Israel Ceramic Tiles Market Size 2026-2030

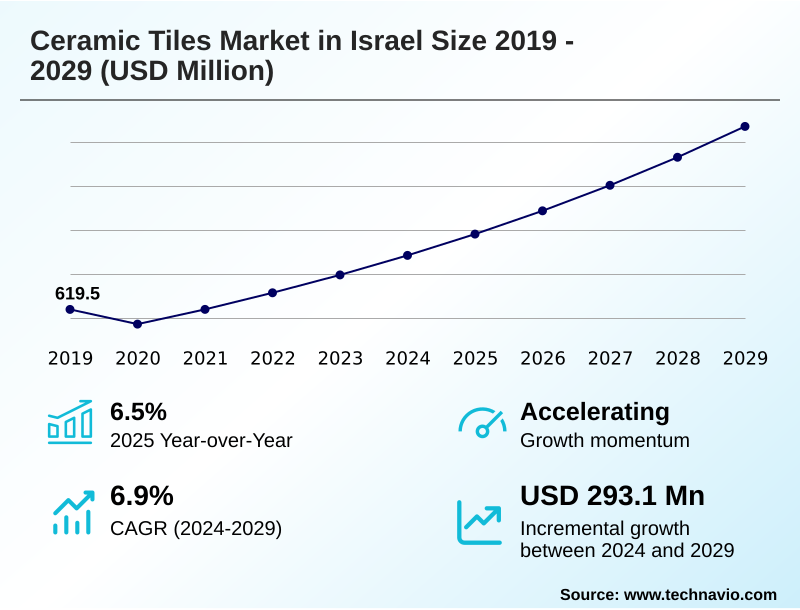

The Israel Ceramic Tiles Market size was valued at USD 790.7 million in 2025, growing at a CAGR of 7% during the forecast period 2026-2030.

Major Market Trends & Insights

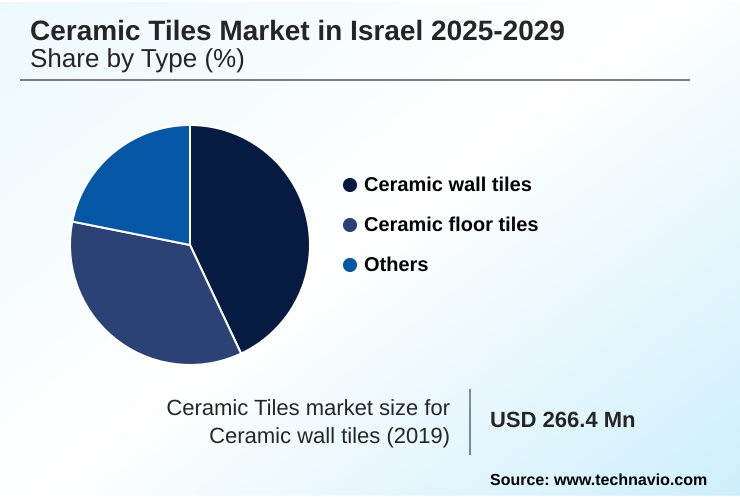

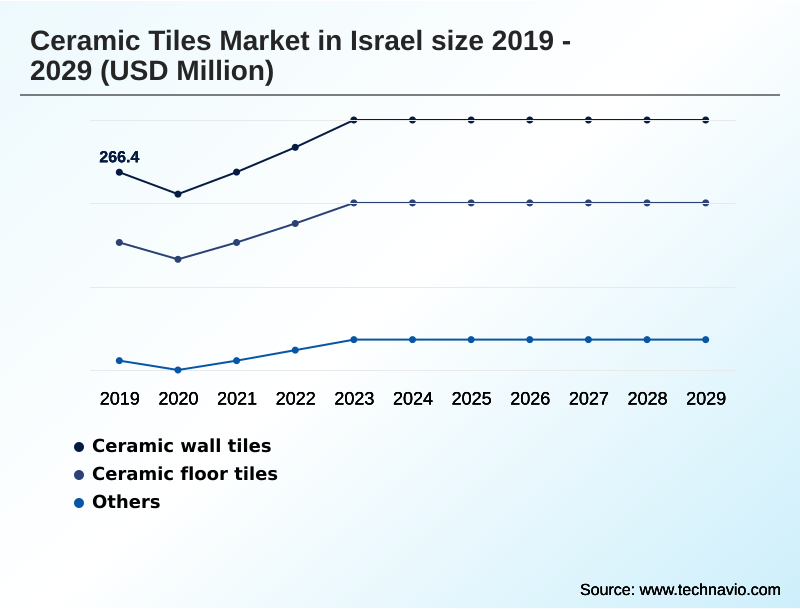

- By Type - Ceramic wall tiles segment was valued at USD 323.6 million in 2024

- By End-user - Residential segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Historic Market Opportunities 2020-2024: USD 522.7 million

