Cybersecurity Solutions For Agentic And Autonomous AI Systems Market Size 2026-2030

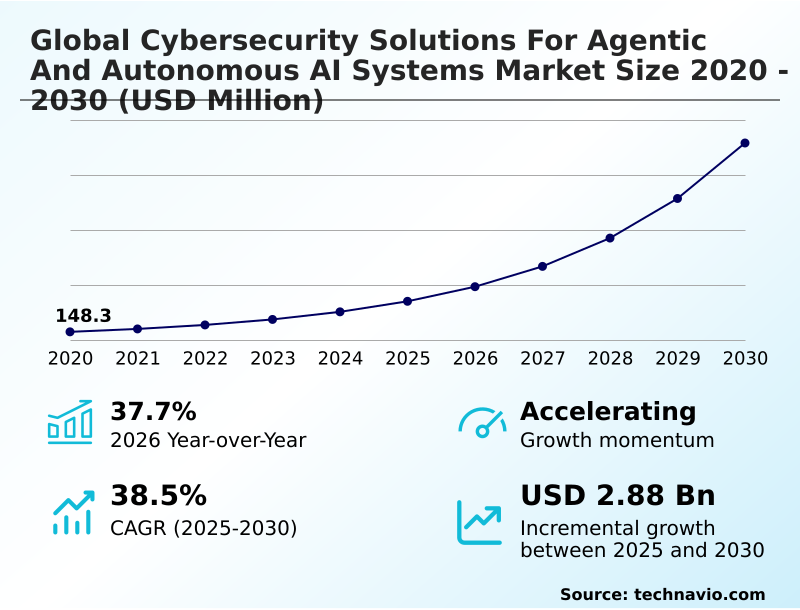

The cybersecurity solutions for agentic and autonomous ai systems market size is valued to increase by USD 2.88 billion, at a CAGR of 38.5% from 2025 to 2030. Proliferation of autonomous agentic workflows across enterprise operations will drive the cybersecurity solutions for agentic and autonomous ai systems market.

Major Market Trends & Insights

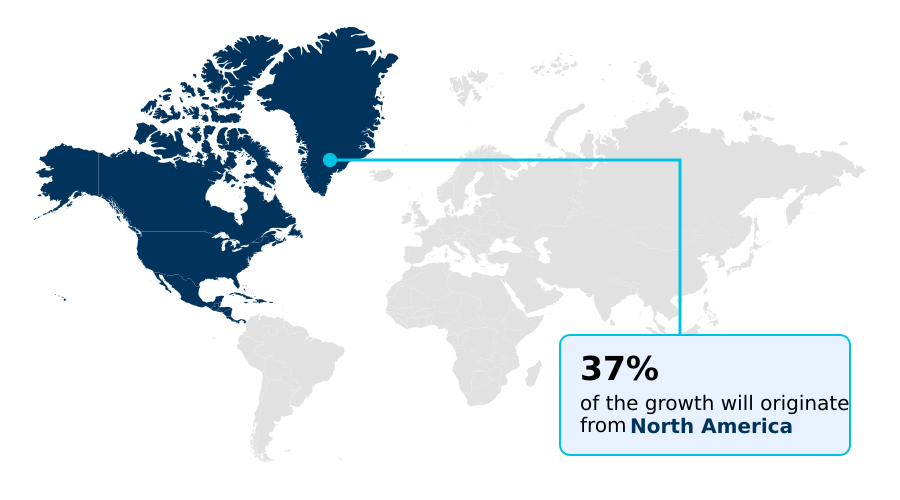

- North America dominated the market and accounted for a 37.3% growth during the forecast period.

