Commercial Airlines Market Size 2026-2030

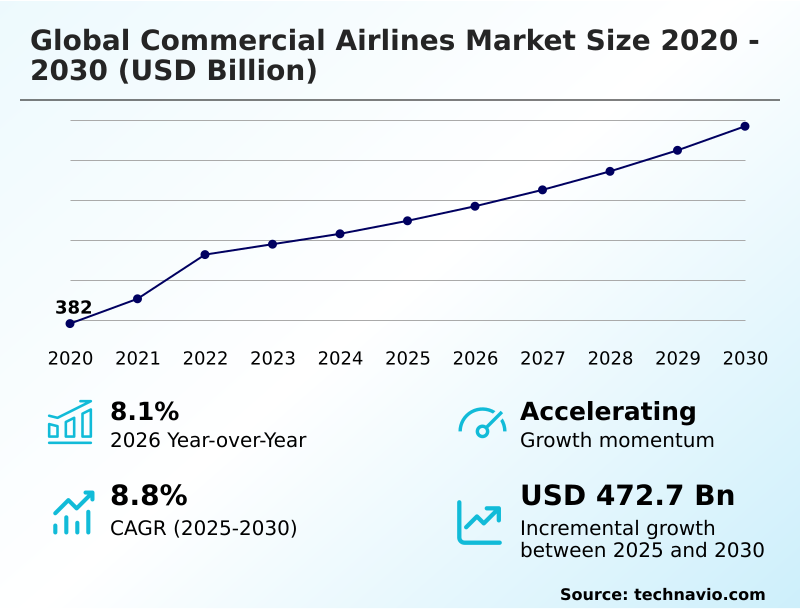

The commercial airlines market size is valued to increase by USD 472.7 billion, at a CAGR of 8.8% from 2025 to 2030. Economic resurgence and infrastructure expansion will drive the commercial airlines market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 44.1% growth during the forecast period.

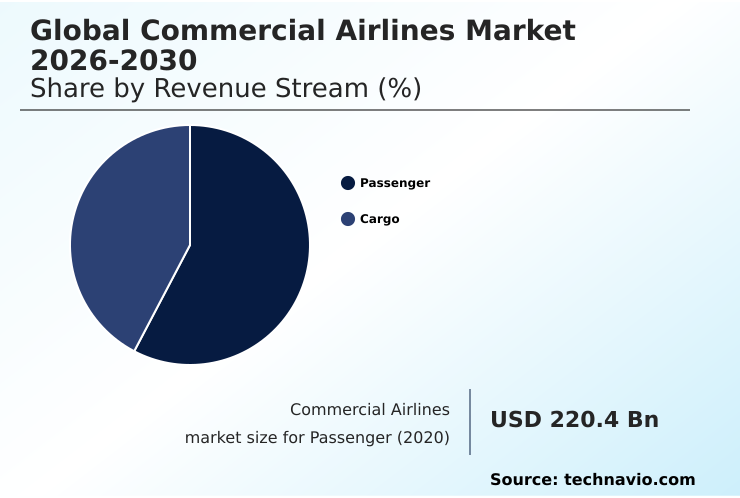

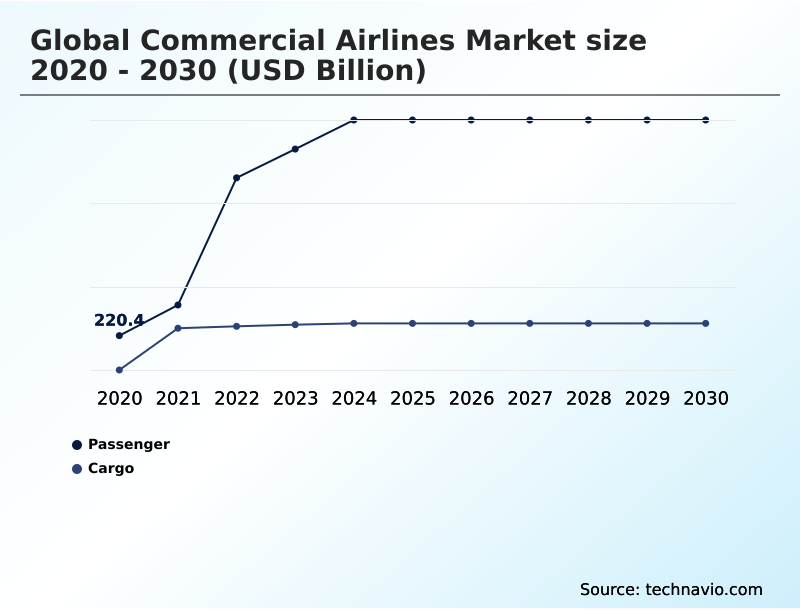

- By Revenue Stream - Passenger segment was valued at USD 589.6 billion in 2024

- By Type - International segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 986.7 billion

- Market Future Opportunities: USD 472.7 billion

- CAGR from 2025 to 2030 : 8.8%

Market Summary

- The commercial airlines market is navigating a period of profound change, balancing robust demand with significant operational and strategic hurdles. A key dynamic is the push toward sustainability, compelling carriers to invest heavily in fleet modernization with aircraft capable of using sustainable aviation fuel.

