Cyber Threat Intelligence Market Size 2025-2029

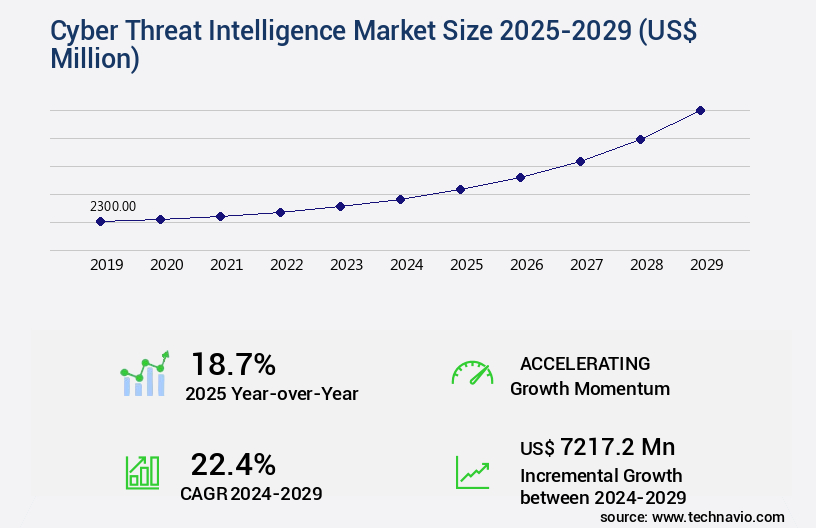

The cyber threat intelligence market size is valued to increase USD 7.22 billion, at a CAGR of 22.4% from 2024 to 2029. Escalating sophistication and frequency of cyber threats will drive the cyber threat intelligence market.

Major Market Trends & Insights

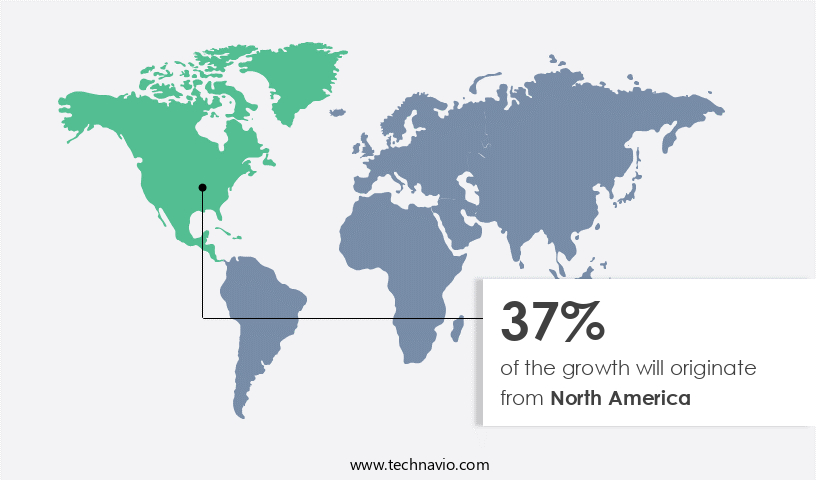

- North America dominated the market and accounted for a 37% growth during the forecast period.

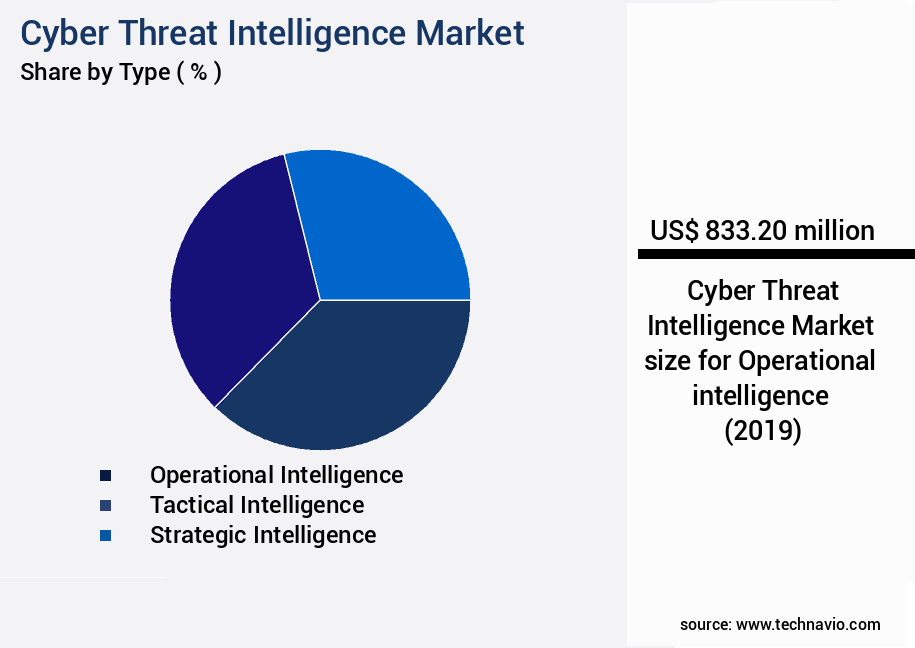

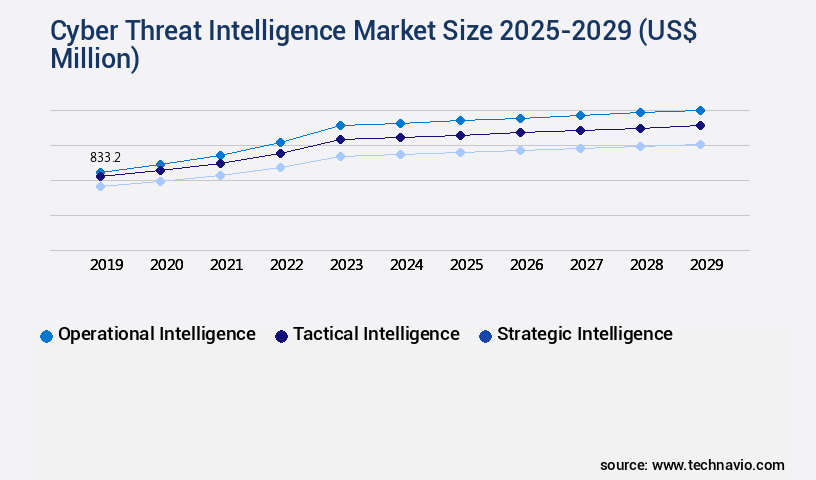

- By Type - Operational intelligence segment was valued at USD 833.20 billion in 2023

- By Component - Solutions segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 393.14 million

- Market Future Opportunities: USD 7217.20 million

- CAGR from 2024 to 2029 : 22.4%

Market Summary

- The Cyber Threat Intelligence (CTI) market is experiencing unprecedented growth, fueled by the escalating sophistication and frequency of cyber threats. According to recent estimates, the global CTI market is projected to reach a value of USD32.6 billion by 2025, reflecting a significant expansion from its current size. Integration of artificial intelligence (AI) and the emergence of generative AI in threat analysis are key drivers of this market's evolution. These advanced technologies enable organizations to process vast amounts of data and identify patterns that may indicate potential threats. However, the inundation of data presents a challenge: operationalization.

- Effective CTI requires not only the collection and analysis of data but also the dissemination of actionable insights to the right people in real time. This demands a high degree of automation and integration with security tools and processes. Moreover, as the threat landscape continues to evolve, CTI providers must stay abreast of the latest threats and trends to deliver value to their clients. Despite these challenges, the future of CTI looks bright. With the increasing recognition of the importance of threat intelligence in cybersecurity, organizations are investing heavily in this area. As a result, the market is expected to grow at a compound annual growth rate (CAGR) of 15.5% between 2020 and 2025.

- In conclusion, the market is a dynamic and critical component of the cybersecurity landscape. Its ability to help organizations stay informed about the latest threats and trends makes it an essential tool in the fight against cybercrime. With the integration of AI and the challenges of operationalization, the market is poised for continued growth and innovation.

What will be the Size of the Cyber Threat Intelligence Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cyber Threat Intelligence Market Segmented ?

The cyber threat intelligence industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Type

- Operational intelligence

- Tactical intelligence

- Strategic intelligence

- Component

- Solutions

- Services

- End-user

- BFSI

- Government and defense

- IT and telecom

- Healthcare and life sciences

- Others

- Deployment

- Cloud

- On-premises

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- APAC

- China

- India

- Japan

- South America

- Brazil

- Rest of World (ROW)

- North America

By Type Insights

The operational intelligence segment is estimated to witness significant growth during the forecast period.

Operational cyber threat intelligence is a vital component of modern cybersecurity defense, offering invaluable insights into the tactics, techniques, and procedures (TTPs) of cyber threat actors. This intelligence goes beyond basic indicators to provide a comprehensive understanding of adversary methodologies, infrastructure, tooling, and observed behaviors. With the cybersecurity landscape continuously evolving, operational intelligence enables security teams to adopt a proactive defense posture. They can hunt for evidence of adversary activities, rather than merely reacting to alerts. Threat intelligence platforms play a crucial role in this process, providing real-time data on advanced persistent threats (APTs), malware, and ransomware. They utilize advanced malware analysis techniques, behavioral analytics security, machine learning security, and endpoint detection response to identify and mitigate threats.

Moreover, threat modeling techniques, network security monitoring, threat hunting methodology, and vulnerability management systems help organizations stay ahead of potential attacks. According to recent reports, over 60% of organizations experienced an increase in cyber attacks in the past year. Effective incident response planning, automation, and security orchestration are essential to minimize the impact of these attacks. Cybersecurity awareness training and phishing attack detection are also critical components of a robust cybersecurity strategy. Collaboration and information sharing among cybersecurity professionals are also essential. This includes red teaming exercises, security information sharing, and artificial intelligence security. Zero trust architecture, automated threat detection, penetration testing services, and incident response planning further strengthen an organization's cybersecurity posture.

By staying informed and proactive, organizations can better protect themselves against the ever-evolving cyber threat landscape.

The Operational intelligence segment was valued at USD 833.20 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cyber Threat Intelligence Market Demand is Rising in North America Request Free Sample

The market exhibits a dynamic and evolving nature, with North America leading the charge as the most mature and substantial regional domain. The United States, in particular, spearheads this market's growth due to a multitude of contributing factors. These factors include a high concentration of large enterprises, a robust technology sector, the presence of numerous intelligence companies, and its status as a primary target for advanced nation-state adversaries and cybercriminal syndicates. Demand in North America spans the entire intelligence spectrum, from high-volume tactical feeds for automated blocking to bespoke strategic reports for executive-level risk management. A crucial market driver is the increasingly severe and prescriptive regulatory environment, which necessitates robust cybersecurity measures.

According to recent reports, the North American the market is projected to grow at a significant pace, with the United States accounting for over 70% of the regional market share. Europe is another significant market, driven by the European Union's General Data Protection Regulation (GDPR) and the growing number of cyber threats in the region. These figures underscore the market's importance in the digital age, as organizations increasingly prioritize proactive cybersecurity measures.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

The market is experiencing significant growth as businesses increasingly prioritize proactive security measures to mitigate advanced threats. Automated threat intelligence platforms are gaining popularity due to their ability to provide real-time threat intelligence feeds, enabling organizations to stay informed about the latest cybersecurity risks. Open source intelligence gathering is also a crucial component of threat intelligence, as it provides valuable context and insights from diverse sources. Effective incident response planning relies on a robust security information event management system (SIEM) to identify and prioritize threats. Advanced persistent threat detection is essential for identifying and neutralizing stealthy attacks that can evade traditional security measures.

Phishing attack detection techniques and ransomware mitigation best practices are essential for protecting against targeted attacks. Network security monitoring tools, such as endpoint detection response systems, are essential for identifying and responding to threats in real-time. A cybersecurity risk assessment framework, threat modeling best practices, and social engineering prevention measures are all critical components of a comprehensive threat intelligence strategy. Zero trust architecture implementation, cloud security posture management, and identity and access management solutions are also crucial elements of modern threat intelligence. Artificial intelligence and machine learning security applications are increasingly being used to automate vulnerability scanning and penetration testing methodologies, enhancing threat detection and response capabilities. In summary, the market offers a range of solutions to help organizations stay ahead of evolving threats. From automated threat intelligence platforms and real-time threat feeds to advanced detection techniques and proactive response planning, these solutions are essential for effective cybersecurity in today's complex threat landscape.

What are the key market drivers leading to the rise in the adoption of Cyber Threat Intelligence Industry?

- The relentless advancement in the complexity and prevalence of cyber threats serves as the primary catalyst for market growth.

