Dental Surgical Equipment Market Size 2025-2029

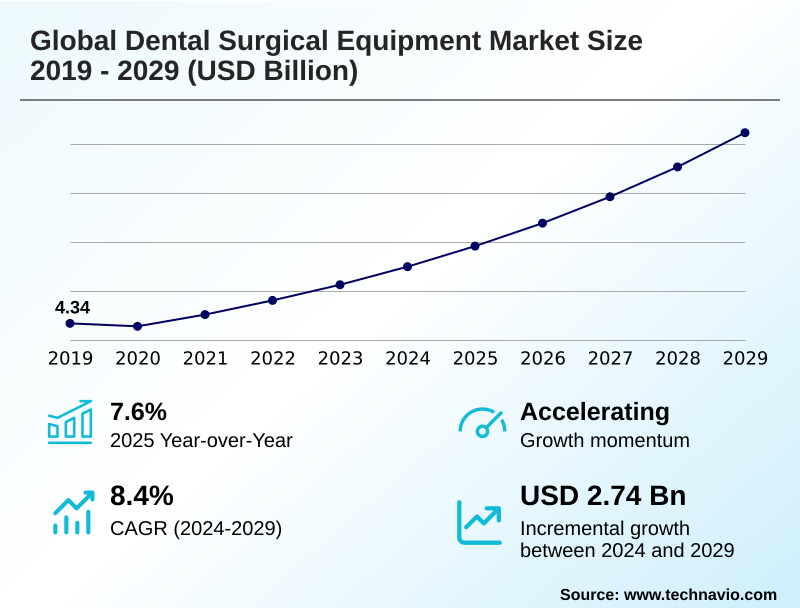

The dental surgical equipment market size is valued to increase by USD 2.74 billion, at a CAGR of 8.4% from 2024 to 2029. Increasing prevalence of dental diseases and related risk factors will drive the dental surgical equipment market.

Major Market Trends & Insights

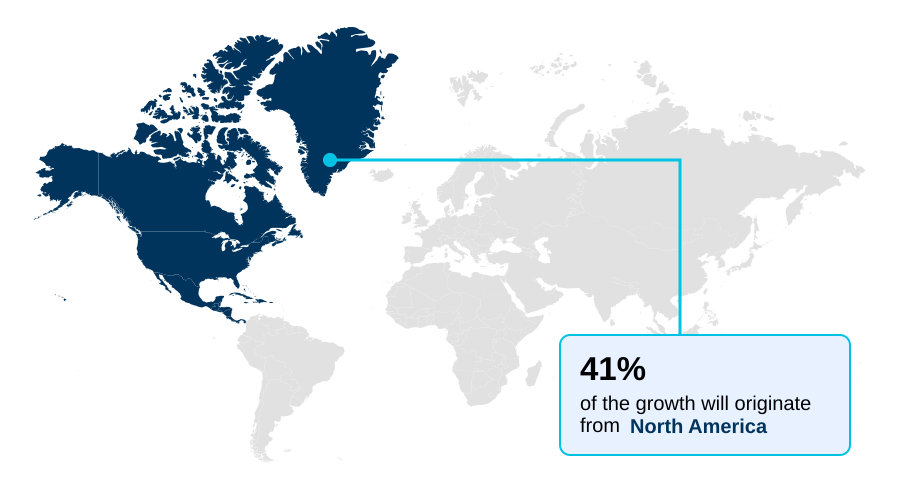

- North America dominated the market and accounted for a 40.7% growth during the forecast period.

