Diesel Engine Market Size 2024-2028

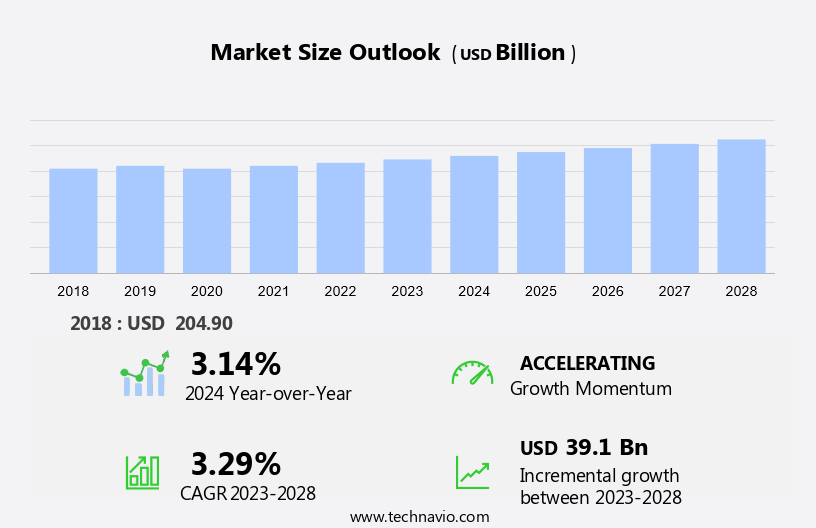

The diesel engine market size is forecast to increase by USD 39.1 billion at a CAGR of 3.29% between 2023 and 2028.

- The market exhibits significant growth due to increasing demand for diesel engines, particularly In the Asia-Pacific region. Thermal efficiency and power output are key advantages of diesel engines, making them a preferred choice for industries such as mining and construction. However, the rising popularity of electric vehicles (EVs) and the high cost of diesel engines are major challenges. Gas prices also impact the market dynamics, with fluctuations influencing the competitiveness of diesel engines. Despite these challenges, the market continues to expand, driven by its proven performance and efficiency in power generation and automobiles.

What will be the Size of the Diesel Engine Market During the Forecast Period?

- The market encompasses various industries, including construction, automobiles, power generation, and heavy-end equipment. These engines are renowned for their efficiency and reliability, making them a preferred choice for numerous applications. In the construction sector, diesel engines power heavy machinery such as excavators, bulldozers, and cranes. Their high thermal efficiency makes them ideal for heavy-duty applications, ensuring productivity and reducing operational costs. The manufacturing sector relies on diesel engines for powering auxiliary equipment, including compressors, generators, and pumps. These engines' strength and reliability make them indispensable in industrial settings. In the power generation sector, diesel engines are used to generate electricity, particularly in areas where grid power is unavailable or unreliable. Their ability to provide a consistent power source makes them a popular choice for data centers and telecommunication facilities. The oil and gas sector utilizes diesel engines in drilling operations and for powering equipment in offshore platforms. Their high power-to-weight ratio and fuel efficiency make them an ideal choice for these applications.

- In the health care sector, diesel engines are used to power emergency generators and backup power systems. Their reliability and ability to provide a consistent power source make them essential in critical applications. The mining sector heavily relies on diesel engines to power heavy machinery, including trucks, loaders, and drills. Their power output and durability make them a preferred choice for these applications. In the transportation sector, diesel engines power heavy vehicles, including buses, trucks, and trains. Their fuel efficiency and power output make them a popular choice for long-haul transportation applications. The agricultural sector uses diesel engines to power tractors and other heavy equipment. Their reliability and power output make them essential for farming operations. The maritime sector utilizes diesel engines to power ships and boats. Their high power output and fuel efficiency make them a preferred choice for marine applications. Infrastructural developments, such as road construction and bridge building, require heavy machinery, which is often powered by diesel engines. Their power output and reliability make them an ideal choice for these applications. Diesel engines are also used in various applications, including motorcycles, chainsaws, and heavy-duty pumps. Their power output and fuel efficiency make them a popular choice for these applications. Gas prices play a significant role In the market. When gas prices are high, diesel engines become more attractive due to their fuel efficiency.

- However, when gas prices are low, gasoline engines may become more cost-effective. In summary, the market is diverse and encompasses various industries and applications. Their high thermal efficiency, power output, and reliability make them an ideal choice for heavy-duty applications. The price of gas is a significant factor In the market, with diesel engines becoming more attractive when gas prices are high.

How is this Diesel Engine Industry segmented and which is the largest segment?

The diesel engine industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- End-user

- On road

- Off road

- Geography

- APAC

- China

- India

- Japan

- Europe

- Germany

- North America

- US

- South America

- Middle East and Africa

- APAC

By End-user Insights

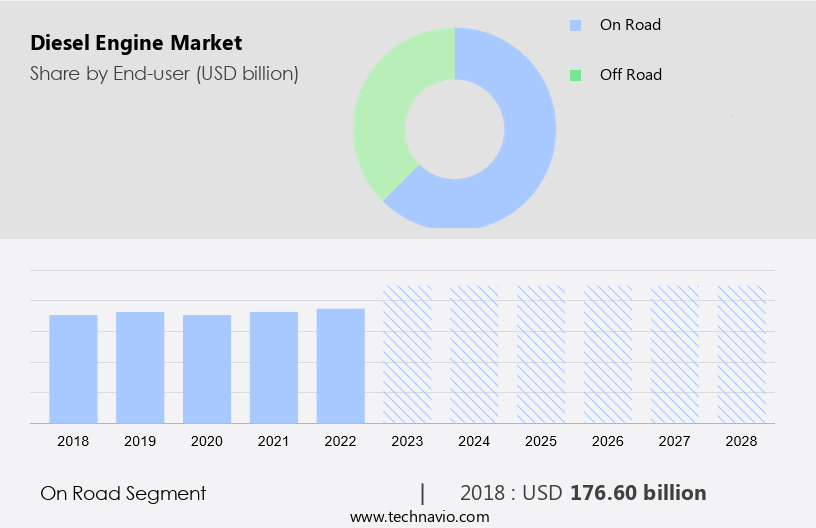

- The on-road segment is estimated to witness significant growth during the forecast period.

The market encompasses various applications, with the on-road segment being a significant contributor. This segment comprises light-duty vehicles, medium-duty vehicles, and heavy-duty vehicles. Light-duty vehicles, which include passenger cars, are gaining popularity in developing countries due to rising disposable incomes. Diesel engines offer better fuel efficiency and operational advantages, making diesel-powered cars an attractive choice when compared to their gasoline counterparts. The affordability of diesel fuel is another factor fueling the demand for diesel engine cars.

Moving on to heavy-duty vehicles, also known as heavy-duty vehicles (HDVs), they consist of medium-duty trucks (3.5-15 tonnes), heavy-duty trucks (more than 15 tonnes), and minibusses. Light-duty trucks, or LDVs, are also part of this category and include light trucks used for transporting people and light commercial vehicles used for freight (< 3.5 tonnes). The thermal efficiency of diesel engines makes them a preferred choice for heavy-duty applications in industries like mining and construction, where high power output and fuel economy are crucial. Despite the high upfront cost of diesel engines, their long-term operational benefits make them a worthwhile investment.

Get a glance at the Diesel Engine Industry report of share of various segments Request Free Sample

The On road segment was valued at USD 176.60 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

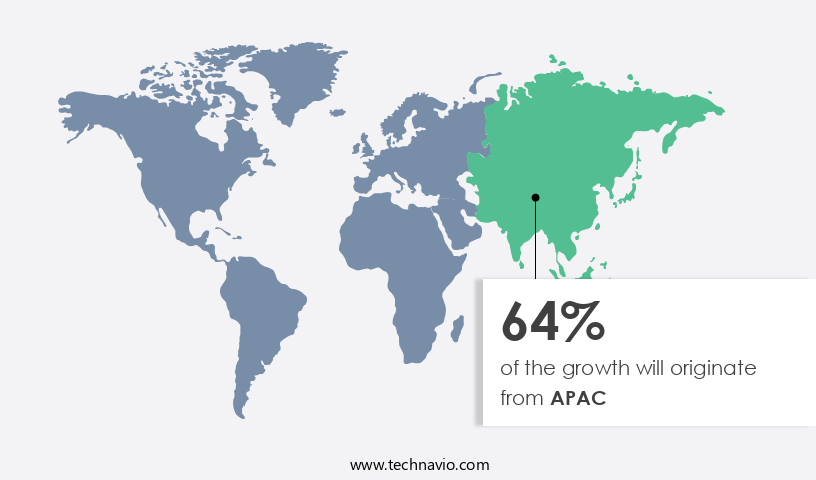

- APAC is estimated to contribute 64% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The Asia Pacific (APAC) region plays a significant role In the market due to its large imports and the presence of various sectors such as ships, trains, automotive vehicles, and power generation. The region's infrastructure projects and transportation networks also contribute to the market's growth. One of the primary reasons for the region's dominance is the lower labor costs, enabling cost-effective production for diesel engine manufacturers. Furthermore, the substantial agriculture, construction, and automotive markets in countries like China, India, Japan, and South Korea are driving the demand for diesel engines. With the increasing population and economic development in APAC, the demand for agricultural equipment is also on the rise.

In 2021, the demand for agricultural products was high In the region, leading to an anticipated increase In the demand for better harvesting machinery. Strict emission regulations are becoming increasingly stringent, and diesel engine manufacturers are focusing on producing engines that meet these standards. This trend is expected to continue, further boosting the market in APAC.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Diesel Engine Industry?

Growing demand for diesel engines from APAC is the key driver of the market.

