Europe Carbon Steel Tubes Market Size 2024-2028

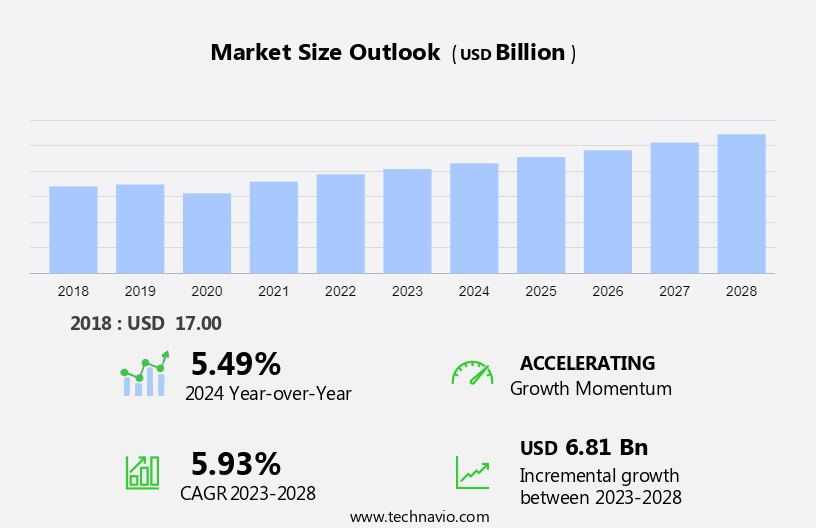

The Europe carbon steel tubes market size is forecast to increase by USD 6.81 billion at a CAGR of 5.93% between 2023 and 2028.

- Carbon steel tubes have gained significant traction in Europe due to the increasing demand from various end-user industries, including oil and gas, power generation, and infrastructure. The construction sector's growth, driven by the increasing installation capacities of power plants, is a significant market growth factor. Additionally, the high energy prices in Europe have led to the preference for it due to their cost-effectiveness and durability. These factors are expected to drive the market over the forecast period. Furthermore, the market is also witnessing trends such as the increasing adoption of carbon steel tubes in renewable energy applications, particularly in wind energy, and the development of advanced carbon steel tubes with improved mechanical properties. However, challenges such as the volatility of raw material prices and the intense competition from alternative materials may hinder market growth. Overall, the market is poised for steady growth, driven by the increasing demand from end-user industries and the adoption of advanced technologies.

What will be the size of the Market during the forecast period?

- The market experiences strong demand due to its extensive applications in various sectors. Primary end-use industries include oil and gas, propane and other gases, and the petrochemicals industry. These are integral to the transportation of these commodities, ensuring safety and efficiency.

- Additionally, the market finds significant traction in renewable energy applications, such as wind turbines and batteries. Furthermore, these are extensively used in industries like medical devices, plastics, detergents, and automotive applications, including tyres, automotive engines, and components like diesel spark plugs and engine block heating. The market's growth is influenced by industrialization and infrastructure development, with applications in shopping centers, airports, commercial passenger vehicles, water infrastructure, nuclear power sector, and chemicals & petrochemicals sector. Environmental conditions necessitate the use of anti-corrosion coatings, further bolstering market demand.

How is this market segmented and which is the largest segment?

The market research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD billion" for the period 2024-2028, as well as historical data from 2018-2022 for the following segments.

- Product

- Welded tubes

- Seamless tubes

- Application

- Construction

- Oil and gas

- Automotive and transportation

- Mechanical engineering

- Others

- Geography

- Europe

- Germany

- UK

- France

- Italy

- Europe

By Product Insights

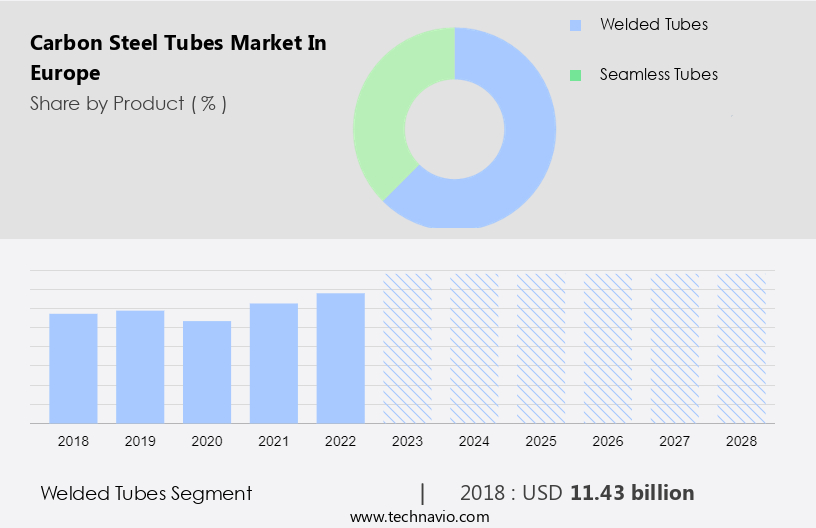

- The welded tubes segment is estimated to witness significant growth during the forecast period.

Carbon steel tubes are extensively used in Europe due to their versatility and wide availability in various shapes, sizes, and thicknesses. These tubes are primarily employed in construction applications, including building frameworks, bridge construction, and industrial structure fabrication, owing to their strongness and reliability. Leading carbon steel tube manufacturers in Europe, such as ArcelorMittal, Tata Steel Europe, and Mannesmann, cater to this demand by providing advanced high-strength steel carbon tubes with superior strength-to-weight ratios. The market also serves sectors like oil & gas, petrochemicals, wind turbines, batteries, medical devices, plastics, detergents, tires, automotive applications, diesel spark plugs, engine block heating, diesel particulate filters, and power plants.

Get a glance at the market share of various segments Request Free Sample

The welded tubes segment was valued at USD 11.43 billion in 2018 and showed a gradual increase during the forecast period.

Market Dynamics

Our researchers analyzed the data with 2023 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

What are the key market drivers leading to the rise in adoption of Europe Carbon Steel Tubes Market?

Increasing demand for carbon steel tubes from end-user industries is the key driver of the market.

- Carbon steel tubes play a pivotal role in various European industries, including infrastructure development, oil and gas, petrochemicals, and automotive. The primary revenue generators for the market are process industries, which utilize these for enhanced operational efficiency. These tubes are essential for transporting final outputs, making market expansion a natural consequence of industry growth. Europe's infrastructure sector is undergoing significant expansion, driving the demand. Airports, railway stations, and metro systems are among the infrastructure projects that use these tubes extensively. Additionally, industries such as oil and gas, petrochemicals, and chemicals continue to grow, increasing the demand in high-pressure and corrosive environments.

- In addition, these are also crucial in the automotive sector, where they are used for applications such as engine block heating, diesel particulate filters, and diesel spark plugs. In the power sector, these are used in power plants and mechanical engineering applications. The market's technological advancements include seamless tubes and ERW pipes, catering to diverse industries and applications. Urban infrastructure development, including piped gas distribution and fire safety segments, is another significant market. The construction industry's increasing expenditures, sales of homes, and population growth further boost demand. In the chemical and petrochemical sector, these are used in various applications due to their resistance to mechanical stress and environmental conditions.

What are the market trends shaping the Europe Carbon Steel Tubes Market?

Increasing installation capacities of power plants is the upcoming trend in the market.

- The market is experiencing growth due to the increasing installation capacity of power plants. This expansion is driven by the use of it in various applications, such as the construction and engineering process of wind power energy towers and solar energy generation plants. The European Union's commitment to reducing carbon emissions and the resulting regulations create a favorable environment for power plant development. In addition to power generation, these are also utilized in numerous industries, including automotive & transportation, mechanical engineering, petrochemicals, and construction. These tubes offer benefits such as high strength, durability, and resistance to mechanical stress and corrosive atmospheres.

- Furthermore, applications in sectors like oil & gas industry, piped gas distribution, and fire safety segments are also significant. Market expansion is further fueled by advancements in technology, population growth, and sales of homes and construction expenditures. These are used in various forms, including seamless tubes, ERW pipes, and alloy, black, carbon, mild, stainless, and iron steels. Applications in sectors like automotive applications, diesel spark plugs, engine block heating, diesel particulate filters, and industrialization are also substantial. The transportation sector's demand for carbon steel tubes is increasing due to their use in pipelines for transporting high-pressure gases like propane and butane, as well as in the production of plastics, detergents, tyres, and other products.

What challenges does Europe Carbon Steel Tubes Market face during the growth?

High energy prices in region is a key challenge affecting the market growth.

