Data Center Blade Server Market Size 2026-2030

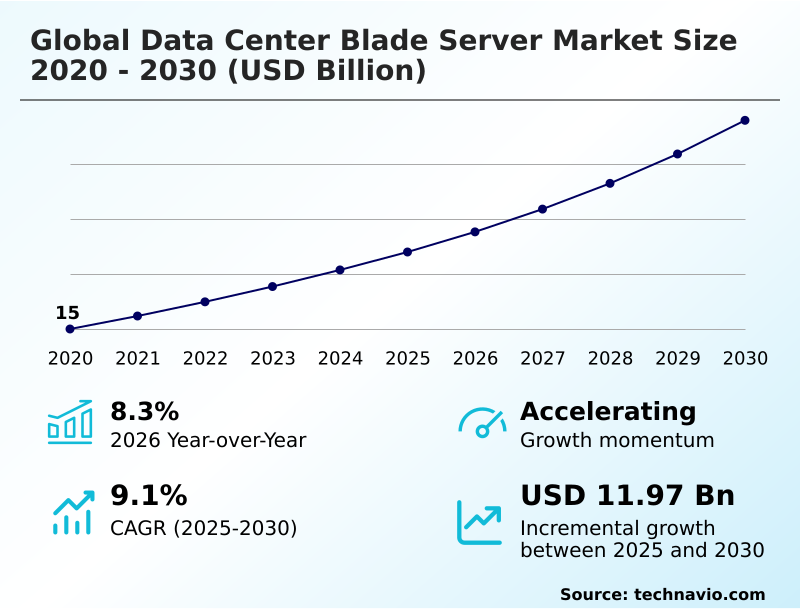

The data center blade server market size is valued to increase by USD 11.97 billion, at a CAGR of 9.1% from 2025 to 2030. Exponential growth of artificial intelligence (AI) and machine learning (ML) will drive the data center blade server market.

Major Market Trends & Insights

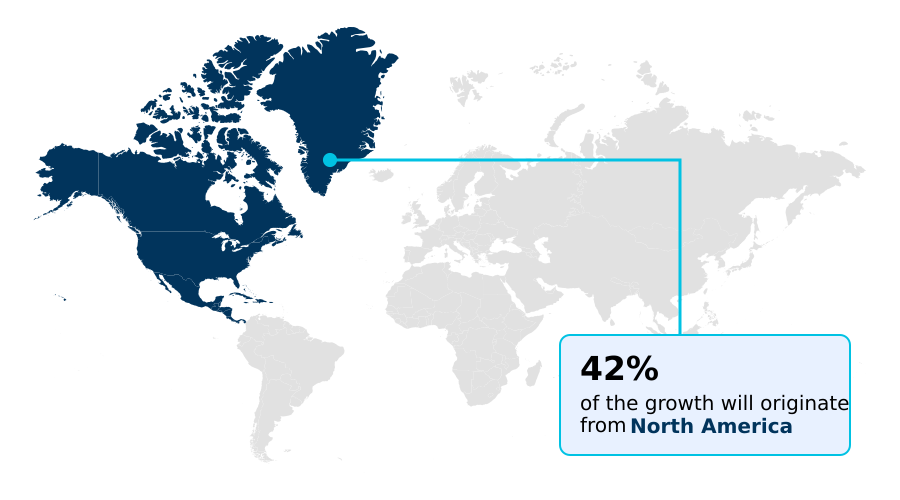

- North America dominated the market and accounted for a 42.1% growth during the forecast period.

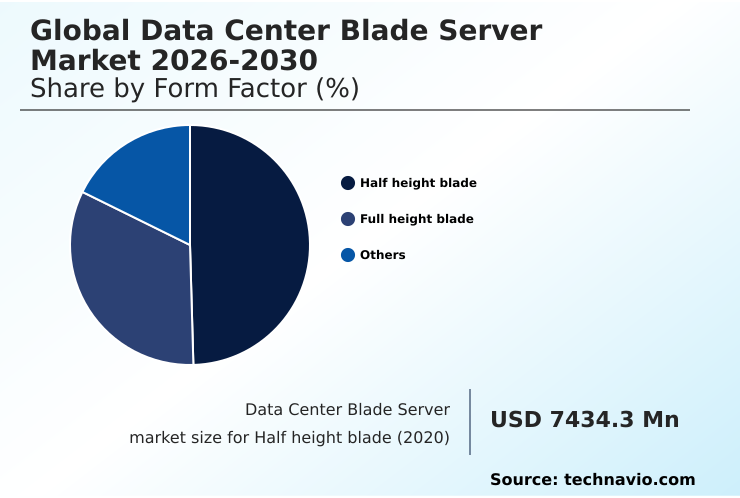

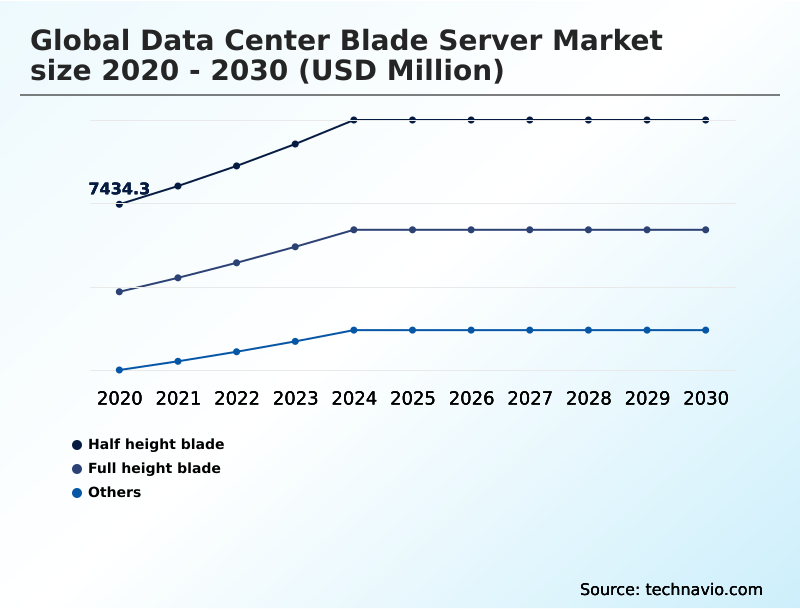

- By Form Factor - Half height blade segment was valued at USD 9.86 billion in 2024

- By Type - Tier 3 segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 18.96 billion

- Market Future Opportunities: USD 11.97 billion

- CAGR from 2025 to 2030 : 9.1%

Market Summary

- The data center blade server market is undergoing a significant transformation, driven by the escalating need for high-density, energy-efficient computing. The primary catalyst is the explosion of artificial intelligence and machine learning workloads, which demand specialized full-height blade configurations capable of housing multiple high-wattage accelerators.

- This has forced a market-wide pivot toward advanced thermal management, making direct-to-chip liquid cooling a standard feature rather than a niche option. Concurrently, the principles of composable infrastructure, enabled by high-speed unified fabric and Compute Express Link (CXL), are turning the blade chassis into a fluid resource pool.

- For instance, a financial services firm can now dynamically allocate GPU and memory resources from a shared pool to different blades for real-time risk analytics, drastically improving resource utilization. However, the high initial capital expenditure for proprietary chassis systems and intense competition from hyperconverged infrastructure (HCI) present considerable challenges.

- Success in this evolving landscape depends on delivering not just hardware density but also sophisticated software-defined management and a clear path to managing the power and cooling complexities of next-generation processors, ensuring a strong total cost of ownership proposition.

What will be the Size of the Data Center Blade Server Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Data Center Blade Server Market Segmented?

The data center blade server industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- Form factor

- Half height blade

- Full height blade

- Others

- Type

- Tier 3

- Tier 4

- Tier 2

- Tier 1

- Application

- Virtualization and cloud computing

- AI and ML Workloads

- Big data analytics

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- APAC

- China

- Japan

- India

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Colombia

- Rest of World (ROW)

- North America

By Form Factor Insights

The half height blade segment is estimated to witness significant growth during the forecast period.

The half-height blade segment remains foundational for enterprise virtualization and general cloud workloads, prized for its optimal balance of computational density and cost-effectiveness.

This modular computing format enables organizations to maximize independent compute nodes within a single blade chassis, directly addressing the need for server consolidation and a smaller data center footprint.

The design inherently improves operational expenditure (Opex) by centralizing power and cooling.

For mission-critical workloads, the architecture's efficiency is paramount; successful deployments have demonstrated the ability to reduce server provisioning time by more than 30%, a critical metric for agile business operations.

The continued adoption is driven by its ability to support high-density computing for a majority of enterprise applications without requiring the specialized infrastructure of more advanced systems.

The Half height blade segment was valued at USD 9.86 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 42.1% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Data Center Blade Server Market Demand is Rising in North America Get Free Sample

The geographic landscape of the global data center blade server market 2026-2030 is led by North America, which is projected to contribute 42.1% of the market's incremental growth, driven by hyperscale cloud providers and AI infrastructure investments.

In this region, full-height blade systems with direct-to-chip liquid cooling are in high demand.

Europe's market is heavily influenced by data sovereignty and sustainability regulations, favoring blade enclosures that deliver superior power usage effectiveness (PUE); some deployments in the region have achieved a PUE below 1.1.

Meanwhile, the market in APAC is defined by rapid 5G network expansion and edge computing deployments, creating strong demand for modular computing solutions like micro-blades.

These regional dynamics highlight a global shift toward specialized, high-density computing platforms tailored to specific workload and regulatory requirements.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- The strategic application of blade servers is becoming increasingly specialized, moving beyond general server consolidation to address specific, high-value use cases. The demand for a blade server for AI model training is driving the adoption of advanced thermal solutions, with liquid cooling for full-height blades becoming essential to manage the heat from dense GPU clusters.

- In parallel, enterprises are leveraging high-density virtualization blade solutions to maximize compute resources in private cloud environments. This is often coupled with the adoption of composable infrastructure for private cloud, which uses technologies like CXL fabric attached memory expansion to create flexible, software-defined resource pools.

- This approach delivers more than double the computational throughput per watt compared to legacy rack-based deployments for certain workloads. For organizations focused on financial optimization, the debate over blade server vs rack server TCO is being won by blades in dense environments, with many now focused on reducing Opex with blade server consolidation.

- At the network perimeter, edge computing micro-blade servers are enabling low-latency processing for 5G and IoT applications. In specialized sectors, the need for a blade server for financial trading and for secure government cloud blade servers highlights the platform's ability to deliver high performance, security, and reliability in mission-critical scenarios.

What are the key market drivers leading to the rise in the adoption of Data Center Blade Server Industry?

- The exponential growth of artificial intelligence and machine learning workloads is a primary driver for the market, demanding unprecedented computational density and specialized server architectures.

- Market growth is primarily driven by the unstoppable demand for high-density computing, fueled by AI model training and inference workloads.

- The blade server's shared infrastructure is architecturally superior for this purpose, with new full-height blade designs supporting up to four times the thermal design power (TDP) of previous generations. This density is essential for maximizing the compute-per-square-foot metric.

- The second major driver is the critical need for energy efficiency, where the centralized management of power and cooling in a blade chassis delivers superior Power Usage Effectiveness (PUE); new power systems are exceeding the 80 PLUS Titanium efficiency standard by 2%.

- Finally, the move toward software-defined management and composable infrastructure, enabling hot-swappable components and dynamic resource allocation, significantly reduces operational expenditure (Opex) and provisioning time.

What are the market trends shaping the Data Center Blade Server Industry?

- The industrialization of liquid cooling solutions is becoming a standard design consideration for high-density blade servers. This shift is driven by the escalating thermal output from processors and accelerators used in ultra-high-density AI workloads.

- Key market trends are coalescing around thermal management, security, and resource flexibility. The industrialization of liquid cooling is a direct response to the escalating thermal design power (TDP) of AI accelerators, with advanced blade enclosures now supporting multiple high-wattage GPUs.

- This shift enables data centers to achieve a Power Usage Effectiveness (PUE) below 1.1, a feat unattainable with air cooling in high-density environments. Concurrently, the establishment of a silicon-root-of-trust is becoming a standard security feature, embedding trust into the silicon-level boot process to protect against firmware attacks. This is complemented by AI-driven cyber resilience managed at the chassis level.

- Furthermore, the rise of composable infrastructure, facilitated by Compute Express Link (CXL) and a unified fabric, is enabling unprecedented resource disaggregation and memory pooling within the blade chassis.

What challenges does the Data Center Blade Server Industry face during its growth?

- A key challenge affecting industry growth is the high initial capital expenditure associated with proprietary chassis systems, which can lead to company lock-in and reduced procurement flexibility.

- Significant challenges constrain market adoption, led by high initial capital expenditure (Capex) and the proprietary chassis designs that result in vendor lock-in. This financial model is a barrier for organizations without large upfront budgets. A second major challenge is the complexity of managing extreme thermal loads.

- Despite consolidation benefits, over 30% of older blade chassis in some environments are not fully populated due to cooling limitations. This necessitates costly and complex upgrades to cooling distribution units (CDUs) and power distribution units (PDUs). Finally, intense competition from hyperconverged infrastructure (HCI) and Open Compute Project (OCP) solutions threatens the market.

- HCI offers similar management simplification without the proprietary hardware, while OCP provides hyperscale cloud providers with a cost-effective, company-agnostic alternative, diverting a massive segment of potential demand.

Exclusive Technavio Analysis on Customer Landscape

The data center blade server market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the data center blade server market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Data Center Blade Server Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, data center blade server market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Atos SE - Offerings include highly dense, modular computing infrastructure engineered to maximize processing power and operational efficiency through shared resources and centralized management.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Atos SE

- Cisco Systems Inc.

- Dell Technologies Inc.

- Fujitsu Ltd.

- Hewlett Packard

- Hitachi Vantara LLC

- Hon Hai Precision. Ltd.

- Huawei Technologies Co. Ltd.

- IBM Corp.

- Inspur Group.

- Inventec Corp.

- Lenovo Group Ltd.

- NEC Corp.

- New H3C Technologies

- Oracle Corp.

- Penguin Solutions

- Quanta Computer lnc.

- Sugon Information Co.

- Super Micro Computer Inc.

- Wistron Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Data center blade server market

- In February 2025, Hewlett Packard Enterprise unveiled its next-generation liquid-cooled blade enclosure for the HPE Synergy platform, featuring factory-integrated manifolds to support significantly higher thermal design power per compute module.

- In May 2025, Dell Technologies introduced a new full-height PowerEdge MX blade module integrating an advanced Compute Express Link (CXL) 3.0-enabled fabric, allowing multiple blades to share a disaggregated memory pool.

- In October 2025, Supermicro announced its latest generation of SuperBlade enclosures featuring CXL fabric-attached memory expansion, enabling a single blade server to access terabytes of memory from a dedicated memory blade within the same chassis.

- In March 2025, Cisco Systems announced a major overhaul of its UCS X-Series power subsystem, introducing a new generation of high-efficiency power supply units that achieved a certified efficiency rating exceeding the 80 PLUS Titanium standard by 2%.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Data Center Blade Server Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 312 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 9.1% |

| Market growth 2026-2030 | USD 11969.1 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 8.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, The Netherlands, Spain, China, Japan, India, South Korea, Australia, Indonesia, Saudi Arabia, UAE, South Africa, Israel, Turkey, Brazil, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The data center blade server market is fundamentally evolving around the principles of modularity and disaggregation. The traditional value proposition of server consolidation is now secondary to the architecture's role as a foundation for next-generation workloads.

- The integration of a unified fabric and a high-speed chassis backplane is critical, enabling true composable infrastructure where resources are pooled and provisioned on demand. Technologies like Compute Express Link (CXL) are transforming the blade enclosure into a dynamic system, supporting features like memory pooling and resource disaggregation.

- This allows for the deployment of specialized, accelerator-enabled models without replacing the entire shared infrastructure. For boardroom decisions, this translates into a more flexible capital expenditure strategy, where investments in the chassis are future-proofed against rapid changes in processor and accelerator technology. Deployments using this architecture have achieved a 30% reduction in processing time for data-intensive tasks.

- The focus is now on hot-swappable components, software-defined management, and the ability of the blade chassis to support high-density computing with superior compute-per-square-foot metrics.

What are the Key Data Covered in this Data Center Blade Server Market Research and Growth Report?

-

What is the expected growth of the Data Center Blade Server Market between 2026 and 2030?

-

USD 11.97 billion, at a CAGR of 9.1%

-

-

What segmentation does the market report cover?

-

The report is segmented by Form Factor (Half height blade, Full height blade, and Others), Type (Tier 3, Tier 4, Tier 2, and Tier 1), Application (Virtualization and cloud computing, AI and ML workloads, Big data analytics, and Others) and Geography (North America, Europe, APAC, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

North America, Europe, APAC, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Exponential growth of artificial intelligence (AI) and machine learning (ML), High initial capital expenditure and company lock-in due to proprietary

-

-

Who are the major players in the Data Center Blade Server Market?

-

Atos SE, Cisco Systems Inc., Dell Technologies Inc., Fujitsu Ltd., Hewlett Packard, Hitachi Vantara LLC, Hon Hai Precision. Ltd., Huawei Technologies Co. Ltd., IBM Corp., Inspur Group., Inventec Corp., Lenovo Group Ltd., NEC Corp., New H3C Technologies, Oracle Corp., Penguin Solutions, Quanta Computer lnc., Sugon Information Co., Super Micro Computer Inc. and Wistron Corp.

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of operational efficiency and a lower total cost of ownership (TCO). The adoption of sophisticated software-defined management platforms is proving critical, with some organizations achieving a 40% reduction in server provisioning time, directly lowering operational expenditure (Opex). This is particularly relevant for hyperscale cloud providers and large enterprises managing mission-critical workloads.

- Furthermore, the focus on sustainability is driving demand for blade systems that can operate with superior energy efficiency. Deployments utilizing integrated liquid cooling have demonstrated the ability to achieve a Power Usage Effectiveness (PUE) ratio below 1.1, a significant improvement over traditional air-cooled infrastructure.

- This efficiency gain is crucial for managing the high capital expenditure (Capex) associated with modern data center builds and meeting stringent environmental regulations, making blade architecture a strategic choice for sustainable, large-scale computing.

We can help! Our analysts can customize this data center blade server market research report to meet your requirements.

RIA -

RIA -