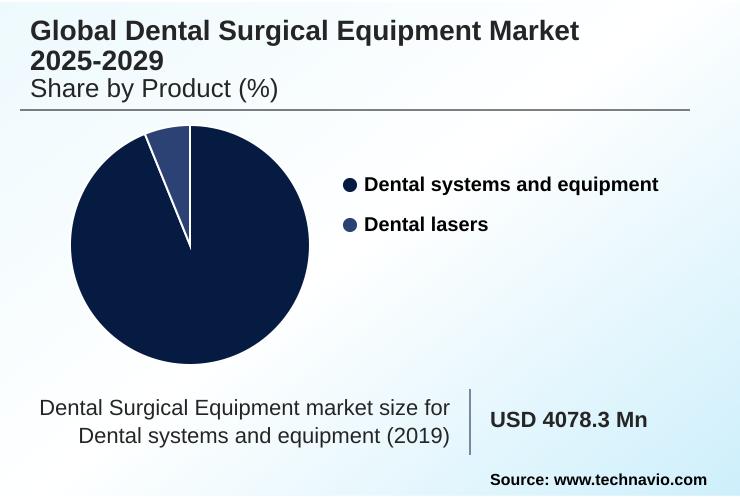

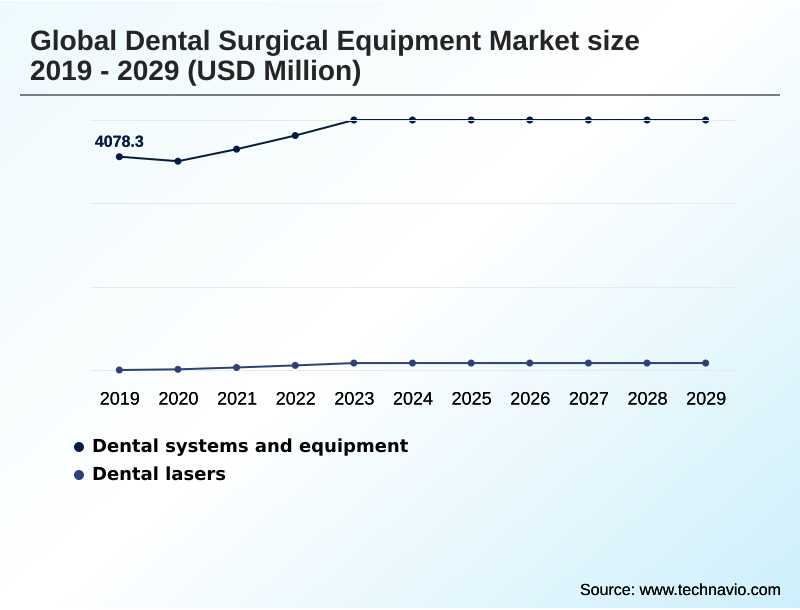

- By Product - Dental systems and equipment segment was valued at USD 4.73 billion in 2023

- By End-user - Clinics segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 3.89 billion

- Market Future Opportunities: USD 2.74 billion

- CAGR from 2024 to 2029 : 8.4%

Market Summary

- The dental surgical equipment market is defined by a continuous drive toward procedural precision and enhanced patient outcomes. A core driver is the rising incidence of oral diseases, which necessitates sophisticated interventions from restorative dentistry workflows to complex maxillofacial reconstructive surgery.

- This demand is met by rapid technological evolution, particularly in digital dentistry integration, where tools like cone beam computed tomography and intraoral scanners are becoming standard for evidence-based treatment planning. These systems facilitate minimally invasive dentistry and enable the use of advanced biomaterials for bone grafting.

- A significant trend is the adoption of chairside fabrication, where a clinic can design, mill, and place a permanent restoration in a single visit, drastically improving clinical workflow efficiency. However, the high capital equipment investment required for technologies such as robotic-assisted implant surgery and dental operating microscopes presents a considerable challenge.

- Many practices must balance the clear benefits of enhanced diagnostic accuracy and procedural predictability against significant dental clinic overhead management, influencing procurement decisions between new and refurbished dental equipment market options.

What will be the Size of the Dental Surgical Equipment Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Dental Surgical Equipment Market Segmented?

The dental surgical equipment industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- Product

- Dental systems and equipment

- Dental lasers

- End-user

- Clinics

- Hospitals

- Therapeutic area

- Restorative dentistry

- Orthodontics

- Endodontics

- Prosthodontics

- Others

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By Product Insights

The dental systems and equipment segment is estimated to witness significant growth during the forecast period.

The dental surgical equipment market is segmented by product into dental systems and equipment, and dental lasers.

The dental systems and equipment segment, which includes advanced cad/cam dental systems and chairside dental milling units, is driven by the pursuit of clinical workflow efficiency.

Innovations in this area focus on integrating digital impression systems with fabrication processes, achieving over 99% dimensional stability in 3d printed surgical guides. This allows for the creation of patient-specific implants and enhances restorative dentistry workflows.

The segment also covers foundational equipment where dental practice ergonomics are critical.

Meanwhile, the dental lasers segment, encompassing both soft tissue lasers and all-tissue dental lasers, is expanding due to its applications in minimally invasive dentistry, offering significant advantages in periodontal regenerative procedures and reducing post-operative recovery improvement.

The Dental systems and equipment segment was valued at USD 4.73 billion in 2023 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 40.7% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Dental Surgical Equipment Market Demand is Rising in North America Get Free Sample

The geographic landscape of the market is characterized by varied adoption rates and investment priorities.

North America accounts for over 40% of the market's incremental growth, driven by high healthcare expenditure and the widespread adoption of digital dentistry integration, with advanced digital workflows reducing prosthetic turnaround times by more than 50% in many clinics.

Europe follows, with a strong emphasis on high-quality engineering and procedural predictability, particularly in its well-established private dental practice economics.

The Asia region presents a dynamic environment where rising healthcare investment fuels demand for a broad range of technologies, from foundational dental autoclaves to advanced endodontic motors.

In the Rest of World, which includes burgeoning markets in South America and the Middle East, the focus is often on capital equipment investment that balances cost with performance, influencing dental service organization procurement strategies.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the dental surgical equipment market is increasingly complex, shaped by a confluence of technological, economic, and clinical factors. A key consideration for many practices is the total cost of dental implant surgery equipment, which extends beyond the initial purchase to include ongoing maintenance costs for CAD CAM systems and the need for specialized dental professional training programs.

- The benefits of using dental lasers for soft tissue management with lasers are well-documented, yet their adoption is weighed against the initial investment. Similarly, comparing intraoral scanner accuracy levels is a critical step in procurement, as this directly impacts the efficacy of a digital workflow for crown fabrication.

- The return on investment (roi) on chairside milling systems is a major discussion point, balancing convenience against cost. In endodontics, the endodontic success rate with microscopes is driving their integration into practice. The industry also sees innovation in foundational areas, with ongoing improvements in the ergonomics of dental operator stools and advances in dental suction systems.

- Technology such as cbct radiation dose reduction techniques and navigational systems in implantology are changing standards of care. Simultaneously, challenges in digital impression taking persist, while trends in dental local anesthesia delivery continue to evolve. The rise of 3d printing for orthodontic aligners and new material selection for 3d printed crowns highlight the shift toward customized, patient-centric solutions.

What are the key market drivers leading to the rise in the adoption of Dental Surgical Equipment Industry?

- The increasing prevalence of dental diseases and their associated risk factors is a key driver fueling market growth.

- Market growth is fundamentally driven by the high global prevalence of oral diseases and an expanding geriatric population.

- Data indicates that approximately three out of every 10 individuals aged 65-74 have complete tooth loss, creating sustained demand for prosthodontic rehabilitation and dental implant motors.

- Additionally, with an average of seven in 10 schoolchildren experiencing tooth decay, the need for restorative dentistry workflows is constant. This clinical demand is supported by favorable reimbursement policies and an increasing number of dental professionals worldwide.

- This expansion of the dental workforce, coupled with greater public awareness, fuels capital equipment investment in technologies that support both foundational procedures and complex interventions like maxillofacial reconstructive surgery and endodontic retreatment protocols.

What are the market trends shaping the Dental Surgical Equipment Industry?

- Technological advances and a consistent stream of new product launches are prominent trends shaping the market. These innovations are enhancing procedural efficiency and expanding treatment capabilities.

- Key trends are reshaping the market, driven by innovations that enhance precision and efficiency. The adoption of 3D printing technologies is accelerating, with new systems reducing material consumption by up to 85% compared to traditional subtractive manufacturing. This technology is central to producing patient-matched medical devices and surgical guides.

- Another significant development is the integration of robotic-assisted implant surgery, which improves procedural predictability. Furthermore, advancements in intraoral scanners and digital smile design software are streamlining prosthodontic rehabilitation and same-day restorations.

- Strategic mergers and acquisitions are also prevalent, enabling companies to consolidate technologies like photobiomodulation therapy and expand their global footprint, thereby influencing private dental practice economics and fostering a more competitive landscape focused on integrated digital solutions.

What challenges does the Dental Surgical Equipment Industry face during its growth?

- The high cost associated with advanced dental equipment poses a significant challenge to market adoption and industry growth.

- The primary challenge facing the market is the substantial cost of advanced equipment, which constrains adoption, particularly for smaller clinics. The investment required for a high-end chairside milling unit can be more than ten times that of a basic clinical setup, a significant hurdle when practice overheads already average around 75%.

- This economic pressure makes dental clinic overhead management a critical concern and drives a segment of the market toward the refurbished dental equipment market as a cost-effective alternative. Furthermore, disparities in access to care and limited dental insurance reimbursement codes in many regions restrict the patient base for advanced procedures.

- Intense competition also pressures margins, compelling companies to innovate while managing costs across their supply chains for items ranging from surgical handpieces to obturation systems.

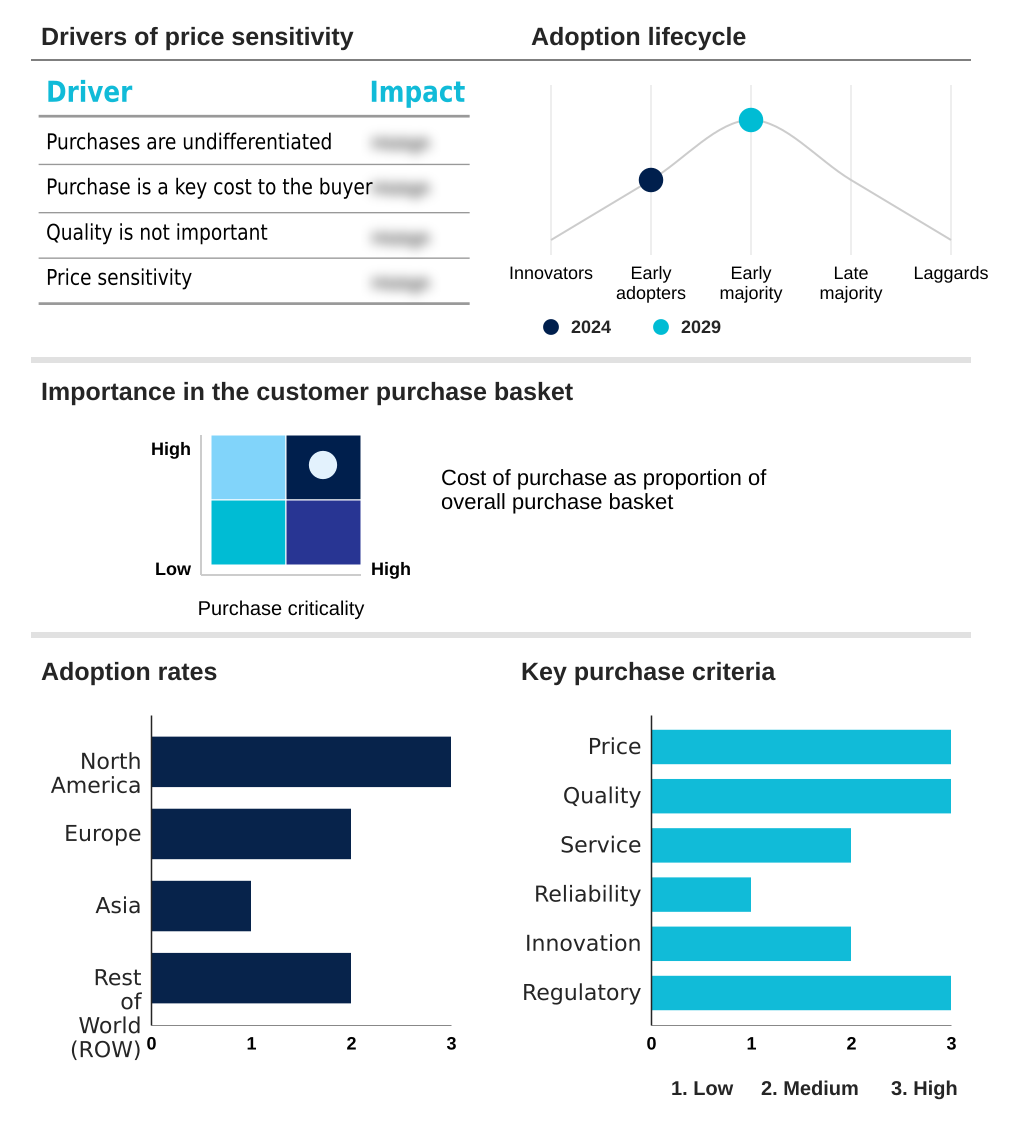

Exclusive Technavio Analysis on Customer Landscape

The dental surgical equipment market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the dental surgical equipment market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Dental Surgical Equipment Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, dental surgical equipment market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

3Shape AS - Key offerings include advanced intraoral scanners, lab scanners, CBCT systems, and integrated CAD/CAM solutions for comprehensive digital dentistry workflows.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- 3Shape AS

- A dec Inc.

- Alliage SA

- AMD Lasers Inc.

- BIOLASE Inc.

- Carestream Dental LLC

- Coltene Whaledent AG

- DENTAURUM GmbH

- Dentsply Sirona Inc.

- Envista Holdings Corp.

- GC Corp.

- Henry Schein Inc.

