Femoral Head Prostheses Market Size 2026-2030

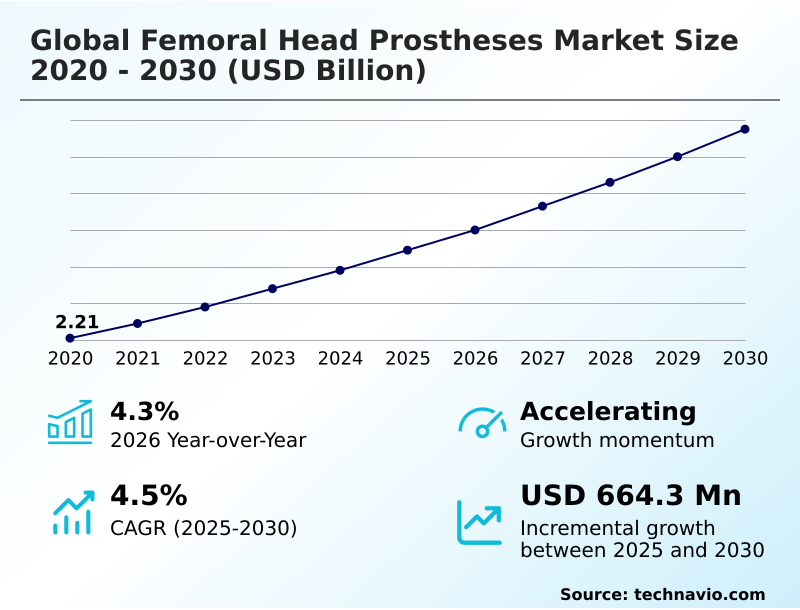

The femoral head prostheses market size is valued to increase by USD 664.3 million, at a CAGR of 4.5% from 2025 to 2030. Increasing prevalence of osteoarthritis, rheumatoid arthritis, and trauma will drive the femoral head prostheses market.

Major Market Trends & Insights

- North America dominated the market and accounted for a 44.5% growth during the forecast period.

- By End-user - Hospitals segment was valued at USD 1.35 billion in 2024

- By Material - Ceramic femoral head prostheses segment accounted for the largest market revenue share in 2024

Market Size & Forecast

- Market Opportunities: USD 1.14 billion

- Market Future Opportunities: USD 664.3 million

- CAGR from 2025 to 2030 : 4.5%

Market Summary

- The femoral head prostheses market is centered on restoring mobility for patients with degenerative or trauma-induced hip conditions. Growth is fueled by an aging global population and a higher incidence of osteoarthritis, driving demand for hip arthroplasty. Key advancements in orthopedic implants focus on improving implant longevity and biocompatibility, with materials like biolox delta ceramics and oxidized zirconium becoming standard.

- The industry is also seeing a shift toward surgical precision through robotic-assisted hip replacement and computer-assisted navigation. For instance, a hospital system might adopt a specific modular femoral head system based on data showing it reduces revision total hip arthroplasty rates, aligning clinical excellence with long-term financial strategy.

- However, the high cost of procedures and the need for skilled surgeons present considerable barriers to access, particularly in emerging economies. Balancing innovation in joint biomechanics with cost-containment pressures from reimbursement policies remains a central dynamic shaping the market's trajectory.

What will be the Size of the Femoral Head Prostheses Market during the forecast period?

Get Key Insights on Market Forecast (PDF) Get Free Sample

How is the Femoral Head Prostheses Market Segmented?

The femoral head prostheses industry research report provides comprehensive data (region-wise segment analysis), with forecasts and estimates in "USD million" for the period 2026-2030, as well as historical data from 2020-2024 for the following segments.

- End-user

- Hospitals

- ASCs

- Speciality clinics

- Research and academic institution

- Material

- Ceramic femoral head prostheses

- Metal femoral head prostheses

- Ceramicised metal femoral head prostheses

- Product type

- Modular femoral heads

- Monoblock femoral heads

- Geography

- North America

- US

- Canada

- Mexico

- Europe

- Germany

- UK

- France

- Asia

- Rest of World (ROW)

- North America

By End-user Insights

The hospitals segment is estimated to witness significant growth during the forecast period.

The global femoral head prostheses market is segmented by end-user, including hospitals, Ambulatory Surgical Centers (ASCs), specialty clinics, and research institutions. Hospitals remain the primary setting for complex procedures like revision total hip arthroplasty, where advanced orthopedic implants are crucial.

These facilities leverage sophisticated technologies to manage conditions stemming from avascular necrosis and improve implant longevity. A key focus is on minimizing postoperative complications through enhanced surgical precision.

For instance, the adoption of advanced intraoperative tools has been shown to reduce the risk of implant malpositioning by over 15%, directly impacting joint biomechanics and patient recovery.

