North America Colocation and Managed Hosting Services Market Size 2024-2028

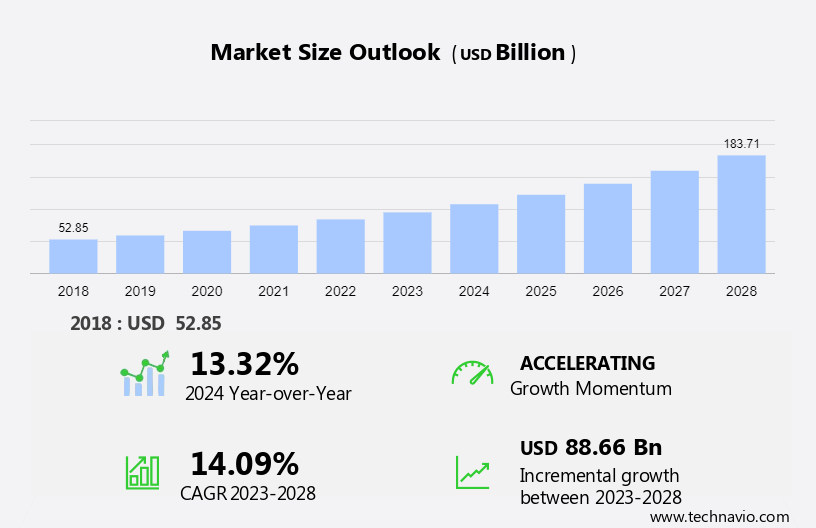

The North America colocation and managed hosting services (CMH) market size is forecast to increase by USD 88.66 billion at a CAGR of 14.09% between 2023 and 2028.

- The market is experiencing significant growth due to several key trends. One major trend is the increasing adoption of cloud-based storage services, which is driving the demand for colocation services as businesses seek to store their data in secure and reliable data centers. Another trend is the increasing focus on data center consolidation, as companies look to reduce costs and improve efficiency by housing multiple servers in a single data center. However, the market is also facing challenges, such as the cost escalation of colocation services due to the need for flexibility and customization. These factors are shaping the growth of the market. The market is expected to continue expanding as businesses seek to optimize their IT infrastructure and improve their data security and availability.

What will be the size of the North America Colocation and Managed Hosting Services Market during the forecast period?

- The market is experiencing strong growth, driven by the increasing demand for dependable and secure solutions In the information technology industry. This market encompasses data centers, regulated cloud providers, and colocation networks that offer leasing space for servers, networking gear, and hardware. The proliferation of IoT devices and edge computing is fueling the need for colocation services, as businesses seek to minimize latency and ensure reliable connectivity. Cloud-based storage systems, AI, and remote monitoring services are also key drivers, enabling businesses to streamline operations and improve efficiency.

- Security remains a top priority, with solutions including biometric access restrictions, surveillance cameras, backup power sources, and managed hosting agreements with security patches and updates. Cooling systems and power supplies are essential components of data centers, ensuring optimal performance and uptime. Overall, the market for colocation and managed hosting services in North America is poised for continued expansion, providing valuable solutions for businesses seeking to optimize their IT infrastructure.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- BFSI

- Communication and IT

- Manufacturing

- Government and public sector

- Others

- Type

- Wholesale

- Retail

- Geography

- North America

- Canada

- Mexico

- US

- North America

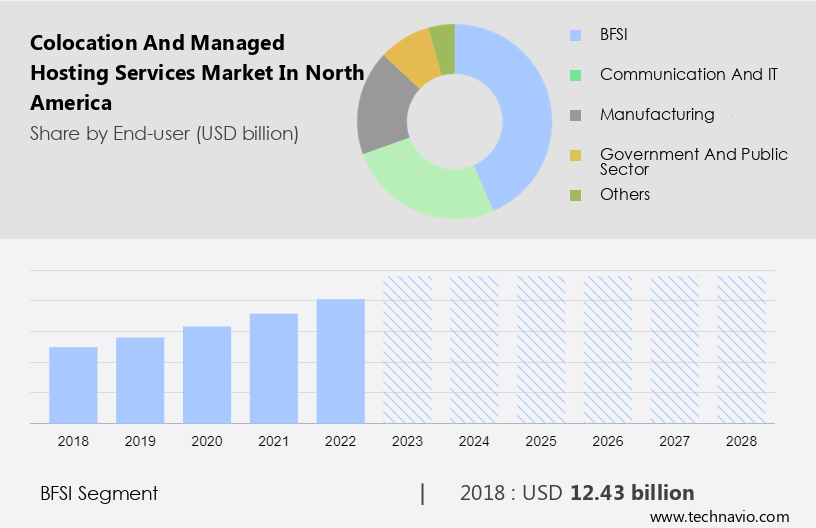

By End-user Insights

- The BFSI segment is estimated to witness significant growth during the forecast period.

Colocation and managed hosting services have gained significant traction in North America, particularly within the banking and financial services industry (BFSI). With the increasing trend of m-commerce and e-commerce, the need for secure and compliant IT infrastructure solutions has become paramount. Colocation facilities and managed hosting providers in North America offer advanced security measures, including firewalls, encryption, intrusion detection, and physical security to safeguard sensitive financial data. These services enable BFSI companies to access an interconnected infrastructure, reduce costs, and ensure a high level of network security and flexibility. Additionally, colocation and managed hosting services cater to various sectors such as IT infrastructure, retail, IT and telecom, government defense, healthcare, energy, media and entertainment, and more.

These providers offer a range of options, including hyper-scale facilities, private enclosures, private suites, build-in suites, wholesale placement rooms, and outsourced colocations. The pricing capacity includes electricity, cooling, IT network, power densities, and virtualization. Moreover, energy efficiency is a significant concern for colocation and managed hosting providers, with solutions such as adaptive control systems, energy-efficient lighting systems, and active airflow management. Uptime flexibility, information technology infrastructure, servers, networking gear, hardware, secure solutions, and dependable solutions are also essential offerings. The integration of cloud services, including cloud-based storage systems, IoT, AI, remote monitoring services, and managed hosting agreements, further enhances the value proposition of colocation and managed hosting services.

Get a glance at the market share of various segments Request Free Sample

The BFSI segment was valued at USD 12.43 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of North America Colocation and Managed Hosting Services Market?

An increase in the adoption of cloud-based storage services is the key driver of the market.

- In North America, the colocation and managed hosting services market is witnessing significant growth due to the increasing adoption of cloud-based storage systems and edge computing. Colocation data centers provide businesses with the flexibility to house their IT infrastructure in a secure and reliable environment, while managed hosting services offer additional benefits such as remote monitoring, security patches, and software updates. IoT devices and AI are driving the demand for low-latency applications and distributed edge sites, which require proximity to data processing capabilities. Colocation networks and hyper scale facilities offer the necessary infrastructure for these applications, including power supplies, cooling systems, and high IT network power densities.

- The Information Technology industry, including IT and Telecom, Retail, Government and Defense, Healthcare, Energy, Media and Entertainment, and IT infrastructure, are major consumers of colocation and managed hosting services. These industries require secure and dependable solutions for their IT facilities, and outsourced colocations offer cost-effective and flexible alternatives to building and maintaining their own data centers. Colocation providers offer various options for leasing space, including private enclosures, private suites, build-in suites, wholesale placement rooms, and virtualization. Pricing capacity is determined by factors such as electricity, cooling, and IT network usage. Energy-efficient lighting systems, adaptive control systems, active airflow management, cold aisle containment, and uptime flexibility are essential features for modern data centers.

What are the market trends shaping the North American colocation and Managed Hosting Services Market?

Increasing focus on data center consolidation is the upcoming trend In the market.

- In North America, the colocation and managed hosting services market is witnessing significant growth due to the increasing demand for IT infrastructure consolidation. Companies are seeking to minimize operational costs by merging data centers or reducing their size. The adoption of a common cloud platform by software companies is also contributing to this trend. Virtualization plays a crucial role in data center consolidation, enabling enterprises to store and process information more efficiently. The one-to-one relationship between physical servers and storage has evolved, allowing for the reduction of procurement of additional storage infrastructure. Moreover, the integration of IoT devices, edge computing, and cloud-based storage systems is driving the need for colocation and managed hosting services.

- Industries such as IT and Telecom, Government and Defense, Healthcare, Energy, Media and Entertainment, and Retail are increasingly relying on these services to manage their IT infrastructure. Hyper-scale facilities, private enclosures, private suites, build-in suites, wholesale placement rooms, and IT facilities are all options available to businesses seeking colocation and managed hosting services. These solutions offer dependable power supplies, cooling systems, biometric access restrictions, surveillance cameras, and backup power sources. Managed hosting agreements provide businesses with security patches, software updates, IT management, cloud integration, and distributed edge sites for low-latency applications. However, concerns around data breaches and privacy are also driving the need for strong network monitoring, threat detection, and incident response capabilities.

What challenges does the North America Colocation and Managed Hosting Services Market face during the growth?

Cost escalation of colocation services due to the need for flexibility is a key challenge affecting the market growth.

- The market is experiencing significant growth due to the increasing demand for IT infrastructure solutions that offer flexibility and efficiency. Data centers are evolving to accommodate the needs of various industries, including IT and Telecom, Retail, Government Defense, Healthcare, Energy, Media and Entertainment, and more. To meet these demands, colocation service providers are investing in hyper-scale facilities, offering private enclosures, suites, build-in suites, wholesale placement rooms, and IT facilities for outsourced colocation. These advanced data centers must support high power densities and offer virtualization, TCO reduction, retrofitting with energy-efficient lighting systems, adaptive control systems, and active airflow management, such as cold aisle containment.

- Uptime flexibility is crucial, and these facilities must provide dependable solutions with secure access through biometric restrictions and surveillance cameras, backup power sources, and managed hosting agreements that include security patches and software updates. Edge computing, a technology that enables IoT solutions, is gaining popularity, necessitating low-latency applications and distributed edge sites. Cloud integration is also essential, as cloud service providers increasingly offer on-premises cloud on-ramps. However, concerns over data breaches and privacy are driving the need for strong network monitoring, threat detection, and incident response. The market dynamics are shaped by the Information Technology industry's continuous evolution, with servers, networking gear, hardware, and secure solutions all requiring colocation and managed hosting services.

Exclusive North America Colocation and Managed Hosting Services Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AT and T Inc.

- China Telecom Corp. Ltd.

- Cogent Communications Holdings Inc.

- Colocation America

- Colt Technology Services Group Ltd.

- CyrusOne LLC

- Digital Realty Trust Inc.

- Equinix Inc.

- Fidelity National Information Services Inc.

- Flexential Corp.

- International Business Machines Corp.

- Iron Mountain Inc.

- Koch Industries Inc.

- Lumen Technologies Inc.

- QTS Realty Trust LLC

- Rackspace Technology Inc.

- TeraGo Inc.

- UnitedLayer LLC

- Verizon Communications Inc.

- Wow Technologies Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market continues to experience significant growth as businesses seek to optimize their IT infrastructure and improve operational efficiency. Colocation services enable organizations to lease space in data centers to house their servers and networking equipment, while managed hosting providers offer additional services such as power, cooling, and IT management. Regulated cloud providers play a crucial role in this market, offering secure solutions for industries with stringent compliance requirements. IoT devices and edge computing are driving the demand for colocation networks, which provide low-latency connections to support real-time data processing. Cloud-based storage systems, AI, and virtualization are transforming IT infrastructure, leading to increased power densities and the need for energy-efficient cooling systems.

Moreover, TCO (Total Cost of Ownership) is a key consideration for businesses evaluating colocation and managed hosting services, with energy costs and uptime flexibility being significant factors. Retrofitting existing facilities with energy-efficient lighting systems, adaptive control systems, and active airflow management is becoming increasingly common to reduce operational expenses and improve sustainability. Cold aisle containment and uptime flexibility are essential features for IT infrastructure, ensuring optimal performance and minimizing downtime. The information technology industry is a major consumer of colocation and managed hosting services, with servers, networking gear, hardware, and secure solutions being critical components of IT infrastructure. Outsourced colocations offer businesses the flexibility to scale their IT infrastructure as needed, without the upfront capital investment and ongoing maintenance costs.

Furthermore, pricing capacity and electricity costs are important considerations for businesses evaluating colocation and managed hosting services. Cooling systems and power supplies are essential components of data center infrastructure, with biometric access restrictions, surveillance cameras, backup power sources, and managed hosting agreements providing additional security and reliability. Security patches and software updates are essential for maintaining the security and performance of IT infrastructure. Cloud integration, distributed edge sites, and on-premises cloud on-ramps are key trends In the market, enabling businesses to leverage the benefits of cloud services while maintaining control over their IT infrastructure. Data breaches and privacy concerns are major challenges for businesses, with network monitoring, threat detection, and incident response being critical components of IT security.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

153 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 14.09% |

|

Market Growth 2024-2028 |

USD 88.66 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

13.32 |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across North America

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -