Compostable Plastic Market Size 2024-2028

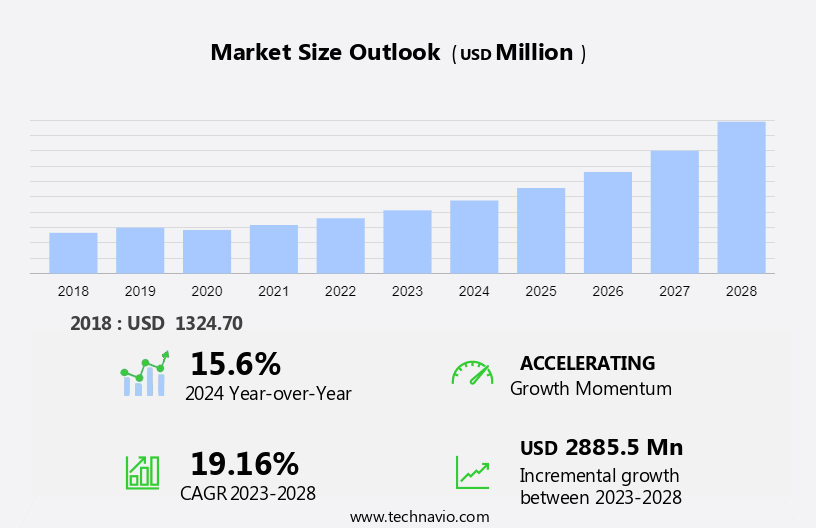

The compostable plastic market size is forecast to increase by USD 2.89 billion at a CAGR of 19.16% between 2023 and 2028. The market is experiencing significant growth due to increasing concerns over plastic pollution and the need for ethical waste management. This trend is particularly prominent in the e-commerce industry, where the demand for environmentally friendly packaging, shipping materials, and mailing bags is on the rise. As online shopping continues to rise, the carbon footprint of delivery services becomes a major concern. In response, governments and businesses are encouraging the adoption of compostable plastics as a sustainable alternative to conventional plastics. However, the high costs associated with compostable plastics remain a challenge, which may hinder their widespread adoption. Key market growth factors include the growing use of compostable packaging and government initiatives encouraging the replacement of conventional plastics. Despite the challenges, the benefits of compostable plastics in reducing plastic pollution make them an attractive option for businesses and consumers seeking to minimize their environmental impact.

The market for compostable plastics is gaining momentum due to increasing environmental concerns and governmental initiatives towards sustainable waste management. These eco-friendly alternatives to conventional plastics are made from biodegradable materials, such as polylactic acid (PLA) and starch-based plastics, which decompose naturally under specific conditions. Municipal waste management is a significant contributor to the compostable plastics market. As governments and organizations focus on reducing landfill waste and promoting green procurement policies, the demand for compostable plastic products, such as bags, containers, and silverware, is on the rise. Biobased products derived from renewable feedstocks like sugarcane and corn starch are increasingly replacing traditional polymers and petrochemical counterparts.

Furthermore, the extraction and refining processes for these plant-based materials and Aerobic and anaerobic decomposition are becoming more efficient, making them a cost-effective alternative to conventional plastics. The compostable plastics market is witnessing growth in various sectors, including electronics, medical, and consumer goods. In the electronics industry, compostable plastics are used in packaging and insulation materials. In the medical sector, they are used for disposable medical equipment and single-use medical devices. Consumer awareness regarding the environmental impact of plastic waste is also driving the demand for compostable plastic packaging in the food and beverage industry. With rising environmental awareness, the demand for plant based materials and bio based materials is increasing, as they offer sustainable alternatives to traditional materials, reducing environmental impact and supporting a more eco-friendly future.

