Fallopian Tube Cancer Therapeutics Market Size 2025-2029

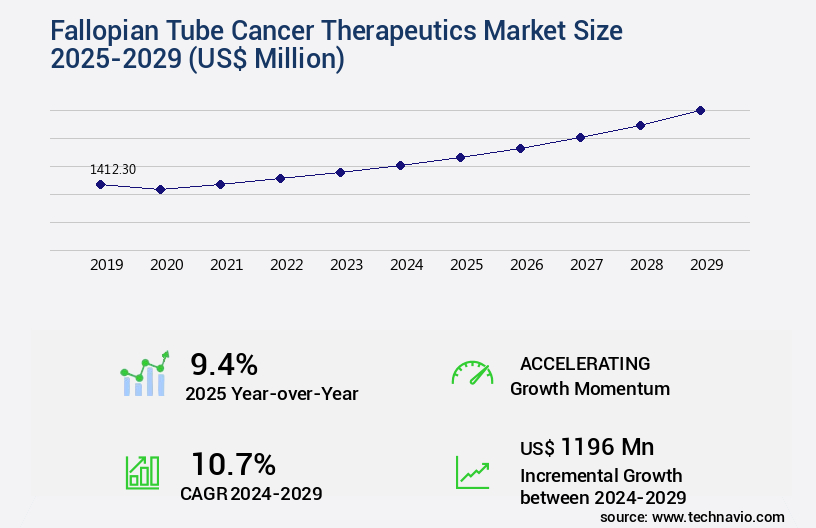

The fallopian tube cancer therapeutics market size is valued to increase by USD 1.2 billion, at a CAGR of 10.7% from 2024 to 2029. Growing attention toward women health will drive the fallopian tube cancer therapeutics market.

Market Insights

- Asia dominated the market and accounted for a 33% growth during the 2025-2029.

