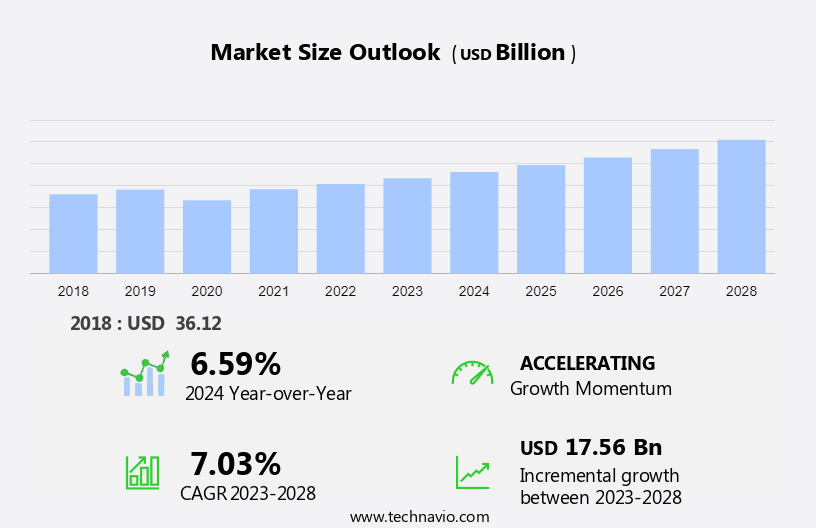

Compound Semiconductor Market Size 2024-2028

The compound semiconductor market size is forecast to increase by USD 17.56 billion at a CAGR of 7.03% between 2023 and 2028. The market's growth rate hinges on various factors, notably the escalating demand for enhanced power density, driven by technological advancements and the proliferation of portable devices. Additionally, the rising adoption of smartphones fuels market expansion, reflecting increased consumer reliance on mobile technology. Moreover, the growing need for enhanced communication networks, driven by evolving connectivity requirements, contributes significantly to market growth, shaping the trajectory of the industry.

The market growth and forecasting report includes key player's detailed analyses of the competitive landscape of the market and information about 20 market companies, including Broadcom Inc., Infineon Technologies AG, IQE Plc, Microchip Technology Inc., Micron Technology Inc., Mitsubishi Electric Corp., Nichia Corp., NXP Semiconductors NV, Qorvo Inc., Qualcomm Inc., Renesas Electronics Corp., Samsung Electronics Co. Ltd., Skyworks Solutions Inc., Sony Group Corp., STMicroelectronics International NV, Texas Instruments Inc., Toshiba Corp., and Wolfspeed Inc. Additionally, Advanced Wireless Semiconductor Co. s key company, offers compound semiconductor such as InGaP HBT, Switch pHEMT, Cu Pillar Bump, 0.5um ED pHEMT, 0.25um ED pHEMT, 0.15um E pHEMT, 0.25um ED BiHEMT, and VCSEL.

What will be the Size of the Market During the Forecast Period?

For More Highlights About this Report, Download Free Sample in a Minute

Market Segmentation By Type, End-user and Geography

The Compound Semiconductor Market exhibits a diverse landscape shaped by various factors. Expenditure in research and development drives innovation, particularly in sectors like aerospace and medical applications. These semiconductors boast superior conductivity and thermal conductivity, critical for advancements such as miniaturization and battery-powered products. The advent of 5G technology underscores the demand for efficient amplifiers and transmission systems. However, challenges such as addressing production complexities persist, highlighting the need for continuous innovation in the market.

