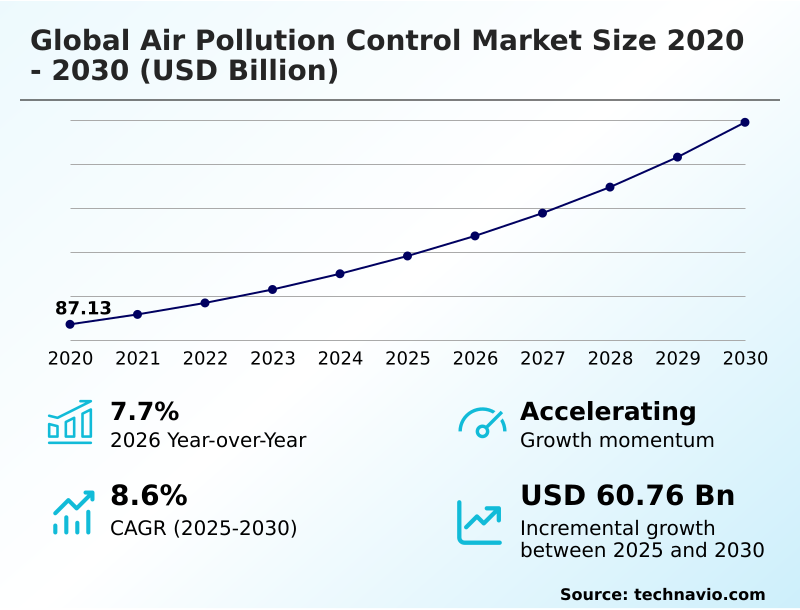

Air Pollution Control Market Size 2026-2030

The air pollution control market size is valued to increase by USD 60.76 billion, at a CAGR of 8.6% from 2025 to 2030. Stringent regulatory frameworks and compliance mandates will drive the air pollution control market.

Major Market Trends & Insights

- APAC dominated the market and accounted for a 39.5% growth during the forecast period.

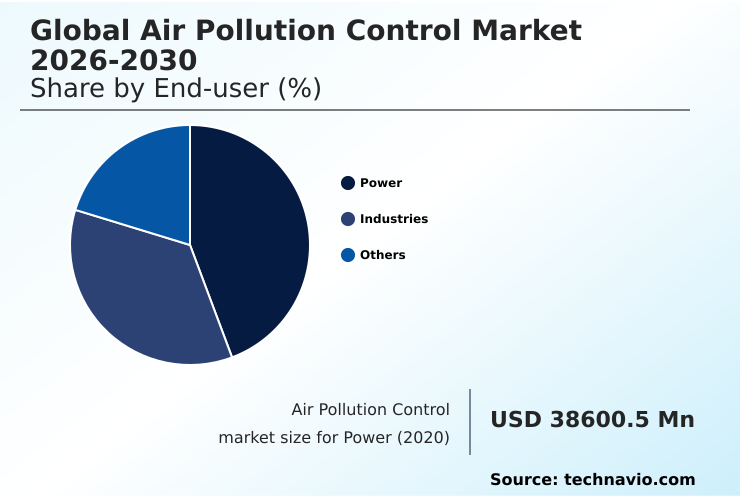

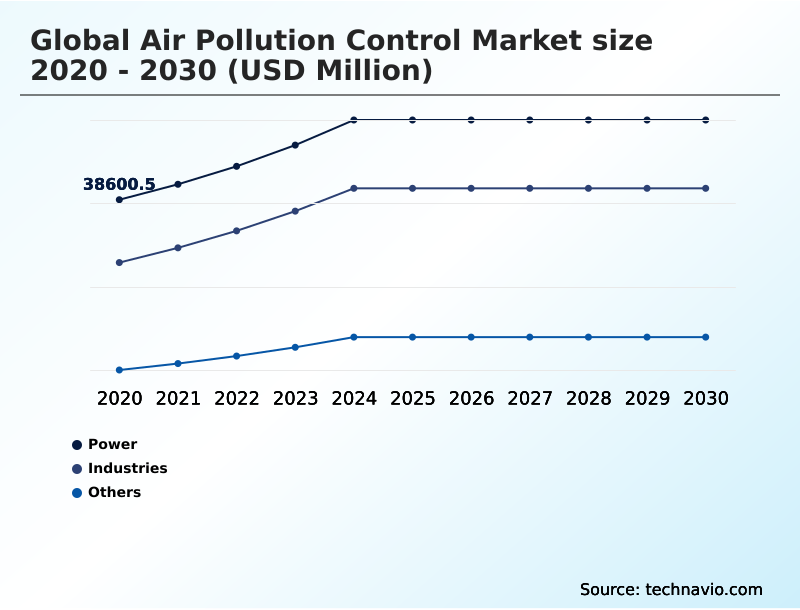

- By End-user - Power segment was valued at USD 48.40 billion in 2024

- By Product - Scrubbers segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 91.82 billion