This pursuit of superior clinical efficacy reinforces the hospital segment's role in driving demand for premium femoral head prostheses, especially those designed for complex reconstruction and improved biocompatibility.

The Hospitals segment was valued at USD 1.35 billion in 2024 and showed a gradual increase during the forecast period.

Regional Analysis

North America is estimated to contribute 44.5% to the growth of the global market during the forecast period.Technavio’s analysts have elaborately explained the regional trends and drivers that shape the market during the forecast period.

See How Femoral Head Prostheses Market Demand is Rising in North America Get Free Sample

The geographic landscape of the global femoral head prostheses market is led by North America, which accounts for approximately 44.5% of the market's incremental growth, driven by high adoption rates of advanced surgical technologies and favorable reimbursement policies.

Europe follows, with a market characterized by stringent Medical Device Regulation (MDR) standards and a focus on long-term clinical data, contributing to its 4.9% CAGR.

The Asia-Pacific region is the fastest-growing market, propelled by rising healthcare expenditure, an aging population, and government initiatives promoting access to hip replacement surgery.

The Rest of the World (ROW), including South America and the Middle East, shows steady growth as healthcare infrastructure and access to orthopedic care improve.

This regional diversification requires manufacturers to navigate different regulatory pathways and pricing structures to capitalize on global demand.

Market Dynamics

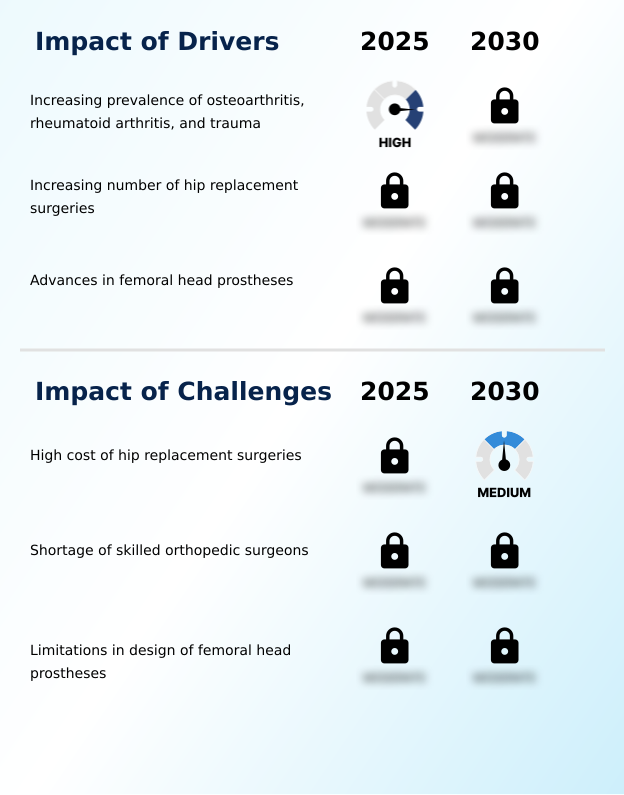

Our researchers analyzed the data with 2025 as the base year, along with the key drivers, trends, and challenges. A holistic analysis of drivers will help companies refine their marketing strategies to gain a competitive advantage.

- Strategic decision-making in the global femoral head prostheses market 2026-2030 requires a nuanced understanding of implant performance and surgical technique. The debate over ceramic versus metal femoral head longevity continues, with data on the wear characteristics of ceramic-on-polyethylene showing superior long-term performance. However, the cost-effectiveness of CoCr femoral heads ensures their continued use in specific patient populations.

- The benefits of direct anterior approach hip replacement, such as faster recovery, are driving its adoption, influencing implant design. Simultaneously, the role of modularity in revision hip arthroplasty is critical for addressing complex cases, though it introduces challenges in managing metal ion release from implants and preventing trunnionosis in modular hip implants.

- Surgeons must also weigh the impact of femoral head size on dislocation risk against the desire for greater motion. The choice between oxidized zirconium vs ceramic femoral heads is another key consideration, balancing fracture resistance with wear properties. For high-risk patients, dual mobility systems for high-risk patients are becoming a standard to enhance stability.

- Improving outcomes in total hip arthroplasty depends on optimizing implant fit with modular systems and a deep understanding of the biocompatibility of different hip implant materials. Robotic surgery accuracy in hip replacement is transforming the field, while advances in femoral stem design integration promise better fixation.

- Ultimately, the economic impact of revision hip surgery and the challenges of periprosthetic joint infection push the industry toward more durable, long-term performance of hip prostheses, all while navigating complex regulatory pathways for orthopedic implants. Femoral head options for young active patients, in particular, must balance durability with high functional demands.

What are the key market drivers leading to the rise in the adoption of Femoral Head Prostheses Industry?