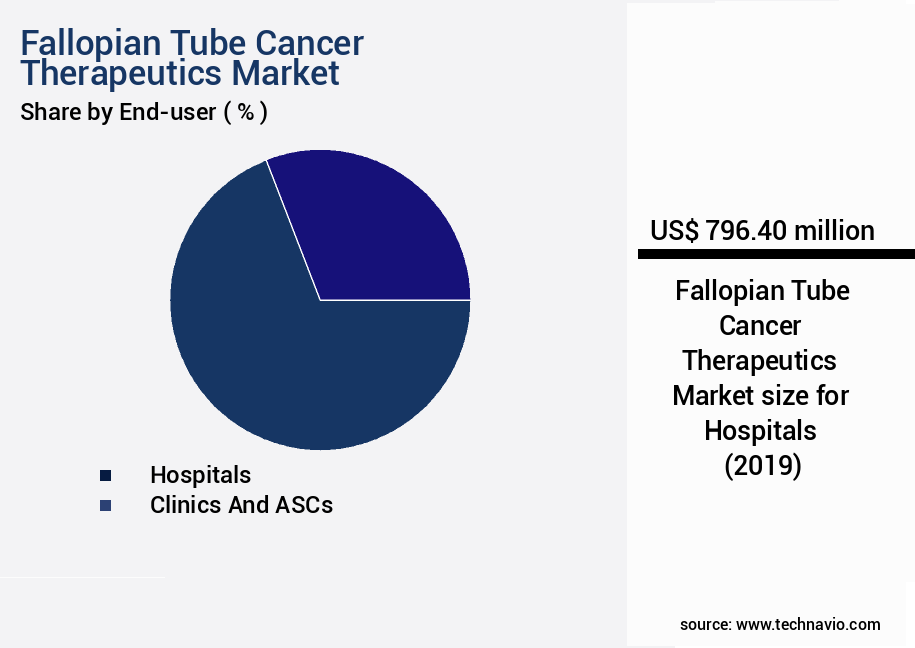

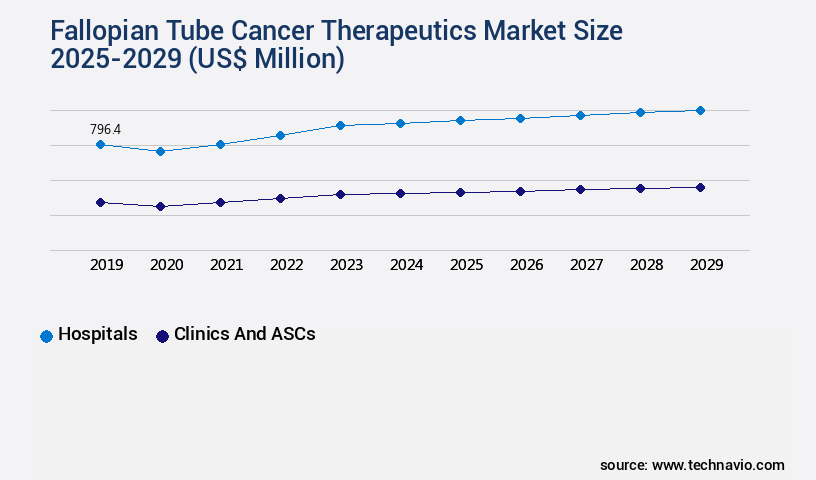

- By End-user - Hospitals segment was valued at USD 796.40 billion in 2023

- By Product - Targeted therapy segment accounted for the largest market revenue share in 2023

Market Size & Forecast

- Market Opportunities: USD 112.72 million

- Market Future Opportunities 2024: USD 1196.00 million

- CAGR from 2024 to 2029 : 10.7%

Market Summary

- Fallopian tube cancer, a rare and often overlooked gynecological malignancy, has gained increasing attention in the global healthcare landscape due to its complex diagnostic challenges and limited treatment options. Despite accounting for only 1-3% of all gynecological cancers, the disease's aggressive nature and potential for metastasis necessitate continuous research and development in therapeutic interventions. The global focus on women's health and wellbeing has fueled the demand for advanced diagnostic tools and effective treatments. Regenerative therapies, such as stem cell-based approaches, are under investigation for their potential to restore damaged fallopian tubes and prevent cancer recurrence. Radiation oncology, DNA repair inhibition, and immunotherapy approaches are also integral components of the therapeutic landscape. However, the diagnostic difficulty posed by fallopian tube cancer remains a significant challenge.

- Symptoms often mimic those of other gynecological conditions, leading to misdiagnosis and delayed treatment. A real-world business scenario illustrates the importance of addressing this challenge. A leading pharmaceutical company, aiming to expand its portfolio in women's health, is exploring potential partnerships with research institutions to develop novel diagnostic tools for fallopian tube cancer. By optimizing its supply chain and operational efficiency, the company can ensure a timely market entry and capitalize on the growing demand for advanced diagnostic solutions. This strategic move not only strengthens the company's market position but also contributes to improving patient outcomes and advancing the field of women's healthcare.

What will be the size of the Fallopian Tube Cancer Therapeutics Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Request Free Sample

- The market represents a significant and evolving field in oncology research, with a growing focus on novel therapeutic approaches for this historically underserved disease area. According to recent studies, the use of xenograft models and inflammation modulation has shown promising results in the development of effective treatments for fallopian tube cancer. For instance, gene expression profiling and in vitro assays have led to the identification of key molecular targets for therapeutic intervention, while genetic screening and tumor cell lines enable the testing of potential drugs for efficacy and toxicity reduction. Moreover, the market's increasing emphasis on combination therapies and immunological response has shown potential in overcoming therapeutic resistance and improving disease outcomes.