- Market Future Opportunities: USD 60.76 billion

- CAGR from 2025 to 2030 : 8.6%

Market Summary

- The air pollution control market encompasses the technologies and methods used to reduce harmful pollutants from industrial, commercial, and transportation sources. Growth is primarily driven by stringent environmental legislation and an increasing focus on public health, which compel industries to adopt advanced systems for particulate matter filtration and hazardous air pollutants control.

- A significant trend is the integration of pollution abatement with decarbonization strategies, including carbon capture utilization and storage, moving the market beyond mere compliance. However, high capital and operational costs remain a substantial challenge.

- For instance, a manager of a heavy industrial facility must balance the significant upfront investment for a wet scrubbers or selective catalytic reduction retrofit against the long-term operational savings and the necessity of meeting new, non-negotiable emission ceilings.

- This scenario highlights the central tension between financial constraints and the escalating demand for cleaner industrial processes and advanced technologies like direct air capture technology.

What will be the Size of the Air Pollution Control Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Air Pollution Control Market Segmented?

The air pollution control industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Power

- Industries

- Others

- Product

- Scrubbers

- Catalyst converters

- Others

- Technology

- Flue gas desulfurization

- Baghouse systems

- Selective catalytic reduction

- Geography

- APAC

- China

- India

- Japan

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Middle East and Africa

- Saudi Arabia

- UAE

- South Africa

- South America

- Brazil

- Argentina

- Rest of World (ROW)

- APAC

By End-user Insights

The power segment is estimated to witness significant growth during the forecast period.

The power segment is undergoing a significant transformation, driven by the imperative to transition toward low-carbon energy systems. This shift compels utility providers to adopt advanced abatement technologies beyond basic filtration, integrating sophisticated carbon capture utilization and storage infrastructure.

The focus is now on projects like bioenergy with carbon capture, which require complex flue gas conditioning and amine-based gas treatment to produce net-zero industrial commodities.

As a result, modern systems are evaluated on their ability to meet ultra-low emission standards, with flue gas desulfurization technologies now routinely exceeding 98% capture efficiency.

This operational sustainability metrics-driven approach redefines pollution control as a core component of asset viability in a decarbonizing economy, moving beyond simple stationary source emission control to a more holistic strategy encompassing gas phase filtration and catalytic filter bags.

The Power segment was valued at USD 48.40 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

