Copper Market Size 2026-2030

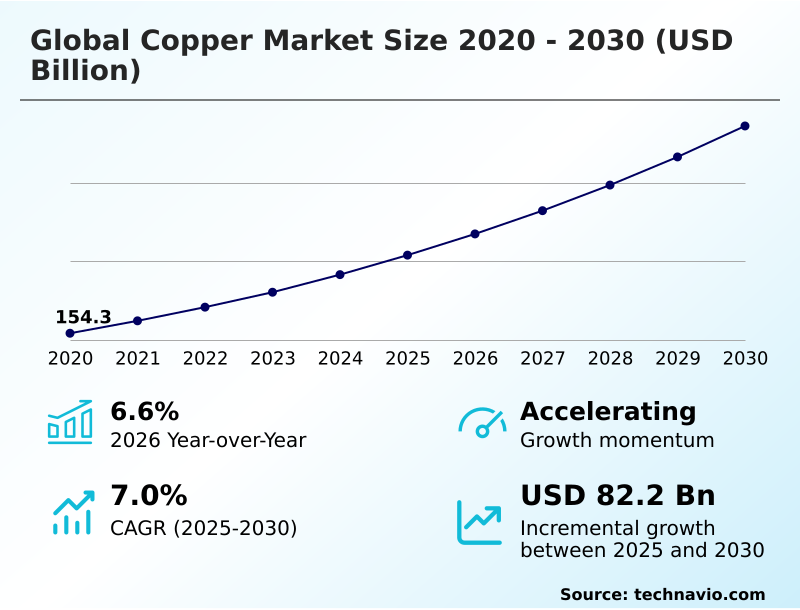

The copper market size is valued to increase by USD 99.13 billion, at a CAGR of 6.8% from 2025 to 2030. Structural grades in global primary mine production will drive the copper market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 70.8% growth during the forecast period.

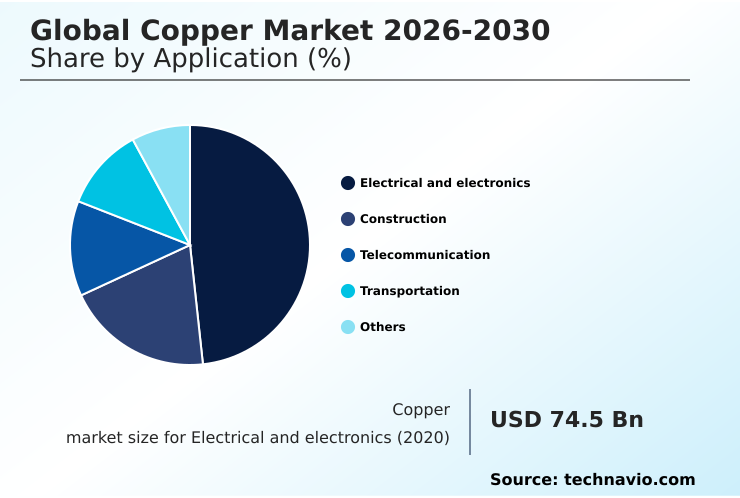

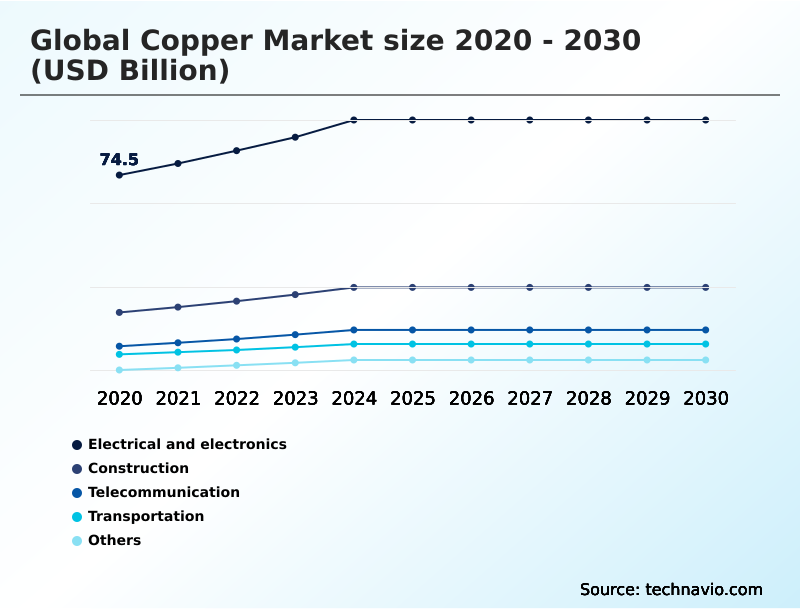

- By Application - Electrical and electronics segment was valued at USD 76.95 billion in 2024