- The market is primarily driven by the increasing global prevalence of conditions such as osteoarthritis, rheumatoid arthritis, and trauma-related hip injuries.

- The primary driver for the global femoral head prostheses market 2026-2030 is the escalating volume of hip replacement procedures, fueled by the rising prevalence of osteoarthritis treatment needs in an aging global population.

- The demand for primary total hip arthroplasties is on a trajectory to more than double over the next two decades in certain key markets.

- This surge is supported by advancements in minimally invasive surgical techniques, which expand the eligible patient pool to younger, more active individuals. Innovations in materials, particularly the shift to ceramic-on-polyethylene bearings, address the critical need for durability.

- These advanced materials have demonstrated wear rates up to 90% lower than previous-generation options. The direct correlation between procedural volume and implant demand makes demographic trends and technological advances in orthopedic surgery fundamental growth catalysts.

What are the market trends shaping the Femoral Head Prostheses Industry?

- A key market trend is the increasing focus on robotic-assisted hip replacement surgeries. This is driven by the demand for greater precision and improved patient outcomes.

- The market is experiencing a significant shift with the rising adoption of robotic-assisted surgery and the increasing use of dual mobility constructs. These trends are driven by a clinical focus on enhancing surgical precision and reducing postoperative complications. For instance, robotic platforms have been shown to decrease implant placement errors by over 15%, directly contributing to better long-term implant survivorship.

- Concurrently, the migration of procedures to ambulatory surgical centers is accelerating, with these facilities now accounting for nearly 30% of all primary hip replacements in some regions. This transition demands streamlined, efficient implant systems that support faster operating room turnover.

- The market is also seeing a focus on head-neck taper junction integrity to minimize wear and improve joint stability restoration, further pushing innovation in implant design and material science.

What challenges does the Femoral Head Prostheses Industry face during its growth?

- A significant challenge affecting industry growth is the high cost associated with hip replacement surgeries, which can limit patient access in various regions.

- Key challenges constraining market growth include the high cost of procedures and limitations in implant design. In many developed nations, the total cost of a hip replacement can be up to ten times higher than in medical tourism destinations, limiting access for uninsured or underinsured patients.

- This price sensitivity is amplified by the influence of group purchasing organizations that negotiate aggressively on behalf of healthcare providers. Furthermore, the industry faces challenges related to leg length discrepancy and other postoperative issues stemming from suboptimal implant fit. Even with advanced preoperative planning, achieving perfect anatomical replication remains difficult.

- A shortage of skilled surgeons also creates a bottleneck, with patient wait times in some public health systems exceeding 4.5 months, artificially capping the number of procedures performed and restricting market expansion.

Exclusive Technavio Analysis on Customer Landscape

The femoral head prostheses market forecasting report includes the adoption lifecycle of the market, covering from the innovator’s stage to the laggard’s stage. It focuses on adoption rates in different regions based on penetration. Furthermore, the femoral head prostheses market report also includes key purchase criteria and drivers of price sensitivity to help companies evaluate and develop their market growth analysis strategies.

Customer Landscape of Femoral Head Prostheses Industry

Competitive Landscape

Companies are implementing various strategies, such as strategic alliances, femoral head prostheses market forecast, partnerships, mergers and acquisitions, geographical expansion, and product/service launches, to enhance their presence in the industry.

Altimed JSC - Offerings include advanced orthopedic implants, featuring a range of ceramic and metallic femoral head prostheses engineered for reconstructive hip arthroplasty.

The industry research and growth report includes detailed analyses of the competitive landscape of the market and information about key companies, including:

- Altimed JSC

- Amplitude SAS

- Corentec Co. Ltd.

- Corin Group Plc

- DePuy Synthes

- Elite Surgical Pvt. Ltd.

- Exactech Inc.

- Gruppo Bioimpianti Srl

- Lepu Medical Co. Ltd.

- Medacta International SA

- Meril Life Sciences Pvt. Ltd.

- Normmed Medikal ve

- Ortho Development Corp.

- Smith and Nephew plc

- Surgival Co.

- United Orthopedic Corp.

- Zimed Healthcare Ltd.

- Zimmer Biomet Holdings Inc.

Qualitative and quantitative analysis of companies has been conducted to help clients understand the wider business environment as well as the strengths and weaknesses of key industry players. Data is qualitatively analyzed to categorize companies as pure play, category-focused, industry-focused, and diversified; it is quantitatively analyzed to categorize companies as dominant, leading, strong, tentative, and weak.

Recent Development and News in Femoral head prostheses market

- In May, 2025, Stryker reported a 12.7% year-over-year increase in its first-quarter hip sales, reflecting strong demand in the orthopedic market.

- In March, 2025, Stryker showcased its Mako 4 system, introducing new capabilities for the Mako Total Hip application, including a first-to-market feature for robotic hip revision surgery.