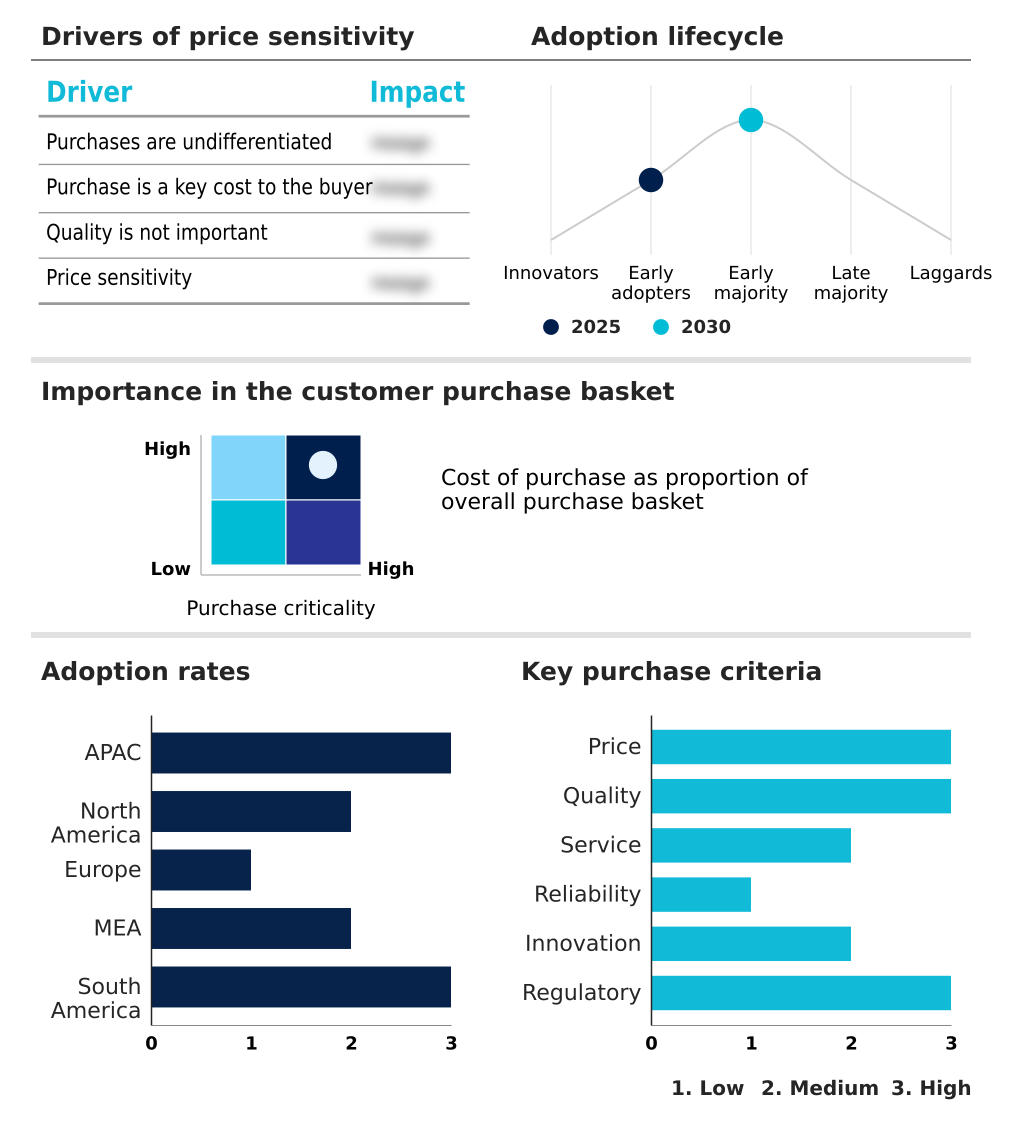

APAC is estimated to contribute 39.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Air Pollution Control Market Demand is Rising in APAC Get Free Sample

The market's geographic landscape is characterized by distinct regional priorities.

APAC, accounting for nearly 39.53% of the incremental growth, is driven by rapid industrialization and governmental mandates to improve air quality, leading to large-scale deployment of baghouse systems and wet electrostatic precipitator technology.

This is exemplified by projects demonstrating 20% ammonia substitution in thermal power plants.

In contrast, North America and Europe focus on advanced technologies, including bio-cogeneration plant emissions reduction and direct air capture technology, spurred by mature regulatory frameworks and decarbonization incentives.

This regional divergence creates a multifaceted market where demand is shaped by both immediate public health needs and long-term climate objectives that require continuous compliance monitoring, fugitive dust suppression, and high-efficiency particulate air filtration technologies such as v-bank air filter design.

Market Dynamics

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the air pollution control market requires a detailed evaluation of various technological pathways and their operational impacts. A scrubbers vs electrostatic precipitators comparison is fundamental for industries dealing with specific particulate characteristics, while a deeper analysis of the cost of carbon capture in cement production is critical for long-term decarbonization strategies.

- For mobile sources, understanding the euro 7 emission standards impact on catalysts is vital, just as managing sox and nox in marine engines is key to assessing the efficiency of marine scrubbers for imo compliance. Stationary sources present different challenges, such as retrofitting coal power plants with fgd systems or optimizing scr systems for low-load conditions.

- Specialized applications are also expanding, from voc recovery in petrochemical refining and fine dust control in open-pit mining operations to implementing advanced hvac filtration for hospital indoor air quality. The benefits of pulse-jet fabric filters in providing high-efficiency particulate removal are well-documented.

- Technologies like catalytic oxidation for voc destruction and advanced baghouse filter media for heavy industry offer superior performance over legacy systems, often improving pollutant removal efficiency by over 15%, which directly enhances compliance with evolving industrial flue gas treatment solutions.

- This focus extends to niche areas like direct reduction iron plant emission control, air pollution control for waste-to-energy plants, reducing particulate matter from diesel engines, ammonia co-firing in thermal power stations, nitrogen oxide control for gas turbine exhausts, and innovative carbon capture pre-treatment system design.

What are the key market drivers leading to the rise in the adoption of Air Pollution Control Industry?