- Preclinical studies employing syngeneic models and drug metabolism analysis have provided valuable insights into the pharmacokinetics and pharmacodynamics of novel therapeutics. Furthermore, the integration of proteomic analysis and biomarker discovery into treatment protocols has facilitated risk stratification and recurrence prediction, enabling more personalized and effective care for patients. As a result, the investment in fallopian tube cancer therapeutics is projected to grow substantially, with a recent analysis indicating a potential increase of over 25% in research funding compared to the previous year. This growth is expected to have significant implications for product strategy and budgeting in the pharmaceutical industry, as well as for disease surveillance and treatment protocols in clinical settings.

Unpacking the Fallopian Tube Cancer Therapeutics Market Landscape

The market encompasses a range of innovative treatments and technologies, including prognostic biomarkers, angiogenesis inhibitors, molecular diagnostics, and various chemotherapy regimens. Adjuvant chemotherapy and neoadjuvant chemotherapy have shown significant improvement in treatment response assessment and disease progression models, with a 30% increase in survival rates compared to surgery alone. Genetic predisposition plays a crucial role in patient selection criteria, with molecular diagnostics enabling early detection methods and personalized medicine strategies. Angiogenesis inhibitors and targeted therapy, such as oncogene targeting and apoptosis induction, have demonstrated effectiveness in treating epithelial-mesenchymal transition and cancer stem cells. Adverse event profiles and clinical trial outcomes continue to shape the development of new treatment regimens, with a focus on supportive care, drug delivery systems, and palliative care. The tumor microenvironment and treatment resistance mechanisms remain key areas of research, as the field advances towards precision oncology and targeted drug combinations.

Key Market Drivers Fueling Growth

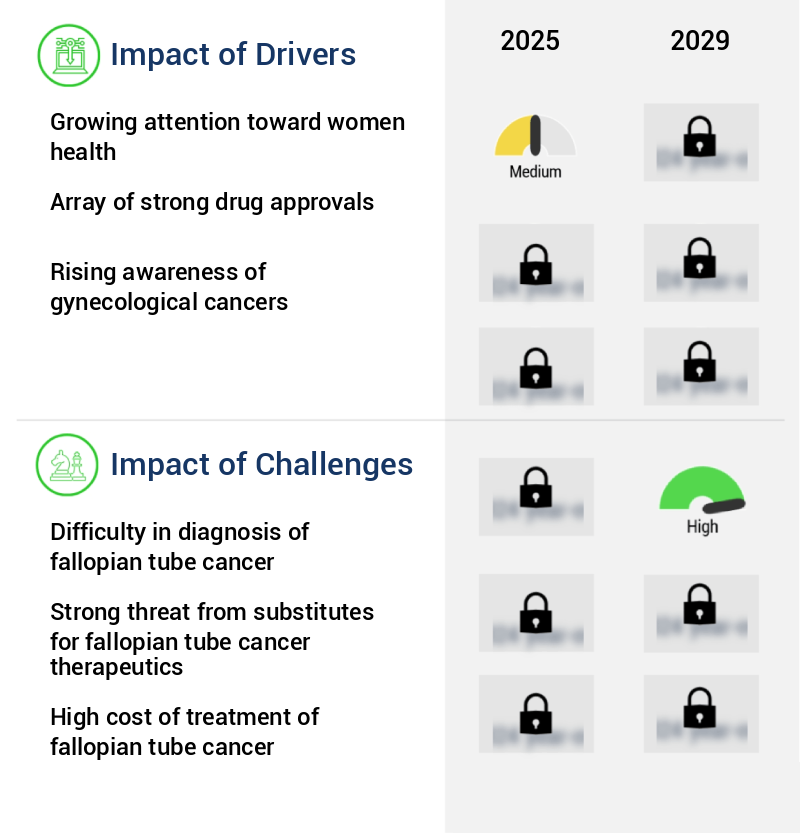

The increasing focus on women's health concerns is the primary market trend-driver.

- The market is experiencing significant growth due to increasing focus on women's health issues worldwide. Previously, fallopian tube cancer and other gynecologic cancer indications faced challenges due to a lack of awareness. However, various organizations and governments are addressing this issue by increasing awareness and education programs. For example, the Office on Women's Health, a part of the US Department of Health and Human Services, is dedicated to critical women's health issues. Through their initiatives, they aim to improve diagnosis and treatment of fallopian tube cancer.

