creating a pervious pavement aggregate.

- For cellular glass in cryogenic applications, its performance is unmatched due to its non-porous structure, which is also a key factor for its use in various industrial settings. The process of installing cellular glass insulation blocks requires precision, and a primary consideration for project managers is the cost of cellular glass insulation. However, a lifecycle cost analysis often favors it.

- The material's durability of cellular glass insulation, high fire rating of cellular glass, and its function as a cellular glass as a vapor barrier justify the investment. These qualities make it a prime choice for cellular glass for green roofs and cellular glass for foundation insulation.

- A cellular glass compressive strength test ensures quality, while its resistance to chemicals is vital for industrial use. The high recycled content in cellular glass also aligns with sustainability goals. For operational planning, its long-term reliability translates to a total cost of ownership that can be up to 20% lower than alternatives in certain high-stakes environments.

What are the key market drivers leading to the rise in the adoption of Cellular Glass Industry?

- The increasing demand for energy-efficient building materials, driven by stricter building codes and a focus on sustainability, serves as a key driver for the market's growth.

- The market is propelled by the demand for energy-efficient building materials in critical industrial sectors. The need for effective cryogenic insulation for LNG tanks and cryogenic storage insulation in the chemical industry is a major factor.

- The material's properties as a non-combustible material and its inherently low thermal conductivity make it an ideal fire resistant insulation, crucial for meeting modern building code compliance.

- For industrial pipe insulation, pipe insulation shells offer reliable thermal performance at a high operating temperature.

- A comprehensive life cycle assessment often demonstrates that this fireproof building insulation offers lower long-term costs, with facilities reporting energy loss reductions of up to 15%.

- This makes it a preferred choice for industrial thermal insulation, especially in insulation for chemical plants, where safety and efficiency are paramount.

What are the market trends shaping the Cellular Glass Industry?

- A significant market trend is the growing adoption of cellular glass in green roof and urban landscaping projects, valued for its lightweight nature and excellent drainage capabilities.

- A primary trend is the growing use of foam glass gravel as a lightweight aggregate in sustainable infrastructure projects. This ecologically friendly insulation, notable for its high recycled glass content, is becoming integral to green roof insulation and urban landscaping. Its application as a green roof drainage layer and in pervious pavement aggregate systems improves stormwater management by over 30%.

- The material’s non-capillary structure is also effective for frost heave prevention. As a sustainable building material, it contributes to a significant embodied energy reduction in construction projects. These sustainable insulation solutions are gaining traction, with foam glass for landscaping and as a lightweight fill material seeing increased specification.

- The market for recycled glass building products is expanding, with foam glass aggregate leading the charge in circular economy applications.

What challenges does the Cellular Glass Industry face during its growth?

- A primary challenge affecting market growth is the high initial cost of cellular glass when compared to conventional insulation materials, which can deter adoption in cost-sensitive projects.

- A key challenge is the material's higher initial cost and the specialized cellular glass installation knowledge required, which can impact project budgets and timelines. While its dimensional stability and role in thermal bridge prevention are significant advantages, the technical cellular glass specification can be a hurdle.

- For instance, ensuring proper use as a structural insulation core within a building envelope insulation system requires skilled labor. Its properties as a pest resistant insulation with excellent sound absorption, contributing to a higher sound transmission class, are premium features. This acid-resistant material also aids in corrosion under insulation prevention.

- However, comparing cellular glass vs foamglas or other alternatives on price alone overlooks its value as a non-toxic insulation material and its effectiveness in acoustic insulation panels. The perception of complexity in handling the cellular glass block remains a barrier to wider adoption.

Exclusive Technavio Analysis on Customer Landscape

The cellular glass market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cellular glass market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cellular Glass Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cellular glass market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Beerenberg AS - A portfolio of cellular glass insulation products, including blocks and pipe sections, delivers durable thermal protection for commercial and industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Beerenberg AS

- Energocell Kft.

- Excelsior Ceramics

- Foamit Group

- Glapor Werk Mitterteich GmbH

- Huali Thermal Insulation

- Huaneng Zhongtian Group Co. Ltd.

- IBSL Group Ltd.

- Insultherm

- Misapor AG

- Owens Corning

- POLYDROS S.A.