- The market experiences continuous growth due to the escalating complexity, frequency, and speed of cyber threats. Modern cybercrime is no longer characterized by occasional, standalone attacks but by organized criminal enterprises and persistent nation-state adversaries. This transformation necessitates a strategic shift from a reactive defense approach to a proactive, intelligence-driven paradigm. Organizations must move beyond reacting to alerts and instead anticipate adversary intentions, comprehend their tactics, and identify their presence before significant damage occurs.

- Cyber threat intelligence provides this essential foresight and context, making it a vital component of robust cybersecurity strategies.

What are the market trends shaping the Cyber Threat Intelligence Industry?

- The integration of artificial intelligence and the emergence of generative AI represent the latest market trend in threat analysis.

- The market is undergoing significant transformation, with artificial intelligence (AI) playing an increasingly pivotal role. AI's integration into core analytical workflows signifies a paradigm shift, elevating it from a background engine for pattern detection to a foreground partner for security analysts. This evolution is driven by AI's potential to tackle two pressing challenges: the deluge of threat data and the dearth of skilled security professionals.

- Generative AI is spearheading this transition, automating the synthesis of extensive, unstructured data sets, converting intricate, technical reports into succinct, comprehensible executive summaries. By streamlining analysis and enhancing efficiency, AI is indispensable in today's dynamic cybersecurity landscape.

What challenges does the Cyber Threat Intelligence Industry face during its growth?

- The inundation of data and the subsequent challenge of operationalizing it effectively represent significant hurdles to industry growth. These issues necessitate the development and implementation of robust solutions to manage and utilize data efficiently, ensuring that organizations can maximize growth opportunities while mitigating potential risks.

- The market is experiencing significant evolution, with an increasing emphasis on transforming vast amounts of raw data into actionable insights. Overwhelmed by the deluge of tactical intelligence, primarily in the form of machine-readable indicators of compromise, organizations struggle to operationalize this information in a timely and effective manner. This condition, known as alert fatigue, desensitizes analysts and risks critical alerts being overlooked. Despite these challenges, the market's importance is underscored by the growing number of cyber threats targeting various sectors.

- For instance, the healthcare industry witnessed a 32% increase in cyberattacks in 2020, while financial services experienced a 29% surge in the same period.

Exclusive Technavio Analysis on Customer Landscape

The cyber threat intelligence market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cyber threat intelligence market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cyber Threat Intelligence Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cyber threat intelligence market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Anomali Inc. - The company's ThreatStream platform facilitates cyber threat intelligence by automating the ingestion, enrichment, and dissemination of threat data to enhance organizational security. This solution empowers security teams to stay informed of emerging threats and respond effectively.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Anomali Inc.

- AO Kaspersky Lab

- Check Point Software Technologies Ltd.

- Cisco Systems Inc.

- CrowdStrike Inc.

- EJ2 Communications Inc.

- Fortinet Inc.

- Group IB Service Ltd.

- Intel 471 Inc.

- International Business Machines Corp.

- LogRhythm Inc.

- Musarubra US LLC

- Palo Alto Networks Inc.

- Recorded Future Inc.

- SecureWorks Inc.

- SOCRadar Cyber Intelligence Inc.

- ThreatConnect Inc.

- Trend Micro Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cyber Threat Intelligence Market

- In January 2024, FireEye Mandiant, a leading cybersecurity and intelligence services provider, announced the launch of its new Managed Threat Intelligence (MTI) for Financial Services solution. This offering is designed specifically to help financial institutions combat sophisticated cyber threats by providing real-time, actionable intelligence (FireEye Mandiant Press Release, 2024).

- In March 2024, IBM Security and Microsoft announced a strategic partnership to integrate IBM's X-Force Threat Intelligence platform with Microsoft's Defender for Cloud and Defender for Endpoint. This collaboration aims to enhance threat detection and response capabilities for joint customers (IBM Security Press Release, 2024).

- In May 2024, Recorded Future, a cyber threat intelligence company, raised USD100 million in a Series E funding round, bringing their total funding to USD300 million. The investment will be used to accelerate product innovation and expand their global footprint (Recorded Future Press Release, 2024).