Market Segmentation

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

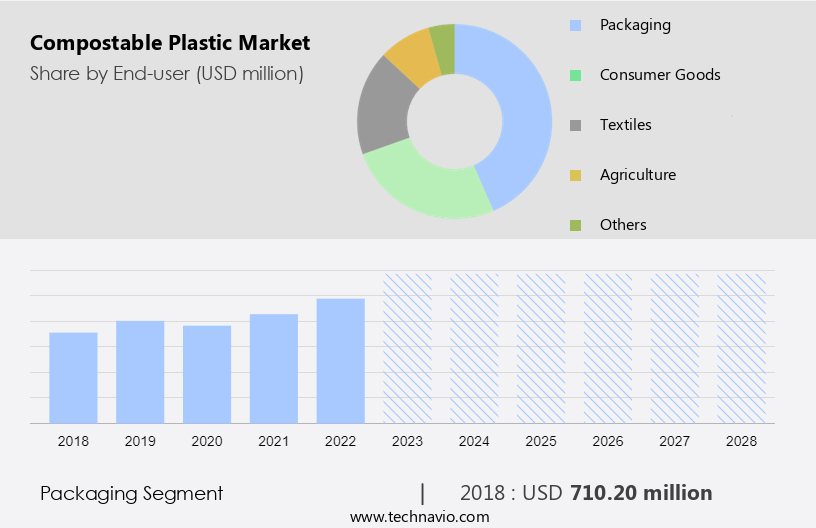

- Packaging

- Consumer goods

- Textiles

- Agriculture

- Others

- Product

- Compostable bag

- Compostable cutlery

- Compostable gloves

- Compostable straw

- Others

- Geography

- Europe

- Germany

- UK

- France

- North America

- US

- APAC

- China

- South America

- Middle East and Africa

- Europe

By End-user Insights

The packaging segment is estimated to witness significant growth during the forecast period. Compostable plastics, also known as biodegradable plastics, have gained significant attention in the US market due to increasing governmental initiatives towards reducing municipal waste and promoting the use of biobased products. Two primary types of compostable packaging are rigid and flexible, which are utilized in various applications such as bottles, cups, pots, films, and bags. The food industry is a significant consumer of compostable packaging, with its usage in fresh food, dry snacks, candy, bakery goods, juice bottles, and meat trays. Additionally, compostable packaging is preferred for premium and branded products with specific requirements. According to industry reports, over 60% of bioplastics are used in packaging applications.

Furthermore, biodegradable plastics, including polylactic acid (PLA) and starch bags, are subjected to various standards such as BS N13432. These plastics are derived from renewable feedstocks like sugarcane and corn. Biobased packaging offers several advantages, including reduced carbon footprint and compatibility with existing recycling infrastructure. The US market for compostable plastics is expected to grow significantly due to increasing consumer awareness and governmental initiatives.

Get a glance at the market share of various segments Request Free Sample

The Packaging segment was valued at USD 710.20 million in 2018 and showed a gradual increase during the forecast period.

Regional Insights

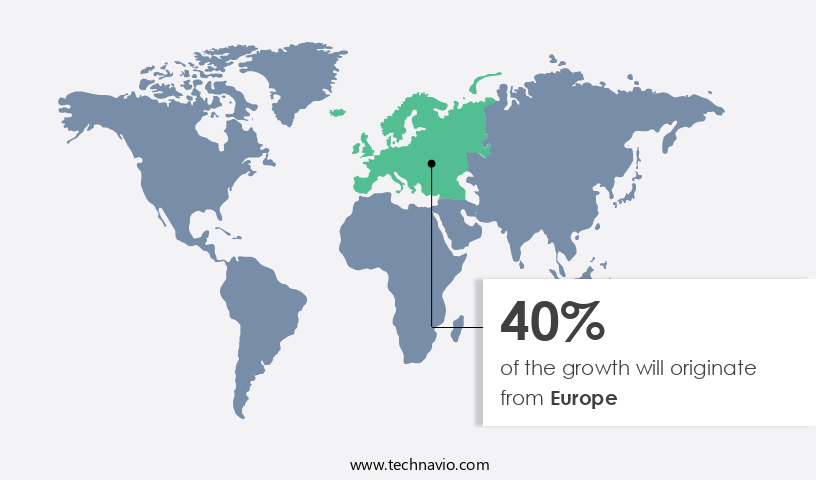

Europe is estimated to contribute 40% to the growth of the global market during the forecast period. Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions Request Free Sample

The market in Europe holds a substantial share in the global industry due to the increasing consumer awareness and environmental concerns. The demand for eco-friendly alternatives to traditional plastic products, such as biodegradable sutures and drug delivery systems, is driving market growth. Europe's commitment to sustainability is further reinforced by governments establishing composting infrastructure to encourage the use of bioplastics. Germany and France are leading markets within Europe, with a significant number of medium and large-sized companies contributing to the industry. The German plastic industry comprises three main sectors: plastic materials production, plastic processing, and plastic machinery production. Key applications of compostable plastics include construction materials, biodegradable insulation, and niche products. As the market continues to expand, it is expected to bring about innovative solutions to address plastic waste concerns.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

Market Driver

Growing use of compostable packaging is the key driver of the market. Compostable plastic packaging has gained significant traction in the business world as a viable alternative to traditional single-use plastic packaging. With increasing environmental consciousness, there is a growing demand for eco-friendly solutions, leading to the compostable packaging industry's expansion.

Furthermore, this growth is driven by large corporations prioritizing sustainability, consumer preferences, and regulatory initiatives such as the EU Single-Use Plastics Directive. Compostable containers, silverware, and bags offer the advantage of biodegrading into carbon dioxide, water, inorganic compounds, and biomass, which can be used as natural fertilizers in agriculture. This end-of-life performance makes compostable packaging an attractive choice for restaurants, grocery shops, and other businesses seeking to reduce their environmental footprint.