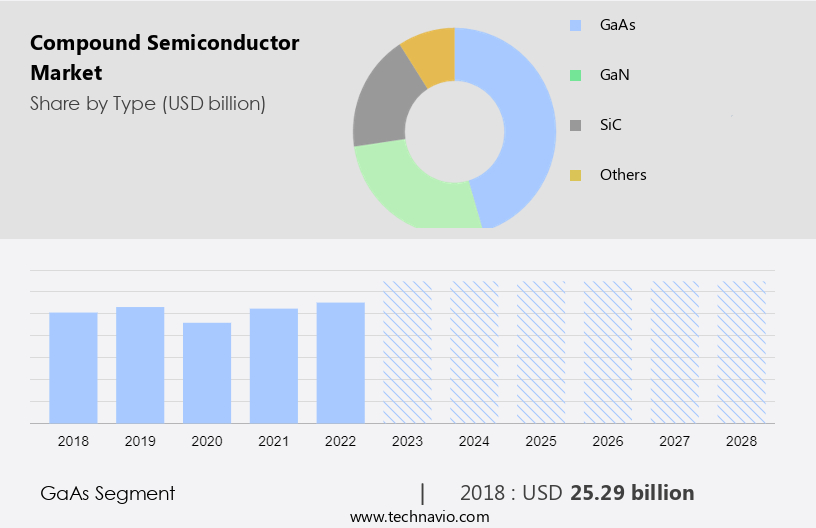

Type Analysis

The GaAs segment is estimated to witness significant growth during the forecast period. The growth of this segment is fuelled by the enhanced durability, efficient power consumption, and superior performance of GaAs components. In addition, these benefits make these components an attractive solution in sectors such as consumer electronics and communications. Furthermore, this will ultimately increase market revenue during the forecast period. However, the share of GaAs components, such as amplifiers and switches, is expected to decline.

Get a glance at the market contribution of various segments Download the PDF Sample

The GaAs segment was the largest segment and was valued at USD 25.29 billion in 2018. Moreover, this is primarily due to the saturation of the global smartphone market, which is a major revenue contributor for GaAs components. In addition, GaAs-based semiconductors hold a major share of the global compound semiconductor market. Furthermore, this is because they are widely used in smartphones and have witnessed a high demand in recent years, proportionally with the growth of the smartphone industry. In addition, the need for GaA components is rising because of the rapid development of wireless communication devices. Hence, such factors are fuelling the growth of this segment which in turn drives the market during the forecast period.

End-user Analysis

The growing adoption of smartphones will fuel the consumer electronics segment, which in turn will increase the market. Smartphones comprise power amplifiers and switches that generally use GaAs. In addition, with the increasing global smartphone shipments, the demand for GaAs components will also rise during the forecast period. Most of the content in a handset is made of silicon, but power amplifiers and switches use GaAs devices. Moreover, prominent smartphone vendors, such as Apple and Samsung Electronics, are increasingly using GaAs-based amplifiers and switches in their new products. In addition, consumer electronic devices are the largest source of energy consumption. Hence, such factors are fuelling this segment which in turn drives the market during the forecast period.

Regional Overview

For more insights on the market share of various regions Download PDF Sample now!

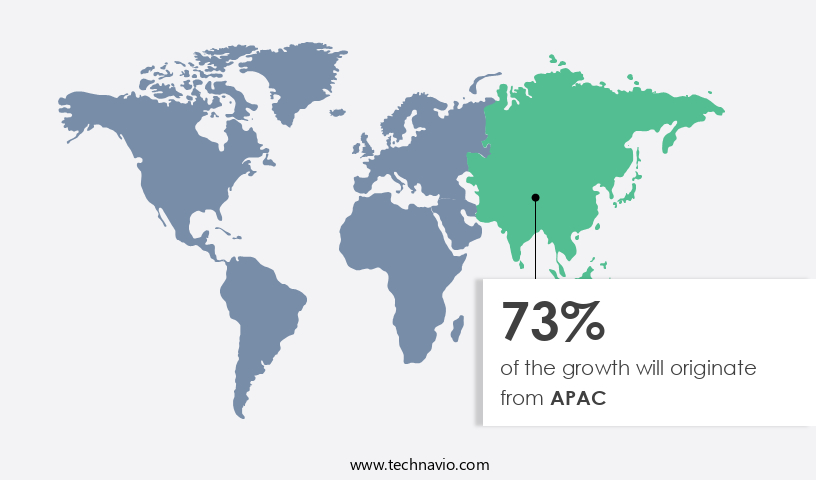

APAC is estimated to contribute 73% to the growth of the global market during the forecast period. Technavio's analysts have provided extensive insight into the market forecast, detailing the regional trends and drivers influencing the market's trajectory throughout the forecast period. The growing urbanization coupled with stable economic growth, the increasing presence of automotive manufacturers, coupled with the increasing demand for advanced automobiles, the growing demand for semiconductors from the aerospace, electronics, and other end-user industries in developing countries such as China and India, and the presence of global and local companies are the major factors driving the market in APAC. In addition, the demand in the urban population, coupled with stable economic growth, has increased the demand for passenger cars integrated with advanced automotive components such as silicon carbide (SiC) for energy efficiency, which is fueling the compound semiconductor market in the region. Moreover, automobile manufacturers such as Mahindra and Mahindra Ltd., Tata Motors Ltd., Isuzu Motors Ltd., Mitsubishi Motors Corp., Nissan Motor Co. Ltd., and Suzuki Motor Corp. have a major presence in APAC. Hence, such factors are driving the market in APAC during the forecast period.