- Institut Straumann AG

- Ivoclar Vivadent AG

- Midmark Corp.

- Patterson Dental

- Planmeca Oy

- Septodont Holding

- Ultradent Products Inc.

- ZimVie Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Dental surgical equipment market

- In September, 2024, Dentsply Sirona introduced Primescan 2, a cloud-native intraoral scanning solution designed to streamline restorative workflows by enabling wireless scanning directly to cloud platforms, significantly reducing turnaround times.

- In August, 2024, Case Western Reserve University School of Dental Medicine completed a $2.6 million renovation of its simulation clinic, which included a $350,000 investment in Bien-Air Optima MX2 electric motor systems and other state-of-the-art dental technology.

- In February, 2025, Oral Care announced a strategic partnership with De Tandartsengroep to enhance its operational capabilities and expand its service portfolio by integrating advanced dental technologies across its network.

- In May, 2025, the Straumann Group is expected to complete the full acquisition of maxon dental GmbH, a move aimed at strengthening its portfolio in dental biomaterials and regenerative solutions.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Dental Surgical Equipment Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2024 |

| Historic period | 2019-2023 |

| Forecast period | 2025-2029 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.4% |

| Market growth 2025-2029 | USD 2735.9 million |

| Market structure | Fragmented |

| YoY growth 2024-2025(%) | 7.6% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, Japan, India, South Korea, Indonesia, Thailand, Brazil, Saudi Arabia, UAE, South Africa, Argentina, Turkey, Egypt and Nigeria |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The dental surgical equipment market is advancing through the integration of sophisticated digital technologies and precision-engineered systems. Innovations in cad/cam dental systems and chairside dental milling are redefining restorative procedures, while the adoption of cone beam computed tomography and digital impression systems enhances diagnostic capabilities.

- The market sees continuous development in specialized tools like piezoelectric surgery units and endodontic motors, which offer greater control and predictability. A key metric of this progress is the ability of new-generation 3d printed surgical guides to achieve over 99% dimensional stability, directly impacting the success of computer-guided implant placement.

- Developments in materials, including zirconia milling blocks and high-performance polymers, complement these hardware advancements. However, the significant upfront cost of technologies like dental operating microscopes and robotic-assisted implant surgery forces a critical evaluation in boardroom budgeting, where the long-term benefits of improved outcomes must be weighed against immediate capital expenditure.

- This economic reality shapes procurement strategies, influencing decisions around adopting everything from advanced dental implant motors and guided surgery platforms to essential sterilization equipment like dental autoclaves and ultrasonic cleaners.

What are the Key Data Covered in this Dental Surgical Equipment Market Research and Growth Report?

-

What is the expected growth of the Dental Surgical Equipment Market between 2025 and 2029?

-

USD 2.74 billion, at a CAGR of 8.4%

-

-

What segmentation does the market report cover?

-

The report is segmented by Product (Dental systems and equipment, and Dental lasers), End-user (Clinics, and Hospitals), Therapeutic Area (Restorative dentistry, Orthodontics, Endodontics, Prosthodontics, and Others) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of dental diseases and related risk factors, High cost of dental equipment

-

-

Who are the major players in the Dental Surgical Equipment Market?

-

3Shape AS, A dec Inc., Alliage SA, AMD Lasers Inc., BIOLASE Inc., Carestream Dental LLC, Coltene Whaledent AG, DENTAURUM GmbH, Dentsply Sirona Inc., Envista Holdings Corp., GC Corp., Henry Schein Inc., Institut Straumann AG, Ivoclar Vivadent AG, Midmark Corp., Patterson Dental, Planmeca Oy, Septodont Holding, Ultradent Products Inc. and ZimVie Inc.

-

Market Research Insights

- Market dynamics are increasingly shaped by the pursuit of efficiency and improved clinical outcomes, supported by robust data. The adoption of advanced fabrication methods, for instance, reduces material waste by up to 85% compared to traditional machining, directly impacting dental clinic overhead management.

- Furthermore, the integration of digital workflows has been shown to reduce patient chair time by an average of 25%, a critical factor for private dental practice economics and patient satisfaction. This shift toward digital dentistry integration is a key component of capital equipment investment strategies, particularly for dental service organization procurement.

- As procedural predictability becomes a primary purchasing criterion, technologies that support evidence-based treatment planning are seeing higher adoption, influencing decisions across the refurbished dental equipment market and for new acquisitions.

We can help! Our analysts can customize this dental surgical equipment market research report to meet your requirements.

RIA -

RIA -