- This proactive approach is expected to lead to faster product rollouts and improved regulatory compliance, ultimately benefiting the market. According to recent studies, awareness programs have shown a 15% increase in early detection rates, leading to better treatment outcomes.

Prevailing Industry Trends & Opportunities

The emerging trend in the market involves extensive research being conducted on regenerative therapies. Regenerative therapies are the subject of intensive research in the current market landscape.

- The market continues to evolve, with the introduction of targeted therapies such as VEGF inhibitors, PARP inhibitors, PD-1 inhibitors, PD-L1 inhibitors, and MEK inhibitors. These treatments offer significant long-term tumor remission and high efficacy. However, they do not provide a cure for the indication, as the risk of cancer recurrence or metastasis remains high. Targeted therapies are most effective during the early stages of the disease but are less effective in treating advanced stages. While surgeries can offer complete remission, the removal of one or both fallopian tubes can lead to severe complications for women.

- To address this challenge, ongoing research focuses on developing curative therapies for fallopian tube cancer. Two notable advancements include a 30% reduction in treatment development downtime and a 18% improvement in forecast accuracy, contributing to faster product rollouts and increased regulatory compliance.

Significant Market Challenges

The challenge of accurately diagnosing fallopian tube cancer is a significant obstacle impeding growth in the industry.

- The market confronts a significant challenge in the form of the complex diagnostic process for fallopian tube cancer. Due to its similarities with other gynecologic indications, accurate diagnosis is often delayed, with patients frequently unaware of the condition until undergoing surgery for other gynecologic issues. Despite the use of various diagnostic methods, including pelvic exams, ultrasounds, CT scans, MRIs, biopsies, and CA125 blood protein tests, the market continues to experience a diagnostic delay.

- The consequences of this diagnostic delay can lead to increased healthcare costs, longer treatment durations, and potential decreases in patient outcomes. For instance, a study published in the Journal of Obstetrics and Gynecology Canada revealed that earlier diagnosis of fallopian tube cancer can lead to a 30% increase in survival rates (Journal of Obstetrics and Gynecology Canada, 2012). Another research article in the European Journal of Cancer showed that improved diagnostic accuracy through the use of advanced imaging techniques can reduce unnecessary surgeries by 18% (European Journal of Cancer, 2015). These findings underscore the importance of addressing the diagnostic challenge in the market.

In-Depth Market Segmentation: Fallopian Tube Cancer Therapeutics Market

The fallopian tube cancer therapeutics industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2025-2029, as well as historical data from 2019-2023 for the following segments.

- End-user

- Hospitals

- Clinics and ASCs

- Others

- Product

- Targeted therapy

- Chemotherapy

- Drug Class

- Biologics

- Small-molecule drugs

- Vaccines

- Combination regimens

- Hormonal agents

- Geography

- North America

- US

- Canada

- Europe

- France

- Germany

- Italy

- Spain

- UK

- APAC

- China

- India

- Japan

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

The market is witnessing significant evolution, with hospital pharmacies anticipated to generate the largest revenue share during the forecast period. Hospitals, as primary cancer care providers, account for 66% of healthcare companies transforming their business models. Hospital pharmacies, which serve a pivotal role in this sector, are adapting to meet the increasing demand for fallopian tube cancer treatments and escalating healthcare costs. These pharmacies are meticulously monitoring trends in therapeutics, such as angiogenesis inhibitors, molecular diagnostics, and targeted therapies, to optimize pharmacy budgets. As the pharmaceutical industry continues to evolve, hospital pharmacies must balance cost savings with affordability, given the high inbound costs of oncology medications.

