Environmental Catalyst Market Size 2025-2029

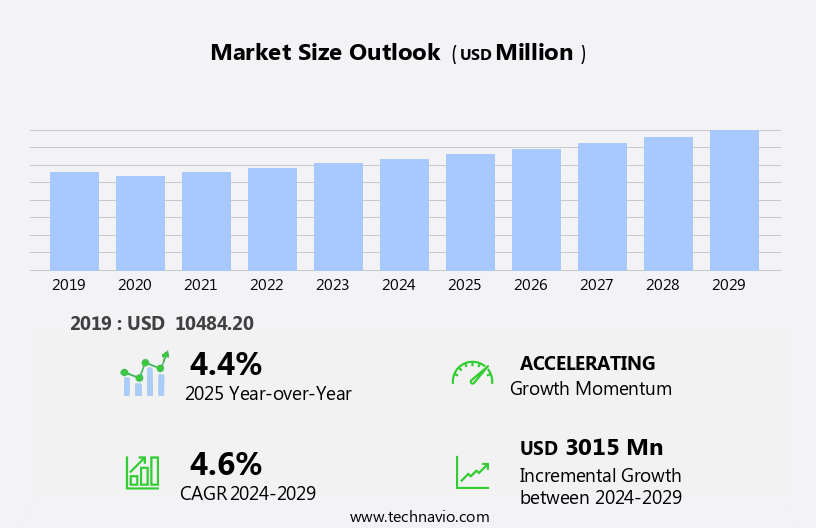

The environmental catalyst market size is forecast to increase by USD 3.02 billion at a CAGR of 4.6% between 2024 and 2029.

- The market is experiencing significant growth driven by stringent environmental regulations aimed at reducing emissions and improving air quality. These regulations, particularly in the transportation and energy sectors, are increasing the demand for environmental catalysts. Furthermore, the adoption of these catalysts in renewable energy applications, such as fuel cells and solar photovoltaics, is expanding the market's reach. However, the market's growth is not without challenges. The volatility in raw materials prices, such as palladium and platinum, used in the production of environmental catalysts poses a significant risk to market stability. Companies seeking to capitalize on this market opportunity must closely monitor raw material prices and explore alternative catalyst technologies or sourcing strategies.

- Additionally, investing in research and development to improve catalyst efficiency and reduce production costs can help companies stay competitive in this dynamic market. Overall, the market presents a compelling growth opportunity for companies committed to sustainable technologies and innovative solutions.

What will be the Size of the Environmental Catalyst Market during the forecast period?

- The market encompasses a range of technologies and applications aimed at reducing emissions and mitigating climate change. Key market drivers include the growing demand for green chemistry in various industries, the shift towards alternative fuels, and the increasing focus on emission reduction and air pollution control. Catalytic converter technology, diesel oxidation catalysts, catalytic combustion, and catalytic oxidation are among the key catalyst technologies driving this market. The market is also influenced by the circular economy and the increasing importance of municipal waste management, emission monitoring, and the reduction of fixed source pollutants. The adoption of clean technology, such as hydrogen fuel cells and renewable energy sources, is also contributing to the growth of the market.

- Moreover, the market is being shaped by the global push for climate change mitigation, energy efficiency, and the widespread adoption of zero-emission vehicles. Industrial emissions, particularly from gas engines and industrial processes, are a significant focus area for emission reduction and pollution control initiatives. Environmental sustainability, sustainable manufacturing, and environmental engineering are also key areas of application for environmental catalysts. The market is further influenced by stringent environmental regulations and the growing importance of clean air initiatives. Overall, the market is expected to continue growing as the world transitions towards a more sustainable and low-carbon economy.

How is this Environmental Catalyst Industry segmented?

The environmental catalyst industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

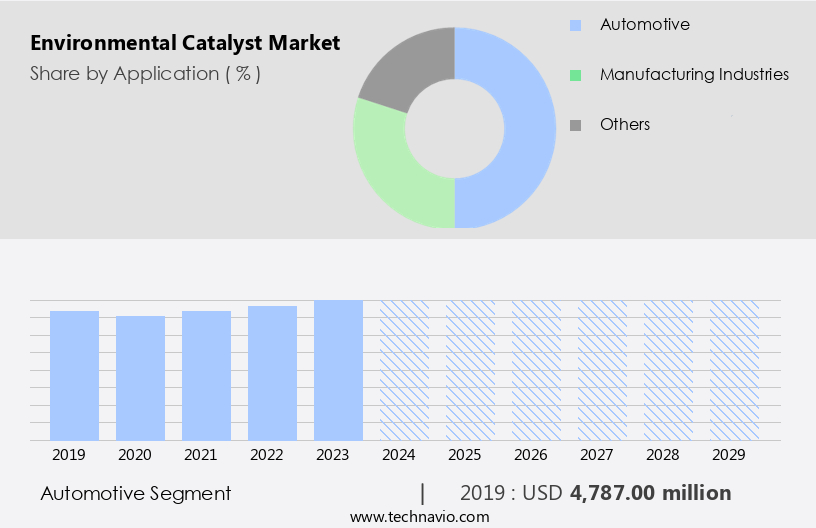

- Application

- Automotive

- Manufacturing industries

- Others

- Type

- CO oxidation catalysts

- Selective catalytic reduction catalysts (SCRC)

- VOC oxidation catalysts

- Others

- Product Type

- Precious metals

- Mixed metal oxides

- Base metals

- Geography

- APAC

- China

- India

- Japan

- South Korea

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- UK

- South America

- Middle East and Africa

- APAC

By Application Insights

The automotive segment is estimated to witness significant growth during the forecast period.

The automotive industry is a significant application sector for environmental catalysts, playing a vital role in reducing vehicular emissions and improving air quality. Catalytic converters, a key automotive component, utilize environmental catalysts to convert harmful pollutants into less harmful substances. As governments intensify efforts to address air pollution, the automotive sector faces increasing pressure to integrate efficient catalytic solutions. Regulatory bodies, such as the Euro 6 standards in Europe and CAFE standards in the US, mandate the use of advanced catalytic converters in vehicles. The continuous evolution of these standards necessitates ongoing innovation in environmental catalysts to meet or exceed regulatory requirements.

This includes the development of selective catalytic reduction systems for diesel engines, gasoline particulate filters, and diesel particulate filters for reducing nitrous oxide emissions, volatile organic compounds, and carbon monoxide. Additionally, emission control technologies, such as nanoparticle technology and filter management devices, are gaining popularity for their effectiveness in reducing harmful emissions from both mobile and stationary sources. The focus on environmental compliance and consumer preferences for cleaner air is driving the demand for advanced emission control systems in various industries, including power generation and cement production.

Get a glance at the market report of share of various segments Request Free Sample

The Automotive segment was valued at USD 4.79 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

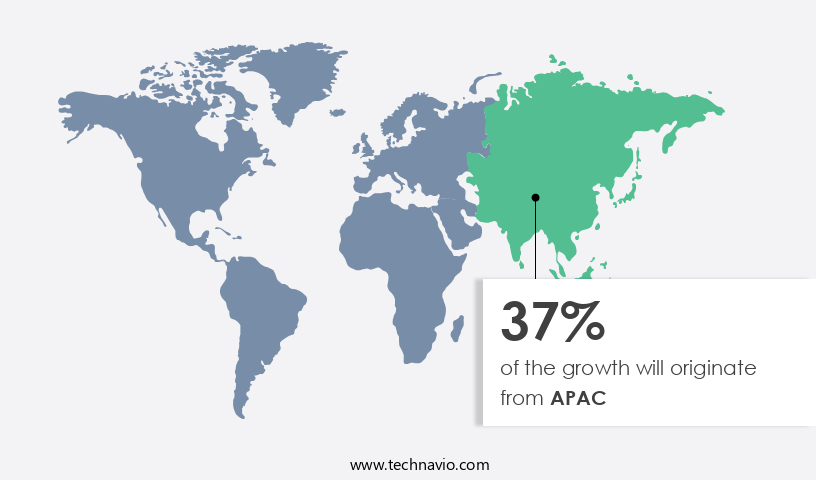

APAC is estimated to contribute 37% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

For more insights on the market size of various regions, Request Free Sample

The market in the Asia Pacific (APAC) region is experiencing notable growth due to industrial expansion, economic growth, and stricter environmental regulations. With APAC being the world's manufacturing hub, countries like China and India contribute significantly to industrial output, leading to a high demand for environmental catalysts. Industries in the region, including automotive, power generation, and manufacturing, are under pressure to comply with stringent emission standards. In China, rapid industrialization and increasing concerns about air quality have led to the implementation of rigorous environmental regulations. These regulations are driving the adoption of environmental catalysts to reduce harmful emissions from industries and mobile sources.