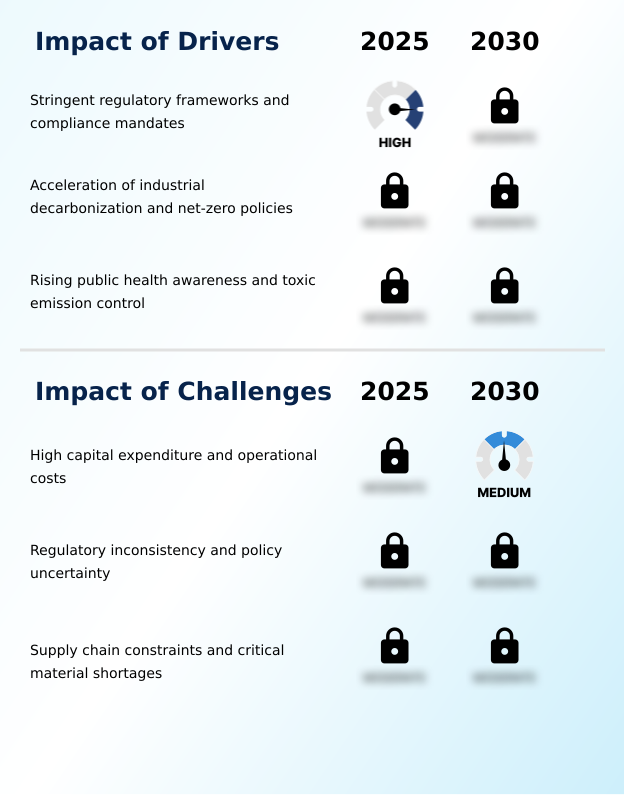

- Stringent regulatory frameworks and compliance mandates are a key driver of the market.

- The market is primarily propelled by the intensifying rigor of environmental legislation, compelling heavy industries to adopt best available techniques for emission abatement.

- In certain industrializing economies, this has led to new rules mandating that key sectors slash particulate matter and sulfur dioxide emissions by approximately 50% and 40%, respectively.

- A second transformative driver is the global imperative to decarbonize hard-to-abate sectors, integrating traditional air quality management with carbon capture. This trend is bolstered by new legal frameworks unlocking significant investment for industrial decarbonization pathways.

- A third critical driver is the heightened focus on public health, which is expanding the market for advanced filtration and catalytic oxidation technologies.

- This is evidenced by government bodies awarding multi-year contracts, such as one for five years, to support the revision of standards for toxic air emissions, driving downstream adoption of state-of-the-art pollution control technologies and promoting fence-line community protection.

What are the market trends shaping the Air Pollution Control Industry?

- Strategic rebranding and the integration of decarbonization portfolios represent a key upcoming market trend. This shift highlights a move towards comprehensive climate protection strategies.

- A dominant trend is the strategic pivot of industrial firms toward holistic decarbonization identities, merging traditional particulate matter filtration with next-generation energy solutions. This deep operational realignment is complemented by a decisive move away from transactional sales toward data-driven lifecycle service agreements, where predictive maintenance algorithms enhance reliability and guarantee continuous compliance.

- This is demonstrated by service agreements that can span over six years, ensuring long-term operational assurance. Furthermore, a technological surge in developing advanced low-resistance filtration systems and ceramic filter elements addresses the dual pressures of improving indoor air quality management and reducing building carbon footprints.

- Innovations in this area can offer a significantly lower pressure drop compared to legacy filters, directly supporting both sustainability goals and occupant health through best available control technology and effective gas stream impurity management.

What challenges does the Air Pollution Control Industry face during its growth?

- High capital expenditure and operational costs represent a key challenge affecting industry growth.

- A primary market challenge is the substantial capital requirement for advanced technologies, coupled with high operational costs that represent a non-revenue-generating expense for many industries. This financial friction is intensified by regulatory fragmentation and unpredictability across jurisdictions, which complicates equipment standardization and long-term strategic planning.

- Furthermore, the market is increasingly threatened by global supply chain rigidities, particularly concerning the availability of critical raw materials. For instance, the market for platinum and palladium, essential for catalytic converters, has faced a structural supply deficit for three consecutive years.

- This platinum group metals dependency creates bottlenecks and rising input costs, challenging the deployment of essential environmental infrastructure, including systems for stationary source emission control, and complicates efforts to establish a circular economy of catalyst materials under existing ambient air quality standards.

Exclusive Technavio Analysis on Customer Landscape

The air pollution control market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the air pollution control market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Air Pollution Control Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, air pollution control market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Ahlstrom Oyj - Delivers a portfolio of air pollution control technologies, including electrostatic precipitators, fabric filters, and wet scrubbers, targeting large-scale industrial applications.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Ahlstrom Oyj

- Airex Industries Inc.

- American Air Filter Co. Inc.

- Andritz AG

- Babcock and Wilcox

- Camfil AB

- Donaldson Co. Inc.

- Doosan Lentjes GmbH

- DuPont de Nemours Inc.