- Market Future Opportunities 2025-2030: USD 318.1 million

- CAGR from 2025 to 2030 : 7%

Market Summary

- The ceramic tiles market in Israel is dominated by the residential sector, which accounted for over 67% of demand in 2024. Concurrently, new construction applications represented more than 46% of total tile consumption, underscoring the market's dependence on housing development. A key driver is the government's push for urban renewal projects, which accelerates demand for both functional and decorative tiles.

- However, this growth is constrained by a persistent challenge: a severe labor shortage in the construction industry, with an estimated deficit of 28,000 workers, which delays project timelines and inflates installation costs.

- From an operational standpoint, importers and distributors face the business scenario of balancing large inventory stockpiles to service high-volume construction projects against the risks of supply chain disruptions from geopolitical tensions, which can increase freight costs by up to 20%. This dynamic forces companies to optimize sourcing strategies and manage logistics carefully to maintain profitability.

What will be the Size of the Israel Ceramic Tiles Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Israel Ceramic Tiles Market Segmented?

The israel ceramic tiles industry research report provides comprehensive data (region-wise segment analysis), with forecasts and analysis for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Type

- Ceramic wall tiles

- Ceramic floor tiles

- Others

- End-user

- Residential

- Commercial

- Application

- New construction

- Replacement

- Renovation

- Geography

- Middle East and Africa

- Israel

- Middle East and Africa

How is the Israel Ceramic Tiles Market Segmented by Type?

The ceramic wall tiles segment is estimated to witness significant growth during the forecast period.

The ceramic wall tiles segment, which accounted for over 43% of market revenue in 2024, is heavily influenced by residential applications and renovation projects. This contrasts with ceramic floor tiles, where durability is the primary purchasing driver.

Urban renewal projects, which saw a 10% increase in government-approved units, have significantly boosted demand for wall coverings that offer contemporary aesthetics.

In response, manufacturers are using digital printing technology to create customized designs, while the adoption of thin porcelain tiles that can be applied over existing surfaces reduces installation time.

A growing focus on sustainable building practices is also evident, with increasing demand for tiles made from recycled materials to meet green building certifications and water conservation standards.

The Ceramic wall tiles segment was valued at USD 323.6 million in 2024 and showed a gradual increase during the forecast period.

What are the key Drivers, Trends, and Challenges in the Israel Ceramic Tiles Market?

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- When evaluating flooring and wall solutions, stakeholders analyze the cost of ceramic tiles for residential projects, which varies based on material and origin. The benefits of large-format porcelain tiles, such as a seamless appearance and reduced maintenance, are a key consideration, especially in new construction where they can expedite installation by up to 15% compared to smaller formats.

- For outdoor spaces, identifying durable outdoor ceramic tile options is critical in Israel's climate; these tiles must offer UV protection and slip resistance. For commercial spaces, determining the best ceramic tiles for high-traffic commercial use involves assessing wear ratings and lifecycle costs, with porcelain often being the preferred choice for its superior durability.

- Increasingly, sustainable ceramic tile manufacturing processes are a deciding factor for developers aiming for green building certifications, influencing procurement choices. Similarly, understanding the requirements for ceramic tile installation for underfloor heating is essential in modern residential builds, where system compatibility can affect long-term energy efficiency by as much as 10%.

- These specific use-case considerations guide decisions for architects and developers, shaping demand across different segments.

What are the key market drivers leading to the rise in the adoption of Israel Ceramic Tiles Industry?