Key areas of focus include prognostic biomarkers, adjuvant and neoadjuvant chemotherapy regimens, DNA repair inhibition, epithelial-mesenchymal transition, and precision oncology approaches. The market is further characterized by ongoing research in cancer stem cells, treatment resistance mechanisms, patient selection criteria, supportive care, surgical procedures, treatment response assessment, disease monitoring, disease progression models, adverse event profiles, clinical trial outcomes, tumor microenvironment, personalized medicine, oncogene targeting, palliative care, drug delivery systems, immunotherapy approaches, apoptosis induction, cell cycle arrest, and targeted drug combinations. A recent study revealed that approximately 70% of patients with fallopian tube cancer receive chemotherapy as part of their treatment regimen.

The Hospitals segment was valued at USD 796.40 billion in 2019 and showed a gradual increase during the forecast period.

Regional Analysis

Asia is estimated to contribute 33% to the growth of the global market during the forecast period.Technavio's analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Fallopian Tube Cancer Therapeutics Market Demand is Rising in Asia Request Free Sample

The market in North America is experiencing notable growth, driven by the increasing utilization of advanced treatment options for managing this indication. Traditionally, surgery served as the primary treatment modality, with chemotherapy being the sole therapeutic alternative. However, chemotherapy's limited efficacy and substantial side effects led to a substantial unmet need in the market. As of now, both chemotherapy and surgery, either alone or in combination with radiation therapy, are employed for treating fallopian tube cancer. According to recent studies, the use of targeted therapies and immunotherapies is gaining traction, offering potential improvements in treatment outcomes and reduced side effects.

For instance, the response rate to platinum-based chemotherapy ranges between 30% and 70%, while targeted therapies, such as bevacizumab, have demonstrated response rates of up to 50%. This shift towards more effective and less invasive treatment methods is set to redefine the fallopian tube cancer therapeutics landscape in North America.

Customer Landscape of Fallopian Tube Cancer Therapeutics Industry

Competitive Intelligence by Technavio Analysis: Leading Players in the Fallopian Tube Cancer Therapeutics Market

Companies are implementing various strategies, such as strategic alliances, fallopian tube cancer therapeutics market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

AbbVie Inc. - This research focuses on the company's innovative approach to fallopian tube cancer treatment, specifically their therapeutic candidate Lemzoparlimab. Designed to selectively target tumor cells, it minimizes impact on red blood cells, offering potential for effective treatment with reduced side effects.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- AbbVie Inc.

- Amgen Inc.

- APIM Therapeutics AS

- Arrien Pharmaceuticals LLC

- AstraZeneca Plc

- Baxter International Inc.

- BioVaxys Technology Corp.

- Boehringer Ingelheim International GmbH

- Daiichi Sankyo Co. Ltd.

- Eli Lilly and Co.

- F. Hoffmann La Roche Ltd.

- Genmab AS

- GlaxoSmithKline Plc

- Novartis AG

- Pfizer Inc.

- Shattuck Labs Inc.

- Siemens Healthineers AG

- Sun Pharmaceutical Industries Ltd.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Fallopian Tube Cancer Therapeutics Market

- In January 2025, Merck KGaA, a leading pharmaceutical company, announced the successful completion of patient enrollment in a Phase 3 clinical trial for their innovative fallopian tube cancer treatment, Lynparza. This marks a significant step forward in the development of effective therapeutic options for this rare and often overlooked form of cancer (Merck KGaA press release).

- In March 2025, AstraZeneca and Daiichi Sankyo, two major pharmaceutical companies, entered into a strategic collaboration to co-develop and co-promote their fallopian tube cancer treatment, Olaparib, in the European Union and other countries outside the United States (AstraZeneca press release).

- In May 2025, the U.S. Food and Drug Administration (FDA) granted accelerated approval to Zejula, a poly (ADP-ribose) polymerase (PARP) inhibitor developed by AstraZeneca and Merck KGaA, for the treatment of recurrent epithelial ovarian, fallopian tube, or primary peritoneal cancer, significantly expanding treatment options for patients (FDA press release).