- By Type - Primary segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 151.37 billion

- Market Future Opportunities: USD 99.13 billion

- CAGR from 2025 to 2030 : 6.8%

Market Summary

- The Copper Market is navigating a period of significant structural tightening, characterized by a growing divergence between the accelerating requirements of the energy transition and the persistent operational challenges facing primary extraction.

- The material remains the fundamental conductor for the electrification of the economy, acting as an indispensable material for renewable energy systems, electric vehicle infrastructure, and the massive expansion of smart grid infrastructure.

- However, the supply side is under increasing strain due to declining ore grades at long-life mines, escalating energy costs for pyrometallurgical smelting, and the technical complexity of developing new projects. Consequently, the industry is witnessing a profound shift toward the circular economy, with secondary copper recovery and urban mining technologies becoming critical.

- As a business scenario, a manufacturer of HVDC submarine cables must now balance the need for high-purity copper cathodes against supply chain volatility, increasingly using predictive maintenance in mining data and digital twin modeling to forecast availability and secure long-term contracts for copper concentrate supply, mitigating risks associated with geologic disruptions and resource nationalism.

- This evolution ensures copper maintains its status as a strategic critical mineral, essential for global decarbonization goals.

What will be the Size of the Copper Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Copper Market Segmented?

The copper industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Application

- Electrical and electronics

- Construction

- Transportation

- Telecommunication

- Others

- Type

- Primary

- Secondary

- Product type

- Wire

- Tube

- Flat rolled products

- Rods and bars

- Foil

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- France

- UK

- North America

- US

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Colombia

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- Rest of World (ROW)

- APAC

By Application Insights

The electrical and electronics segment is estimated to witness significant growth during the forecast period.

The electrical and electronics segment is foundational, driven by copper's unmatched conductivity. Demand for high-purity copper cathodes and advanced materials like electrodeposited copper foil is intensifying, particularly for power distribution in data centers supporting AI, where electromigration resistance is key.

The proliferation of high-performance computing requires vast quantities of copper interconnects and efficient thermal management systems using inner-grooved copper tubes.

This demand is creating new, high-volume consumption channels, with some applications seeing a 28% increase in material specification upgrades to support high-frequency environments.

The push for miniaturization in semiconductors also relies on rolled copper foil and copper-tin alloys for reliable interconnects, while digital transformation in mining ensures a steady supply of these critical materials for legacy mining operations and modern high-voltage power transmission systems.

The Electrical and electronics segment was valued at USD 76.95 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

APAC is estimated to contribute 70.8% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Copper Market Demand is Rising in APAC Get Free Sample

The geographic landscape is shifting as regions prioritize domestic supply chain resilience and mineral security initiatives.

In North America, policy-driven inventory strategies have led to events such as a 28% increase in imports from specific trade partners ahead of anticipated tariffs.

APAC remains a consumption powerhouse, but its role is evolving toward advanced processing and urban mining technologies. In South America, binational mining treaties and green mining initiatives are enabling the development of complex ore bodies using advanced hydrometallurgical solvent extraction.

Meanwhile, the Middle East is securing upstream assets to support its own infrastructure goals.

This global recalibration is driven by the need to secure materials like oxygen-free high-conductivity copper and copper-clad aluminum wire for energy and tech sectors, reflecting a complex interplay of geology and geopolitics.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The future of the copper market is inextricably linked to global megatrends, with the impact of AI on copper demand and the soaring copper demand for data center cooling creating new consumption frontiers.

- The role of copper in electric vehicle batteries is particularly critical, with copper foil for lithium-ion battery anodes being a key component driving material specifications and purity requirements. A crucial industry debate remains copper vs aluminum in power transmission, where copper’s superior conductivity is weighed against aluminum's cost and weight advantages.

- Concurrently, advanced copper recycling technology trends are gaining strategic importance to address the challenges in primary copper mine production and bolster the strategic importance of secondary copper supply. The impact of decarbonization on copper consumption is profound, increasing the copper intensity in renewable energy systems and highlighting the importance of sustainable copper mining and ESG factors.

- This is seen in applications from optimizing copper use in HVAC systems to developing new copper alloys for high-speed rail infrastructure. Ultimately, the market is navigating copper price volatility and supply disruptions, the tariff impact on global copper trade, and the talent shortage in copper mining industry.

- These factors shape everything from the production of high-purity copper in semiconductor manufacturing to copper's role in smart grid modernization.

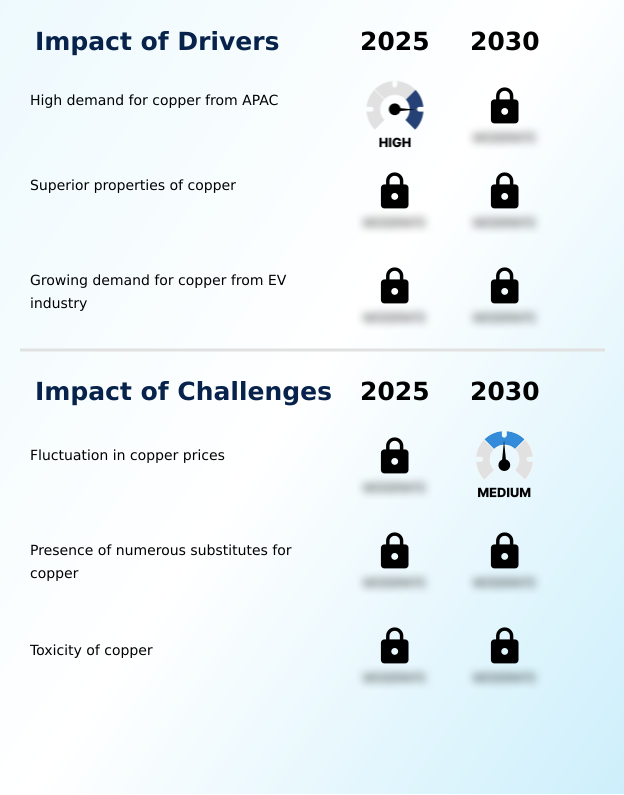

What are the key market drivers leading to the rise in the adoption of Copper Industry?

- Declining structural grades in global primary mine production are a significant driver, creating supply constraints that directly influence market pricing and investment strategies.

- The global energy transition is a primary driver, with massive investment in smart grid infrastructure and energy interconnectors demanding unprecedented volumes of copper.

- Electrification is a key factor, with electric vehicles requiring up to four times more copper than conventional cars, driving demand for 800-volt architectures and related components.

- This consumption is amplified by the build-out of data centers for AI, which places immense stress on power systems.

- To meet this need, the industry is advancing green mining initiatives and adopting technologies like gearless mill drive technology and ring-geared mill drive systems.

- These advanced grinding solutions, part of a broader push for digital transformation in mining, improve efficiency and help manage the challenge of declining ore grades and support the expansion of high-voltage power transmission networks.

What are the market trends shaping the Copper Industry?

- A widening structural deficit is fundamentally reshaping the market landscape. This is compelling nations to engage in strategic stockpiling of copper, now viewed as a critical asset for energy security and defense readiness.

- Market dynamics are increasingly shaped by structural deficit dynamics and the rise of strategic national stockpiling, transforming copper into a strategic asset. CRM Act compliance and a focus on allied supply chains are intensifying as nations pursue mineral security initiatives to counter resource nationalism. This has spurred investment in deep-sea mining exploration and technologies that deliver a low-carbon production footprint.

- For instance, advancements in secondary copper recovery reduce energy use by up to 85% compared to primary extraction. This trend, coupled with the development of pyrometallurgical smelting and froth flotation process optimizations, reflects a market where supply security and sustainability are paramount, influencing everything from copper cathode production to the sourcing of copper-silver alloys.

What challenges does the Copper Industry face during its growth?

- Escalating trade protectionism and the increasing complexity of tariff regulations present a key challenge, threatening the stability and efficiency of the global supply chain.

- Key challenges revolve around supply chain integrity and operational capacity, with structural supply imbalances and geologic disruptions creating significant volatility. The industry confronts escalating trade protectionism policies and complex tariff regulatory complexity, which fragment the global market.

- Furthermore, an interdisciplinary talent scarcity hinders the full implementation of advanced systems like autonomous hauling fleets and automated drilling systems in legacy mining operations. This skills gap is cited by 77% of executives as a primary barrier to digital strategies.