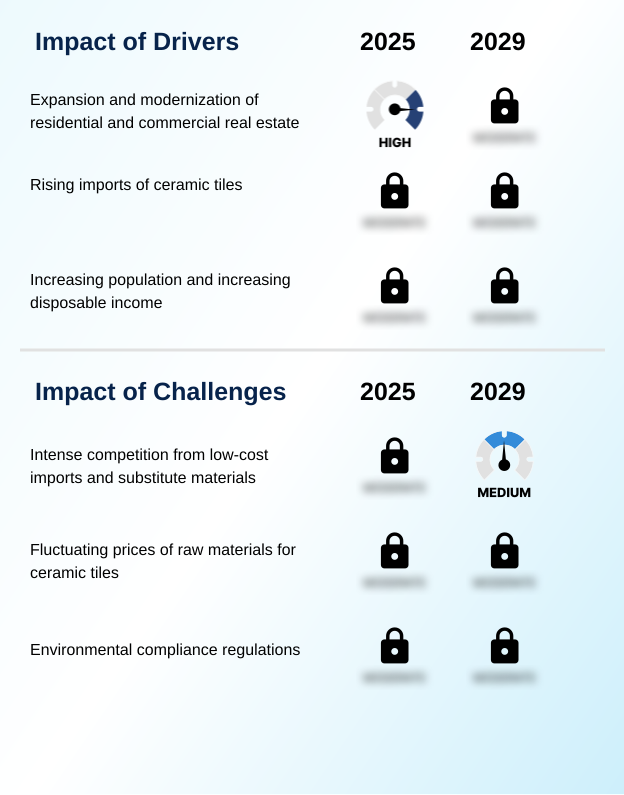

- The resurgence in construction and housing development is a key driver for the ceramic tiles market in Israel.

- The primary driver for the ceramic tiles market in Israel is the resurgence in new construction, with apartment starts recently exceeding 80,000 units annually. This boom in the residential sector directly fuels demand for indoor flooring and wall covering solutions.

- Government initiatives further amplify this driver; for example, urban renewal projects that approved the addition of over 30,000 housing units create large-scale procurement opportunities. These projects often specify ceramic tiles due to their durability and cost-effectiveness over the building's lifecycle.

- This sustained construction activity, particularly in high-density residential applications, provides a stable demand pipeline for sanitaryware and other tile manufacturers and importers, underpinning market growth.

What are the market trends shaping the Israel Ceramic Tiles Industry?

- The increasing popularity of large-format and porcelain tiles is a significant market trend, driven by demand for modern, minimalist designs with seamless aesthetics and enhanced durability.

- A prominent trend in the ceramic tiles market in Israel is the adoption of large-format porcelain tiles, which now account for a significant portion of specifications in high-end projects. These tiles, often exceeding 120cm, reduce grout lines by over 75% compared to traditional sizes, creating a seamless appearance aligned with minimalist designs.

- This shift is enabled by advancements in digital printing technology, which allows for hyper-realistic replications of materials like wood and marble, offering a cost-effective alternative with superior durability. For instance, digitally printed wood-look ceramic planks offer the aesthetic of timber with 100% water resistance, making them ideal for kitchens and bathrooms.

- This customization capability, including high-gloss finishes and terrazzo-inspired tiles, is a key factor driving demand in the renovation sector.

What challenges does the Israel Ceramic Tiles Industry face during its growth?

- Persistent labor shortages in the construction and installation sectors represent a key challenge impacting the industry's growth trajectory.

- A significant challenge confronting the ceramic tiles market in Israel is the persistent labor shortage, with an estimated deficit of 28,000 skilled installers. This gap slows project completion times by an average of 9% and increases installation costs, directly impacting project profitability. Compounding this issue are supply chain vulnerabilities.

- As an import-heavy market, geopolitical tensions can cause freight costs to surge and lead to unpredictable delays, disrupting the availability of critical materials like large-format porcelain tiles and specialized adhesives.

- These logistical hurdles force distributors to hold larger, more expensive inventories of double charge tiles or risk being unable to meet demand from ongoing new construction and renovation projects, thereby constraining market responsiveness.

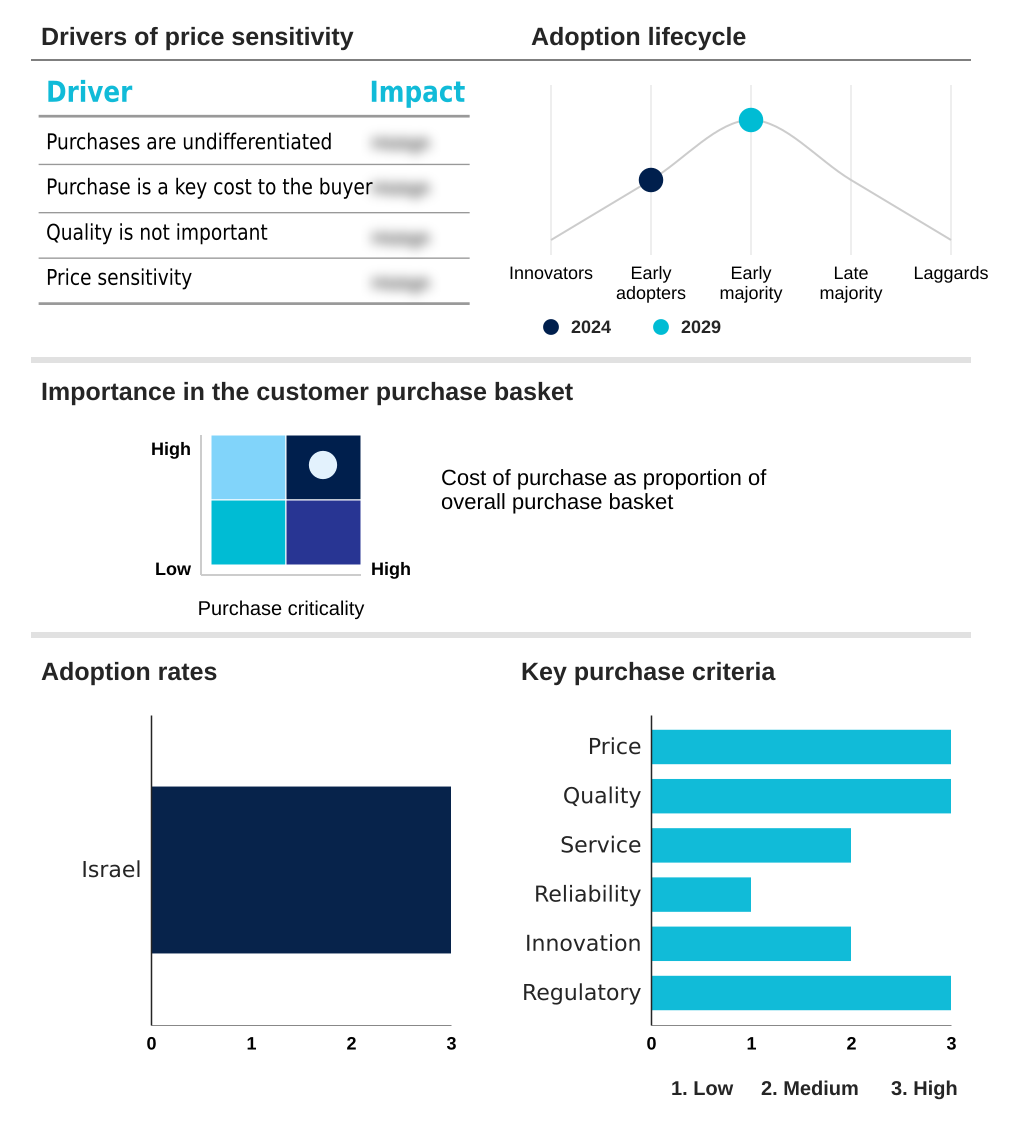

Exclusive Technavio Analysis on Customer Landscape

The israel ceramic tiles market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the israel ceramic tiles market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Israel Ceramic Tiles Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, israel ceramic tiles market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

ABK Group Industrie - The vendor landscape provides a spectrum of ceramic and porcelain tiles, from high-performance architectural solutions and large-format slabs to decorative, design-driven surfaces for residential and commercial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- ABK Group Industrie

- Ceramiche Atlas Concorde Spa

- ceramica cielo s.p.a.

- Ceramica Cleopatra Group

- CERAMICHE CAESAR Spa

- Fea Ceramics

- Gruppo Italcer S.p.A.

- Insca

- LEXIRA SURFACES LLP

- Marazzi Group

- Nueva Alaplana S.L.

- Pastorelli

- PORCELANOSA Grupo AIE

- RAMIRRO CERAMICA LLP

- The Armenian Ceramics Balian

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Market Intelligence Radar: High-Impact Developments & Growth Signals

- In the Construction Materials industry, tightening regulations on carbon emissions and the push for green building certifications are compelling manufacturers to adopt eco-friendly processes. This directly impacts the ceramic tiles market in Israel 2026-2030 by increasing demand for products with high recycled content and lower energy footprints, influencing material sourcing and sustainable building practices.

- The adoption of digital technologies like 3D printing and advanced automation is improving production efficiency and customization capabilities. For ceramic tiles, this translates into more intricate designs via digital printing, reduced waste, and the development of innovative products like thin porcelain tiles, meeting demands from the renovation sector.