- The demand for diesel engines is experiencing growth In the Asia Pacific (APAC) region, primarily driven by the expansion of the construction, mining, transportation, and industrial sectors. The need for dependable power sources, expanding power generation capacity, and the proliferation of manufacturing and processing industries are major factors fueling the market in APAC. China, India, and Indonesia are primary markets for diesel engines in this region due to their strong economic growth and significant infrastructure investments, particularly in road and railway development. Moreover, international manufacturers are attracted to setting up their manufacturing facilities in this region, particularly in China and India, due to the cost benefits these countries provide.

- Additionally, environmental concerns, such as the need for cleaner engines, are increasingly influencing the market. Agriculture remains a significant consumer of diesel engines, with agricultural mechanization being a major driver of demand. However, the shift towards electric and hybrid vehicles is expected to impact the market negatively. The APAC region will continue to be the fastest-growing major economy In the world, further boosting the demand for diesel engines. In summary, the market in APAC is poised for steady growth due to the region's economic expansion, infrastructure development, and the continued demand for diesel engines in various industries.

What are the market trends shaping the Diesel Engine Industry?

The growing popularity of EVs (electric vehicles) is the upcoming market trend.

- The increasing popularity of electric vehicles (EVs), specifically battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs), poses a significant challenge for the market. EVs are becoming increasingly preferred due to their reduced environmental impact and compliance with emission regulations set by various environmental regulatory bodies worldwide. EVs provide numerous advantages, including lower operating costs due to the cheaper price of electricity compared to gasoline, diesel, and petrol, and fewer moving parts, resulting in reduced maintenance costs.

- Moreover, EVs offer superior performance, providing smooth acceleration, strong torque, excellent handling, and quiet operation. These benefits make EVs an attractive alternative to diesel-powered vehicles in various sectors such as construction, manufacturing, health care, oil and gas, telecommunications, data centers, and mining. The environmental, social, and economic benefits of EVs are driving their adoption, making them a formidable competitor In the automotive market.

What challenges does the Diesel Engine Industry face during its growth?

The high cost of diesel engines is a key challenge affecting the industry's growth.

- Diesel engines incur higher costs compared to their gasoline counterparts due to several factors. One reason is the requirement of advanced technologies such as turbochargers and intake air intercoolers in diesel engines to enhance their performance. The longer stroke of diesel engines, which results from higher compression, also increases the bore length and drives up costs. In regions with low temperatures, glow plugs are essential for diesel engines to operate efficiently, adding to the overall cost.

- Moreover, the technology needed to meet stringent emission norms, including the reduction of particulate matter and NOx, is expensive. In the Medium Power category and High Power segment of the Commercial vehicles sector and Off-highway vehicles, as well as In the Automotive sector, digitalization, sustainability, resilience, and infrastructure investments are key trends. As the market for diesel engines continues to evolve, it is crucial for stakeholders to stay informed and adapt to these trends to remain competitive.

Exclusive Customer Landscape

The diesel engine market forecasting report includes the adoption lifecycle of the market, market growth and forecasting, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the diesel engine market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, diesel engine market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry. The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AB Volvo

- AGCO Corp.

- BorgWarner Inc.

- Caterpillar Inc.

- Continental AG

- Cummins Inc.

- Deere and Co.

- DEUTZ AG

- Doosan Corp.

- General Motors Co.

- Hyundai Heavy Industries Group

- Kohler Co.

- Kubota Corp.

- Mercedes Benz Group AG

- Mitsubishi Heavy Industries Ltd.

- Robert Bosch GmbH

- Rolls Royce Holdings Plc

- Volkswagen AG

- Wartsila Corp.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market is a significant contributor to various industries, including construction, manufacturing, healthcare, oil, gas, telecommunication, data centers, mining, and power generation. It offers high thermal efficiency, making them a preferred choice for applications requiring high power output. The automotive sector, particularly heavy vehicles and commercial vehicles, is a major consumer due to their fuel efficiency and power capabilities. However, the increasing focus on environmental concerns and stringent emission regulations has led to the development of cleaner alternatives, such as electric and hybrid vehicles. This shift may impact the demand, particularly In the automotive sector. Despite this, the demand remains strong in sectors such as infrastructure projects, transportation networks, and heavy-end equipment applications, including mining, ships, trains, and heavy vehicles.

Thus, the high-cost used in these applications offer superior power and efficiency, making them a necessary investment for these industries. Two-stroke and four-stroke continue to dominate the market, with the latter gaining popularity due to their lower emissions and improved fuel efficiency. The market in portable equipment, motorcycles, chainsaws, and other applications is also growing, driven by the need for power in remote locations and the increasing demand for mechanization in agriculture. The market is expected to grow, driven by infrastructure investments, digitalization, and the need for resilience in various industries. The market is also witnessing innovation In the form of advanced technologies aimed at improving thermal efficiency and reducing emissions.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

156 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 3.29% |

|

Market growth 2024-2028 |

USD 39.1 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

3.14 |

|

Key countries |

US, China, Germany, Japan, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Diesel Engine Market Research and Growth Report?

- CAGR of the Diesel Engine industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, Europe, North America, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the diesel engine market growth of industry companies

We can help! Our analysts can customize this diesel engine market research report to meet your requirements.

RIA -

RIA -