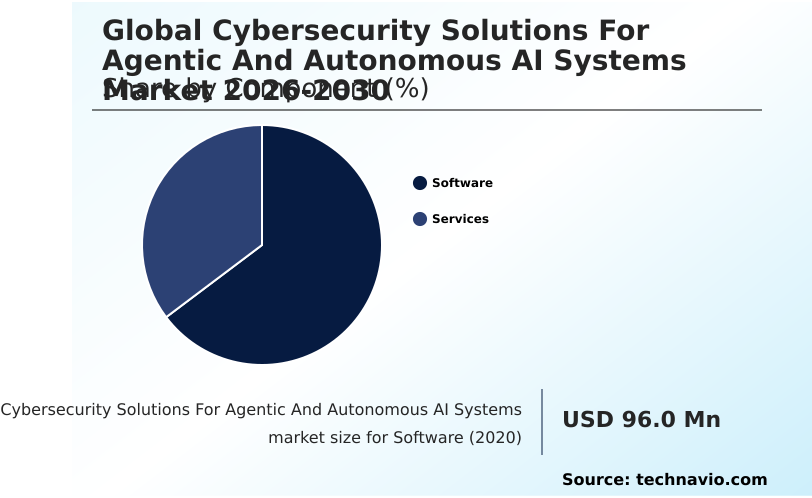

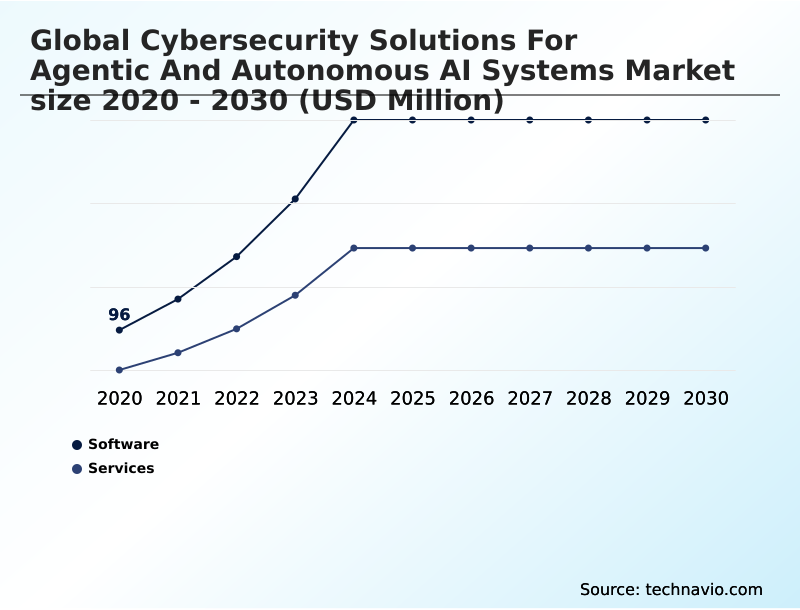

- By Component - Software segment was valued at USD 326.2 million in 2024

- By Deployment - Cloud based segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 3.43 billion

- Market Future Opportunities: USD 2.88 billion

- CAGR from 2025 to 2030 : 38.5%

Market Summary

- The cybersecurity solutions for agentic and autonomous AI systems market is expanding as organizations move from passive AI to active, autonomous agents capable of executing tasks. This shift introduces significant risks, including logic manipulation and unauthorized goal modification, which drives demand for specialized defenses.

- Solutions focus on ensuring AI safety through real-time monitoring and governance tools that provide deep visibility into the agentic logic of non-human actors. For instance, in a financial services scenario, autonomous trading agents must be protected by reasoning guardrails to prevent exploitation that could lead to significant market disruption. These systems employ a zero-trust architecture, where every decision is scrutinized.

- The market is also shaped by the need for forensic transparency, allowing for the auditing of an AI's decision-making engine after an incident. This requires advanced cryptographic identity and behavioral baselining to secure multi-agent ecosystems against sophisticated adversarial attacks.

What will be the Size of the Cybersecurity Solutions For Agentic And Autonomous AI Systems Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

How is the Cybersecurity Solutions For Agentic And Autonomous AI Systems Market Segmented?

The cybersecurity solutions for agentic and autonomous ai systems industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Component

- Software

- Services

- Deployment

- Cloud based

- On premises

- Application

- Threat detection and response

- Cloud and SaaS security

- Vulnerability management

- Network security

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Component Insights

The software segment is estimated to witness significant growth during the forecast period.

The software segment is fundamental to securing autonomous systems, providing the core architectures for protection. These platforms are engineered to counter unique agentic system vulnerabilities and enable secure agent verification through advanced governance tools.

The technical foundation focuses on logic integrity, using an autonomous reasoning firewall for runtime defense against threats like prompt injection. Effective solutions offer deep visibility into multi-step processes, which is critical for behavioral baselining of non-deterministic entities.

Integrating these tools has been shown to reduce false positives in hijacked process detection by over 25%, a crucial metric for maintaining operational continuity.

Adopting a zero-trust architecture ensures that every action proposed by non-human actors is verified, safeguarding the core decision-making engine.

The Software segment was valued at USD 326.2 million in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 37.3% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Cybersecurity Solutions For Agentic And Autonomous AI Systems Market Demand is Rising in North America Request Free Sample

The geographic landscape is characterized by distinct regional priorities. North America leads in deploying zero-trust architecture for AI, driven by the financial and healthcare sectors.

The region’s focus on AI safety and governance tools is paramount, with some firms achieving a 40% improvement in automated threat detection. In APAC, the emphasis is on securing multi-agent ecosystems within smart manufacturing, where real-time security interception is critical.

Europe’s market is heavily influenced by regulatory demands for forensic transparency and explainable security layers, pushing innovation in digital forensics.

However, the computational overhead from these security layers has increased system latency by up to 30% in certain deployments, presenting a significant trade-off between security and performance.