- Overcoming these hurdles requires investment in both technology and human capital to enhance domestic supply chain resilience, improve ESG reporting benchmarks, and create a more robust data-liquid mining ecosystem.

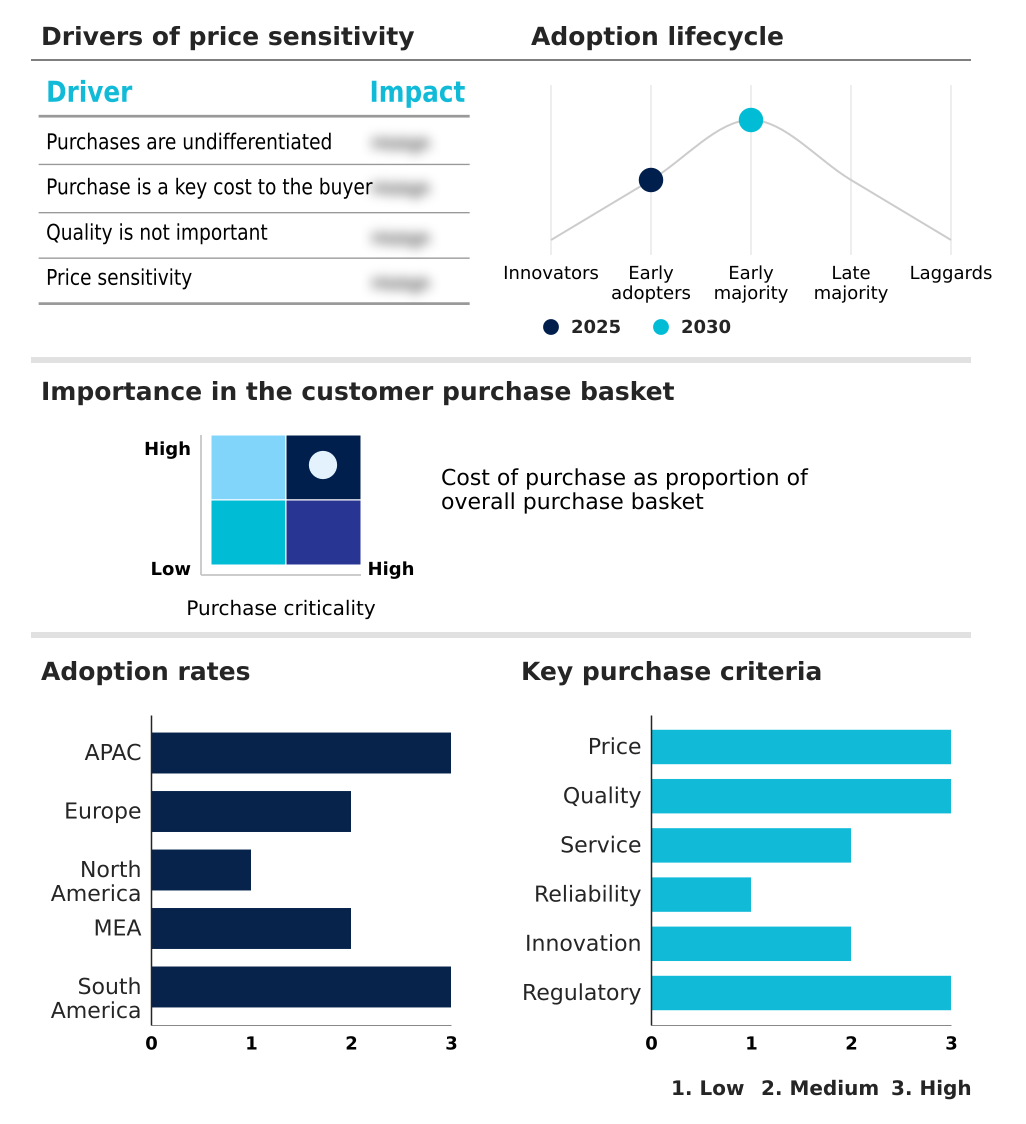

Exclusive Technavio Analysis on Customer Landscape

The copper market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the copper market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Copper Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, copper market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Aeris Resources Limited - Analysis indicates a focus on producing copper concentrates, refined cathodes, and a diversified mining portfolio for global industrial markets.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Aeris Resources Limited

- Anglo American plc

- Antofagasta plc

- Aurubis AG

- BHP Group Ltd.

- Boliden Group

- Capstone Copper Corp

- Freeport McMoRan Inc.