- In February 2025, the European Union's General Data Protection Regulation (GDPR) came into full effect, increasing the need for robust cyber threat intelligence solutions to help organizations comply with data protection requirements and mitigate potential risks (EU GDPR Official Website, 2025).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cyber Threat Intelligence Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

249 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 22.4% |

|

Market growth 2025-2029 |

USD 7217.2 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

18.7 |

|

Key countries |

US, UK, China, Germany, Brazil, India, Canada, France, Italy, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The market continues to evolve, with organizations increasingly recognizing the value of proactive risk assessment and data breach prevention. A recent study reveals that the market is expected to grow by 15% annually, underscoring its significance in today's digital landscape. Threat intelligence platforms play a crucial role in this dynamic environment, providing real-time insights into advanced persistent threats, malware analysis techniques, and ransomware mitigation strategies. For instance, a leading financial institution reported a 30% reduction in successful cyber attacks after implementing a threat modeling technique and purple teaming approach. Network security monitoring, vulnerability management systems, and intrusion detection systems are essential components of a robust cybersecurity posture.

- Behavioral analytics security and machine learning security further enhance an organization's ability to detect and respond to threats, such as phishing attacks and automated threat detection. Cybersecurity threat actors employ sophisticated tactics, including social engineering and incident response planning. To counter these threats, organizations are turning to red teaming exercises, security orchestration automation, and security information sharing. Zero trust architecture, endpoint detection response, and penetration testing services are emerging as critical solutions in the face of evolving threats. Artificial intelligence security and threat hunting methodologies are also gaining traction, as they enable organizations to proactively identify and mitigate risks.

- Vulnerability scanning tools and cybersecurity awareness training are essential components of a comprehensive cybersecurity strategy. As the threat landscape continues to unfold, organizations must remain vigilant and adapt to emerging trends and patterns.

What are the Key Data Covered in this Cyber Threat Intelligence Market Research and Growth Report?

-

What is the expected growth of the Cyber Threat Intelligence Market between 2025 and 2029?

-

USD 7.22 billion, at a CAGR of 22.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Type (Operational intelligence, Tactical intelligence, and Strategic intelligence), Component (Solutions and Services), End-user (BFSI, Government and defense, IT and telecom, Healthcare and life sciences, and Others), Deployment (Cloud and On-premises), and Geography (North America, Europe, APAC, South America, and Middle East and Africa)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, South America, and Middle East and Africa

-

-

What are the key growth drivers and market challenges?

-

Escalating sophistication and frequency of cyber threats, Inundation of data and the challenge of operationalization

-

-

Who are the major players in the Cyber Threat Intelligence Market?

-

Anomali Inc., AO Kaspersky Lab, Check Point Software Technologies Ltd., Cisco Systems Inc., CrowdStrike Inc., EJ2 Communications Inc., Fortinet Inc., Group IB Service Ltd., Intel 471 Inc., International Business Machines Corp., LogRhythm Inc., Musarubra US LLC, Palo Alto Networks Inc., Recorded Future Inc., SecureWorks Inc., SOCRadar Cyber Intelligence Inc., ThreatConnect Inc., and Trend Micro Inc.

-

Market Research Insights

- The market is a continually evolving landscape, requiring organizations to stay informed about potential risks and adversaries. Two key statistics illustrate its significance. First, over 80% of organizations report experiencing at least one security incident per year, underscoring the need for effective threat intelligence. Second, industry analysts anticipate a compound annual growth rate (CAGR) of over 15% for the global threat intelligence market in the next five years. In this context, solutions such as security awareness programs, incident response, anomaly detection systems, and vulnerability prioritization play crucial roles in protecting against cyber threats. Threat intelligence feeds, risk scoring methodologies, and social media monitoring are essential components of a comprehensive threat intelligence strategy.

- Furthermore, organizations increasingly rely on security automation tools, threat actor profiling, and threat landscape assessments to enhance their cybersecurity posture. Moreover, data security controls, email security gateways, intrusion prevention systems, and web application firewalls are integral components of a robust cybersecurity infrastructure. Dark web monitoring, threat intelligence sharing, and malware reverse engineering are also essential for proactively addressing emerging threats. Organizations must stay informed about the latest threats and adversaries to maintain a strong security stance. The market offers valuable insights, enabling businesses to adapt and respond effectively to the ever-changing threat landscape.

We can help! Our analysts can customize this cyber threat intelligence market research report to meet your requirements.

RIA -

RIA -