Market Trends

Growing government initiatives encouraging replacement of conventional plastics with compostable plastics is the upcoming trend in the market. The global issue of plastic pollution has gained significant attention due to the alarming increase in plastic consumption, particularly in the packaging industry. The environmental impact of plastic use is evident at every stage of its life cycle. Governments and consumers are responding to this crisis by advocating for eco-friendly alternatives to traditional plastic packaging.

Furthermore, bioplastics, also known as compostable plastics, are gaining popularity due to their potential to reduce plastic waste and minimize environmental harm. However, the adoption of these materials is not without challenges. Durability and shelf life are critical considerations in the transportation and use of compostable packaging. Consumer education and labeling are essential to ensure proper disposal and maximize the benefits of using bioplastics. Material technology is advancing to address these challenges, with companies investing in research and development to improve the performance and sustainability of compostable plastics. As the market for compostable packaging continues to grow, it is important for stakeholders to work together to address the complexities of implementing this solution at scale.

Market Challenge

High costs of compostable plastics compared with conventional plastics is a key challenge affecting the market growth. Compostable plastic, an alternative to conventional plastic, is gaining traction in various industries due to growing concerns over plastic pollution and the need for ethical waste management. In the e-commerce sector, particularly online shopping, the demand for environmentally friendly packaging and shipping materials, including mailing bags, is on the rise. However, the production cost of compostable plastic is higher than that of conventional plastic, ranging from 25% to 75%, primarily due to the high polymerization cost. Additionally, most compostable plastic production processes are still in the development stage and have not yet reached economies of scale. Another challenge is the lack of a comprehensive supply chain network at upcoming capacity locations.

Furthermore, the technology behind compostable plastic production is not yet fully convincing as it is still in its infancy, with various raw materials being tested for optimal production. Despite these challenges, the market for compostable plastic is expected to grow as consumers and businesses prioritize reducing their carbon footprint and contributing to sustainable waste management solutions.

Exclusive Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

Green Dot Bioplastics Inc. - The company focuses on offering bio-composites, biodegradable, elastomers, starch composites and wood composites. The key offerings of the company include compostable plastics under its brand RENEW.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- BASF SE

- BEWI ASA

- Biome Technologies plc

- BioTec Bags India Pvt. Ltd.

- BOSK Bioproducts

- Cargill Inc.

- Danimer Scientific Inc.

- Eastman Chemical Co.

- Fkur Kunststoff GmbH

- Futerro SA

- Green Dot Bioplastics Inc.

- Kaneka Corp.

- KURARAY Co. Ltd.

- Mitsubishi Chemical Corp.

- Neste Corp.

- Northern Technologies International Corp.

- Novamont S.p.A.

- SK Chemicals Co. Ltd.

- Toray Industries Inc.

- TotalEnergies SE

- Trinseo PLC

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Biodegradable plastics have gained significant attention in recent years due to growing municipal waste and environmental concerns. The production of biodegradable plastics utilizes renewable feedstocks such as plant-based materials, including polylactic acid (PLA) derived from sugarcane feedstock, and starch bags. The biodegradable plastics market is driven by governmental initiatives and the increasing demand for eco-friendly alternatives to conventional plastics. The BS EN 13432 standard sets the criteria for compostable plastics, ensuring they biodegrade under controlled composting conditions. Biodegradable plastics are used in various industries, including electronics, medical, and construction, for applications such as biodegradable sutures, drug delivery systems, and insulation.

Consumer awareness and ethical waste management practices have led to the adoption of biodegradable plastics in sectors like restaurants, grocery shops, and the e-commerce industry for compostable packaging, silverware, bags, and shipping materials. The durability and shelf life of biodegradable plastics are comparable to their petrochemical counterparts, making them a viable alternative for various applications. The production of biodegradable plastics involves the extraction and refining of plant-based materials, which may include corn starch and the conversion of these materials into biobased polymers. The use of biodegradable plastics reduces plastic pollution and carbon footprint in transportation and material technology applications.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

201 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 19.16% |

|

Market growth 2024-2028 |

USD 2.88 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

15.6 |

|

Regional analysis |

Europe, North America, APAC, South America, and Middle East and Africa |

|

Performing market contribution |

Europe at 40% |

|

Key countries |

US, Germany, UK, France, and China |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

BASF SE, BEWI ASA, Biome Technologies plc, BioTec Bags India Pvt. Ltd., BOSK Bioproducts, Cargill Inc., Danimer Scientific Inc., Eastman Chemical Co., Fkur Kunststoff GmbH, Futerro SA, Green Dot Bioplastics Inc., Kaneka Corp., KURARAY Co. Ltd., Mitsubishi Chemical Corp., Neste Corp., Northern Technologies International Corp., Novamont S.p.A., SK Chemicals Co. Ltd., Toray Industries Inc., TotalEnergies SE, and Trinseo PLC |

|

Market dynamics |

Parent market analysis, market growth inducers and obstacles, market forecast, fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, market condition analysis for the forecast period |

|

Customization purview |

If our market report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Market Research and Growth Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe, North America, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -