Corrugated Pallets Market Size 2024-2028

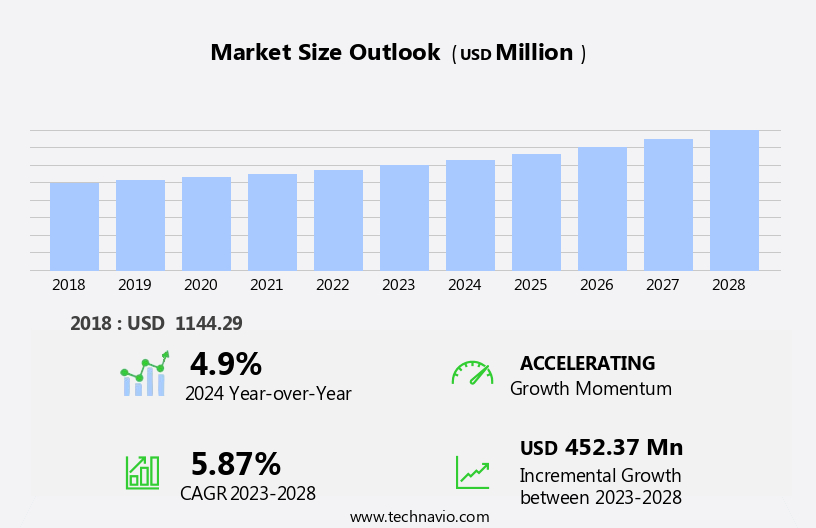

The corrugated pallets market size is forecast to increase by USD 452.37 million at a CAGR of 5.87% between 2023 and 2028.

- The market is witnessing significant growth due to the increasing demand for sustainable packaging solutions. With the rise of e-commerce and the need for efficient logistics, the use of lightweight and durable pallets is becoming increasingly popular. Moreover, the implementation of stringent regulations on volatile organic compounds in packaging materials is driving the market towards the adoption of corrugated pallets, which are made from recycled paper and are eco-friendly.

- Additionally, the automation of manufacturing processes and the use of adhesive in place of nails or staples for pallet construction are key trends In the market. Plastic pallets, while still in use, are facing challenges due to their high carbon footprint and non-biodegradable nature.

What will be the Size of the Corrugated Pallets Market During the Forecast Period?

- The market encompasses the production and distribution of pallets made from paper board, specifically corrugated material. These pallets, also known as paper pallets, offer advantages over traditional wood pallets, including lighter weight, greater durability, and easier recycling. The market's growth is driven by various factors, including the increasing demand for automated material handling systems (AMR) and the shift towards more sustainable and recyclable materials. Corrugated pallets are constructed using top decks and bottom decks, often featuring internal support structures such as cells, honeycomb, support blocks, runners, and other designs. Both manual and automated assembly methods are employed In their production.

- End users in industries like chemical, pharma, agriculture, metal machinery, wholesalers, e-commerce, retail channels, and household consumers rely on corrugated pallets for their versatility and cost-effectiveness. The market's size is substantial, with incremental revenue generated through the continuous innovation in pallet design and manufacturing processes. The use of non-recyclable materials in pallet production remains a challenge, but efforts towards more sustainable alternatives are ongoing.

How is this Corrugated Pallets Industry segmented and which is the largest segment?

The corrugated pallets industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

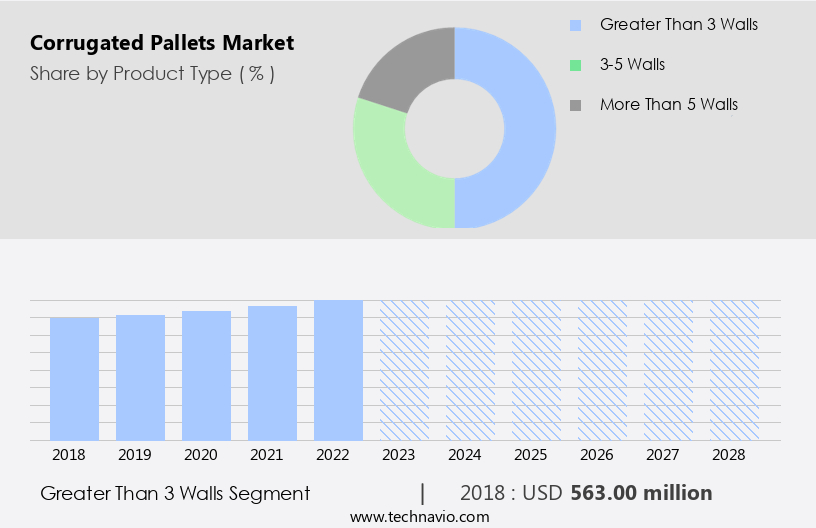

- Product Type

- Greater than 3 walls

- 3-5 walls

- More than 5 walls

- End-user

- Food and beverages

- Chemical and pharma

- Agriculture

- Wholesalers

- Others

- Geography

- APAC

- China

- Japan

- North America

- US

- Europe

- Germany

- France

- South America

- Middle East and Africa

- APAC

By Product Type Insights

- The greater than 3 walls segment is estimated to witness significant growth during the forecast period.

The market is experiencing growth due to the increasing demand for eco-friendly packaging solutions. Among the various types, corrugated pallets with more than three walls, also known as greater than 3 pallets, are gaining popularity. These pallets offer enhanced support and stability, making them suitable for handling bulky or fragile goods in industries such as food and beverage, pharmaceuticals, specialty chemicals, and automotive. The benefits of greater than 3 corrugated pallets include their lightweight yet robust design, which allows for easy transportation and storage while supporting heavy loads. Key materials used In their production include paper board and wood, with automated assembly methods increasing production efficiency.

End users in sectors like chemical, pharmaceutical, agriculture, metal machinery, wholesale, e-commerce, retail, household, and consumers are adopting these pallets due to their sustainability and recyclability. However, concerns regarding the use of non-recyclable materials and criticism from environmental protection agencies and government authorities continue to be debated in the public sphere. Market leaders In the manufacturing sector are addressing these challenges by investing in research and development to produce plastic-free alternatives, thereby increasing the recycling rate and adhering to sustainability initiatives.

Get a glance at the Corrugated Pallets Industry report of share of various segments Request Free Sample

The Greater than 3 walls segment was valued at USD 563.00 million in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

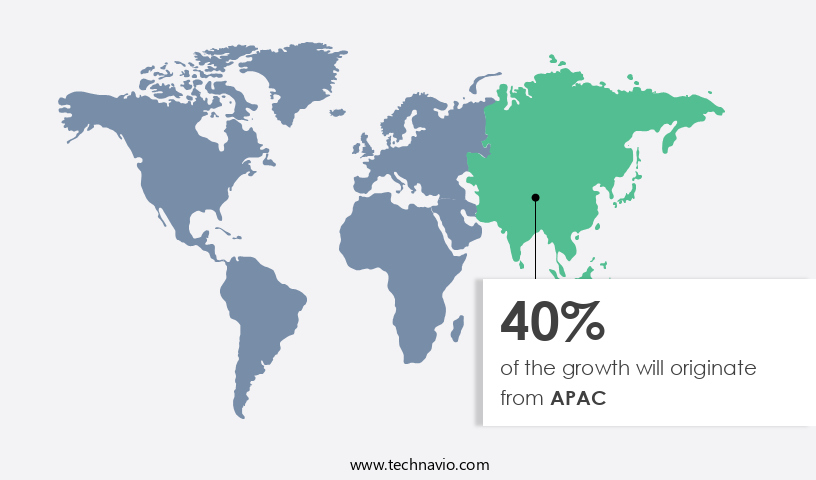

- APAC is estimated to contribute 40% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Asia-Pacific market is projected to experience notable growth during the forecast period. In contrast to traditional wooden and plastic pallets, corrugated pallets, also known as paper pallets, are manufactured using corrugated fiberboard materials. The increasing preference for eco-friendly packaging solutions is driving the demand for corrugated pallets in APAC. These pallets are recyclable and pose no harm to the environment upon disposal, making them a more sustainable option. The burgeoning retail and e-commerce industries In the APAC region are fueling the need for corrugated pallets. Key components of corrugated pallets include top decks, bottom decks, internal support, cells, honeycomb, support blocks, runners, and can be manually or automated assembled.

End users in sectors such as chemical, pharma, agriculture, metal, machinery, wholesalers, e-commerce, retail, household, and consumers are adopting corrugated pallets due to their recyclable nature and sustainability benefits. However, criticism and public debate surrounding non-recyclable materials and legal hurdles from environmental protection agencies and government authorities may pose challenges to market growth. Despite these obstacles, market leaders In the manufacturing sector are investing In the development of advanced technologies, such as automated assembly, to streamline production and enhance efficiency.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Corrugated Pallets Industry?

Increasing demand for sustainable packaging solutions is the key driver of the market.

- The market is experiencing significant growth due to the increasing demand for eco-friendly packaging solutions. With heightened environmental concerns and consumer awareness, businesses across various sectors are prioritizing sustainability. Corrugated pallets, made from recyclable and recycled paper board, offer numerous long-term benefits. They reduce carbon emissions, minimize waste production, and contribute to the circular economy. Moreover, their lightweight nature leads to lower shipping costs and more efficient logistics. Additionally, corrugated pallets can be stacked to optimize storage capacity and save space. Top decks and bottom decks are reinforced with internal support, such as cells, honeycomb, support blocks, runners, and manual or automated assembly methods.

- End users In the chemical, pharma, agriculture, metal, machinery, wholesalers, e-commerce, retail channels, household, and consumer industries are increasingly opting for plastic-free, recyclable corrugated pallets. However, legal hurdles from environmental protection agencies and government authorities may pose challenges to market expansion. Brands and retailers are responding by investing in recycling initiatives and increasing their recycling rates, as evidenced by Eurostat's 67.1% recycling rate for paper in 2020. Market leaders In the manufacturing sector are focusing on developing innovative e-commerce platforms to cater to the growing demand for corrugated pallets In the e-commerce industry.

What are the market trends shaping the Corrugated Pallets Industry?

Growing demand for lightweight and durable pallets is the upcoming market trend.

- The market is witnessing a significant demand for eco-friendly packaging solutions due to increasing concerns regarding environmental impact. These pallets, made primarily from paper board and wood, are a sustainable alternative as they are recyclable and renewable. The durability and portability of corrugated pallets make them an attractive choice for various industries, including chemical, pharma, agriculture, metal, machinery, wholesalers, e-commerce, retail channels, household, and consumers. Environmental sustainability is a top priority for brands and retailers, leading to a preference for plastic-free packaging. According to Eurostat, the recycling rate for paper and paperboard reached 72.5% in 2020. Market leaders In the corrugated pallets industry are addressing this trend by investing in automated assembly methods, such as AMRs (Automated Guided Vehicles), and developing innovative designs like top decks with honeycomb structures, support blocks, runners, and cells.

- Despite the benefits, criticism and public debate surround the use of non-recyclable materials in pallets. Environmental protection agencies and government authorities are implementing stricter regulations to encourage the use of recyclable materials. Brands and retailers are responding by partnering with manufacturers to create more sustainable packaging solutions. The market is expected to continue growing as the demand for eco-friendly alternatives increases.

What challenges does the Corrugated Pallets Industry face during its growth?

Implementation of stringent regulation on volatile organic compounds is a key challenge affecting the industry growth.

- The market faces regulatory challenges due to the use of volatile organic compounds (VOCs) in manufacturing. VOCs, which are organic chemicals with high vapor pressure, contribute to air pollution and potential health hazards. Adhesives, coatings, and other materials in corrugated pallets production may contain VOCs, releasing them during manufacturing, transportation, and disposal. To mitigate environmental impact and safeguard human health, governments and regulatory bodies worldwide impose stringent regulations on VOC emissions. This compliance necessitates additional costs for manufacturers, posing challenges In the corrugated pallets industry. Key market players must navigate these regulations while catering to various end-users, including chemical, pharma, agriculture, metal, machinery, wholesalers, e-commerce, retail channels, household, and consumers.

- Non-recyclable materials, such as plastic, have faced criticism and public debate, leading to a shift towards recyclable alternatives like paper pallets made of paper board. Market leaders are innovating with materials like honeycomb, support blocks, runners, and cells to create more sustainable, plastic-free options. European Union countries, as per Eurostat, have achieved high recycling rates, making recyclable corrugated pallets increasingly popular. Brands and retailers are embracing these eco-friendly solutions, further driving market growth. Despite these challenges, the market continues to evolve, with both manual and automated assembly methods catering to diverse customer needs.

Exclusive Customer Landscape

The corrugated pallets market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the corrugated pallets market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, corrugated pallets market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Brambles Ltd.

- Cascades Inc.

- Craemer GmbH

- DS Smith Plc

- Falkenhahn AG

- Huhtamaki Oyj

- Kamps Inc.

- KraftPal

- Menasha Corp.

- Millwood Inc.

- Mondi Plc

- PGS Group

- Rehrig Pacific Co.

- Schoeller Allibert

- Smurfit Kappa

- Sonoco Products Co.

- Spanco Storage Systems

- UFP Industries Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a diverse range of products utilized for transporting and storing various goods. These pallets, also known as paper pallets, are primarily manufactured using paper board and other materials, such as wood. The use of corrugated pallets has gained significant traction due to their numerous advantages over traditional solid wood pallets. The manufacturing process of corrugated pallets involves the assembly of top decks and bottom decks, with internal support structures like cells, honeycomb, support blocks, runners, and other components. The production methods for these pallets can vary, with both manual and automated assembly methods being employed. Corrugated pallets have garnered attention from various end-user industries, including chemical, pharmaceutical, agriculture, metal manufacturing, and machinery sectors.

In the logistics and supply chain realm, wholesalers, e-commerce platforms, retail channels, and even household consumers have adopted the use of these pallets. The paper board material used In the production of corrugated pallets is a key factor contributing to their popularity. Its lightweight nature, durability, and ease of handling make it an attractive alternative to traditional wooden pallets. Moreover, the use of paper board in pallets is more sustainable compared to non-recyclable materials, which has become a critical consideration in today's market. However, the adoption of corrugated pallets is not without its challenges. Some critics argue that the production and disposal of these pallets can generate significant waste, leading to public debate surrounding their environmental impact.

This has led to increased scrutiny from various environmental protection agencies and government authorities. Despite these challenges, the market for corrugated pallets continues to grow, driven by the increasing demand for recyclable and eco-friendly alternatives. Brands and retailers are increasingly seeking to differentiate themselves by offering plastic-free options to consumers. According to Eurostat, the recycling rate for paper and paperboard In the European Union reached an all-time high of 72.3% in 2020. The market for corrugated pallets is highly competitive, with several key players dominating the landscape. These market leaders continue to innovate and improve their manufacturing processes to meet the evolving needs of their customers.

The integration of advanced technologies, such as automation and AMR (Autonomous Mobile Robots), is becoming increasingly common In the manufacturing of corrugated pallets. In conclusion, the market is a dynamic and evolving landscape, driven by the growing demand for sustainable and eco-friendly alternatives to traditional wooden pallets. The market is characterized by continuous innovation and improvement, as well as the increasing importance of sustainability and recyclability. Despite challenges, the future looks bright for the market, with significant growth opportunities on the horizon.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

167 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.87% |

|

Market growth 2024-2028 |

USD 452.37 million |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

4.9 |

|

Key countries |

US, China, Japan, Germany, and France |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Corrugated Pallets Market Research and Growth Report?

- CAGR of the Corrugated Pallets industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the corrugated pallets market growth of industry companies

We can help! Our analysts can customize this corrugated pallets market research report to meet your requirements.

RIA -

RIA -