Market Dynamics and Customer Landscape

The compound semiconductor market is experiencing significant growth across various sectors including telecommunications, electronics, and consumer goods. group III-V segment and group IV-IV segment, along with materials like Gallium Phosphide (GaP), are pivotal in the development of high-performance devices for wireless communication technologies and power electronics. These semiconductors, known for their superior breakdown electric field strength and suitability for high-voltage applications, are crucial in RF components, solar inverters, and power supplies. The GaN ecosystem and silicon-based devices drive innovation in the compound semiconductor industry, addressing the increasing device complexity and performance demands in sectors such as Defense & Aerospace, Healthcare, and Information and Communication Technology. As the demand for advanced semiconductor wafers and epitaxial materials grows, the compound semiconductor market continues to expand globally.

Key Market Driver

The market is witnessing robust growth, driven by escalating demand for superior power density across various industries like the automotive, aerospace, and consumer electronics sectors. This demand surge is fueled by the need for heightened productivity and additional functionalities in compound semiconductor applications, necessitating elevated power densities. Compound semiconductor materials, renowned for their unique properties, including high temperature resistance and thermal conductivity, are pivotal in addressing these requirements, particularly in critical sectors like aerospace and medical industries. As the industry continues its trajectory towards miniaturization and adopts technologies like 5G, the importance of compound semiconductors becomes even more pronounced. This dynamic landscape, marked by increased expenditure and evolving semiconductor requirements, is driving the market growth significantly during the forecast period, with technological advancements and innovation in electric vehicles and LED technology playing crucial roles.

Significant Market Trends

The growing adoption of renewable energy sources is an emerging trend in the market. The growing focus on renewable energy sources will fuel the market. In addition, renewable energy is expected to produce more than one-fourth of global gross power generation. Furthermore, governments in several countries are making renewable energy a part of their long-term development strategies.

Moreover, the expense of renewable sources such as solar and wind energy has been reduced by more than 50% over the past decade because of technological improvements and economies of scale. In addition, this tremendous implementation of renewable electricity sources is inducing opportunities for business for compound semiconductors, especially SiC devices and GaN. Furthermore, several other countries are deploying ways to encourage clean energy production as it helps in reducing the carbon footprint. Hence, such factors are driving the market growth during the forecast period.

Major Market Restrain

Manufacturing complexities of compound semiconductors are a major challenge hindering the market. Compound semiconductor technology has a complex manufacturing procedure that needs high-end equipment and highly skilled labor. In addition, companies need to invest heavily in R&D to solve complexities regarding manufacturing and mass production to address the rising demand for compound semiconductors and to get the benefit of economies of scale.

Moreover, compound semiconductor fabrication requires many processing steps, starting with the preparation of substrates. In addition, the following processing steps may include the epitaxial growth of a thin semiconductor layer, etching and lithography, ion implantation, deposition techniques, and deposition of metallic conductors. Furthermore, compound semiconductors require special crystal growth methods and processing procedures for further development. Hence, such factors are hindering the market during the forecast period.

Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market research and growth, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth and trends strategies.

Global Market Customer Landscape

MarketPlayers

Companies are implementing various strategies, such as strategic alliances, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

AXT Inc: The company offers compound semiconductors for major electronic and opto electronic applications and a line of industry critical raw materials.

Market analysis and report of qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Segment Overview

The market research report provides comprehensive data (region wise segment analysis), with forecasts and estimates in "USD Billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Type Outlook

- GaAs

- GaN

- SiC

- Others

- End-user Outlook

- Consumer electronics

- Communications

- Defense and aerospace

- Automotive

- Others

- Region Outlook

- North America

- The U.S.

- Canada

- Europe

- The U.K.