- This transition is complicated by persistent supply chain fragility and aircraft delivery backlogs, which delay the retirement of older, less efficient jets. Concurrently, advancements in digital transformation are reshaping the industry. For instance, airlines are implementing predictive maintenance protocols using artificial intelligence integration to anticipate component failures, which can reduce unscheduled groundings and optimize MRO services schedules.

- This allows for better capacity utilization and helps mitigate the impact of widespread labor shortages. The industry also grapples with volatile fuel hedging strategies and rising personnel costs, forcing a relentless focus on operational efficiency through sophisticated crew scheduling systems and optimized flight path algorithms.

- The proliferation of the low-cost carrier model continues to pressure legacy airlines, driving innovation in ancillary revenue streams and differentiated premium cabin offerings to maintain profitability across diverse passenger segments.

What will be the Size of the Commercial Airlines Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Commercial Airlines Market Segmented?

The commercial airlines industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Revenue stream

- Passenger

- Cargo

- Type

- International

- Domestic

- Aircraft type

- Narrow body

- Wide body

- Regional and business jet

- Freighter

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- UK

- Spain

- North America

- US

- Canada

- Mexico

- Middle East and Africa

- UAE

- Turkey

- Saudi Arabia

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By Revenue Stream Insights

The passenger segment is estimated to witness significant growth during the forecast period.

The passenger segment remains the core of the commercial airlines market, driven by demand for both leisure and business travel.

This area is seeing significant digital transformation, with an emphasis on creating a seamless touchless passenger journey through advancements in passenger processing systems.

Airlines are leveraging artificial intelligence integration to refine the customer experience platforms, while also investing in pilot training and advanced flight simulators to ensure operational readiness. Investments in new cabin configuration and inflight entertainment are critical for differentiation.

Operational efficiency is a key focus, with strategies targeting a reduction in ground handling services time by up to 15%, directly improving aircraft turnaround.

Successful fleet management hinges on balancing passenger comfort with the economic realities of fuel efficiency and route optimization.

The Passenger segment was valued at USD 589.6 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