- Europe's economic instability, driven by rising inflation, the Russia-Ukraine conflict, and increasing migration, is causing significant challenges for energy and cost-of-living crises. Fossil fuels, which accounted for 76% of Europe's energy in 2021, with gas and oil contributing 34% and 31% respectively, have become increasingly scarce or inconsistently supplied. This gas shortage and fluctuating energy prices significantly impact industries, particularly those in manufacturing powerhouses like Germany. The energy crisis is leading to increased costs for maintenance and transportation, as well as potential production delays. These are essential components in various industries, including oil and gas, petrochemicals, wind turbines, batteries, medical devices, plastics, detergents, tyres, automotive applications, and mechanical engineering.

- Furthermore, these industries face increased costs due to the energy crisis, which may affect their profitability and market expansion. In the oil and gas industry, carbon steel tubes are used extensively for high-pressure applications in corrosive atmospheres and under mechanical stress. In the petrochemicals industry, they are used in the production and transportation of chemicals. In wind turbines and batteries, carbon steel tubes are used for structural support and containment. In automotive applications, they are used for engine block heating, diesel particulate filters, and diesel spark plugs. The energy crisis also affects urban infrastructure, such as metros, piped gas distribution, and fire safety segments, which rely on carbon steel tubes for their construction.

Exclusive Europe Carbon Steel Tubes Market Customer Landscape

The market forecasting report includes the adoption lifecycle of the market, covering from the innovator's stage to the laggard's stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape

Key Companies & Market Insights

Companies are implementing various strategies, such as strategic alliances, market forecast partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the market.

The market research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Alleima AB

- ArcelorMittal

- Benteler International AG

- Jindal Steel and Power Ltd.

- Marcegaglia Group

- Nippon Steel Corp.

- Salzgitter AG

- Tata Steel

- United States Steel Corp.

- Vallourec SA

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key market players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Research Analyst Overview

Carbon steel tubes have been a vital component in various industries across Europe, playing a significant role in the development of urban infrastructure, mechanical engineering, and the energy sector. The demand for carbon steel tubes is driven by their versatility, durability, and cost-effectiveness in numerous applications. The market is influenced by several factors. The oil and gas industry's expansion, particularly in the exploration and production sectors, is a primary driver. Carbon steel tubes are widely used in the transportation of oil and gas due to their strength and resistance to high-pressure environments and corrosive atmospheres.

Moreover, another significant factor is the increasing industrialization and population growth in Europe. The construction sector's growth, driven by sales of homes and commercial buildings, is a major contributor to the demand for carbon steel tubes. These tubes are used extensively in the construction of metros, piped gas distribution networks, and other infrastructure projects. Moreover, the adoption of carbon steel tubes in various industries, such as automotive and transportation, wind turbines, batteries, medical devices, plastics, detergent manufacturing, and tires, is on the rise. In the automotive sector, carbon steel tubes are used in the production of diesel spark plugs, engine block heating systems, and diesel particulate filters.

Furthermore, the market is also influenced by technological advancements. For instance, the development of seamless tubes has led to increased demand due to their improved mechanical properties and reduced maintenance costs. ERW (Electric Resistance Welded) pipe adoption is also on the rise due to its cost-effectiveness and ease of production. The market for carbon steel tubes in Europe is further influenced by the environmental conditions in which they are used. For instance, in the power plant sector, carbon steel tubes are used to transport gases and fluids in harsh environments, such as those with high temperatures and corrosive atmospheres.

In addition, in the water infrastructure sector, carbon steel tubes are used for their resistance to mechanical stress and their ability to transport water efficiently. The nuclear power sector is another significant consumer of carbon steel tubes due to their high strength and resistance to radiation. The chemicals and petrochemicals sector also uses carbon steel tubes extensively due to their ability to withstand the harsh conditions of chemical processing.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

157 |

|

Base year |

2023 |

|

Historic period |

2018-2022 |

|

Forecast period |

2024-2028 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 5.93% |

|

Market growth 2024-2028 |

USD 6.81 billion |

|

Market structure |

Concentrated |

|

YoY growth 2023-2024(%) |

5.49 |

|

Competitive landscape |

Leading Companies, market report , Market Positioning of Companies, Competitive Strategies, and Industry Risks |

What are the Key Data Covered in this Market Research Report?

- CAGR of the market during the forecast period

- Detailed information on factors that will drive the market growth and forecasting between 2024 and 2028

- Precise estimation of the size of the market and its contribution of the market in focus to the parent market

- Accurate predictions about upcoming market growth and trends and changes in consumer behaviour

- Growth of the market across Europe

- Thorough analysis of the market's competitive landscape and detailed information about companies

- Comprehensive analysis of factors that will challenge the growth of market companies

We can help! Our analysts can customize this market research report to meet your requirements Get in touch

RIA -

RIA -