- REFAGLASS s.r.o.

- Shanghai Metal Corp.

- Sun Refractories

- Wedge Industries Ltd.

- Zhejiang Dehe Insulation Corp. Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cellular glass market

- In September, 2024, Glapor Werk Mitterteich GmbH announced a strategic partnership with a leading North American distributor to expand its market presence for cellular glass boards and gravel, targeting large-scale commercial construction projects.

- In November, 2024, Owens Corning launched a new line of FOAMGLAS insulation with enhanced compressive strength and a 15% improvement in thermal resistance, designed for next-generation cryogenic storage facilities.

- In January, 2025, Foamit Group completed the acquisition of a regional recycled glass processing firm to secure its raw material supply chain, increasing the recycled content in its foam glass aggregate products to over 95%.

- In April, 2025, Beerenberg AS reported securing a major contract for insulating a new LNG facility in APAC, leveraging its specialized corrosion-resistant foam glass linings following the region's new stringent maritime environmental regulations.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cellular Glass Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 281 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.1% |

| Market growth 2025-2029 | USD 137.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 4.1% |

| Key countries | UK, Germany, France, Spain, Italy, The Netherlands, US, Canada, Mexico, China, Japan, India, South Korea, Australia, Indonesia, South Africa, Saudi Arabia, UAE, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cellular glass market is defined by its multifunctionality, serving as a structural insulation core with a closed-cell structure that offers superior thermal insulation properties and moisture impermeability. Its composition of recycled glass content makes it an ecologically friendly insulation and sustainable building material with zero ozone depletion potential, which is critical for life cycle assessment and embodied energy reduction.

- As an inorganic insulation, it is a rot-proof material and pest resistant insulation, offering unmatched dimensional stability and chemical inertness. The high compressive strength makes it a load-bearing insulation ideal for sub-slab insulation, while its non-combustible material status ensures it is a fire resistant insulation, meeting strict building code compliance.

- Its use in pipe insulation shells and cryogenic insulation for high operating temperature environments is common. For construction, foam glass gravel acts as a lightweight aggregate and green roof drainage layer, aiding in frost heave prevention and thermal bridge prevention. This acid-resistant material also provides sound absorption, contributing to a higher sound transmission class.

- The hermetically sealed cells in this closed-pore glass foam create an effective vapor barrier with a low moisture vapor transmission rate and low thermal conductivity, and this incombustible insulation has demonstrated a service life over 50% longer than many organic foams.

What are the Key Data Covered in this Cellular Glass Market Research and Growth Report?

-

What is the expected growth of the Cellular Glass Market between 2025 and 2029?

-

USD 137.9 million, at a CAGR of 4.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Closed glass, and Open glass), Product Type (Block and shell, and Foam glass gravel), End-user (construction, Industrial, and Others) and Geography (Europe, North America, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

Europe, North America, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Increasing demand for energy-efficient building materials, High initial cost compared to conventional insulation materials

-

-

Who are the major players in the Cellular Glass Market?

-

Beerenberg AS, Energocell Kft., Excelsior Ceramics, Foamit Group, Glapor Werk Mitterteich GmbH, Huali Thermal Insulation, Huaneng Zhongtian Group Co. Ltd., IBSL Group Ltd., Insultherm, Misapor AG, Owens Corning, POLYDROS S.A., REFAGLASS s.r.o., Shanghai Metal Corp., Sun Refractories, Wedge Industries Ltd. and Zhejiang Dehe Insulation Corp. Ltd.

-

Market Research Insights

- The market's momentum is supported by its alignment with sustainability goals and superior material characteristics. As a lightweight fill material, its use in civil engineering has reduced project costs by up to 10% by minimizing the need for heavy machinery.

- The adoption of recycled glass insulation is a key factor, with some products containing over 90% recycled content, appealing to environmentally conscious specifiers. In industrial settings, high-performance building envelope systems utilizing cellular glass insulation can improve a facility's thermal performance significantly. The demand for foam glass aggregate is also growing for applications beyond basic insulation.

- This market is defined by a clear value proposition where the initial investment is offset by long-term operational savings and durability, making it a strategic choice for critical infrastructure and sustainable construction.

We can help! Our analysts can customize this cellular glass market research report to meet your requirements.

RIA -

RIA -