- Global supply chain volatility has highlighted the risks of relying on single-source raw materials and long-distance shipping. This forces ceramic tile importers in Israel to diversify their supplier base beyond traditional European sources and manage inventory more strategically to mitigate disruptions and price fluctuations, ensuring cost-effectiveness.

- A marked shift in residential construction toward high-density urban renewal projects and energy-efficient buildings is evident. This drives demand for ceramic tiles that are not only durable for high-traffic environments but also offer properties like thermal insulation, aligning with modern construction needs.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Israel Ceramic Tiles Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 178 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 7% |

| Market growth 2026-2030 | USD 318.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.7% |

| Key countries | Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The ceramic tiles market in Israel operates within an ecosystem heavily reliant on international stakeholders, with over 80% of products being imported. The value chain begins with overseas manufacturers, primarily in Europe, who produce porcelain stoneware and other tiles based on global design trends.

- These products are then brought into the country by distributors who supply to retailers, construction firms, and contractors. Large construction companies, which drive a significant portion of demand in the new construction segment, often procure directly to manage costs for projects requiring thousands of square meters of tiling.

- The final layer consists of installers, whose persistent labor shortage (a deficit of ~28,000 workers) creates significant bottlenecks. This ecosystem is influenced by government bodies that set building standards and urban renewal policies, which can stimulate or redirect demand toward specific products like anti-corrosive ceramic tiles.

What are the Key Data Covered in this Israel Ceramic Tiles Market Research and Growth Report?

-

What is the expected growth of the Israel Ceramic Tiles Market between 2026 and 2030?

-

The Israel Ceramic Tiles Market is expected to grow by USD 318.1 million during 2026-2030, registering a CAGR of 7%. Year-over-year growth in 2026 is estimated at 6.7%%. This acceleration is shaped by resurgence in construction and housing development, which is intensifying demand across multiple end-use verticals covered in the report.

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Ceramic wall tiles, Ceramic floor tiles, and Others), End-user (Residential, and Commercial), Application (New construction, Replacement, and Renovation) and Geography (Middle East and Africa). Among these, the Ceramic wall tiles segment is estimated to witness significant growth during the forecast period, driven by rising adoption across key application areas. Each segment includes detailed qualitative and quantitative analysis, along with historical data from 2020-2024 and forecasts through 2030 with year-over-year growth rates.

-

-

Which regions are analyzed in the report?

-

The report covers Middle East and Africa. Country-level analysis includes Israel, with dedicated market size tables and year-over-year growth for each.

-

-

What are the key growth drivers and market challenges?

-

The primary driver is resurgence in construction and housing development, which is accelerating investment and industry demand. The main challenge is persistent labor shortages in construction and installation, creating operational barriers for key market participants. The report quantifies the impact of each driver and challenge across 2026 and 2030 with comparative analysis.

-

-

Who are the major players in the Israel Ceramic Tiles Market?

-

Key vendors include ABK Group Industrie, Ceramiche Atlas Concorde Spa, ceramica cielo s.p.a., Ceramica Cleopatra Group, CERAMICHE CAESAR Spa, Fea Ceramics, Gruppo Italcer S.p.A., Insca, LEXIRA SURFACES LLP, Marazzi Group, Nueva Alaplana S.L., Pastorelli, PORCELANOSA Grupo AIE, RAMIRRO CERAMICA LLP and The Armenian Ceramics Balian. The report provides qualitative and quantitative analysis categorizing companies as dominant, leading, strong, tentative, and weak based on their market positioning. Company profiles include business segment analysis, SWOT assessment, key offerings, and recent strategic developments.

-

Market Research Insights

- The competitive landscape for the ceramic tiles market in Israel is characterized by a high degree of import reliance, with international brands accounting for over 80% of offerings. Key players like Marazzi Group and Atlas Concorde are focusing on innovation in sustainable materials and advanced digital printing to differentiate their products.

- For instance, recent developments show a push towards large-format porcelain tiles, which now constitute a significant portion of high-end residential specifications. These actions directly address the market's demand for modern, minimalist designs and materials with superior durability for both indoor flooring and outdoor cladding.

- This innovation is crucial for companies to maintain market share amid intense price sensitivity from consumers and competition from substitute materials like vinyl and laminate. Navigating supply chain vulnerabilities, which can add significant logistical costs, remains a primary operational focus for all vendors in this import-driven market.

We can help! Our analysts can customize this israel ceramic tiles market research report to meet your requirements.

RIA -

RIA -