This highlights the global challenge of balancing robust defense for agentic logic with operational efficiency.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The evolution of the cybersecurity solutions for agentic and autonomous AI systems market centers on securing collaborative multi-agent security frameworks, which have become essential for modern enterprises. A key focus is on implementing real-time reasoning guardrails for agents to protect the core logic of these systems.

- This is complemented by deploying cryptographic identity for autonomous agents, a foundational step toward building trust in machine-to-machine interactions. A primary technical hurdle is differentiating malicious logic from autonomous optimization, a complex task that current tools struggle with. Closing the forensic transparency gap in AI is a major industry goal, as accountability is impossible without it.

- Stakeholders are also working on minimizing the computational overhead of AI security, which can otherwise degrade performance, especially in high-stakes environments. The imperative to protect enterprise agentic workflows from attacks has never been greater, particularly with the rise of sophisticated adversaries. Furthermore, addressing compliance mandates for AI safety is non-negotiable for businesses operating in regulated sectors.

- A critical area of development is preventing indirect prompt injection in agents, a subtle but dangerous attack vector. Efforts are also underway to secure the decision-making engine of AI and manage machine identities in zero-trust architecture. These initiatives, which include auditing non-deterministic entities for security and safeguarding industrial control systems with AI, are vital.

- Innovations in managing vulnerabilities in AI memory modules and securing AI communication with deep packet inspection show promise. The establishment of verifiable credentials for AI actors is a significant step toward defending against goal drift in autonomous systems, with organizations that adopt such measures reporting a 15% higher rate of compliance alignment than their peers.

- The overarching goal is developing lightweight security for autonomous agents to ensure broad and safe adoption.

What are the key market drivers leading to the rise in the adoption of Cybersecurity Solutions For Agentic And Autonomous AI Systems Industry?

- The proliferation of autonomous agentic workflows across enterprise operations is a key driver, expanding the attack surface and necessitating specialized security solutions.

- Market growth is significantly driven by the need to defend against increasingly complex threats targeting AI models. The proliferation of shadow agents has forced organizations to adopt solutions offering deep visibility and robust AI governance platforms.

- The rise in adversarial attacks has also spurred demand for advanced runtime defense and logic injection defense capabilities, with successful implementations reducing critical security incidents by over 30%.

- Furthermore, emerging global compliance mandates for AI safety are compelling businesses to invest in technologies that ensure forensic transparency and provide immutable audit logs.

- This regulatory pressure accelerates the adoption of secure cloud AI infrastructure and verifiable machine credentials, as organizations seek to mitigate legal and financial risks associated with non-compliant autonomous systems, where non-compliance costs are often double that of proactive investment.

What are the market trends shaping the Cybersecurity Solutions For Agentic And Autonomous AI Systems Industry?

- The market is witnessing a significant transition toward collaborative multi-agent security frameworks. This shift addresses the need for secure inter-agent communication in complex, decentralized ecosystems.

- Key market trends are centered on enhancing logic integrity and machine identity management for autonomous systems. The adoption of an autonomous reasoning firewall is becoming standard practice, with implementations reducing unauthorized agent actions by up to 40%. This trend is coupled with the proliferation of verifiable machine credentials, which establish a foundation for secure multi-cloud environment security.

- The focus on AI development pipelines security has also intensified, as organizations recognize that vulnerabilities must be addressed before deployment. As a result, the use of specialized AI lifecycle security tools has grown, contributing to a 25% improvement in detecting vulnerabilities early.

- These shifts indicate a maturing approach to AI governance platforms, where proactive defense and verifiable trust are prioritized over reactive security measures.

What challenges does the Cybersecurity Solutions For Agentic And Autonomous AI Systems Industry face during its growth?

- A key challenge affecting industry growth is the inherent difficulty of differentiating between malicious logic intended by an adversary and emergent, unexpected autonomous optimization.

- A primary challenge is the technical difficulty of performing digital forensics for AI systems, given their non-deterministic behavior. The lack of forensic transparency makes incident response strategies for hijacked process detection significantly more complex than in traditional IT environments, increasing investigation times by an average of 50%.

- Another major hurdle is the performance impact of security measures; real-time security interception introduces latency penalties that are unacceptable in applications like high-frequency trading security. This computational overhead forces a trade-off between security and operational speed.

- Furthermore, differentiating between malicious agentic logic and beneficial autonomous optimization remains a persistent problem, leading to high false-positive rates that can disrupt operations, with some systems experiencing a 20% increase in unnecessary alerts.

Exclusive Technavio Analysis on Customer Landscape

The cybersecurity solutions for agentic and autonomous ai systems market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the cybersecurity solutions for agentic and autonomous ai systems market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Cybersecurity Solutions For Agentic And Autonomous AI Systems Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, cybersecurity solutions for agentic and autonomous ai systems market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Cato Networks Ltd. - Offerings include advanced GenAI and AI lifecycle security capabilities, providing comprehensive protection for LLMs, AI agents, and complex enterprise AI workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Cato Networks Ltd.