The automotive sector, in particular, is undergoing a transition towards emission control technologies such as selective catalytic reduction, diesel particulate filters, and gasoline particulate filters. Environmental catalysts play a crucial role in reducing emissions of nitrous oxides, volatile organic compounds, carbon monoxide, and other harmful pollutants from industrial processes and mobile sources. Catalytic converters, made from catalyst materials like metal oxides, are essential components of emission control systems in diesel and gasoline engines. The adoption of hybrid vehicles and electric vehicles is also expected to increase the demand for environmental catalysts in the automotive sector. Government bodies and regulatory agencies are playing a significant role in enforcing emission standards for both mobile and stationary sources.

For instance, the US Environmental Protection Agency (EPA) sets air quality standards for mobile sources, while the US Occupational Safety and Health Administration (OSHA) regulates industrial emissions. Compliance with these regulations is essential for businesses to avoid penalties and maintain a good reputation. In , the market in the APAC region is poised for growth due to increasing industrialization, economic expansion, and stricter environmental regulations. The adoption of emission control technologies and the transition towards cleaner energy sources are expected to further fuel market growth. Companies in the environmental catalyst industry are well-positioned to capitalize on these trends and contribute to the reduction of harmful emissions and improvement of air quality.

Market Dynamics

Our researchers analyzed the data with 2024 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in the adoption of Environmental Catalyst Industry?

- Stringent environmental regulations related to emission standards is the key driver of the market.

- The market is significantly influenced by stringent regulations aimed at reducing industrial pollution. Governments worldwide are enforcing rules to limit emissions, particularly in the automotive sector. For instance, Euro 6 in Europe and CAFE standards in the US set strict pollutant limits, necessitating the use of advanced catalytic converters by automobile manufacturers. These regulations serve as catalysts, driving industries to invest in emission control solutions and increasing the demand for environmental catalysts.

- The need for sustainable industrial processes and the growing awareness of environmental issues further boost market growth. Companies are focusing on research and development to introduce innovative technologies that meet regulatory requirements while minimizing environmental impact.

What are the market trends shaping the Environmental Catalyst Industry?

- Increasing adoption of environmental catalysts in renewable energy applications is the upcoming market trend.

- Environmental catalysts are pivotal in driving the advancement of renewable energy technologies, facilitating the shift towards cleaner energy sources. One significant application of environmental catalysts is in the production of hydrogen via water electrolysis. These catalysts, typically made from precious metals like platinum or alternative non-precious metals such as nickel and iron, boost the efficiency of the process by enhancing the splitting of water into hydrogen and oxygen.

- In the realm of fuel cells, environmental catalysts assume growing importance. They are indispensable in fuel cells, enabling the electrochemical reaction between hydrogen and oxygen, resulting in electricity generation and water as byproducts.

What challenges does the Environmental Catalyst Industry face during its growth?

- Volatility in raw materials prices used in environmental catalysts is a key challenge affecting the industry growth.

- The market encounters a notable challenge due to the reliance on scarce and costly materials, particularly platinum. This precious metal, known for its exceptional catalytic properties, is essential for various catalytic applications, such as automotive catalytic converters and fuel cells. Platinum's scarcity and high market value significantly impact the cost of catalyst production. Recent market forecasts indicate that the price of platinum is projected to reach USD1,100 by mid-2024, with further increases anticipated, reaching USD1,500 by the end of 2025.

- This trend poses a significant challenge for market growth and underscores the need for alternative catalyst solutions or more efficient use of platinum resources.