- In March, 2025, the U.S. FDA granted compassionate use approval for the Reverse Hip Replacement System developed by Hip Innovation Technology, offering a new solution for complex hip stability issues.

- In December, 2024, Smith and Nephew plc received FDA 510(k) clearance for its CORIOGRAPH Pre-Op Planning and Modeling Services, expanding its digital ecosystem for total hip arthroplasty.

Dive into Technavio’s robust research methodology, blending expert interviews, extensive data synthesis, and validated models for unparalleled Femoral Head Prostheses Market insights. See full methodology.

| Market Scope | |

|---|---|

| Page number | 293 |

| Base year | 2025 |

| Historic period | 2020-2024 |

| Forecast period | 2026-2030 |

| Growth momentum & CAGR | Accelerate at a CAGR of 4.5% |

| Market growth 2026-2030 | USD 664.3 million |

| Market structure | Fragmented |

| YoY growth 2025-2026(%) | 4.3% |

| Key countries | US, Canada, Mexico, Germany, UK, France, Italy, Spain, The Netherlands, China, India, Japan, South Korea, Thailand, Indonesia, Brazil, Saudi Arabia, UAE, Turkey, South Africa, Israel, Argentina and Colombia |

| Competitive landscape | Leading Companies, Market Positioning of Companies, Competitive Strategies, and Industry Risks |

Research Analyst Overview

- The femoral head prostheses market provides critical solutions for restoring joint biomechanics through advanced orthopedic implants. The core of this market lies in hip arthroplasty, a procedure essential for patients suffering from conditions like avascular necrosis or severe osteoarthritis.

- Key components include the femoral head prosthesis itself, the femoral stem, and the acetabular cup system, which work together to replicate the natural articular surface. Innovations are centered on implant longevity and biocompatibility, with materials like biolox delta ceramics and cobalt-chromium alloys dominating. Modular femoral head systems offer surgical flexibility, but also introduce risks such as trunnionosis and aseptic loosening.

- A major industry shift involves integrating robotic-assisted hip replacement, which has become a significant capital expenditure decision for hospital boards. Adoption of these platforms has been linked to procedural volume increases of over 20% in specialized centers, demonstrating a clear return on investment.

- This trend highlights the move toward technology-driven precision to improve outcomes, reduce osteolysis, and prevent periprosthetic joint infection, ultimately enhancing the efficacy of hip replacement surgery.

What are the Key Data Covered in this Femoral Head Prostheses Market Research and Growth Report?

-

What is the expected growth of the Femoral Head Prostheses Market between 2026 and 2030?

-

USD 664.3 million, at a CAGR of 4.5%

-

-

What segmentation does the market report cover?

-

The report is segmented by End-user (Hospitals, ASCs, Speciality clinics, and Research and academic institution), Material (Ceramic femoral head prostheses, Metal femoral head prostheses, and Ceramicised metal femoral head prostheses), Product Type (Modular femoral heads, and Monoblock femoral heads) and Geography (North America, Europe, Asia, Rest of World (ROW))

-

-

Which regions are analyzed in the report?

-

North America, Europe, Asia and Rest of World (ROW)

-

-

What are the key growth drivers and market challenges?

-

Increasing prevalence of osteoarthritis, rheumatoid arthritis, and trauma, High cost of hip replacement surgeries

-

-

Who are the major players in the Femoral Head Prostheses Market?

-

Altimed JSC, Amplitude SAS, Corentec Co. Ltd., Corin Group Plc, DePuy Synthes, Elite Surgical Pvt. Ltd., Exactech Inc., Gruppo Bioimpianti Srl, Lepu Medical Co. Ltd., Medacta International SA, Meril Life Sciences Pvt. Ltd., Normmed Medikal ve, Ortho Development Corp., Smith and Nephew plc, Surgival Co., United Orthopedic Corp., Zimed Healthcare Ltd. and Zimmer Biomet Holdings Inc.

-

Market Research Insights

- Market dynamics are shaped by intense competition and evolving buyer behavior, where group purchasing organizations and large hospital networks exert significant pricing pressure. This environment compels manufacturers to demonstrate clear clinical efficacy and economic value. For example, systems that streamline procedures can reduce operating room time by over 15%, a critical metric for ambulatory surgical centers.

- Furthermore, the adoption of patient-specific implants and advanced preoperative planning tools has improved implant survivorship, with some advanced bearings showing a 5% lower revision rate over ten years compared to older technologies.

- As value-based healthcare models become more prevalent, reimbursement policies are increasingly tied to implant performance and the prevention of postoperative complications, forcing a strategic focus on innovations that enhance joint stability restoration and justify investment in premium materials.

We can help! Our analysts can customize this femoral head prostheses market research report to meet your requirements.

RIA -

RIA -