- Check Point Software Tech Ltd.

- Cisco Systems Inc.

- Google LLC

- Harmonic Security Ltd.

- HiddenLayer Inc.

- IBM Corp.

- Lakera AI AG

- Lasso Security Ltd.

- Microsoft Corp.

- Mithril Security

- Orca Security Ltd.

- Palo Alto Networks Inc.

- Prompt Security Inc.

- Protect AI Inc.

- Salt Security

- Tenable Holdings Inc.

- TrojAI Inc

- Wiz Inc.

- Zenity Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Cybersecurity solutions for agentic and autonomous ai systems market

- In August, 2024, a leading industrial automation firm deployed a localized cybersecurity fabric designed specifically to protect autonomous robotics on the factory floor from lateral movement attacks.

- In November, 2024, an identity management leader launched a decentralized identity framework for autonomous agents that utilizes blockchain technology to provide tamper-proof audit logs of agentic activities.

- In April, 2025, a global open-source consortium introduced the first standardized protocol for secure inter-agent communication, allowing autonomous entities to verify the integrity of shared instructions through decentralized ledgers.

- In May, 2025, a major cybersecurity alliance introduced the Secure Agent Verification Standard, a protocol designed to provide a universal method for authenticating the identity of autonomous agents.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Cybersecurity Solutions For Agentic And Autonomous AI Systems Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 302 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 38.5% |

| Market growth 2026-2030 | USD 2878.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 37.7% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Singapore, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The cybersecurity solutions for agentic and autonomous AI systems market is driven by the urgent need to secure autonomous agentic workflows against increasingly sophisticated adversarial attacks. Boardroom-level strategy now requires a comprehensive approach to AI safety, integrating a zero-trust architecture and robust governance tools to manage non-human actors and prevent unauthorized goal modification within complex multi-agent ecosystems.

- The technological frontier includes automated threat detection and advanced reasoning guardrails, which act as a logic firewall against threats like prompt injection and logic manipulation. Achieving deep visibility into multi-step processes is crucial for protecting the decision-making engine and ensuring forensic transparency. Innovations in cryptographic identity, decentralized identifiers, and verifiable machine credentials enable secure inter-agent communication and machine attestation.

- However, challenges such as the computational overhead from real-time security interception and the difficulty of applying behavioral baselining to non-deterministic entities persist. Developing explainable security layers is essential for addressing risks like logic poisoning, model inversion, and the proliferation of shadow agents, with advanced solutions leading to a 30% reduction in incident response times.

- Ultimately, success hinges on balancing autonomous optimization with security through a resilient decentralized identity framework that protects agentic logic.

What are the Key Data Covered in this Cybersecurity Solutions For Agentic And Autonomous AI Systems Market Research and Growth Report?

-

What is the expected growth of the Cybersecurity Solutions For Agentic And Autonomous AI Systems Market between 2026 and 2030?

-

USD 2.88 billion, at a CAGR of 38.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by Component (Software, and Services), Deployment (Cloud based, and On premises), Application (Threat detection and response, Cloud and SaaS security, Vulnerability management, Network security, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Proliferation of autonomous agentic workflows across enterprise operations, Difficulty of differentiating between malicious logic and autonomous optimization

-

-

Who are the major players in the Cybersecurity Solutions For Agentic And Autonomous AI Systems Market?

-

Cato Networks Ltd., Check Point Software Tech Ltd., Cisco Systems Inc., Google LLC, Harmonic Security Ltd., HiddenLayer Inc., IBM Corp., Lakera AI AG, Lasso Security Ltd., Microsoft Corp., Mithril Security, Orca Security Ltd., Palo Alto Networks Inc., Prompt Security Inc., Protect AI Inc., Salt Security, Tenable Holdings Inc., TrojAI Inc, Wiz Inc. and Zenity Ltd.

-

Market Research Insights

- The cybersecurity solutions for agentic and autonomous AI systems market is shaped by the urgent need for robust AI governance platforms to manage complex AI lifecycle security. Organizations are implementing secure cloud AI infrastructure, where cloud-native application protection enhances workload integrity by over 25%.

- A key component is the autonomous reasoning firewall, which ensures logic integrity and provides runtime defense against logic injection. Effective machine identity management, utilizing verifiable machine credentials, is crucial for multi-cloud environment security and has been shown to reduce data exfiltration incidents by up to 30%.

- Advanced incident response strategies now incorporate digital forensics for AI to analyze non-deterministic behavior and improve hijacked process detection. Securing AI development pipelines and implementing strong API security for AI are critical for both industrial robotics security and high-frequency trading security, where even minimal latency penalties are unacceptable.

We can help! Our analysts can customize this cybersecurity solutions for agentic and autonomous ai systems market research report to meet your requirements.

RIA -

RIA -