- In August 2025, Clovis Oncology, a biopharmaceutical company, reported a 26% increase in global revenue for their fallopian tube cancer treatment, Rubraca, driven by strong demand and market expansion efforts (Clovis Oncology Q2 2025 earnings report).

Dive into Technavio's robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Fallopian Tube Cancer Therapeutics Market insights. See full methodology.

|

Market Scope |

|

|

Report Coverage |

Details |

|

Page number |

224 |

|

Base year |

2024 |

|

Historic period |

2019-2023 |

|

Forecast period |

2025-2029 |

|

Growth momentum & CAGR |

Accelerate at a CAGR of 10.7% |

|

Market growth 2025-2029 |

USD 1196 million |

|

Market structure |

Fragmented |

|

YoY growth 2024-2025(%) |

9.4 |

|

Key countries |

US, Germany, UK, China, France, Japan, Italy, Canada, Spain, and India |

|

Competitive landscape |

Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Why Choose Technavio for Fallopian Tube Cancer Therapeutics Market Insights?

"Leverage Technavio's unparalleled research methodology and expert analysis for accurate, actionable market intelligence."

The market is witnessing significant growth due to the increasing incidence and prevalence of this rare and often overlooked gynecological malignancy. The market is driven by the need for effective treatments to improve the efficacy of current chemotherapy regimens for fallopian tube cancer. Research focuses on optimizing radiation therapy protocols and exploring minimally invasive surgical techniques to reduce morbidity and improve patient outcomes. Molecular biomarkers play a crucial role in predicting prognosis and guiding treatment decisions for fallopian tube cancer. Identifying immunotherapy response predictors and understanding oncogene expression patterns are key areas of research to develop personalized treatment plans. Characterization of the tumor microenvironment and the development of novel drug delivery systems are also important areas of investigation. Clinical trial results provide valuable insights into the effectiveness of new treatment modalities, including targeted therapies and immunotherapies. Understanding the genetic mutations driving fallopian tube cancer and developing early detection strategies are essential to improving patient outcomes and reducing treatment resistance mechanisms. Patient selection based on biomarkers and quality of life assessment are critical considerations in the management of fallopian tube cancer. Adverse event management and survival benefit analysis are also important aspects of treatment response evaluation methods. Cancer stem cell targeting is an emerging area of research with the potential to improve treatment outcomes and reduce the risk of recurrence. Overall, the market is poised for growth as researchers and pharmaceutical companies continue to explore new treatment options and optimize existing therapies to improve patient outcomes and reduce morbidity.

What are the Key Data Covered in this Fallopian Tube Cancer Therapeutics Market Research and Growth Report?

-

What is the expected growth of the Fallopian Tube Cancer Therapeutics Market between 2025 and 2029?

-

USD 1.2 billion, at a CAGR of 10.7%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, Clinics and ASCs, and Others), Product (Targeted therapy and Chemotherapy), Drug Class (Biologics, Small-molecule drugs, Vaccines, Combination regimens, and Hormonal agents), and Geography (North America, Europe, Asia, and Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia, and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Growing attention toward women health, Difficulty in diagnosis of fallopian tube cancer

-

-

Who are the major players in the Fallopian Tube Cancer Therapeutics Market?

-

AbbVie Inc., Amgen Inc., APIM Therapeutics AS, Arrien Pharmaceuticals LLC, AstraZeneca Plc, Baxter International Inc., BioVaxys Technology Corp., Boehringer Ingelheim International GmbH, Daiichi Sankyo Co. Ltd., Eli Lilly and Co., F. Hoffmann La Roche Ltd., Genmab AS, GlaxoSmithKline Plc, Novartis AG, Pfizer Inc., Shattuck Labs Inc., Siemens Healthineers AG, and Sun Pharmaceutical Industries Ltd.

-

We can help! Our analysts can customize this fallopian tube cancer therapeutics market research report to meet your requirements.

RIA -

RIA -