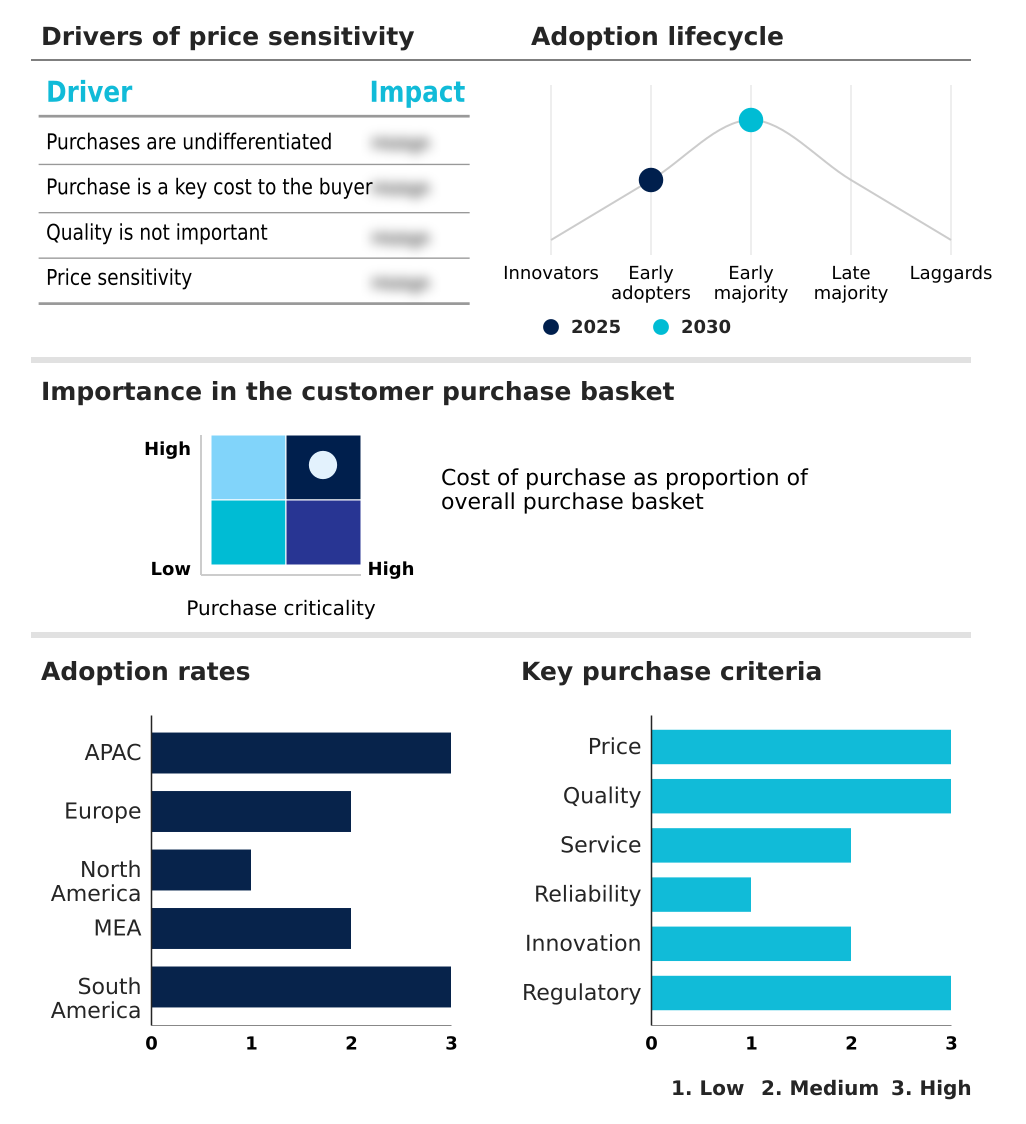

APAC is estimated to contribute 44.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Commercial Airlines Market Demand is Rising in APAC Get Free Sample

The geographic landscape of the commercial airlines market is led by the APAC region, which accounts for over 44% of the projected incremental growth.

This expansion is fueled by strong domestic demand and the expansion of airport infrastructure in key countries.

In contrast, North America and Europe represent mature markets focused on fleet modernization and enhancing operational efficiency through MRO services and advanced air traffic management.

The low-cost carrier model is a significant force globally, driving competition and making air travel more accessible. Airlines worldwide are adopting predictive maintenance to improve reliability, while also managing challenges like fuel hedging strategies and aircraft delivery backlogs.

The development of regional jets and freighter aircraft is also shaping regional connectivity and global air cargo operations, further diversifying market dynamics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the commercial airlines market is increasingly complex, shaped by a confluence of technological, economic, and environmental factors. A primary boardroom focus is the impact of sustainable aviation fuel on operational costs, as carriers weigh the long-term benefits against immediate price premiums.

- This is closely linked to strategies for optimizing airline fleet modernization, where the goal is to balance efficiency gains with capital expenditure. Concurrently, the industry is exploring the technical and infrastructural challenges of hydrogen propulsion in aviation.

- On the operational front, biometric integration for seamless passenger journey is becoming a competitive differentiator, directly linked to the broader digital transformation enhancing airline passenger experience. The use of AI in predictive maintenance for commercial aircraft is crucial for improving reliability and managing maintenance budgets.

- However, these advancements are tempered by the need for managing supply chain fragility in aircraft manufacturing, which can derail fleet renewal timelines. The growth of freighter aircraft in e-commerce logistics continues, with trends in passenger-to-freighter aircraft conversions offering a cost-effective path to capacity expansion.

- Low-cost carrier models for emerging markets are reshaping competitive landscapes, while legacy carriers focus on optimizing ancillary revenue streams for airlines. Behind the scenes, the benefits of airline alliances and codeshare agreements are being maximized to extend network reach. Effective management requires addressing pilot and technician labor shortages and navigating volatility in aviation fuel pricing.

- Success is also dependent on the efficiency of back-end systems, highlighted by the impact of crew scheduling systems on efficiency. Furthermore, improving airline load factors through data analytics, advancements in air traffic management systems, and understanding the economic impact of airport infrastructure expansion are all critical.

- The role of narrow body aircraft in regional connectivity and the deployment of wide body aircraft for long-haul international routes remain central to network planning.

What are the key market drivers leading to the rise in the adoption of Commercial Airlines Industry?

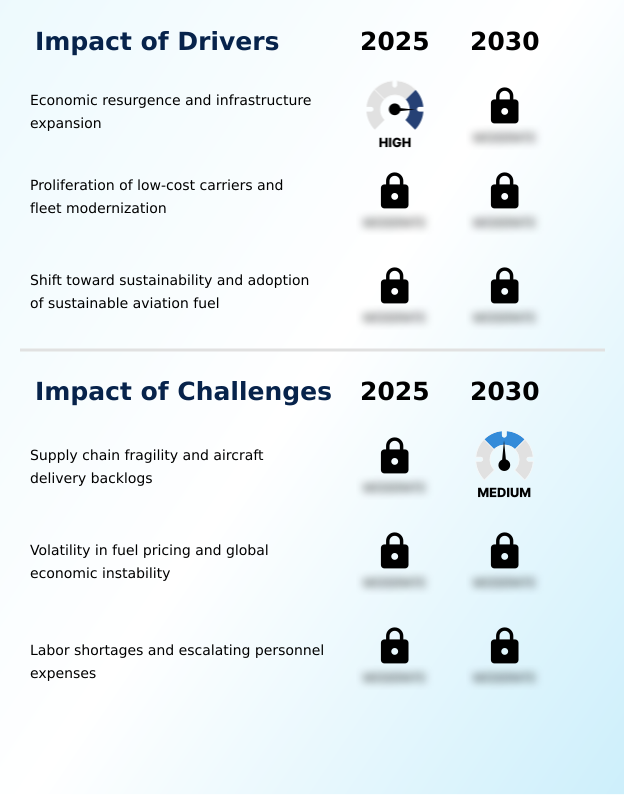

- Economic resurgence, coupled with significant infrastructure expansion, serves as a primary driver for growth within the commercial airlines market.

- Market growth is significantly driven by fleet modernization and the expansion of the low-cost carrier model, which has increased passenger volumes in new markets by over 20% in the initial years of operation.

- Airlines are investing heavily in new aircraft manufacturing to achieve better fuel efficiency, with next-generation narrow body aircraft offering a 15% reduction in consumption compared to previous models.

- This is complemented by expanding airport infrastructure, which enhances connectivity and supports route optimization. The demand for improved passenger transportation services is also pushing carriers to enhance their premium cabin offerings and loyalty programs.

- Strategic airline alliances and investments in MRO services further bolster operational capabilities, while the growth of air cargo operations provides a crucial and expanding revenue stream for carriers globally.

What are the market trends shaping the Commercial Airlines Industry?

- Digital transformation, underscored by the integration of artificial intelligence, is emerging as a pivotal market trend. This evolution is set to redefine operational efficiencies and passenger service standards across the industry.

- Key trends in the commercial airlines market are centered on digitalization and sustainability. The move toward a touchless passenger journey, facilitated by biometric integration and advanced passenger processing systems, is reducing airport wait times by up to 30%. This digital transformation extends to flight operations, where AI-driven flight path optimization is delivering fuel savings of 2-4% on select routes.

- Concurrently, the push for environmental responsibility is accelerating research into hydrogen propulsion and the adoption of carbon offset programs. These initiatives are complemented by investments in modern crew scheduling systems and customer experience platforms, which improve both operational efficiency and passenger loyalty.

- The development of advanced flight simulators is also crucial for addressing industry-wide labor shortages through more effective pilot training, supporting the overall market evolution.

What challenges does the Commercial Airlines Industry face during its growth?

- Supply chain fragility, exacerbated by extensive aircraft delivery backlogs, presents a key challenge that constrains industry growth and operational planning.

- The commercial airlines market confronts significant operational and financial challenges. Persistent supply chain fragility and extensive aircraft delivery backlogs are delaying fleet renewal plans by an average of 18-24 months, forcing carriers to extend the life of older, less efficient aircraft. This exacerbates the impact of volatile fuel prices, which can be mitigated only partially by fuel hedging strategies.

- Furthermore, acute labor shortages across roles from pilots to technicians are driving up operating costs, with personnel expenses now representing nearly 35% of total expenditures for some airlines. These constraints hinder the deployment of both wide body aircraft on long-haul routes and freighter aircraft for cargo, impacting revenue passenger kilometers and overall profitability.

- The industry must navigate these headwinds while continuing to invest in necessary areas like advanced air traffic management.

Exclusive Technavio Analysis on Customer Landscape

The commercial airlines market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the commercial airlines market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Commercial Airlines Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, commercial airlines market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Air Canada - Offers comprehensive aircraft manufacturing solutions, from fuel-efficient platforms to integrated maintenance and digital aviation services, underpinning global fleet modernization efforts.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Air Canada

- Air France KLM SA

- Air India Ltd.

- Airbus SE

- American Airlines Group Inc.

- Cathay Pacific Airways Ltd.

- Delta Air Lines Inc.

- Deutsche Lufthansa AG

- Embraer SA

- Ethiopian Airlines

- International Airlines Group

- Japan Airlines Co. Ltd.

- JetBlue Airways Corp.

- Qatar Airways Group Q.C.S.C.

- Ryanair Holdings plc

- Singapore Airlines Ltd.

- Southwest Airlines Co.

- The Boeing Co.

- The Emirates Group

- United Airlines Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Commercial airlines market

- In August 2024, Southwest Airlines announced an initiative to evaluate hydrogen-based technologies for ground support equipment and future flight potential, signaling a strategic move toward sustainable energy solutions.

- In January 2025, Pegasus Airlines finalized an order for 100 new-generation narrow-body aircraft to expand its operational footprint in European and Middle Eastern markets.

- In February 2025, Delta Air Lines reported the implementation of new fuel hedging strategies and capacity adjustments to mitigate the impact of rising energy costs in the North American market.

- In May 2025, British Airways implemented an expanded biometric boarding system at several international terminals to streamline the departure process and enhance the passenger experience.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Commercial Airlines Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 304 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.8% |

| Market growth 2026-2030 | USD 472.7 billion |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.1% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, Germany, UK, Spain, France, Italy, The Netherlands, US, Canada, Mexico, UAE, Turkey, Saudi Arabia, South Africa, Israel, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The commercial airlines market is at a strategic inflection point, where long-term sustainability goals intersect with immediate operational imperatives. A central challenge for leadership is allocating capital between ambitious fleet modernization programs, essential for integrating sustainable aviation fuel, and the critical digital transformation needed to enhance efficiency.

- While aircraft manufacturing advances, persistent supply chain fragility and aircraft delivery backlogs delay the benefits of next-generation jets. This forces a greater reliance on artificial intelligence integration for predictive maintenance and flight path optimization to extract maximum value from existing assets. For example, carriers leveraging AI have demonstrated an ability to reduce unscheduled maintenance events by over 20%.

- Concurrently, managing labor shortages and deploying effective crew scheduling systems have become as vital as route optimization and refining ancillary revenue streams. The industry's trajectory will be defined by how well companies navigate these competing priorities, from investing in hydrogen propulsion research and pilot training to perfecting the low-cost carrier model and passenger transportation services.

What are the Key Data Covered in this Commercial Airlines Market Research and Growth Report?

-

What is the expected growth of the Commercial Airlines Market between 2026 and 2030?

-

USD 472.7 billion, at a CAGR of 8.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Revenue Stream (Passenger, and Cargo), Type (International, and Domestic), Aircraft Type (Narrow body, Wide body, Regional and business jet, and Freighter) and Geography (APAC, Europe, North America, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Economic resurgence and infrastructure expansion, Supply chain fragility and aircraft delivery backlogs

-

-

Who are the major players in the Commercial Airlines Market?

-

Air Canada, Air France KLM SA, Air India Ltd., Airbus SE, American Airlines Group Inc., Cathay Pacific Airways Ltd., Delta Air Lines Inc., Deutsche Lufthansa AG, Embraer SA, Ethiopian Airlines, International Airlines Group, Japan Airlines Co. Ltd., JetBlue Airways Corp., Qatar Airways Group Q.C.S.C., Ryanair Holdings plc, Singapore Airlines Ltd., Southwest Airlines Co., The Boeing Co., The Emirates Group and United Airlines Inc.

-

Market Research Insights

- The commercial airlines market is characterized by dynamic competitive pressures and a strategic focus on operational excellence. Airlines are leveraging sophisticated revenue management systems to enhance yield, with some carriers reporting improvements of up to 8% on competitive routes. The integration of advanced customer experience platforms is critical for loyalty, improving passenger satisfaction scores by over 15% for early adopters.

- Central to this evolution are investments in modern fleet management and robust airline safety standards. Success depends on optimizing flight operations through airline alliances and effective codeshare agreements, which expand network reach without significant capital outlay.

- Furthermore, efficient baggage handling systems and streamlined passenger processing systems are essential for maintaining high levels of service and capacity utilization at busy airport hubs amid complex aviation regulations and airport slot allocation constraints.

We can help! Our analysts can customize this commercial airlines market research report to meet your requirements.

RIA -

RIA -