Exclusive Customer Landscape

The environmental catalyst market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the environmental catalyst market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, environmental catalyst market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Albemarle Corp. - The company's innovative catalyst solutions, including AlkyStar, enable the production of premium alkylates for clean fuels without relying on liquid acid catalysts in the manufacturing process. This approach enhances search engine visibility, ensuring a clear and informative message for research analysts. By utilizing advanced catalyst technology, the company delivers high-quality alkylates as a blending component, maintaining alignment with our commitment to environmental sustainability and product excellence.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Albemarle Corp.

- Axens Group

- Babcock Power Inc.

- BASF SE

- Catalytic Combustion Corp.

- China Petrochemical Corp.

- China Petrochemical Corp.

- Clariant International Ltd.

- CORMETECH Inc.

- Evonik Industries AG

- Exxon Mobil Corp.

- Heraeus Holding GmbH

- Honeywell International Inc.

- Johnson Matthey Plc

- OMV Aktiengesellschaft

- Topsoes AS

- Treibacher Industrie AG

- Umicore SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

The market encompasses a broad range of applications aimed at reducing harmful emissions from various industrial processes and mobile sources. These catalysts play a crucial role in mitigating the environmental impact of industries such as chemical production, cement manufacturing, and power generation. Chemical processes, including the production of nitrous oxides in calcination plants and the separation of light fractions in FCC units, generate significant volumes of pollutants. Catalytic technologies are employed to minimize these emissions, ensuring regulatory compliance and contributing to improved air quality. Industrial waste streams, particularly those containing volatile organic compounds (VOCs), can also be addressed through the use of catalytic conversion systems.

These technologies convert VOCs into less harmful by-products, contributing to overall emission reduction and improved environmental performance. In the automotive sector, the focus on emission control has intensified in recent years, driven by increasingly stringent air quality standards. Selective catalytic reduction (SCR) systems and catalytic converters, including diesel particulate filters and gasoline particulate filters, are widely used to reduce carbon monoxide, nitrogen oxides, and particulate matter emissions from diesel and gasoline engines. Hybrid vehicles, which combine an internal combustion engine with an electric motor, offer another avenue for emission reduction. Catalytic converters play a critical role in managing the exhaust gases from the internal combustion engine, ensuring that emissions meet stringent automotive standards.

Regulatory bodies continue to play a significant role in driving the adoption of emission control technologies. In the power generation sector, the shift towards renewable electricity sources is reducing the reliance on fossil fuels and, in turn, decreasing associated emissions. However, the continued operation of stationary diesel engines necessitates the use of advanced emission control systems to minimize their impact on air quality. The development of nanoparticle technology has opened up new opportunities for emission control, particularly in the area of catalytic converters. These advanced materials offer enhanced catalytic activity and durability, contributing to more effective emission reduction and longer filter life.

Environmental concerns related to industrial processes and mobile sources continue to grow, with consumers increasingly demanding action to address these issues. Emission control technologies, including catalytic converters and filter management devices, are essential tools in the fight against air pollution and the drive towards sustainable production and transportation. In summary, the market is a dynamic and evolving landscape, driven by the need to address environmental issues associated with industrial processes and mobile sources. Catalytic technologies, including selective catalytic reduction, catalytic converters, and filter management devices, play a crucial role in minimizing harmful emissions and ensuring regulatory compliance.

The ongoing development of advanced materials and technologies will continue to drive innovation and improve the overall environmental performance of various industries.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

231 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 4.6% |

|

Market growth 2025-2029 |

USD 3015 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

4.4 |

|

Key countries |

US, China, India, Japan, Canada, UK, South Korea, Germany, France, and Italy |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Environmental Catalyst Market Research and Growth Report?

- CAGR of the Environmental Catalyst industry during the forecast period

- Detailed information on factors that will drive the growth and forecasting between 2025 and 2029

- Precise estimation of the size of the market and its contribution of the industry in focus to the parent market

- Accurate predictions about upcoming growth and trends and changes in consumer behaviour

- Growth of the market across APAC, North America, Europe, South America, and Middle East and Africa

- Thorough analysis of the market’s competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the environmental catalyst market growth of industry companies

We can help! Our analysts can customize this environmental catalyst market research report to meet your requirements.

RIA -

RIA -