- Germany

- France

- Rest of Europe

- APAC

- China

- India

- South America

- Chile

- Argentina

- Brazil

- Middle East & Africa

- Saudi Arabia

- South Africa

- Rest of the Middle East & Africa

- North America

You may also be interested in:

- Semiconductor Market - Semiconductor Market Analysis North America, APAC, Europe, Middle East and Africa, South America - US, China, India, Germany, France - Size and Forecast

- Vietnam - Semiconductors Market - Vietnam - Semiconductors Market by Application, End-user, and Device - Forecast and Analysis

- Semiconductor Manufacturing Equipment Market - Semiconductor Manufacturing Equipment Market Analysis APAC, Europe, North America, Middle East and Africa, South America - US, China, India, Taiwan, Germany - Size and Forecast

Market Analyst Overview

The market is experiencing a surge in demand driven by innovation in electric vehicles (EVs), renewable energy industry, and wireless communications. Key drivers include investment in semiconductor fabrication facilities and government initiatives promoting infrastructure development and green charger stations. These initiatives are bolstered by investments from commercial enterprises and government in 5G networks and IoT adoption. The market sees a rise in compound semiconductors like gallium nitride (GAN) and gallium arsenide (GaAs), offering high electron mobility and heat resistance. Moreover, integration of semiconductor components in smart technologies and wearable technology is driving market growth. With unique properties like temperature stability and wide bandgap, compound semiconductors are poised to revolutionize industries ranging from consumer electronics to aerospace & defense. The Automotive industry, Aerospace industry, and consumer electronics industries, along with factory floor operations, rely on various elements. Key driving factors in these sectors include innovation, demand for efficiency, and technological advancements. Understanding the Periodic Table of Elements is crucial for optimizing processes and developing cutting-edge products in these fields.

Moreover, the market is experiencing substantial growth, driven by a myriad of factors across industries such as aerospace, automobile, consumer electronics, and solar photovoltaic energy. Key drivers include advancements in Gallium Nitride (GaN)-based transistors, high electron mobility transistors (HEMTs), and optoelectronic components. Innovations in atomic layer deposition (ALD) and chemical vapor deposition (CVD) enable precise fabrication of semiconductor materials like Gallium Phosphide (GAP) and Indium Phosphide (INP). This market growth is further propelled by investments in semiconductor fabrication facilities, facilitating the production of cutting-edge integrated circuits (ICs) and radio frequency devices. Additionally, the proliferation of 5G subscriptions and Internet of Things (IoT) devices drives demand for wide bandgap semiconductors and high-frequency components. With everlight on the horizon, the compound semiconductor market continues to expand, offering solutions for edge computing systems, optical data processing, and quantum computing technologies.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 7.03% |

|

Market Growth 2024-2028 |

USD 17.56 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

6.59 |

|

Regional analysis |

APAC, North America, Europe, South America, and the Middle East and Africa |

|

Performing market contribution |

APAC at 73% |

|

Key countries |

US, China, Japan, South Korea, and Germany |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

|

Key companies profiled |

Advanced Wireless Semiconductor Co., AXT Inc., Broadcom Inc., Infineon Technologies AG, IQE Plc, Microchip Technology Inc., Micron Technology Inc., Mitsubishi Electric Corp., Nichia Corp., NXP Semiconductors NV, Qorvo Inc., Qualcomm Inc., Renesas Electronics Corp., Samsung Electronics Co. Ltd., Skyworks Solutions Inc., Sony Group Corp., STMicroelectronics International NV, Texas Instruments Inc., Toshiba Corp., and Wolfspeed Inc. |

|

Market dynamics |

Parent market analysis, Market growth inducers and obstacles, Fast-growing and slow-growing segment analysis, COVID-19 impact and recovery analysis and future consumer dynamics, and Market condition analysis for the forecast period. |

|

Customization purview |

If our report has not included the data that you are looking for, you can reach out to our analysts and get segments customized. |

What are the Key Data Covered in this Compound Semiconductor Market Research Report?

- CAGR of the market report forecast during the forecast period

- Detailed information on factors that will drive the growth of the market between 2023 and 2028

- Precise estimation of the market size and its contribution to the market in focus on the parent market

- Accurate predictions about upcoming trends and changes in consumer behavior

- Growth of the market industry across APAC, North America, Europe, South America, and the Middle East and Africa

- Thorough market analysis and report of the market’s competitive landscape and detailed information about companies

- Comprehensive market growth analysis of factors that will challenge the growth of Industry companies

We can help! Our analysts can customize this market research report to meet your requirements. Get in touch

RIA -

RIA -