- Elessent Clean Technologies Inc

- Freudenberg and Co. KG

- GEA Group AG

- General Electric Co.

- John Wood Group PLC

- Mitsubishi Heavy Ltd.

- MITTAL BLOWERS INDIA PVT. LTD.

- Parker Hannifin Corp.

- Sumitomo Corp.

- Thermax Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Air pollution control market

- In January 2025, United Catalyst Corp. released a strategic assessment detailing the changing deficits of palladium and rhodium, signaling that the future profitability of the catalytic converter segment will rely heavily on efficient secondary supply chains.

- In February 2025, Andritz AG completed its acquisition of the LDX Group, a strategic move designed to bolster its environmental solutions portfolio and expand its service offerings for industrial emission reduction in the North American market.

- In April 2025, the US Environmental Protection Agency awarded a five-year contract to Eastern Research Group to support the development and revision of standards for toxic air emissions, with a primary goal of reducing health risks from hazardous air pollutants.

- In May 2025, the World Platinum Investment Council published a quarterly report warning of a deepening structural deficit in the global supply of platinum and palladium, projecting that industrial demand would outstrip mining output for the third consecutive year.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Air Pollution Control Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 296 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 8.6% |

| Market growth 2026-2030 | USD 60756.4 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 7.7% |

| Key countries | China, India, Japan, South Korea, Australia, Indonesia, US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, Saudi Arabia, UAE, Egypt, South Africa, Turkey, Brazil, Argentina and Chile |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The air pollution control market is evolving from a focus on standalone compliance hardware to integrated, performance-driven solutions. Leading firms are restructuring their value propositions to address both traditional pollutants and carbon intensity, reflecting a strategic pivot toward holistic industrial decarbonization.

- This boardroom-level shift prioritizes lifecycle service agreements and advanced technologies like carbon capture utilization and storage, moving beyond transactional equipment sales. The market is propelled by stringent enforcement, such as new standards in some regions mandating that specific industries slash particulate matter and sulfur dioxide emissions by up to 50% and 40%, respectively.

- This regulatory pressure, coupled with the need for technologies such as volatile organic compound abatement, hazardous air pollutants control, and nitrogen oxide reduction, reinforces the demand for advanced systems.

- Innovations in thermal oxidizer systems, exhaust gas cleaning systems, and multi-pollutant control systems are becoming critical as industries navigate the complex landscape of environmental compliance and long-term sustainability goals, utilizing solutions like flue gas recirculation and ammonia-free scr systems.

What are the Key Data Covered in this Air Pollution Control Market Research and Growth Report?

-

What is the expected growth of the Air Pollution Control Market between 2026 and 2030?

-

USD 60.76 billion, at a CAGR of 8.6%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Power, Industries, and Others), Product (Scrubbers, Catalyst converters, and Others), Technology (Flue gas desulfurization, Baghouse systems, and Selective catalytic reduction) and Geography (APAC, North America, Europe, Middle East and Africa, South America)

-

-

Which regions are analyzed in the report?

-

APAC, North America, Europe, Middle East and Africa and South America

-

-

What are the key growth drivers and market challenges?

-

Stringent regulatory frameworks and compliance mandates, High capital expenditure and operational costs

-

-

Who are the major players in the Air Pollution Control Market?

-

Ahlstrom Oyj, Airex Industries Inc., American Air Filter Co. Inc., Andritz AG, Babcock and Wilcox, Camfil AB, Donaldson Co. Inc., Doosan Lentjes GmbH, DuPont de Nemours Inc., Elessent Clean Technologies Inc, Freudenberg and Co. KG, GEA Group AG, General Electric Co., John Wood Group PLC, Mitsubishi Heavy Ltd., MITTAL BLOWERS INDIA PVT. LTD., Parker Hannifin Corp., Sumitomo Corp. and Thermax Ltd.

-

Market Research Insights

- Market dynamics are defined by a dual focus on regulatory compliance and the strategic pursuit of industrial decarbonization pathways. The implementation of ultra-low emission standards is a primary catalyst, with some jurisdictions mandating emission reductions of up to 50% for specific pollutants like sulfur dioxide, forcing investment in best available techniques.

- Concurrently, the push for net-zero industrial commodities is driving the adoption of advanced systems, demonstrated by facilities now capturing roughly 50% of total plant emissions through integrated carbon capture.

- This convergence of regulatory pressure and sustainability goals is compelling operators of combined-cycle gas turbines and other industrial plants to prioritize technologies that offer both environmental compliance and a competitive edge in a low-carbon economy.

We can help! Our analysts can customize this air pollution control market research report to meet your requirements.

RIA -

RIA -