- Glencore Plc

- Hindustan Copper Ltd.

- Jiangxi Copper Corp

- KGHM Polska Miedz

- Lundin Mining Corp.

- MMG Ltd.

- Rio Tinto Ltd.

- Sandfire Resources Limited

- Southern Copper Corp.

- Sumitomo Metal Mining Co. Ltd.

- Teck Resources Ltd.

- Vale SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Copper market

- In December 2025, Glencore Plc reaffirmed its copper-led growth strategy, prioritizing low-capital projects at its Katanga complex to meet long-term production goals without pursuing large-scale mergers.

- In January 2026, BHP Group Ltd. raised its copper production guidance for the fiscal year, citing record throughput at the Escondida mine and continued development of the Vicuna project.

- In February 2026, Anglo American plc adjusted its production outlook to align with development phases at its Collahuasi and Quellaveco sites, confirming the temporary restart of a second plant at Los Bronces.

- In April 2026, Antofagasta plc maintained its annual targets despite lower processing rates, underscoring its focus on advancing the Centinela Second Concentrator Project.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Copper Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 313 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 6.8% |

| Market growth 2026-2030 | USD 99131.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 6.4% |

| Key countries | China, India, Japan, South Korea, Indonesia, Australia, Germany, France, UK, Italy, The Netherlands, Spain, US, Canada, Mexico, Brazil, Argentina, Colombia, Saudi Arabia, UAE, South Africa, Turkey and Israel |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The copper market is defined by the convergence of electrification and digitalization, creating intense, sustained demand. This is occurring alongside significant supply-side pressures from declining ore grades and the high capital costs of new mine development. The industry's response involves a deep focus on operational efficiency through technologies like pyrometallurgical smelting, hydrometallurgical solvent extraction, and the SX-EW process.

- The adoption of gearless mill drive technology, autonomous hauling fleets, and ring-geared mill drive systems is becoming standard. A key boardroom decision revolves around the strategic pivot to circularity, with secondary copper recovery and urban mining technologies offering a path to mitigate supply risks.

- For example, secondary production can reduce energy consumption by up to 85%, a metric that directly impacts ESG compliance and profitability.

- This dynamic underscores the importance of securing copper concentrate supply through advanced froth flotation process techniques and heap leaching technology, while producing high-purity copper cathodes and specialized materials like electrodeposited copper foil, copper-clad steel, and copper interconnects to meet the demands of smart grid infrastructure, HVDC submarine cables, and advanced 800-volt architectures.

What are the Key Data Covered in this Copper Market Research and Growth Report?

-

What is the expected growth of the Copper Market between 2026 and 2030?

-

USD 99.13 billion, at a CAGR of 6.8%

-

-

What segmentation does the market report cover?

-

The report is segmented by Application (Electrical and electronics, Construction, Transportation, Telecommunication, and Others), Type (Primary, and Secondary), Product Type (Wire, Tube, Flat rolled products, Rods and bars, and Foil) and Geography (APAC, Europe, North America, South America, Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

APAC, Europe, North America, South America and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Structural grades in global primary mine production, Escalating trade protectionism and tariff regulatory complexity

-

-

Who are the major players in the Copper Market?

-

Aeris Resources Limited, Anglo American plc, Antofagasta plc, Aurubis AG, BHP Group Ltd., Boliden Group, Capstone Copper Corp, Freeport McMoRan Inc., Glencore Plc, Hindustan Copper Ltd., Jiangxi Copper Corp, KGHM Polska Miedz, Lundin Mining Corp., MMG Ltd., Rio Tinto Ltd., Sandfire Resources Limited, Southern Copper Corp., Sumitomo Metal Mining Co. Ltd., Teck Resources Ltd. and Vale SA

-

Market Research Insights

- The market is undergoing a structural shift driven by the twin engines of decarbonization and digitalization. The transition to electric mobility, where vehicles require up to four times more copper, and the expansion of renewable energy infrastructure are creating fundamental demand.

- This is balanced by supply-side pressures, where the adoption of secondary copper recovery is critical, offering up to 85% energy savings compared to primary extraction. However, a persistent interdisciplinary talent scarcity, cited by 77% of executives as a barrier, challenges the implementation of digital transformation in mining and autonomous haulage systems.

- This tension between surging demand from applications like high-voltage power transmission and operational constraints from geologic disruptions and resource nationalism defines the current landscape.

We can help! Our analysts can customize this copper market research report to meet your requirements.

RIA -

RIA -