Enterprise Application And Integration Market Size 2024-2028

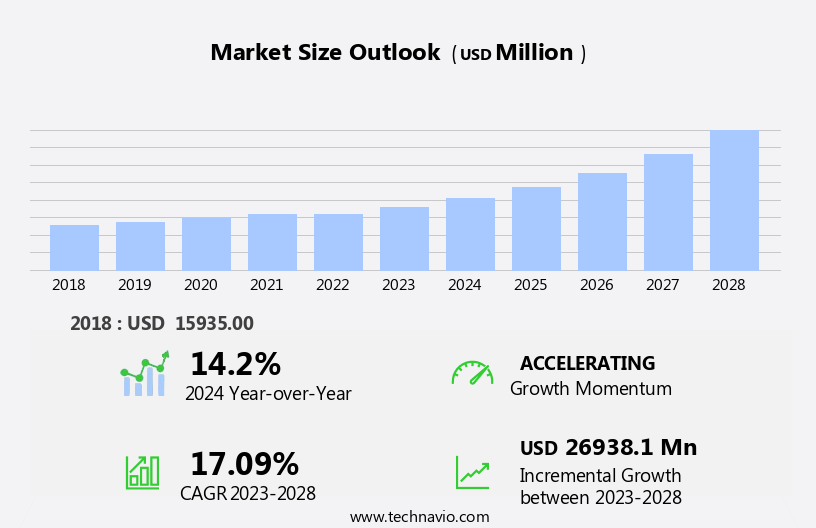

The enterprise application and integration market size is forecast to increase by USD 26.94 billion at a CAGR of 17.09% between 2023 and 2028.

- The Enterprise Application Integration (EAI) market is experiencing significant growth due to the increasing need to enhance business process efficiency. This trend is driven by the widespread adoption of cloud-based integration solutions, such as Integration Platform as a Service (iPaaS), Application Programming Interfaces (APIs), and data integration. The Internet of Things (IoT) and Platform-as-a-Service (PaaS) are also fueling market growth as businesses seek to connect various software applications and systems.

- Data security remains a major concern for enterprises, leading to increased investment in EAI solutions that provide robust security features. Additionally, the integration of Artificial Intelligence (AI) and Business Intelligence (BI) tools, as well as Analytics and Big Data, is becoming increasingly important for gaining valuable insights from data.

What will be the Size of the Enterprise Application And Integration Market During the Forecast Period?

- The market encompasses a range of solutions designed to connect and optimize various business systems and processes. Key components include ERP systems, business intelligence, and middleware infrastructure. Cloud computing is driving significant growth in this market, enabling the integration of SaaS applications and facilitating digital transformation.

- Big data and IoT are also major trends, necessitating advanced integration capabilities to support real-time data exchange and analysis. Open-source software and APIs, such as Anypoint Exchange and Turbo Connector, are increasingly popular for their flexibility and cost-effectiveness. Businesses are focusing on process optimization, data security, and remote work solutions to address IT complexity and enhance connectivity with business partners.

- Integration challenges extend to banking systems, SCM, CRM, and B2B, necessitating the use of Enterprise Service Bus, adapters, and middleware. Digital transformation initiatives continue to fuel market expansion, with a growing emphasis on data security concerns and business process optimization.

How is this Enterprise Application And Integration Industry segmented and which is the largest segment?

The enterprise application and integration industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Deployment

- On-premise

- Cloud

- End-user

- BFSI

- Government

- IT and telecom

- Healthcare

- Others

- Geography

- North America

- Canada

- US

- Europe

- Germany

- APAC

- China

- Japan

- South America

- Middle East and Africa

- North America

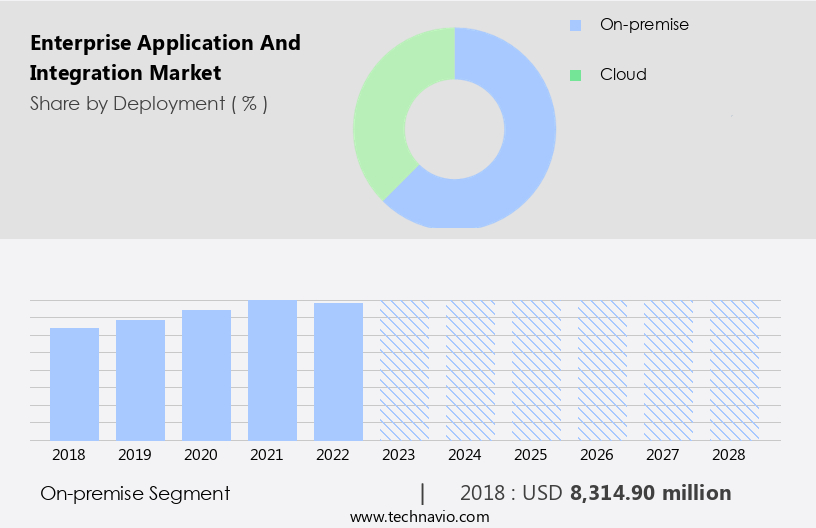

By Deployment Insights

- The on-premise segment is estimated to witness significant growth during the forecast period.

The market encompasses solutions that enable seamless data exchange and process automation among various business applications and systems. ERP systems, BI applications, and middleware infrastructure form the core of this market. Cloud computing, Big Data, IoT, and opensource software are driving innovation. Digital transformation necessitates integration across banking systems, such as Backbase and Grand Central, and IT environments. Large enterprises prioritize business process optimization, data security concerns, and remote work. The cloud segment is expanding due to hybrid integration and cloud-based technologies. AI-driven integration streamlines processes with business partners. Enterprise Service Bus, adapters, and middleware address IT complexity. The on-premises model, while secure, requires significant investments.

Key verticals include SCM, CRM, business intelligence, e-commerce, and TIBCO Software. Venture capital, mergers, acquisitions, and the volume of data fuel market growth. IT infrastructure, customers, web, wireless, and large enterprises continue to shape the landscape.

Get a glance at the Enterprise Application And Integration Industry report of share of various segments Request Free Sample

The On-premise segment was valued at USD 8.31 billion in 2018 and showed a gradual increase during the forecast period.

Regional Analysis

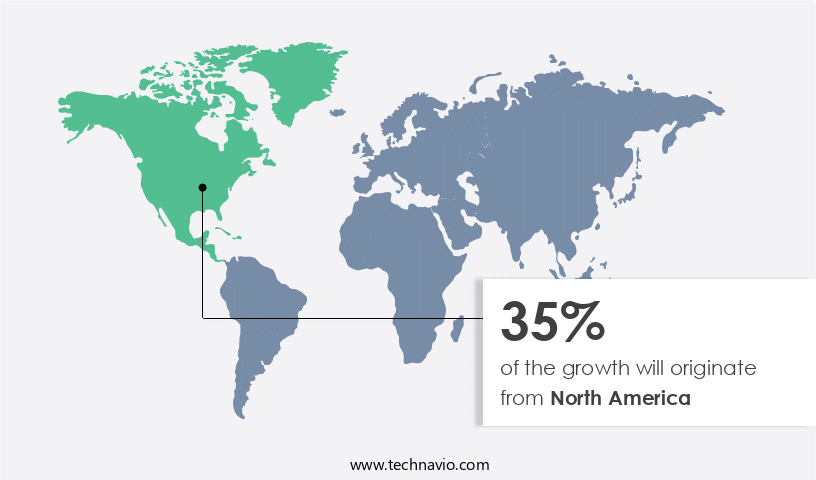

- North America is estimated to contribute 35% to the growth of the global market during the forecast period.

Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market share of various regions, Request Free Sample

The market in North America is experiencing significant growth due to the increasing adoption of application integration solutions by businesses in the region. This trend is driven by the competitive business environment and the need for operational efficiency. The rise of cloud computing is also a key factor, enabling the easy integration of various application software and service platforms. Additionally, the widespread adoption of CRM systems via the cloud is common among North American organizations, leading to the adoption of hybrid models that combine on-premises and cloud solutions. The integration of ERP systems, Business Intelligence applications, and Middleware infrastructure is essential for large enterprises to optimize business processes and ensure data security.

The increasing volume of data, driven by IoT and Big Data, necessitates the use of integration platforms and IT environments that can handle complex IT infrastructures. Cloud-based technologies, such as Turvo Connector, Anypoint Exchange, and Salsify, are popular solutions for integration and digital transformation. The integration of business services, including SCM, E-commerce, and TIBCO Software, is also crucial for businesses in various verticals. Despite the benefits, data security concerns and the complexity of IT environments remain challenges for organizations undergoing integration. Remote work and banking systems also require robust integration solutions. In conclusion, the market in North America is poised for growth, driven by the adoption of cloud computing, hybrid IT solutions, and the need for business process optimization.

Market Dynamics

The Venture Capital (VC) investment landscape is also showing an upward trend In the EAI market, indicating strong industry growth potential. Market challenges include the complexity of integrating legacy systems, ensuring data accuracy and consistency, and managing the increasing volume and variety of data. E-commerce and CRM applications are major areas of focus for EAI solutions, as businesses strive to provide seamless customer experiences and improve operational efficiency. Overall, the EAI market is poised for continued growth as businesses seek to streamline their operations and gain a competitive edge through effective data integration and management.

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise In the adoption of Enterprise Application And Integration Industry?

Enhance the efficiency of business processes is the key driver of the market.

- Enterprise Application Integration (EAI) is a vital aspect of modern business operations, enabling seamless communication and data exchange between various software applications. With the proliferation of ERP systems, CRM, SCM, and BI applications, managing data and processes across these systems has become a complex task. This complexity arises due to the existence of multiple applications, each functioning as an independent information silo. To address this challenge, businesses are turning to integration solutions such as Enterprise Service Bus, Middleware, and Integration Platforms. These solutions facilitate the exchange of data and business rules between applications, enabling effective decision-making and process optimization.

- Moreover, the advent of cloud computing, Big Data, IoT, and OpenSource software has further complicated IT environments, necessitating advanced integration solutions. Digital transformation initiatives, such as Electronic Data Interchange and B2B connectivity, require secure and efficient data exchange between business partners. Data security concerns, remote work, and the increasing volume of data are critical factors driving the adoption of these solutions. Banking systems, too, are embracing integration technologies, with platforms facilitating seamless integration of various banking applications. The IT infrastructure landscape is evolving, with an increasing focus on hybrid integration and cloud-based technologies.

- Large enterprises are investing in AI-driven integration to optimize processes and improve customer experience. The integration market is witnessing significant growth, fueled by mergers and acquisitions, venture capital investments, and the increasing complexity of IT environments. The market caters to various verticals, including manufacturing, healthcare, retail, and finance, providing business services and solutions tailored to their unique requirements.

What are the market trends shaping the Enterprise Application And Integration Industry?

Increased adoption of cloud-based integration solutions is the upcoming market trend.

- The market: Cloud-Based Solutions Drive Business Transformation Enterprises are increasingly adopting cloud computing solutions to modernize their IT infrastructure and optimize business processes. Cloud computing enables organizations to move their Enterprise Resource Planning (ERP) systems and Business Intelligence (BI) applications to the cloud, integrating them with other back-office systems. The popularity of cloud-based integration services is on the rise due to their cost-effectiveness, flexibility, and faster connectivity features. Cloud-based integration services facilitate data exchange within and outside enterprises for various commercial applications. These services are available in two forms: integration platform-as-a-service (iPaaS) and data platform-as-a-service (dPaaS). IPaaS offers a set of cloud-based integration solutions that enable enterprises to integrate their back-office systems without installing physical IT infrastructure.

- Cloud-based integration services play a crucial role in digital transformation, enabling large enterprises to streamline their processes and improve connectivity with their business partners. They also support the integration of various applications, including SCM, CRM, ERP, BI, e-commerce, and EDI. Furthermore, iPaaS solutions enable the seamless integration of IoT devices and Big Data platforms, providing real-time insights to organizations. Data security concerns are a major challenge in cloud-based integration. Enterprises must ensure that their data is secure during transmission and storage. Cloud-based integration solutions offer robust security features, including encryption, access control, and multi-factor authentication, to mitigate these concerns.

- The volume of data being generated and transmitted is increasing exponentially, necessitating the need for efficient integration solutions. Cloud-based integration services enable organizations to manage this complexity, providing a single view of their data across various systems and applications. Additionally, they offer scalability and flexibility, allowing enterprises to easily adapt to changing business requirements. The integration of cloud-based technologies with various verticals, including banking, healthcare, retail, and manufacturing, is driving the growth of the market. The market is expected to continue growing, with AI-driven integration solutions and hybrid integration models gaining popularity. Venture capital investments and mergers and acquisitions are also fueling market growth.

What challenges does the Enterprise Application And Integration Industry face during its growth?

Growing concerns associated with integration is a key challenge affecting the industry growth.

- Enterprise Application Integration (EAI) is a critical aspect of business operations for large enterprises, enabling seamless communication between various applications and systems. However, integrating new Enterprise Resource Planning (ERP) systems, Business Intelligence (BI) applications, and other software solutions with existing Middleware infrastructure can present challenges. Legacy systems, outdated software, and varying OS and hardware configurations are common causes of integration issues. Moreover, the increasing adoption of Cloud computing, Big Data, Internet of Things (IoT), and OpenSource software in digital transformation initiatives adds to the IT complexity. New application software often includes regulatory and compliance features, necessitating integration with banking systems and other industry-specific applications.

- The integration of these new applications with traditional IT environments can hinder smooth operation, particularly In the Cloud segment. Additionally, the volume of data generated by these applications necessitates robust data security concerns, especially with the rise of remote work. Integration Platforms, such as Enterprise Service Bus, Adapters, and Middleware, help address these challenges by providing a unified approach to integration. However, the increasing adoption of AI-driven integration, SCM, CRM, E-commerce, and other business services further adds to the complexity. Hybrid Integration and Cloud-based technologies are becoming increasingly popular to address these challenges. Verticals like BFSI, Telecom, Healthcare, and others are investing in integration solutions to optimize business processes, improve Business Intelligence, and enhance customer experience.

Exclusive Customer Landscape

The enterprise application and integration market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the enterprise application and integration market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, enterprise application and integration market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence In the industry.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Adeptia Inc.

- Atlassian Corp. Plc

- Axway Software SA

- Boomi LP

- Carmatec IT Solutions Pvt. Ltd.

- Fiorano Technologies Inc.

- Fujitsu Ltd.

- Hewlett Packard Enterprise Co.

- Informatica Inc.

- International Business Machines Corp.

- Microsoft Corp.

- Oracle Corp.

- Salesforce Inc.

- SAP SE

- ScienceSoft USA Corp.

- SnapLogic Inc.

- Software AG

- Talend Inc

- TIBCO Software Inc.

- Workato Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a range of technologies and solutions designed to connect and facilitate communication between various applications and systems within an organization. This market is characterized by its continuous evolution, driven by the increasing complexity of IT environments and the need for businesses to adapt to the digital transformation. ERP systems and Business Intelligence (BI) applications are integral components of modern enterprise IT. These systems require seamless integration with other applications and data sources to provide valuable insights and streamline business processes. Middleware infrastructure plays a crucial role in enabling such integration, acting as a bridge between different applications and systems.

Cloud computing has significantly impacted the EAI landscape. With the increasing adoption of cloud-based technologies, there has been a shift towards hybrid integration solutions that can handle both cloud and on-premises applications. Big Data and Internet of Things (IoT) have also added new dimensions to the EAI market, necessitating advanced integration capabilities to handle the volume of data generated by these technologies. OpenSource Software has emerged as a popular choice for many organizations due to its cost-effectiveness and flexibility. Digital transformation initiatives have led to an increased focus on Business Process Optimization and Digital Services. This has resulted in a surge in demand for integration solutions that can support AI-driven integration and real-time data processing.

Data Security concerns have taken center stage In the EAI market, with organizations requiring robust security features to protect sensitive data. Remote work and the increasing use of Banking Systems have further accentuated the need for secure integration solutions. The EAI market caters to various verticals, including Manufacturing, Retail, Healthcare, and Finance. Backbase and Grand Central are some of the notable players In the Integration Platform as a Service (iPaaS) segment. IT Complexity continues to be a challenge for large enterprises, necessitating the adoption of advanced integration solutions. The market for EAI solutions is dynamic and constantly evolving.

Mergers and acquisitions have played a significant role in shaping the market landscape. For instance, TIBCO Software's acquisition of Salsify and AnyPoint Exchange's acquisition by MuleSoft have expanded their product offerings and strengthened their positions In the market. The EAI market is expected to grow significantly In the coming years, driven by the increasing volume of data and the need for businesses to streamline their IT environments. The market is expected to witness robust growth In the cloud segment, as more organizations adopt cloud-based technologies for their integration needs. In conclusion, the market is a critical component of modern enterprise IT. It enables organizations to connect and integrate various applications and systems, enabling seamless data flow and business process optimization. The market is driven by the need for digital transformation, the increasing volume of data, and the adoption of cloud-based technologies. Organizations must carefully evaluate their integration needs and choose solutions that can meet their specific requirements while ensuring data security and compliance.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

186 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 17.09% |

|

Market growth 2024-2028 |

USD 26.94 billion |

|

Market structure |

Fragmented |

|

YoY growth 2023-2024(%) |

14.2 |

|

Key countries |

US, Germany, Canada, China, and Japan |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Enterprise Application And Integration Market Research and Growth Report?

- CAGR of the Enterprise Application And Integration industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across North America, Europe, APAC, South America, and Middle East and Africa

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the enterprise application and integration market growth of industry companies

We can help! Our analysts can customize this enterprise application and integration market research report to meet your requirements.

RIA -

RIA -